With uncertainty rising, is gold’s bull run far from over?

Introduction & Market Context

Teladoc Health Inc (NYSE:TDOC) released its first quarter 2025 financial results on April 30, revealing continued challenges across its telehealth business. The company’s stock, which has already declined significantly from its 52-week high of $15.21, fell an additional 4.31% in after-hours trading to $6.88 following the announcement.

The quarterly presentation highlighted a 3% year-over-year revenue decline and a significant goodwill impairment charge, while showing divergent performance between its two main business segments. These results come as Teladoc continues to navigate a challenging post-pandemic environment for telehealth services.

Quarterly Performance Highlights

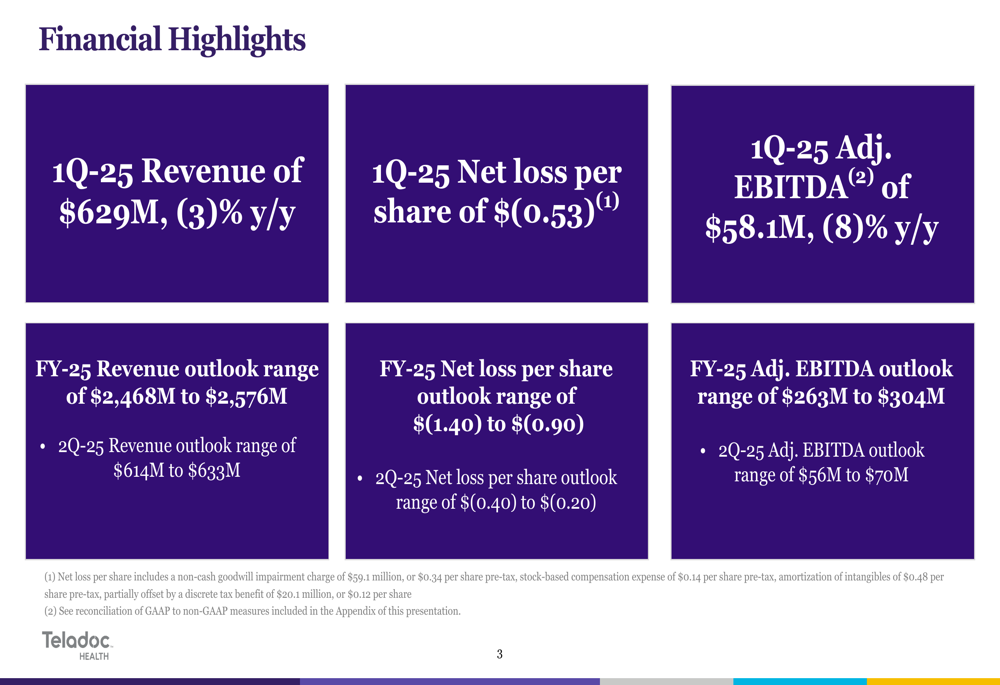

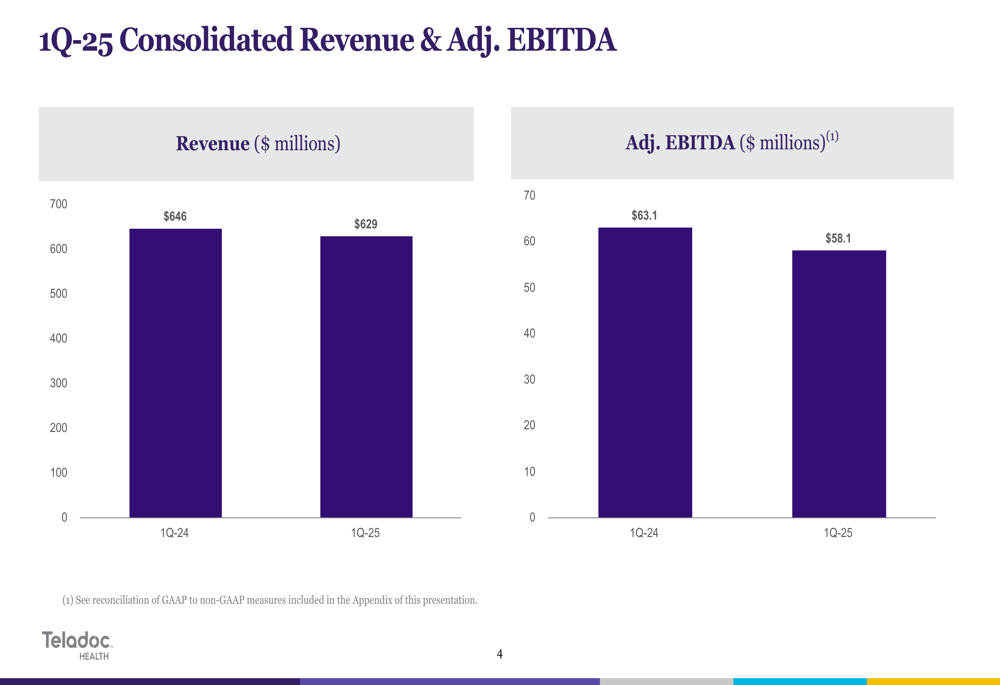

Teladoc reported Q1 2025 revenue of $629 million, representing a 3% decrease compared to the $646 million reported in the same period last year. The company posted a net loss per share of $(0.53), which included a non-cash goodwill impairment charge of $59.1 million, equivalent to $0.34 per share pre-tax. Adjusted EBITDA came in at $58.1 million, down 8% from $63.1 million in Q1 2024.

As shown in the following financial highlights from the company’s presentation:

The consolidated revenue and adjusted EBITDA comparison clearly illustrates the year-over-year decline in both metrics:

Segment Analysis

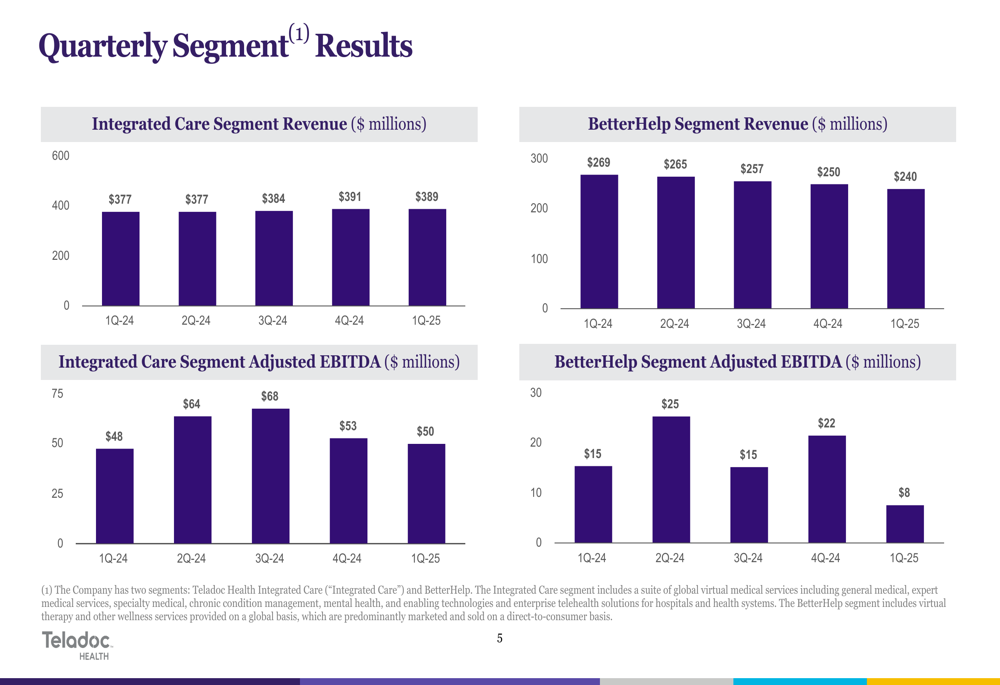

Teladoc’s business performance showed a stark contrast between its two main segments. The Integrated Care segment, which includes virtual healthcare services and chronic condition management, demonstrated relative stability with Q1 2025 revenue of $389 million, a slight increase from $377 million in Q1 2024. However, adjusted EBITDA for this segment declined to $50 million from $48 million a year earlier.

In contrast, the BetterHelp mental health segment continued its downward trend, with revenue falling to $240 million in Q1 2025 from $269 million in Q1 2024. More concerning was the sharp decline in adjusted EBITDA for BetterHelp, which dropped to just $8 million from $15 million a year ago.

The following chart illustrates this divergent segment performance over the past five quarters:

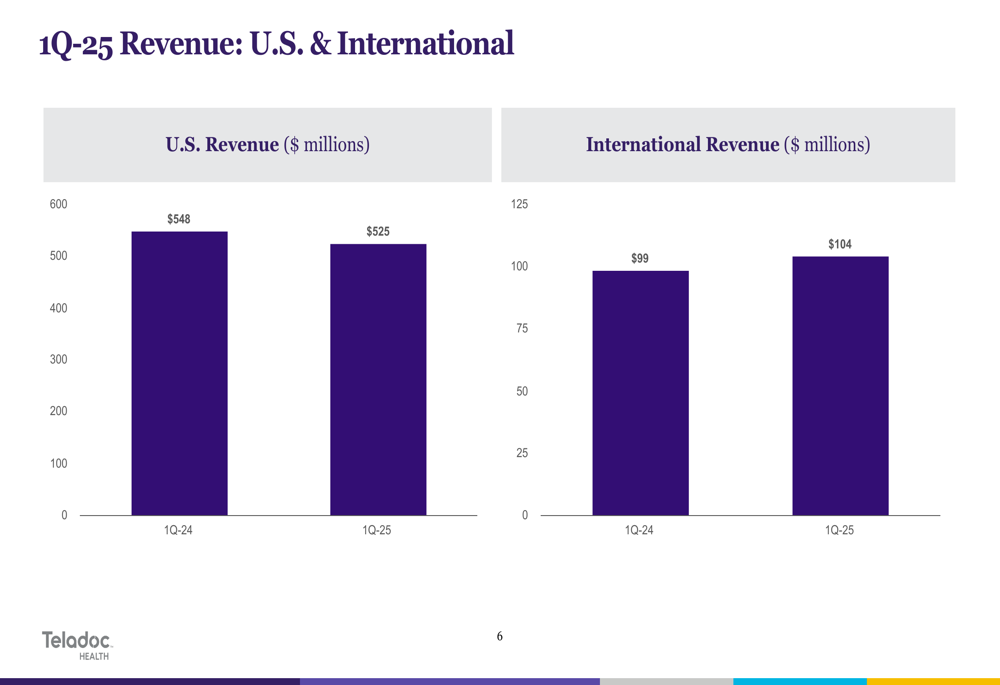

From a geographic perspective, U.S. revenue declined to $525 million in Q1 2025 from $548 million in Q1 2024, while international revenue showed modest growth, increasing to $104 million from $99 million in the prior year period:

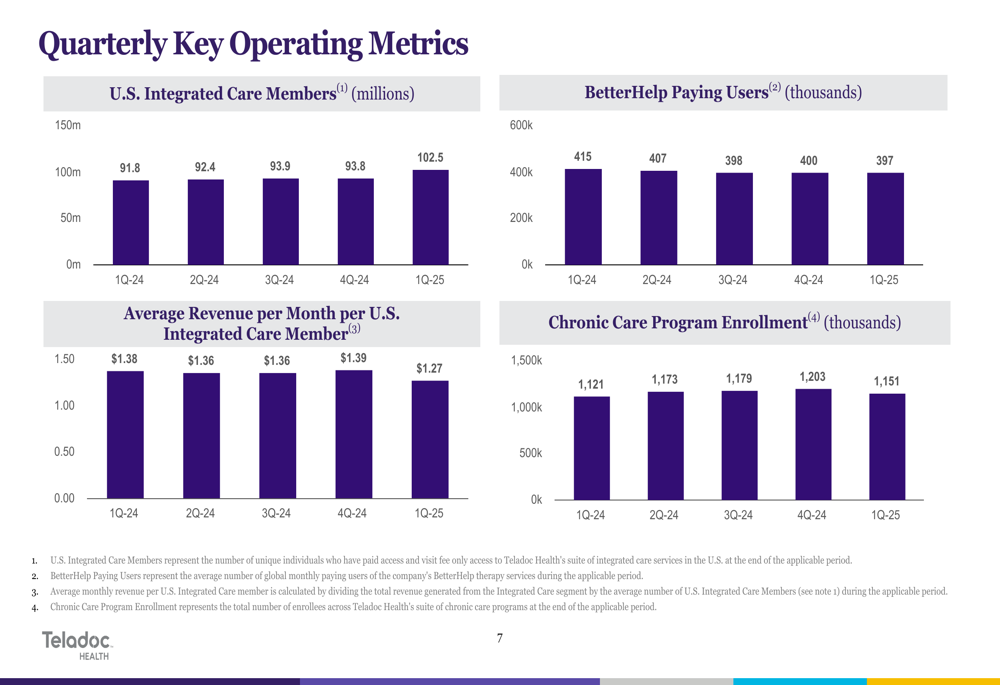

Key Operating Metrics

Despite revenue challenges, Teladoc reported significant growth in its U.S. Integrated Care membership, which increased to 102.5 million in Q1 2025, up 11.7% from 91.8 million in Q1 2024. However, the average revenue per U.S. Integrated Care member per month declined to $1.27 from $1.38 a year earlier.

BetterHelp paying users continued to decline, falling to 397,000 in Q1 2025 from 415,000 in Q1 2024. Chronic Care Program enrollment also showed a slight increase year-over-year but declined sequentially from the previous quarter.

The following chart details these key operating metrics:

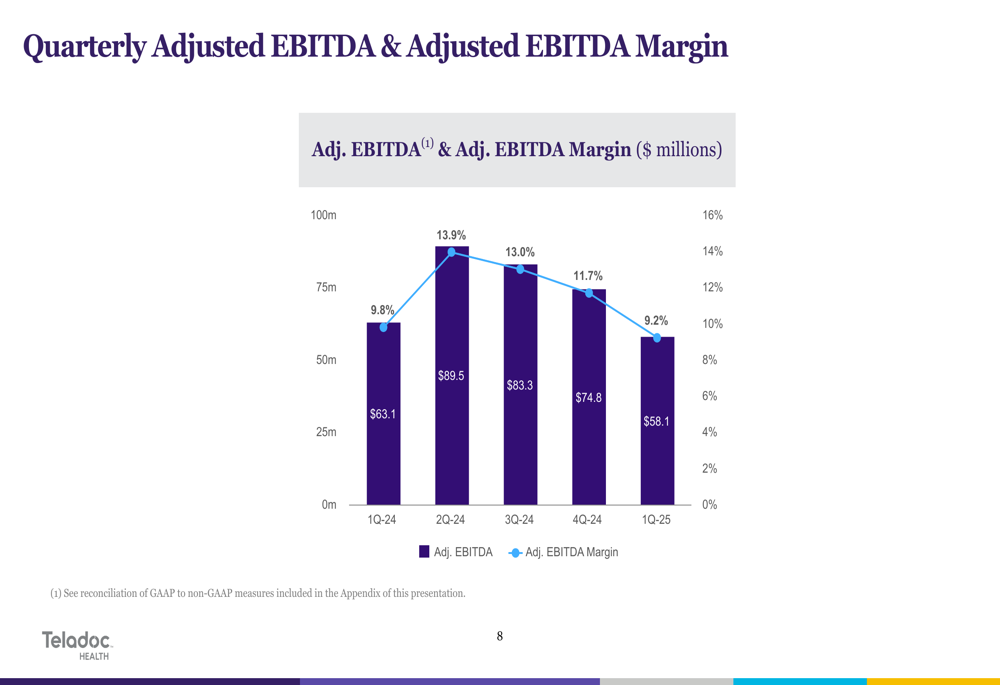

Teladoc’s adjusted EBITDA margin contracted to 9.2% in Q1 2025, down from 9.8% in the same period last year, continuing a downward trend from the peak of 13.9% achieved in Q2 2024:

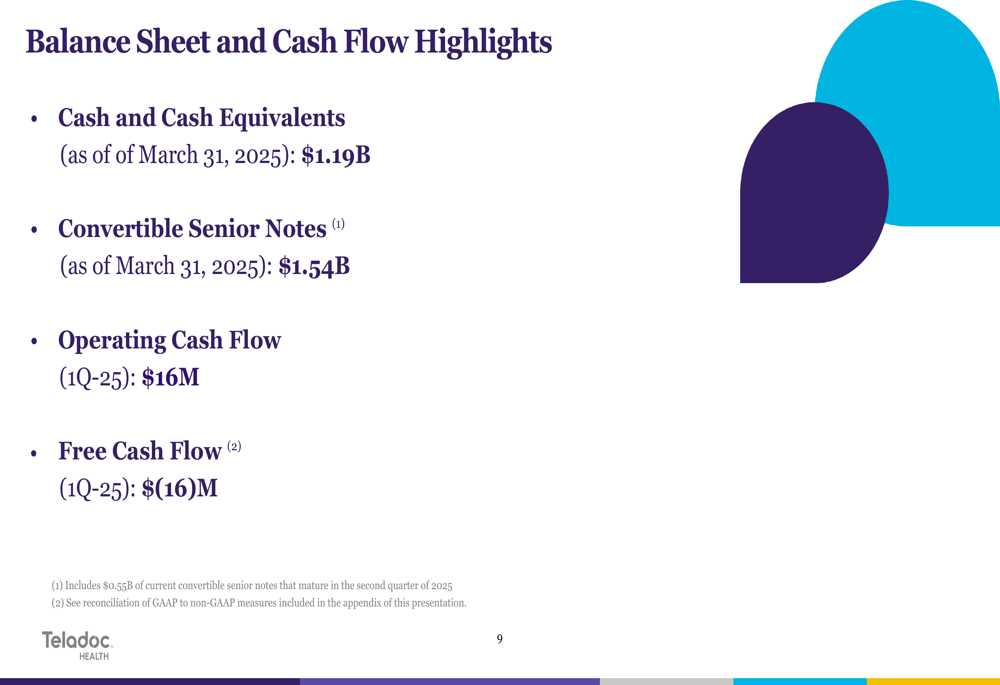

Financial Position and Cash Flow

As of March 31, 2025, Teladoc maintained a strong cash position with $1.19 billion in cash and cash equivalents. The company reported $1.54 billion in convertible senior notes on its balance sheet. Operating cash flow for Q1 2025 was positive at $16 million, but free cash flow was negative at $(16) million, primarily due to capital expenditures and capitalized software development costs totaling $31.6 million.

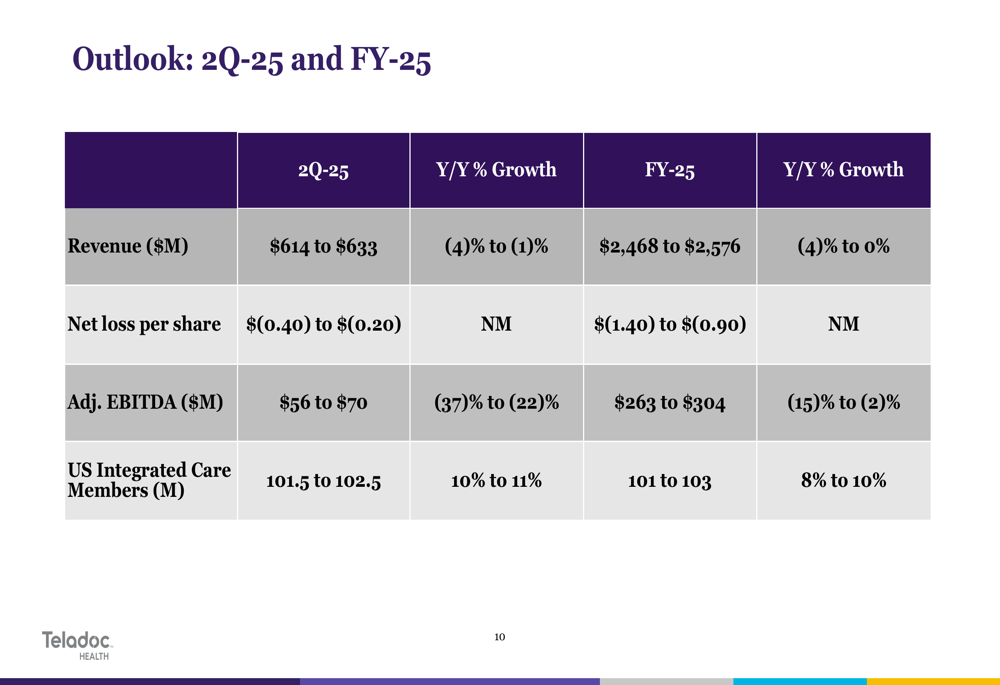

Forward Guidance and Outlook

Teladoc provided guidance for both Q2 2025 and the full year, projecting continued revenue challenges. For Q2 2025, the company expects revenue between $614 million and $633 million, representing a year-over-year decline of 1% to 4%. Full-year 2025 revenue is projected to be between $2,468 million and $2,576 million, ranging from a 4% decline to flat growth compared to 2024.

The company expects adjusted EBITDA for Q2 2025 to be between $56 million and $70 million, representing a significant year-over-year decline of 22% to 37%. For the full year 2025, adjusted EBITDA is projected to be between $263 million and $304 million, a decline of 2% to 15% from 2024.

The detailed outlook is presented in the following chart:

Conclusion

Teladoc’s Q1 2025 results reflect ongoing challenges in the telehealth sector, particularly within its BetterHelp mental health segment. While the company continues to grow its Integrated Care membership base, declining revenue per member and persistent profitability issues remain concerns. The $59.1 million goodwill impairment charge further highlights the company’s struggles to maintain valuation in a post-pandemic environment.

With the stock trading near its 52-week low and a market capitalization of approximately $1.92 billion, investors will be closely watching whether Teladoc’s management can stabilize the BetterHelp segment and improve profitability metrics in the coming quarters. The company’s substantial cash reserves provide some financial flexibility, but the negative free cash flow and declining adjusted EBITDA margins suggest continued challenges ahead.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.