Novo Nordisk, Eli Lilly fall after Trump comments on weight loss drug pricing

Topgolf Callaway Brands (NASDAQ:MODG) released its second quarter 2025 earnings presentation on August 6, revealing better-than-expected results and an improved outlook for the remainder of the year, despite year-over-year revenue declines. The company has raised its full-year guidance following the divestiture of Jack Wolfskin, pointing to strengthening performance in its core golf equipment business and signs of recovery in its Topgolf segment.

Quarterly Performance Highlights

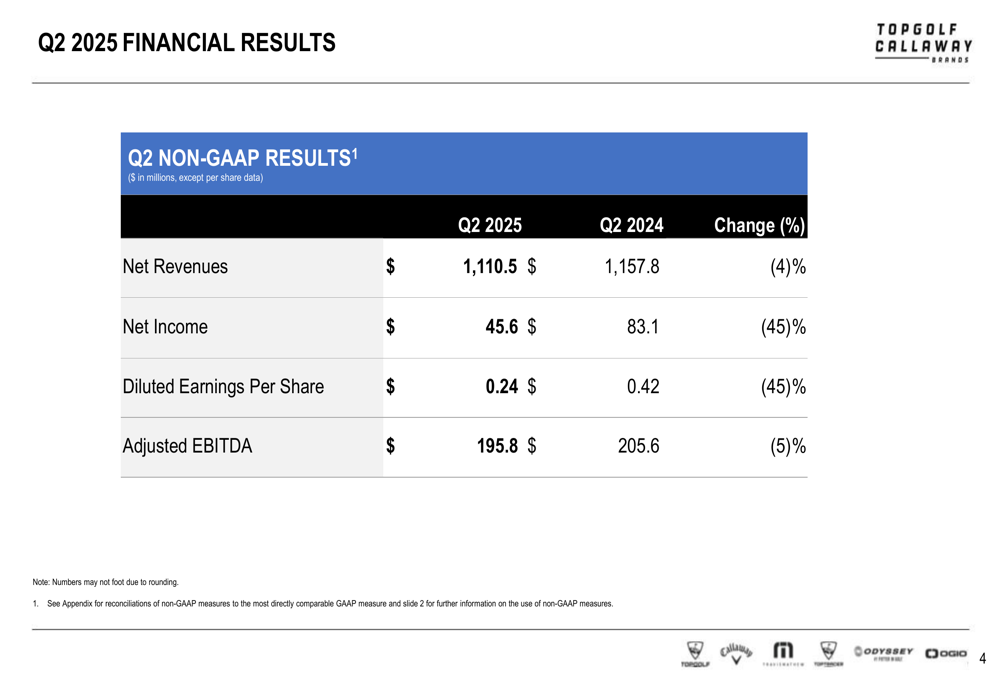

Topgolf Callaway reported Q2 2025 consolidated net revenue of $1.11 billion, representing a 4% decrease compared to the same period in 2024. Adjusted EBITDA came in at $195.8 million, down 5% year-over-year. Net income fell more significantly, dropping 45% to $45.6 million, with diluted earnings per share also declining 45% to $0.24.

As shown in the following financial results summary:

Despite these declines, management indicated that both revenue and Adjusted EBITDA exceeded their expectations for the quarter. The company’s stock closed at $8.99 on August 6, with a slight 0.89% increase in aftermarket trading according to available market data.

Segment Performance

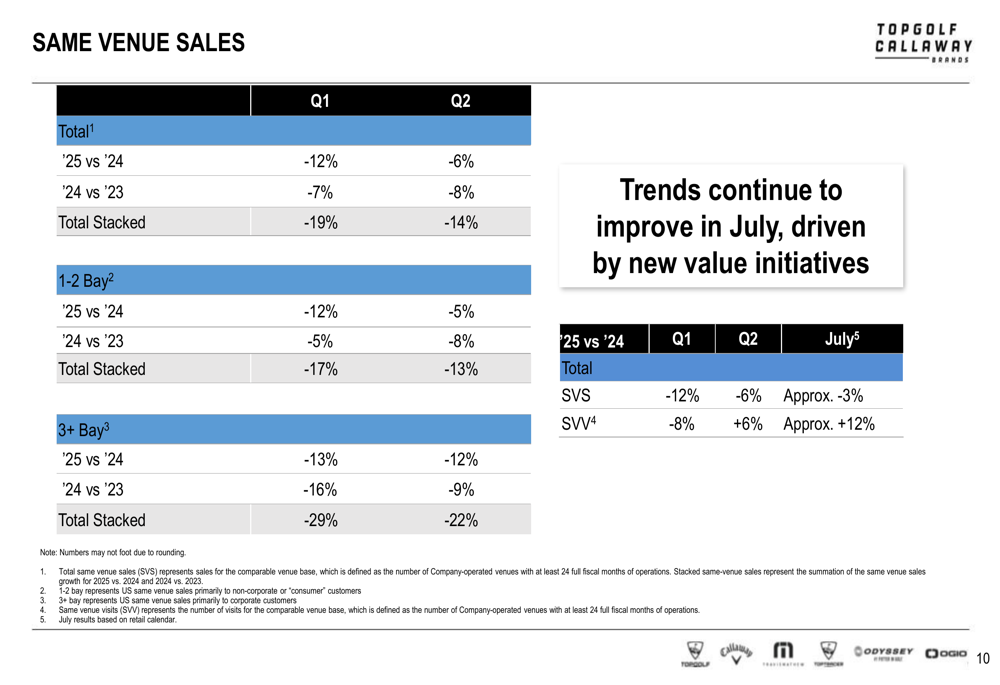

The company’s presentation highlighted several positive developments across its business segments. In the Topgolf segment, same venue visits showed positive growth in Q2, increasing 6% year-over-year. This represents a significant improvement in traffic trends, even as the company continues to face challenges with same venue sales.

The same venue sales data shows a clear trend of sequential improvement:

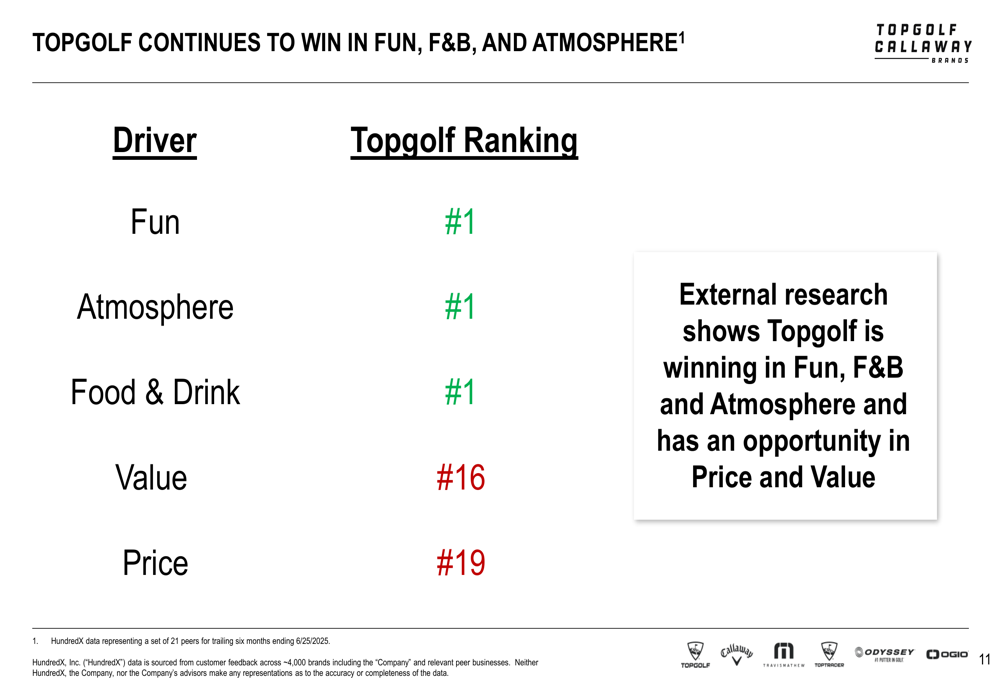

Topgolf’s competitive positioning remains strong in key experience metrics, though value perception presents an opportunity for improvement:

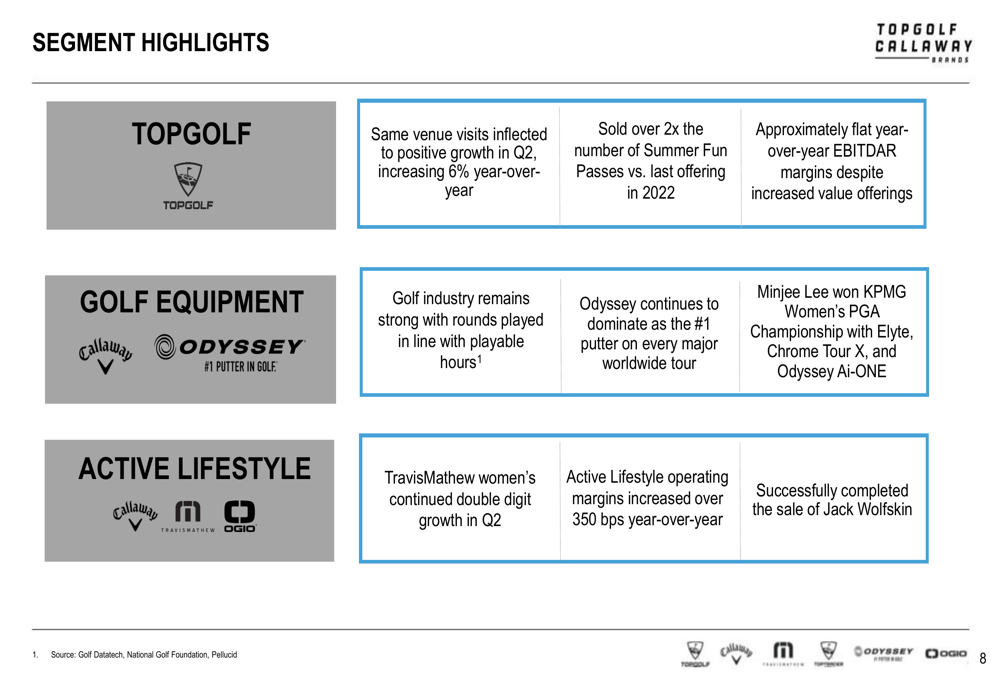

In the Golf Equipment segment, the company noted that the golf industry remains strong. Odyssey continues to dominate as the #1 putter on every major worldwide tour, and the company highlighted Minjee Lee’s win at the KPMG Women’s PGA Championship using Callaway equipment.

The Active Lifestyle segment saw Travis Mathew women’s line continue its double-digit growth in Q2, while operating margins increased over 350 basis points year-over-year. The most significant development in this segment was the successful completion of the Jack Wolfskin sale.

As illustrated in the segment highlights:

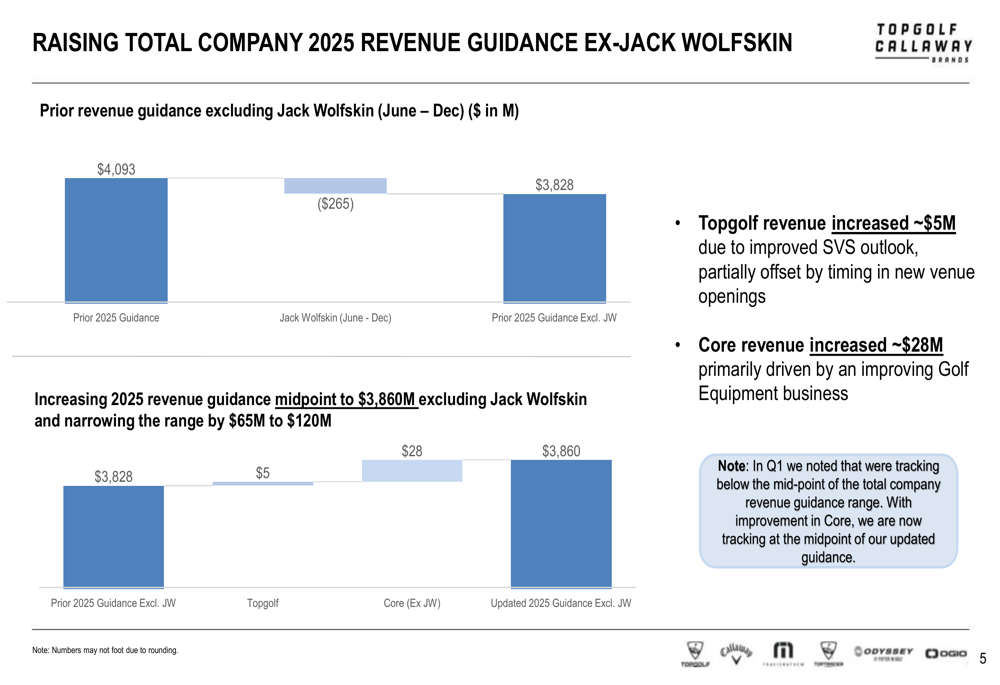

Updated Guidance

Following the divestiture of Jack Wolfskin, Topgolf Callaway has raised its full-year 2025 guidance for its continuing business. The company now expects total revenue of $3.86 billion, up from the previous ex-Jack Wolfskin guidance of $3.83 billion. This increase is primarily driven by a $28 million improvement in core revenue outlook due to an improving Golf Equipment business, along with a $5 million increase in Topgolf revenue expectations.

The revenue guidance changes are illustrated here:

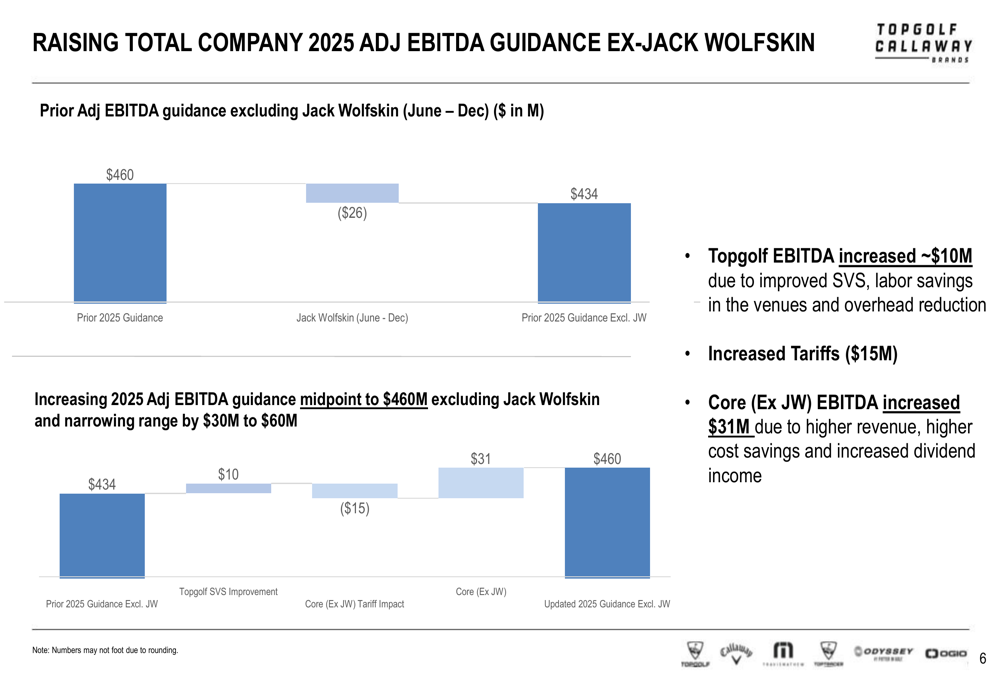

Similarly, the company has raised its Adjusted EBITDA guidance to $460 million, up from the previous ex-Jack Wolfskin guidance of $434 million. This $26 million increase comes despite a $15 million headwind from increased tariffs, and is attributed to higher revenue, increased cost savings, higher dividend income, and improved Topgolf performance.

The Adjusted EBITDA guidance changes are shown below:

For the full year 2025, the company now projects:

- Consolidated Net Revenue: $3.80 - $3.92 billion

- Topgolf Revenue: $1.71 - $1.77 billion

- Topgolf Same Venue Sales: -6% to -9%

- Consolidated Adjusted EBITDA: $430 - $490 million

- Topgolf Adjusted EBITDA: $265 - $295 million

For Q3 2025, the company expects:

- Net Revenue: $880 - $920 million

- Adjusted EBITDA: $78 - $98 million

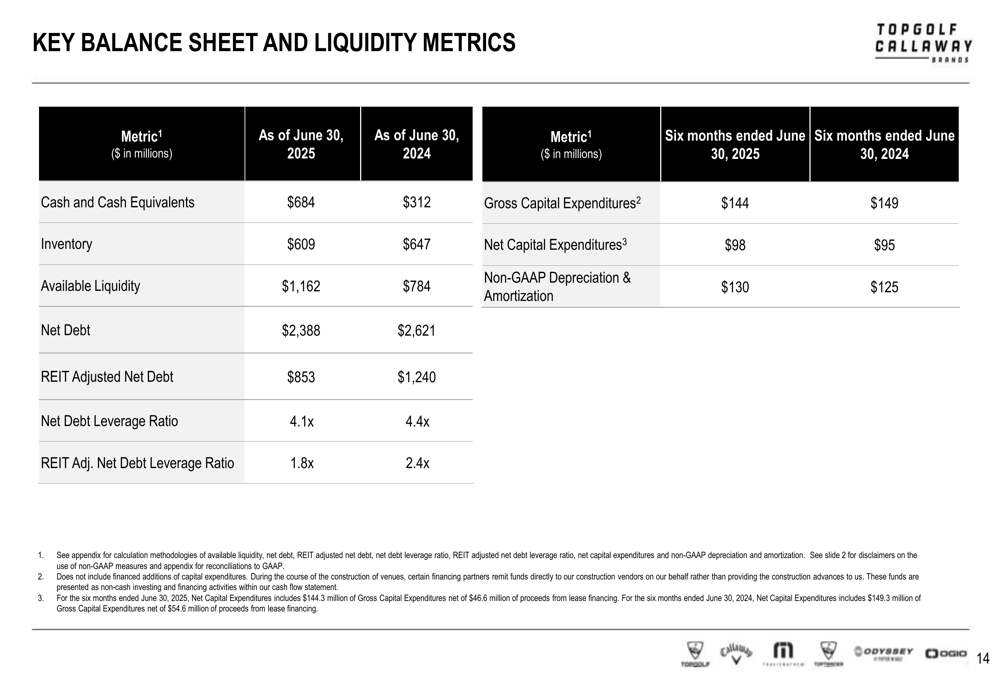

Financial Position & Liquidity

The completion of the Jack Wolfskin sale has significantly strengthened Topgolf Callaway’s financial position. The company reported that its available liquidity increased by 48% to over $1.1 billion. Cash and cash equivalents stood at $684 million as of June 30, 2025, more than double the $312 million reported a year earlier.

Net debt decreased to $2.39 billion from $2.62 billion in the prior year, while the net debt leverage ratio improved to 4.1x from 4.4x. When adjusted for REIT financing, the company’s net debt leverage ratio stands at a more favorable 1.8x, compared to 2.4x a year ago.

The key balance sheet metrics are summarized below:

Forward-Looking Statements

Topgolf Callaway continues to invest in brand partnerships and product innovation across its segments. Recent highlights include The Fantastic Four: First Steps Topgolf Experience, Happy Gilmore 2 Limited Edition Products, and Travis Mathew’s Limited Edition Pro Plus Golf Shoe in partnership with Guinness.

As shown in these brand initiatives:

The company faces ongoing challenges, particularly in the Topgolf segment where same venue sales remain negative despite showing improvement. While Topgolf ranks #1 in fun, atmosphere, and food & drink, it ranks significantly lower in value (#16) and price (#19), indicating potential areas for strategic focus.

The improved guidance suggests management confidence in the company’s trajectory for the remainder of 2025, with particular strength expected in the core Golf Equipment business. The divestiture of Jack Wolfskin appears to be part of a strategic refocusing on higher-performing segments, while also strengthening the company’s financial flexibility through improved liquidity and reduced leverage.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.