BETA Technologies launches IPO of 25 million shares priced $27-$33

Introduction & Market Context

Tractor Supply Company (NASDAQ:TSCO) released its first quarter 2025 earnings presentation on April 24, 2025, revealing mixed results that prompted a 5.31% decline in the company’s stock price. While the rural lifestyle retailer reported a 2.1% increase in net sales to $3.47 billion, comparable store sales declined by 0.9%, marking a reversal from the 1.1% growth seen in the same period last year. The company also lowered its full-year guidance across several key metrics.

The results come as Tractor Supply continues to navigate a challenging retail environment, with consumers showing more cautious spending patterns, particularly in seasonal categories. Despite these headwinds, the company highlighted progress in its strategic initiatives and continued expansion efforts.

Quarterly Performance Highlights

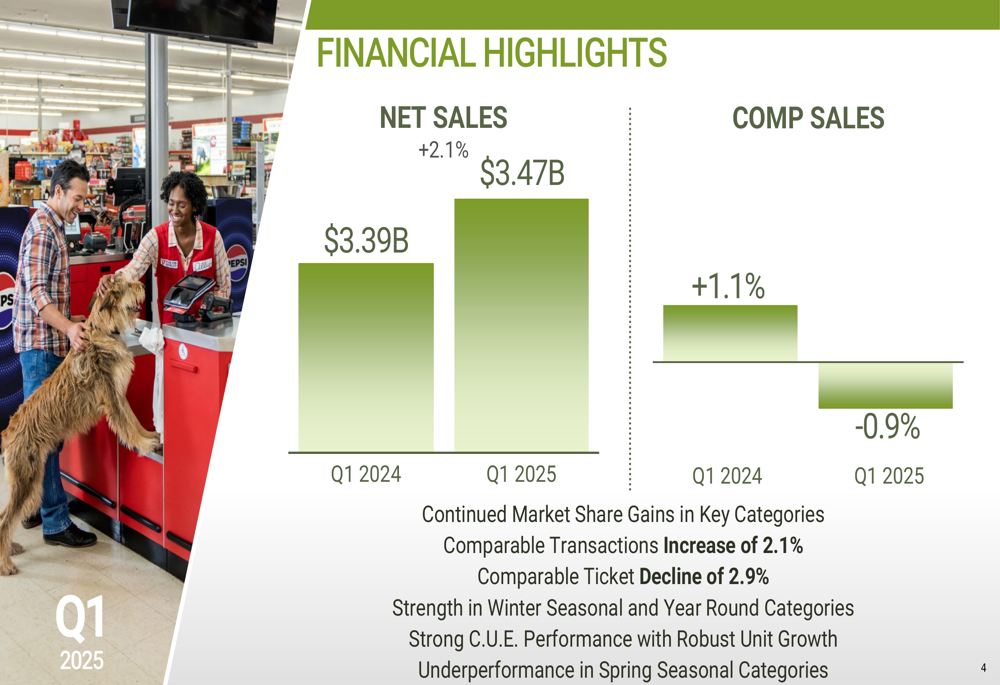

Tractor Supply’s Q1 2025 performance showed a divergence between overall sales growth and same-store performance. Net sales increased by 2.1% to $3.47 billion, up from $3.39 billion in Q1 2024, primarily driven by new store openings. However, comparable store sales declined by 0.9%, compared to a 1.1% increase in the prior year period.

The company reported an interesting split in consumer behavior, with comparable transactions increasing by 2.1% while the average ticket size decreased by 2.9%. Management noted strength in winter seasonal and year-round categories, along with robust unit growth in its C.U.E. (Consumable, Usable, Edible) products, but acknowledged underperformance in spring seasonal categories.

As shown in the following chart of quarterly sales performance:

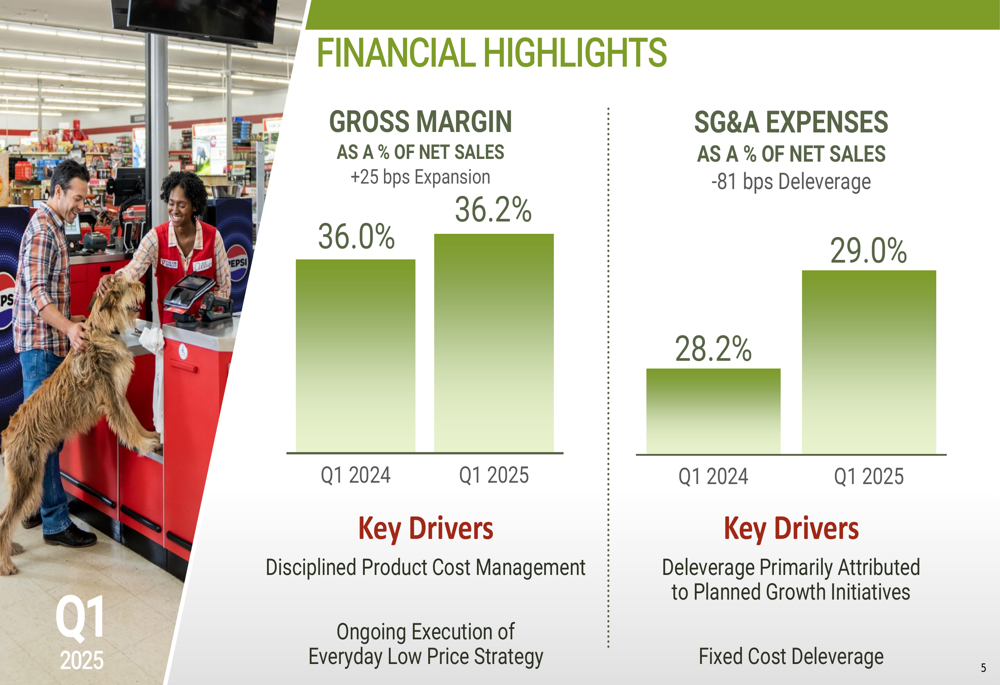

Gross margin showed modest improvement, expanding by 25 basis points to 36.2% compared to 36.0% in Q1 2024. The company attributed this increase to disciplined product cost management and ongoing execution of its everyday low price strategy. However, selling, general and administrative (SG&A) expenses increased by 81 basis points to 29.0% of net sales, up from 28.2% in the prior year period, primarily due to planned growth initiatives and fixed cost deleverage.

The following chart illustrates the margin and expense trends:

Detailed Financial Analysis

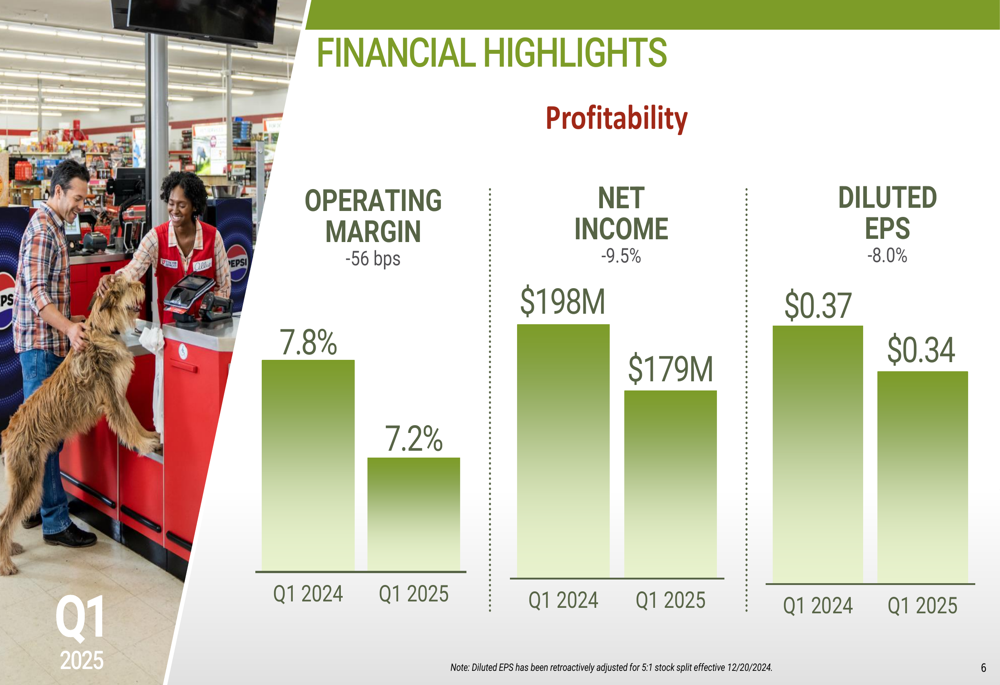

The increase in SG&A expenses outpaced gross margin improvement, resulting in compressed operating margins and lower profitability. Operating margin decreased by 56 basis points to 7.2%, down from 7.8% in Q1 2024. This margin pressure flowed through to the bottom line, with net income declining by 9.5% to $179 million compared to $198 million in the same period last year.

Diluted earnings per share (EPS) fell by 8.0% to $0.34, down from $0.37 in Q1 2024. The company noted that diluted EPS figures have been retroactively adjusted for the 5:1 stock split that became effective on December 20, 2024.

The following chart details the company’s profitability metrics:

These results represent a continuation of the challenges seen in Q4 2024, when the company reported EPS of $0.44, slightly below the forecast of $0.45, on revenue of $3.77 billion, which also missed expectations. The sequential decline in profitability metrics suggests that margin pressures have intensified in the first quarter of 2025.

Strategic Initiatives

Despite the financial headwinds, Tractor Supply continued to advance its strategic initiatives during the quarter. The company reported that enrollment in its Neighbor’s Club loyalty program is approaching 40 million customers, representing a significant portion of its customer base. The company now has over 600 Garden Centers operational across its store network and kicked off its 2025 Spring Chick Days in stores, a seasonal promotion that typically drives foot traffic.

In terms of infrastructure development, Tractor Supply announced its 11th distribution center in Nampa, Idaho, further expanding its supply chain capabilities to support future growth.

The following image highlights these operational achievements:

The company also emphasized its community engagement and partnership initiatives under its "Life Out Here" strategy. Key developments included a strategic partnership with Field & Stream, support for the third annual "Relief for Rescues" fundraiser with MuttNation, the nationwide rollout of Weber products to all stores, and the celebration of 10 years of grants for growing to benefit FFA (Future Farmers of America).

Forward-Looking Statements

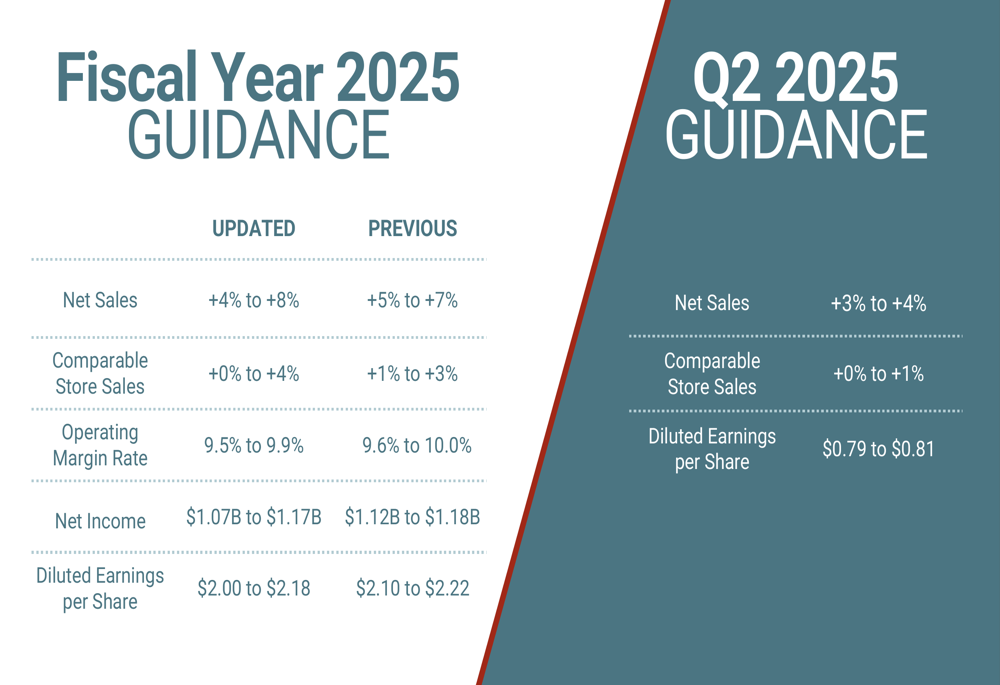

In a significant development, Tractor Supply revised its fiscal year 2025 guidance, generally lowering expectations from previous forecasts. The company now expects net sales growth of 4% to 8%, a change from the previous guidance of 5% to 7% provided in its Q4 2024 earnings. Comparable store sales are projected to increase between 0% and 4%, compared to the earlier forecast of 1% to 3%, indicating greater uncertainty in the outlook.

Operating margin is now expected to be between 9.5% and 9.9%, down from the previous range of 9.6% to 10.0%. Net income is projected to be $1.07 billion to $1.17 billion, lower than the previous guidance of $1.12 billion to $1.18 billion. Similarly, diluted EPS guidance was reduced to $2.00 to $2.18, down from $2.10 to $2.22.

For the second quarter of 2025, Tractor Supply expects net sales to increase by 3% to 4%, with comparable store sales growth of 0% to 1%. Diluted EPS for Q2 is projected to be between $0.79 and $0.81.

The following chart details the company’s updated guidance:

The revised guidance suggests that Tractor Supply is taking a more cautious approach to its full-year outlook, likely reflecting the challenges observed in the first quarter and uncertainty about consumer spending patterns for the remainder of the year. The wider ranges in some metrics, particularly comparable store sales, indicate increased uncertainty in the company’s forecasting.

Despite these near-term challenges, Tractor Supply remains committed to its long-term "Life Out Here 2030" strategy, which focuses on delivering legendary customer experiences, advancing ONE Tractor capabilities, operating the Tractor Way, supporting its team members, and generating healthy shareholder returns. The company’s continued investment in new stores, distribution centers, and strategic partnerships demonstrates confidence in its long-term growth prospects, even as it navigates a more challenging short-term environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.