Adaptimmune stock plunges after announcing Nasdaq delisting plans

Introduction & Market Context

Tryg A/S (CPH:TRYG), the second-largest general insurer in the Nordic region, reported solid Q3 2025 results, continuing the positive momentum seen in the previous quarter. The company’s shares closed at 167.6 on October 9, 2025, and have traded between 141.5 and 173.9 over the past 52 weeks.

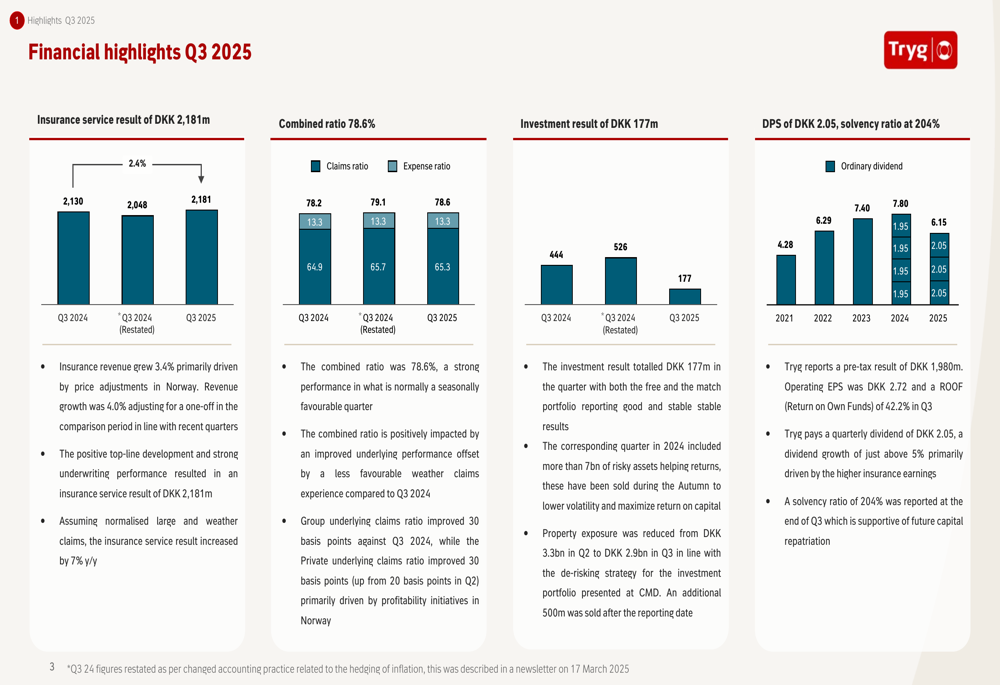

The Q3 results show an insurance service result of DKK 2,181 million, up 2.4% from the same period last year, with insurance revenue growth of 3.4% (4.0% when adjusted for a one-off). These results build on the strong performance reported in Q2 2025, when Tryg beat earnings expectations with an EPS of 2.8.

Quarterly Performance Highlights

Tryg reported a combined ratio of 78.6% for Q3 2025, indicating strong underwriting profitability. The insurance service result increased by 7% year-over-year when adjusted for normalized large and weather claims, demonstrating the company’s solid operational performance.

As shown in the following financial highlights chart, Tryg maintained its strong profitability while delivering an ordinary dividend of DKK 2.05 per share:

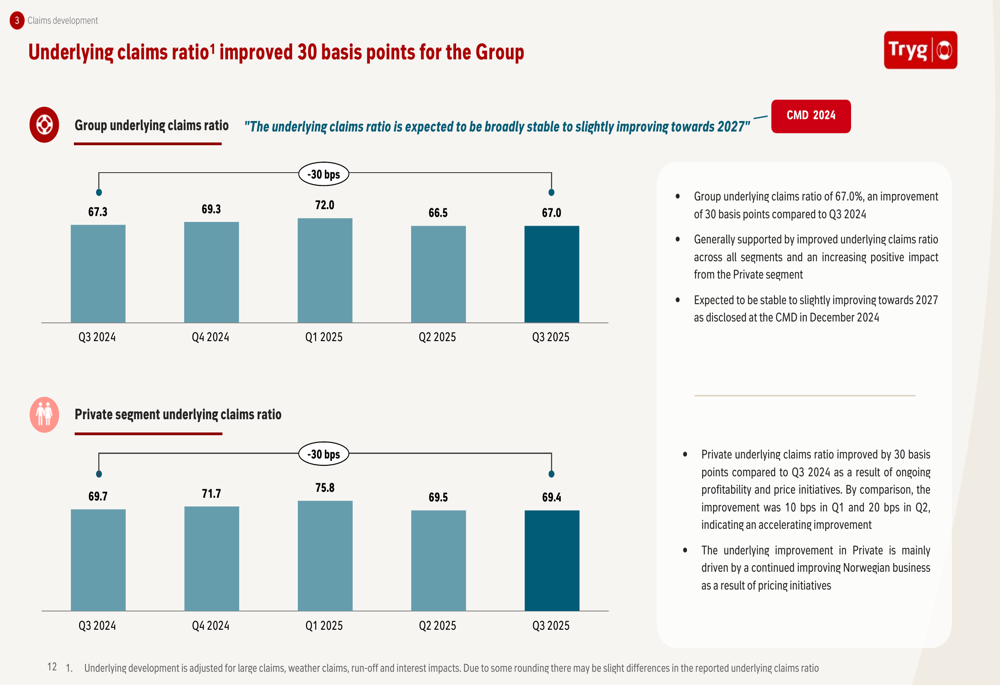

The company’s underlying claims ratio improved by 30 basis points compared to Q3 2024, reaching 67.0%. This improvement reflects Tryg’s continued focus on technical excellence and risk management. The Private segment also saw a 30 basis point improvement in its underlying claims ratio.

As illustrated in this chart of the underlying claims ratio development:

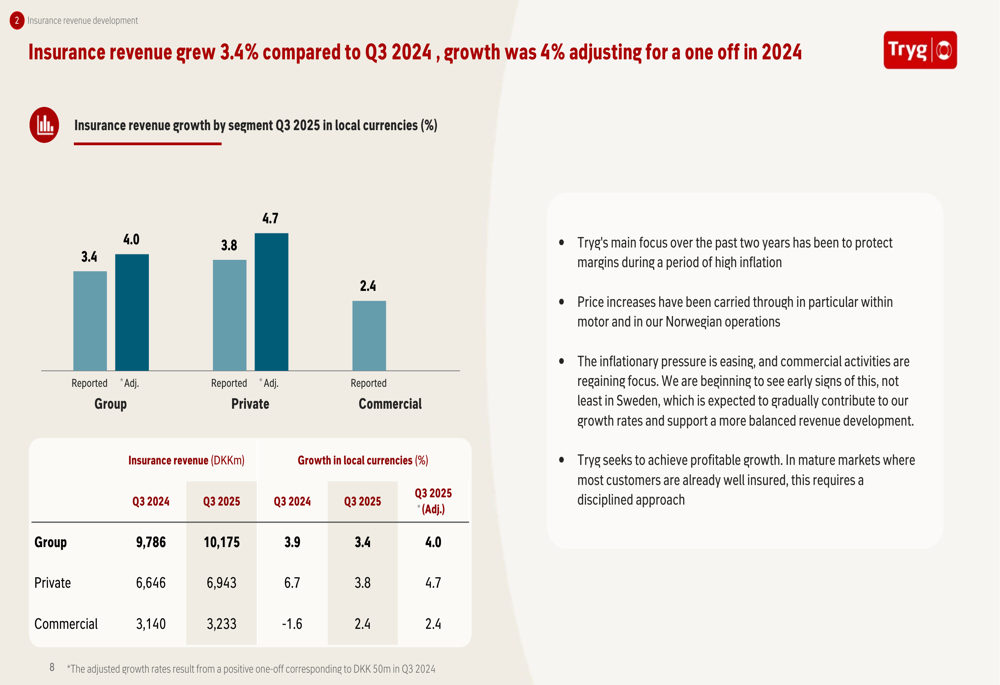

Revenue growth remained solid at 3.4%, or 4.0% when adjusted for a one-off in 2024. The Private segment grew by 3.8% (4.7% adjusted), while the Commercial segment increased by 2.4%. Tryg emphasized that its main focus has been on protecting margins during high inflation, with price increases implemented in motor insurance and Norwegian operations.

The following chart illustrates the insurance revenue growth by segment:

Geographical Performance

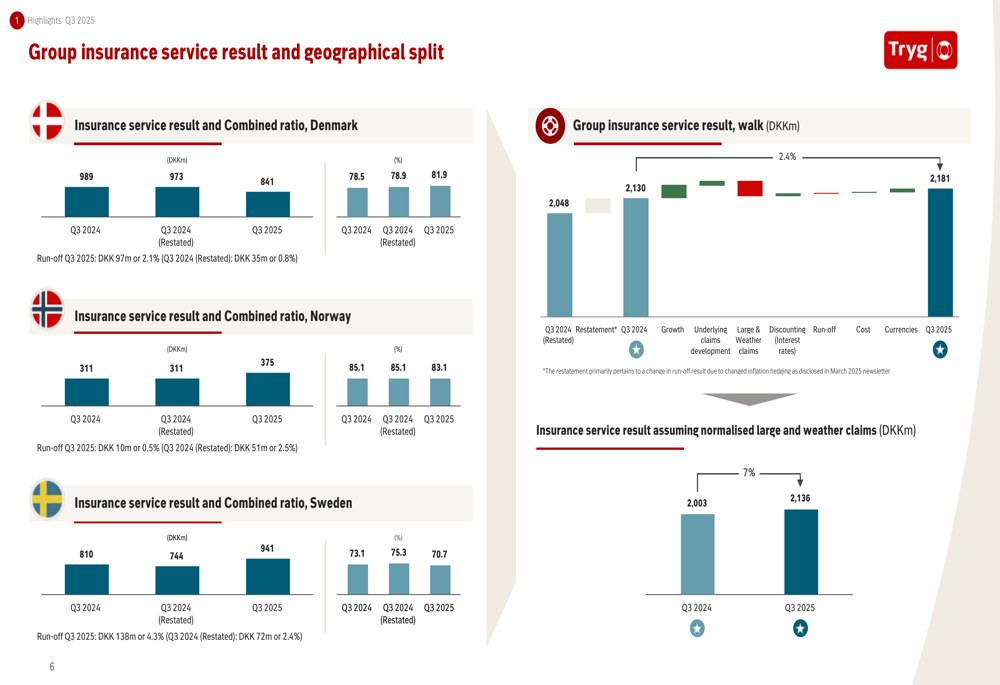

Tryg’s performance varied significantly across its geographical segments. Sweden emerged as the standout performer with a combined ratio of 70.7%, improving from 75.3% in Q3 2024. Denmark’s combined ratio deteriorated to 81.9% from 78.9%, while Norway showed improvement at 83.1% compared to 85.1% in the same period last year.

The geographical split of the insurance service result is shown in the following chart:

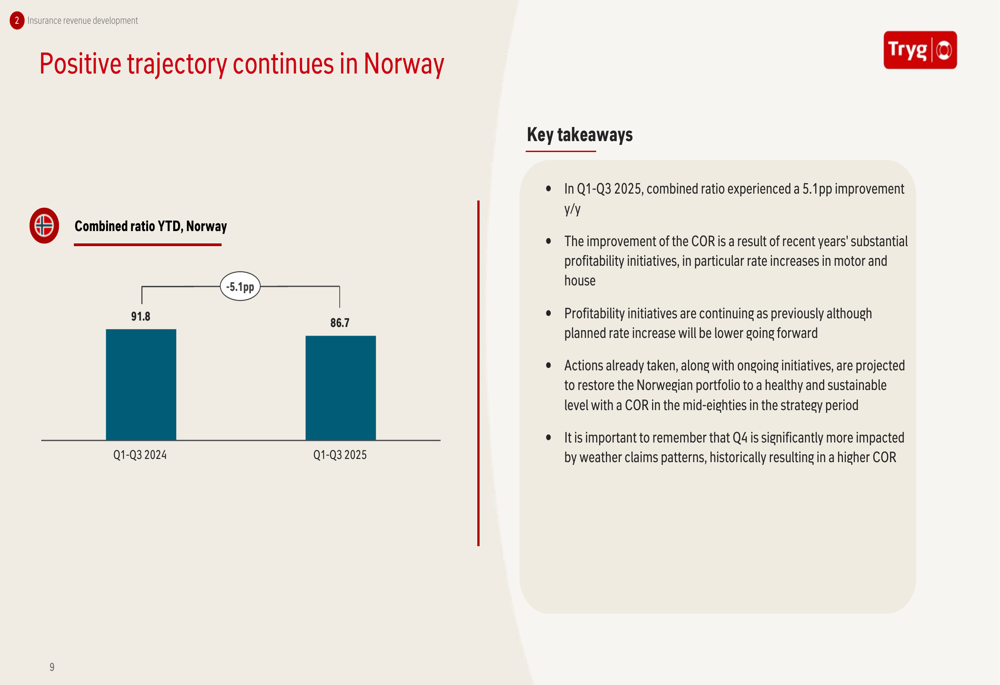

Norway deserves special mention as it continues to show significant improvement. The combined ratio for the first nine months of 2025 improved by 5.1 percentage points year-over-year, reaching 86.7% compared to 91.8% for the same period in 2024. This improvement is attributed to substantial profitability initiatives, particularly rate increases in motor and house insurance.

As shown in this chart of Norway’s performance trajectory:

Johan Brahmer, Group CEO, highlighted this improvement during the previous earnings call, stating, "We are seeing very strong improvement both in Norway and on Motor." This positive trend has continued into Q3 2025.

Investment Activities & Solvency

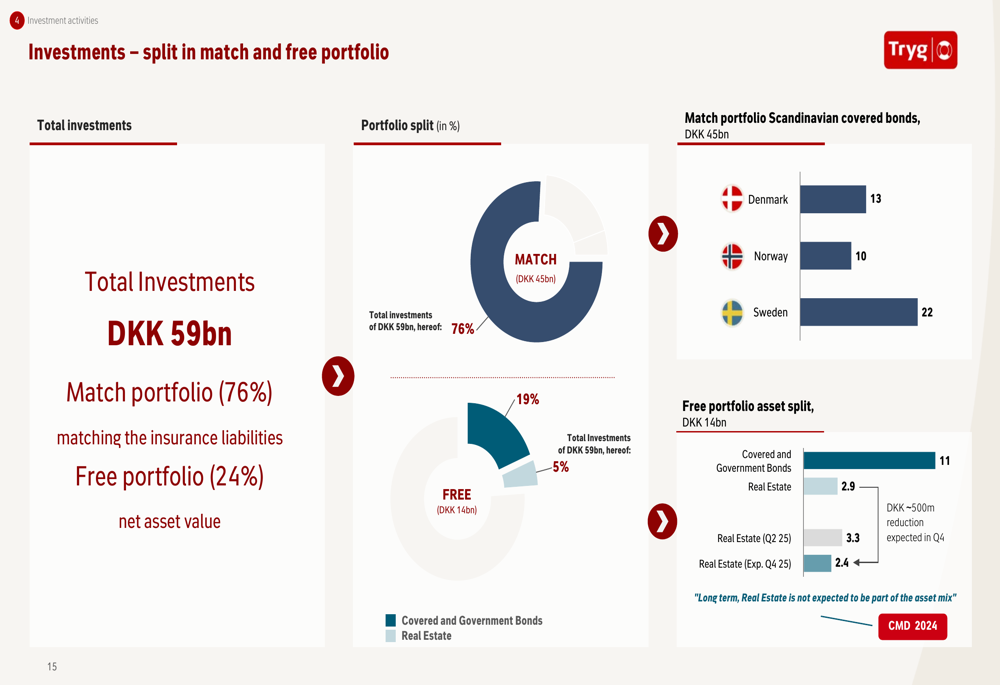

Tryg reported an investment result of DKK 177 million in Q3 2025, significantly lower than the DKK 526 million reported in Q3 2024. The free portfolio contributed DKK 87 million, while the match portfolio added DKK 177 million. Other financial income and expenses were negative at DKK -87 million.

The company’s investment portfolio of DKK 59 billion is split between a match portfolio (76%) and a free portfolio (24%), as illustrated in the following chart:

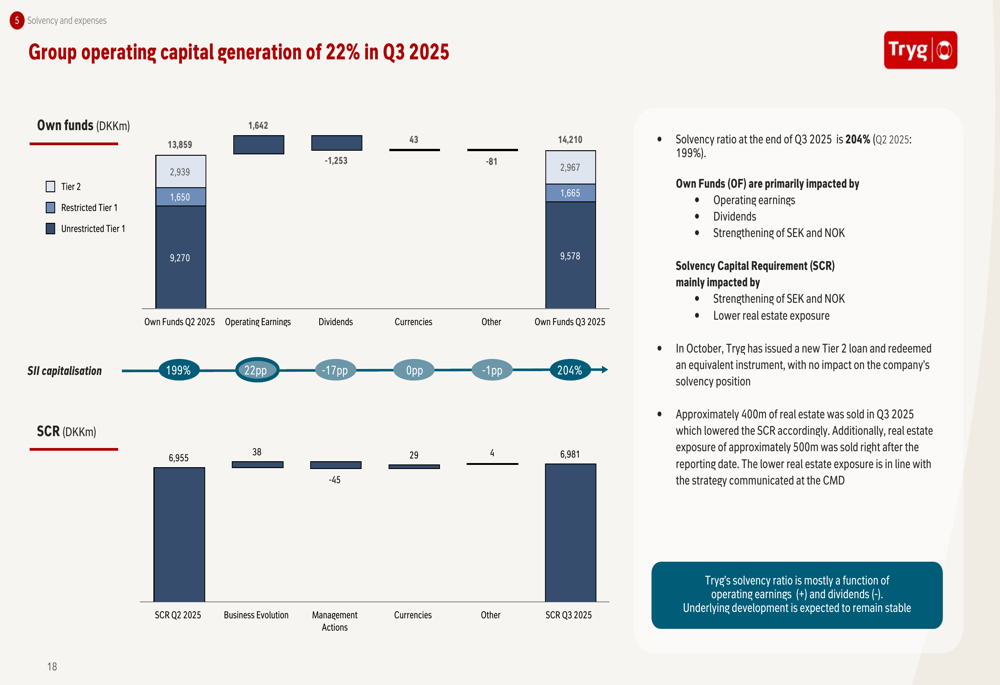

Tryg’s solvency position remains strong with a solvency ratio of 204% at the end of Q3 2025, up from 199% reported in Q2 2025. This improvement is attributed to operating earnings, dividend payments, strengthening of SEK and NOK, and lower real estate exposure.

The company’s operating capital generation and solvency position are illustrated in the following chart:

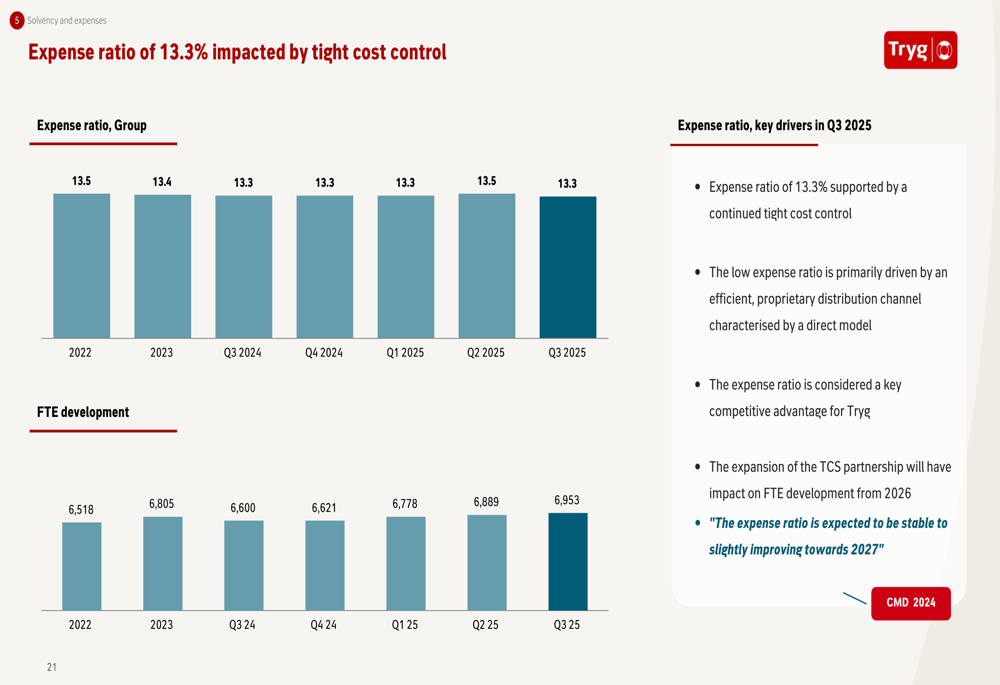

Tryg continues to maintain tight cost control, with an expense ratio of 13.3% in Q3 2025. The company expects the expense ratio to be stable to slightly improving towards 2027.

The expense ratio and FTE development are shown in this chart:

Strategic Initiatives & 2027 Targets

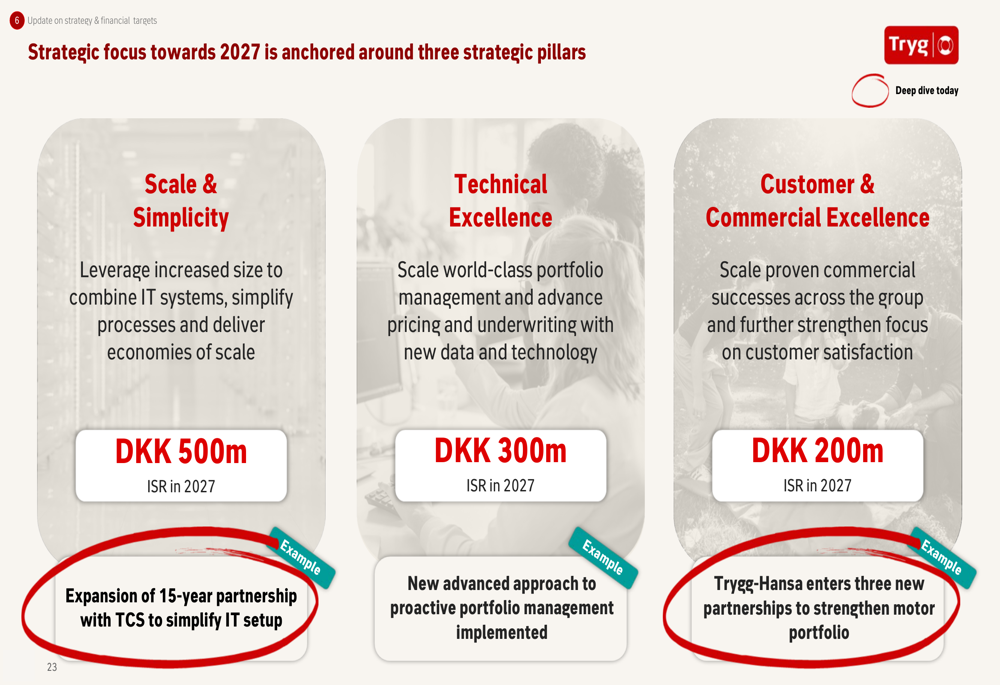

Tryg’s strategy towards 2027 is anchored around three strategic pillars: Scale & Simplicity, Technical Excellence, and Customer & Commercial Excellence. These initiatives are expected to contribute DKK 500 million, DKK 300 million, and DKK 200 million respectively to the insurance service result by 2027.

The strategic focus is illustrated in the following chart:

Key strategic developments in Q3 2025 include the expansion of a 15-year partnership with TCS to simplify the IT setup and new partnerships in Sweden. Trygg-Hansa, Tryg’s Swedish operation, entered new partnerships with Subaru, Carla, and Hedin Automotive to strengthen its motor portfolio.

Looking ahead, Tryg has set ambitious targets for 2027, including a combined ratio of approximately 81%, insurance service results of DKK 8.0-8.4 billion, and a return on own funds of 35-40%. The company also aims to continue improving customer satisfaction, which has remained stable at 82 for three consecutive quarters.

The financial and strategic targets for 2027 are summarized in this chart:

Mikael Karsten, Group CTO, emphasized during the previous earnings call that the company is "concentrated on the things that we can affect and pricing and driving profitability initiatives accordingly." This focus on controllable factors appears to be yielding positive results as Tryg progresses toward its 2027 targets.

While Tryg faces challenges from inflationary pressures and competition in Nordic markets, the company’s solid Q3 2025 performance demonstrates its ability to navigate these challenges effectively while maintaining strong profitability and a robust solvency position.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.