Goldman Sachs chief credit strategist Lotfi Karoui departs after 18 years - Bloomberg

Introduction & Market Context

U-Haul Holding Company (NASDAQ:UHAL) recently presented its first quarter fiscal 2026 results, revealing a company focused on expanding its self-storage business while maintaining its core moving operations. Despite reporting revenue growth that exceeded analyst expectations, the company faced operational challenges that pressured profits. Following the earnings announcement, U-Haul’s stock closed at $56.72, up 2.65% from the previous session, suggesting investors were encouraged by the company’s revenue performance despite the earnings miss.

The company reported revenue of $1.63 billion, surpassing forecasts of $1.60 billion, but posted earnings per share of $0.68, significantly below the expected $1.21. This 43.8% negative earnings surprise comes as U-Haul continues to invest heavily in its growth initiatives while managing increased operational costs.

Quarterly Performance Highlights

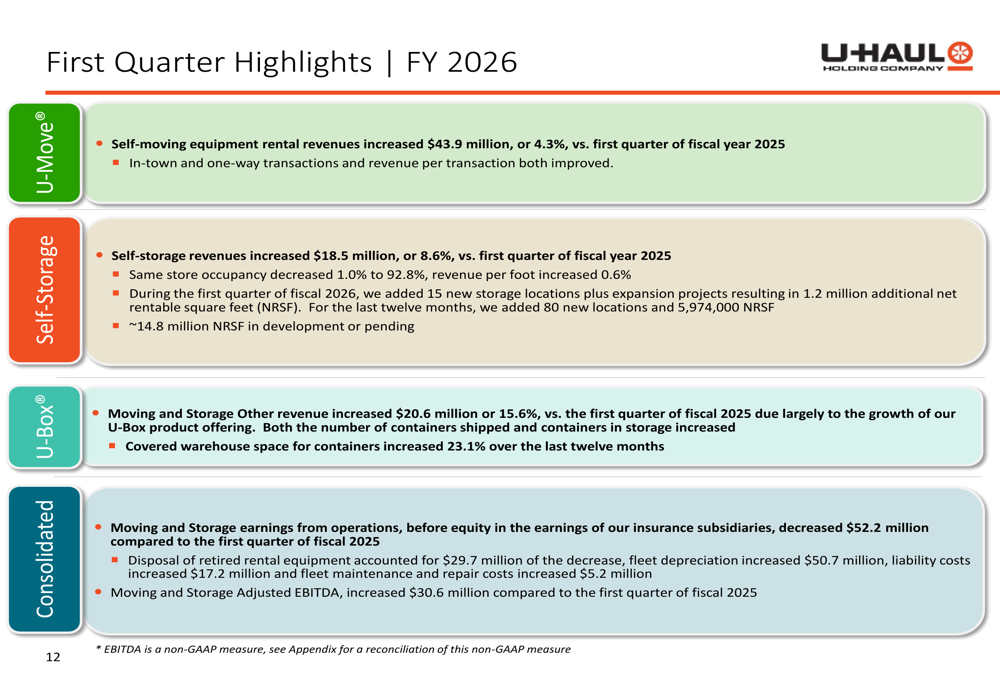

U-Haul’s first quarter showed strength across its three main business segments, with particularly notable growth in its self-storage and U-Box operations. The company’s self-moving equipment rental revenues increased by $43.9 million (4.3%) compared to the first quarter of fiscal 2025, with improvements in both in-town and one-way transactions and revenue per transaction.

As shown in the following overview of the company’s key business segments:

Self-storage revenues grew by $18.5 million (8.6%) versus the same quarter last year. While same-store occupancy decreased slightly by 1.0% to 92.8%, revenue per square foot increased by 0.6%. The company’s U-Box portable moving and storage business saw significant growth, with revenues increasing by 15.6% compared to Q1 FY2025.

However, Moving and Storage earnings from operations declined by $52.2 million year-over-year, primarily due to several factors: disposal of retired rental equipment ($29.7 million), increased fleet depreciation ($50.7 million), higher liability costs ($17.2 million), and increased fleet maintenance and repair costs ($5.2 million). Despite these challenges, Adjusted EBITDA increased by $30.6 million compared to the first quarter of fiscal 2025.

The following chart illustrates the company’s first quarter highlights across its business segments:

Strategic Focus on Self-Storage Expansion

U-Haul continues to position itself as a leader in the self-storage industry, currently ranking as the #3 self-storage company in the U.S. by square footage owned. The company’s integrated business model creates synergies between its moving and storage operations, with approximately 50% of U-Haul self-storage transactions including an associated U-Move transaction.

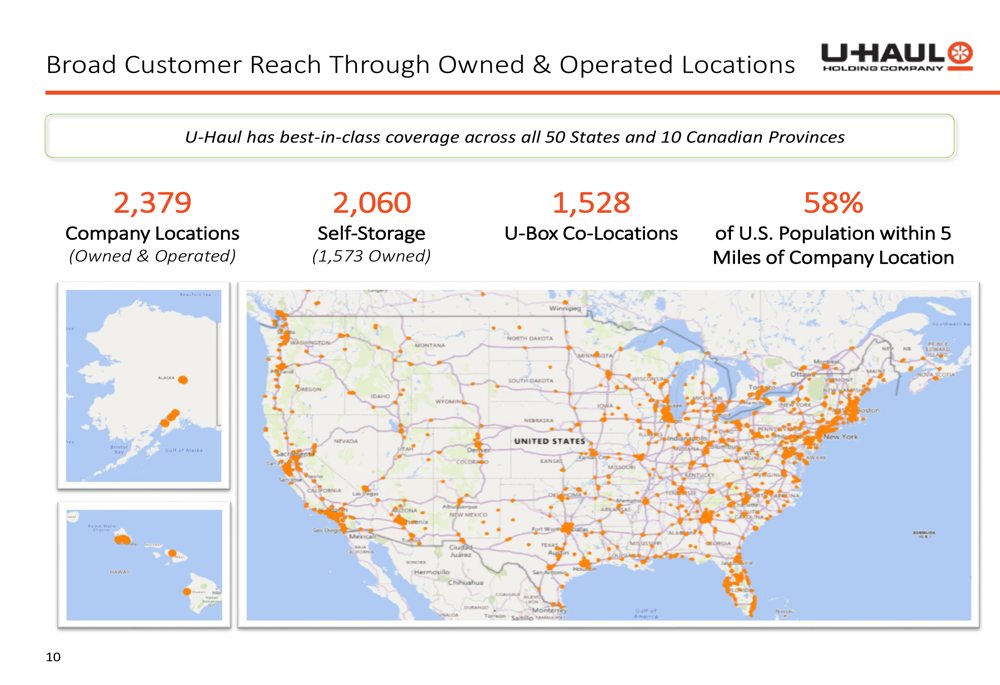

The company’s presentation emphasized its extensive geographic footprint, with 2,379 company-owned and operated locations across all 50 states and 10 Canadian provinces. This network is further expanded through independent dealers, bringing the total location count to 24,517. According to the company, 58% of the U.S. population lives within 5 miles of a company location, and 90% lives within 5 miles of a U-Haul dealer.

The following map illustrates U-Haul’s broad customer reach through owned and operated locations:

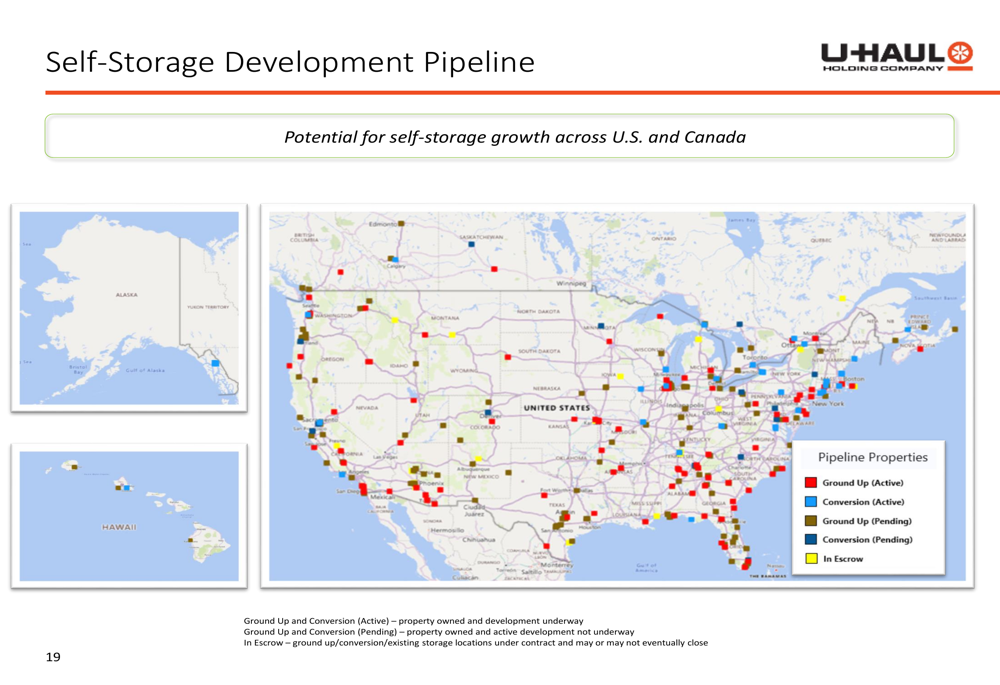

U-Haul’s self-storage development pipeline remains robust, with the company adding 15 new storage locations plus expansion projects that contributed 1.2 million additional net rentable square feet during the quarter. Over the past twelve months, the company has added 80 new locations and 5.97 million net rentable square feet. Looking ahead, approximately 14.8 million square feet are in development or pending.

The company’s self-storage expansion strategy is illustrated in this development pipeline map:

Detailed Financial Analysis

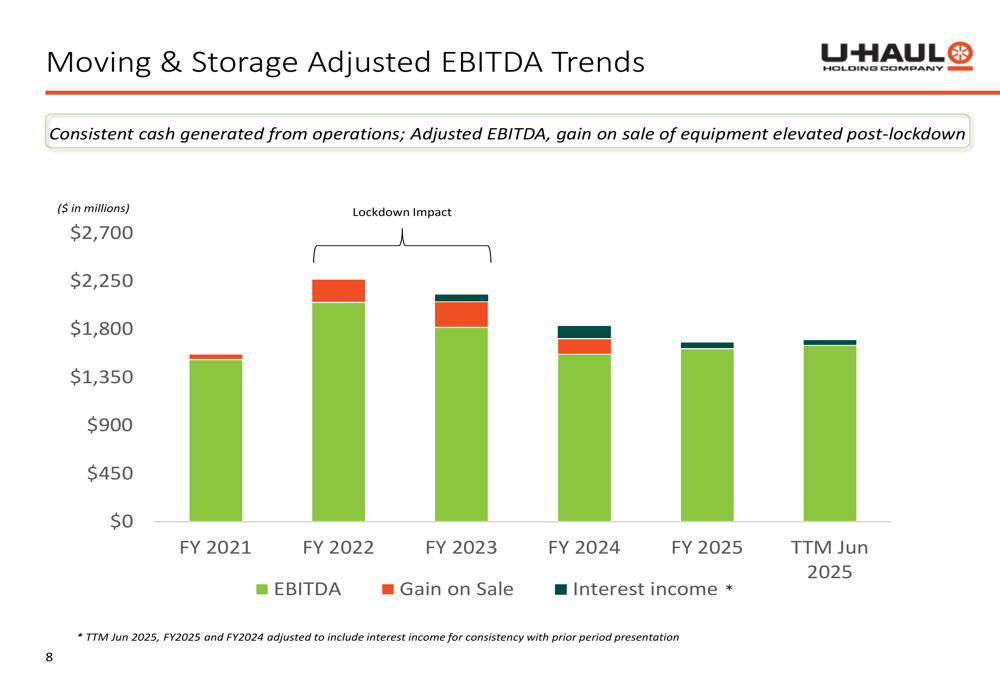

U-Haul’s financial performance reflects its strategic focus on long-term growth, particularly in the self-storage segment. The company’s Moving & Storage adjusted EBITDA has remained relatively stable in recent years after the post-pandemic surge, with the trailing twelve months ending June 2025 showing $1.73 billion in adjusted EBITDA.

The following chart shows the Moving & Storage Adjusted EBITDA trends over recent years:

The company’s revenue mix continues to evolve, with self-storage representing an increasing portion of total revenues. For the trailing twelve months ending June 2025, U-Move (equipment rental) contributed $3.77 billion (68% of revenue), Self-Storage contributed $916 million (16% of revenue), and other segments including U-Box made up the remainder.

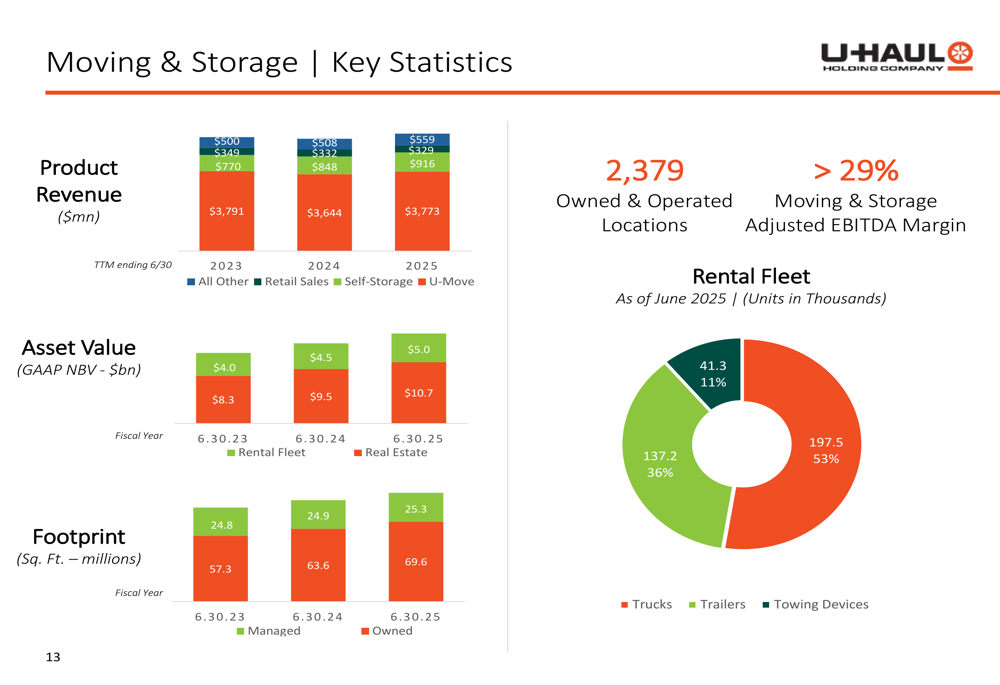

U-Haul’s key financial statistics are presented in the following comprehensive overview:

The company maintains a well-capitalized balance sheet with a net leverage ratio of 4.0x as of June 30, 2025. Total debt stood at approximately $7.3 billion against total assets of $16.9 billion. This leverage position allows U-Haul to continue investing in growth initiatives while maintaining financial stability.

Growth Potential and Forward Outlook

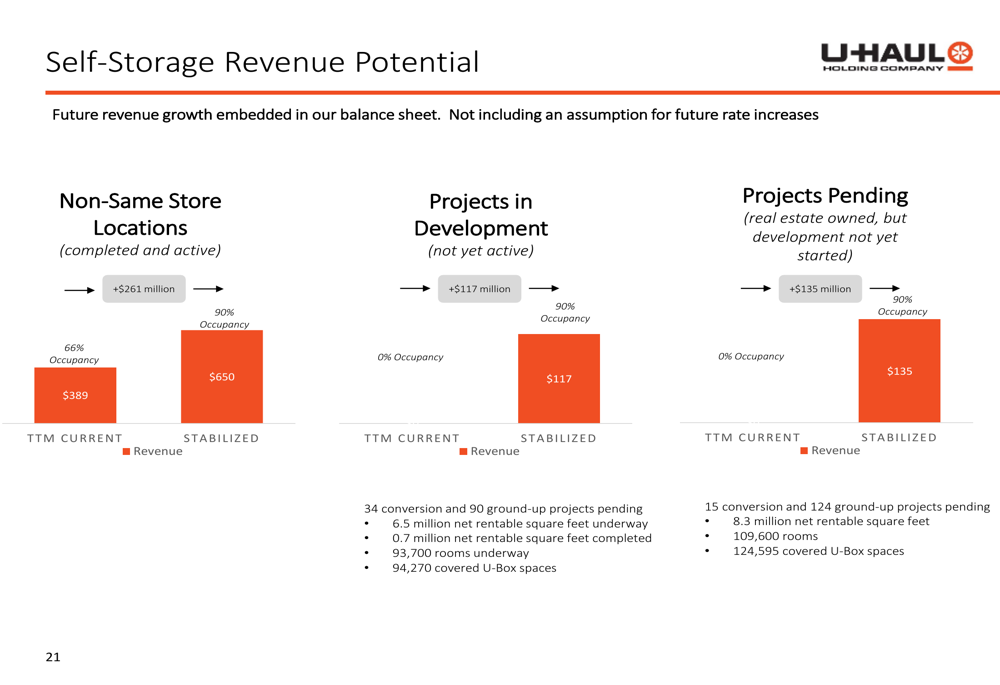

U-Haul’s presentation highlighted significant revenue potential from its self-storage expansion. The company projects additional revenue of $261 million from non-same store locations once they reach stabilized 90% occupancy (currently at 66%). Projects in development and pending projects could add another $252 million in revenue once completed and stabilized.

The following chart illustrates this self-storage revenue potential:

Over the past five years, U-Haul has added 296 new storage locations, 26.2 million net rentable square feet, with investments totaling $5.8 billion. The company has outpaced its self-storage REIT competitors in terms of square footage growth, increasing its owned rentable square footage by 60% since June 2022, compared to 30% for CubeSmart (NYSE:CUBE), 31% for Public Storage (NYSE:PSA), and 37% for Extra Space Storage (NYSE:EXR) and Life Storage combined.

During the earnings call, Vice Chairman Sam Schoen expressed optimism about U-Box’s growth potential, stating, "I don’t see why there’s any reason that U-Box couldn’t be as big as U-Haul is today." CFO Jason Berg highlighted the company’s strategic equipment placement, saying, "We’re going through the process of placing this new equipment in places that we think it’s gonna be productive."

Looking ahead, U-Haul plans to continue its storage expansion, maintaining a development pace of 4.5-6 million square feet annually. However, the company faces challenges including increased personnel costs (up $20 million), rising liability costs (up $17 million), and higher fleet maintenance expenses (up $5 million), which could continue to pressure margins in the near term.

Conclusion

U-Haul’s first quarter fiscal 2026 results reflect a company in transition, strategically expanding its self-storage business while maintaining its core moving operations. Despite operational challenges that impacted profitability, the company continues to grow revenue across all segments and invest in long-term growth initiatives. With a well-capitalized balance sheet and significant revenue potential from its development pipeline, U-Haul appears positioned for continued expansion in the self-storage market, though investors will be watching closely to see if the company can address the cost pressures that affected its bottom line this quarter.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.