Walmart halts H-1B visa offers amid Trump’s $100,000 fee increase - Bloomberg

Introduction & Market Context

U-Haul Holding Company (NASDAQ:UHAL) presented its fourth quarter fiscal 2025 results on May 29, 2025, highlighting revenue growth across key segments despite facing profitability headwinds. The company reported a wider-than-expected quarterly loss of $0.41 per share, missing analyst expectations of -$0.22, while revenue exceeded forecasts at $1.23 billion. U-Haul shares experienced a slight decline of 0.02% in after-hours trading following the announcement, reflecting investor concerns about the earnings miss despite the revenue beat.

The company continues to expand its self-storage footprint while maintaining its position as North America’s leader in do-it-yourself moving and storage solutions. With a market capitalization of $12.25 billion and trailing twelve-month revenue of $5.69 billion, U-Haul maintains significant market presence despite facing challenges with increased costs and capital expenditures.

Quarterly Performance Highlights

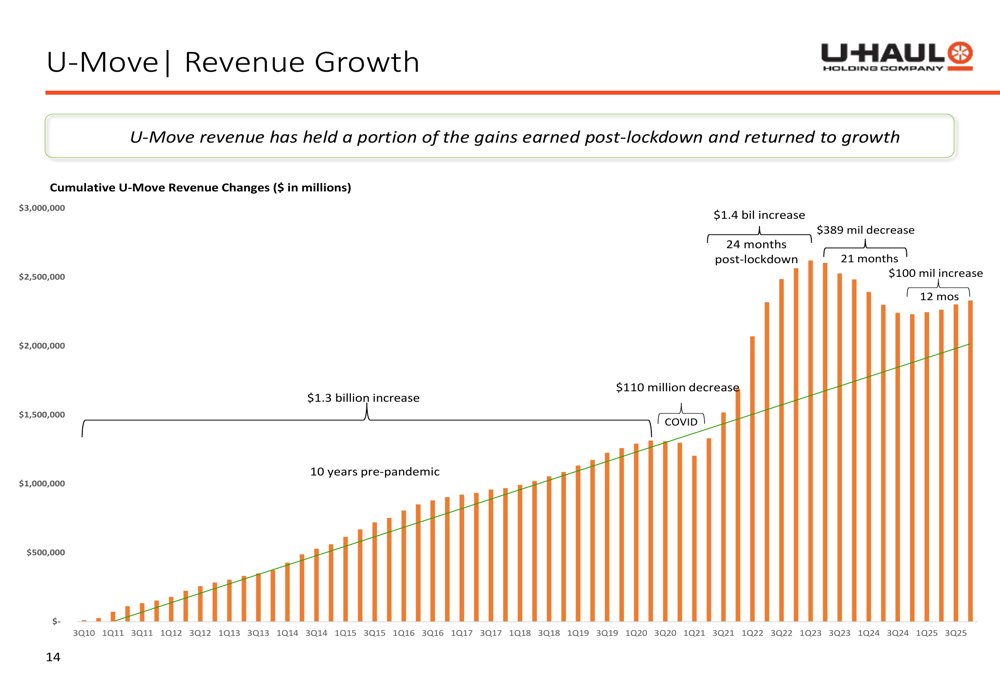

U-Haul’s fourth quarter showed revenue growth across its main business segments. Self-moving equipment rental revenues increased by $29.0 million (4.0%) compared to the fourth quarter of fiscal 2024, marking the fourth consecutive quarter of steadily improving year-over-year results. For the full fiscal year 2025, U-Move revenues increased by $100.8 million or 2.8%.

As shown in the following chart detailing U-Move revenue growth:

Self-storage revenues also showed strong growth, increasing by $17.8 million (8.4%) compared to the same quarter last year. The total portfolio of occupied rooms increased by 39,197 or 6.8% versus the fourth quarter of fiscal 2024. However, the company experienced a slight decline in occupancy rates, with same-store average monthly occupancy at 91.9% in Q4 FY2025 compared to 92.4% in Q4 FY2024, while total portfolio average monthly occupancy decreased to 77.3% from 79.8%.

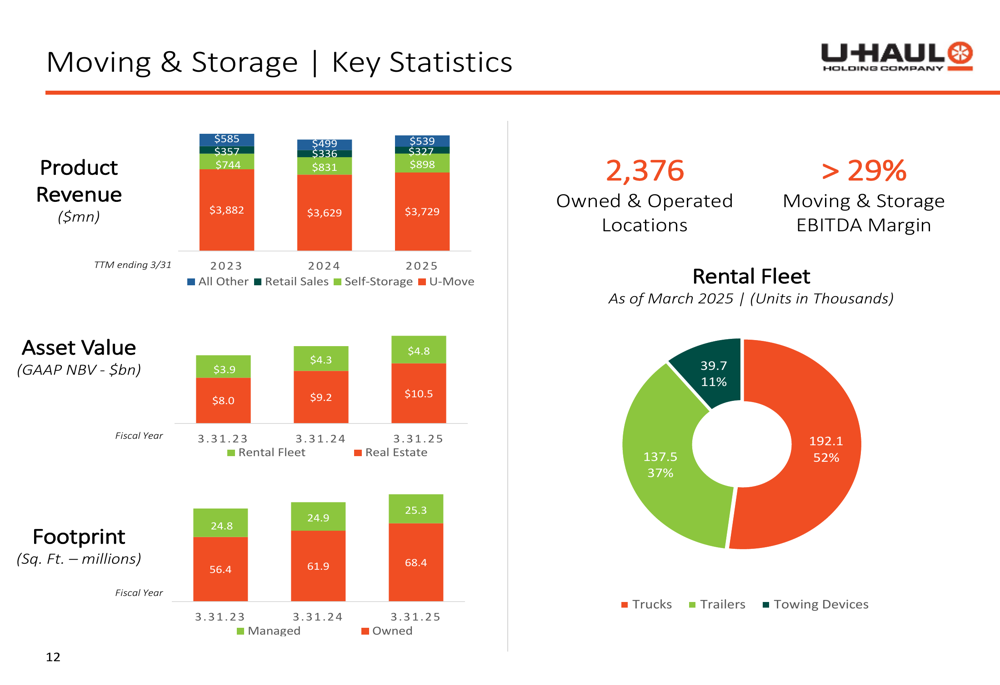

The company’s business model continues to leverage synergies between its moving and storage segments, with nearly 50% of U-Haul self-storage transactions having an associated U-Move transaction.

The following chart illustrates U-Haul’s comprehensive business model with key statistics:

Despite revenue growth, U-Haul reported a net loss of $82.3 million for the quarter, significantly wider than the $863,000 loss reported in the same period last year. This widening loss reflects increased costs in personnel and liability, as well as capital expenditures for new rental equipment.

Strategic Initiatives

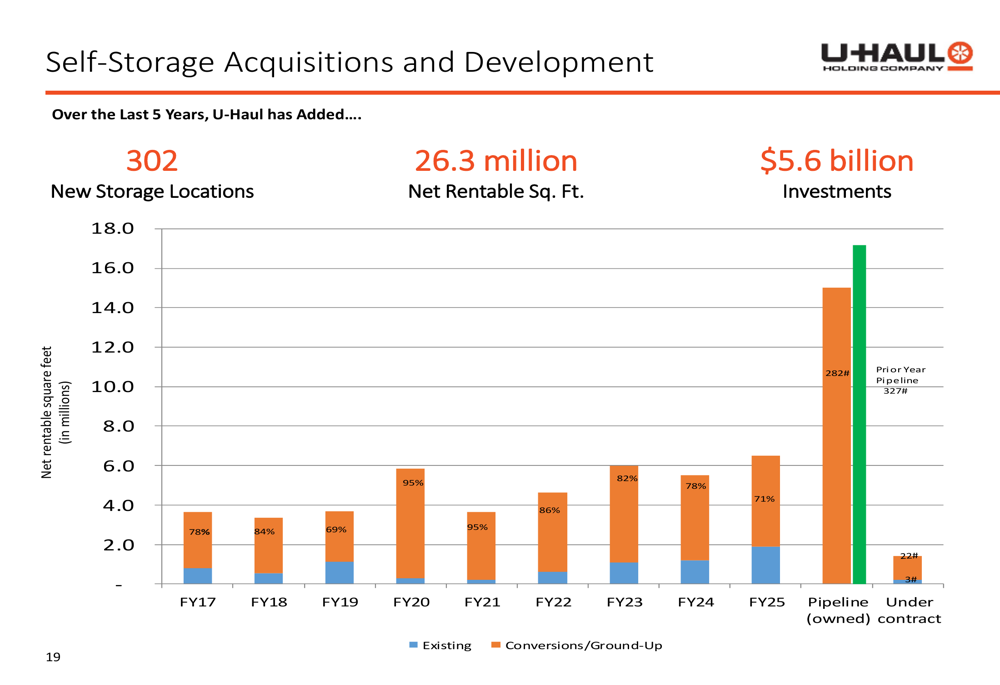

U-Haul continues to focus on expanding its self-storage business, which represents a significant growth opportunity. The company has added 302 new storage locations and 26.3 million net rentable square feet over the past five years, representing investments totaling $5.6 billion.

The following chart illustrates U-Haul’s self-storage acquisition and development activity:

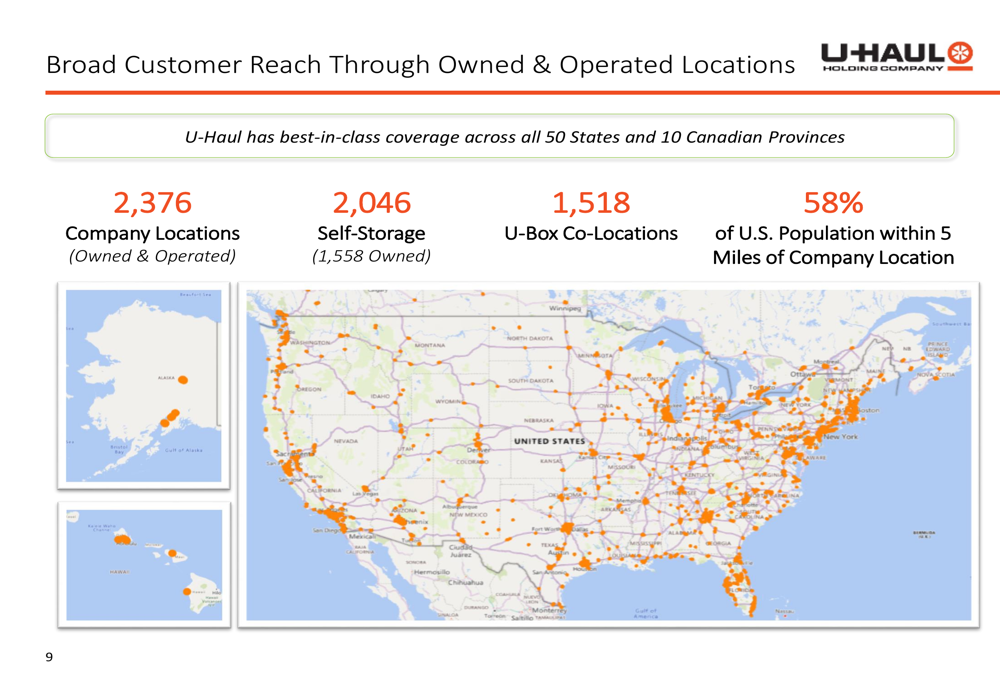

The company’s extensive network provides significant market coverage, with 58% of the U.S. population within 5 miles of a company-owned location and 90% within 5 miles of a U-Haul dealer. This extensive reach is visualized in the following map:

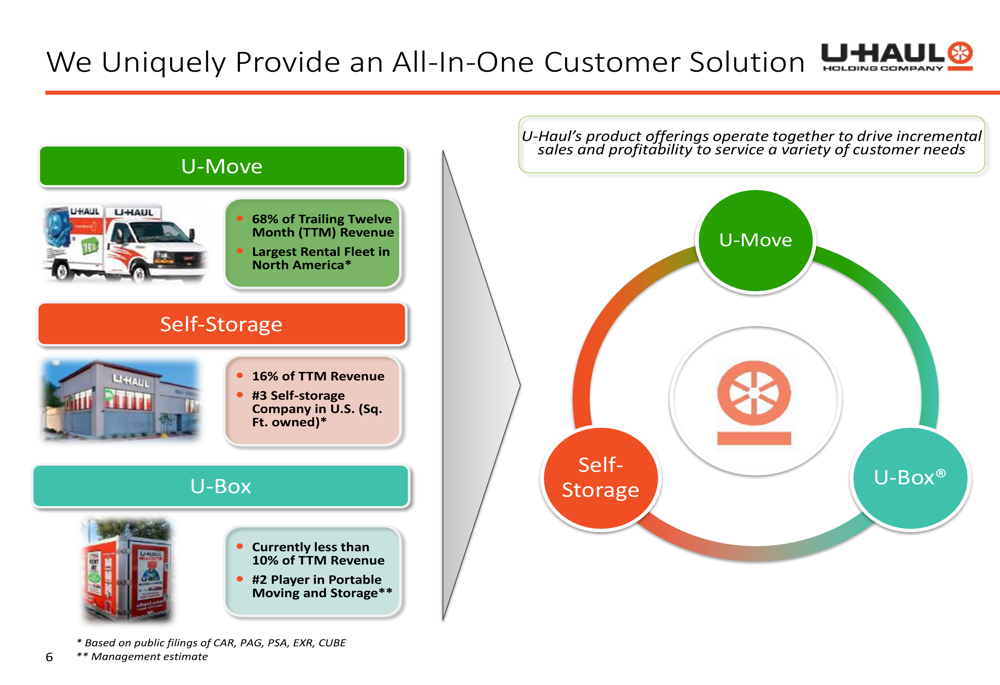

U-Haul’s business model leverages three main product offerings: U-Move (68% of trailing twelve-month revenue), Self-Storage (16%), and U-Box (less than 10%). This integrated approach provides customers with a comprehensive solution for their moving and storage needs.

As shown in the following illustration of U-Haul’s customer solution:

Detailed Financial Analysis

While U-Haul continues to generate substantial revenue, its financial leverage has increased over time. The company’s debt-to-assets ratio stood at 41.1% as of March 31, 2025, with total debt of $7.19 billion against total assets of $17.52 billion. Net leverage has increased from 2.4x in fiscal 2021 to 3.9x in fiscal 2025, reflecting the company’s significant investments in growth initiatives.

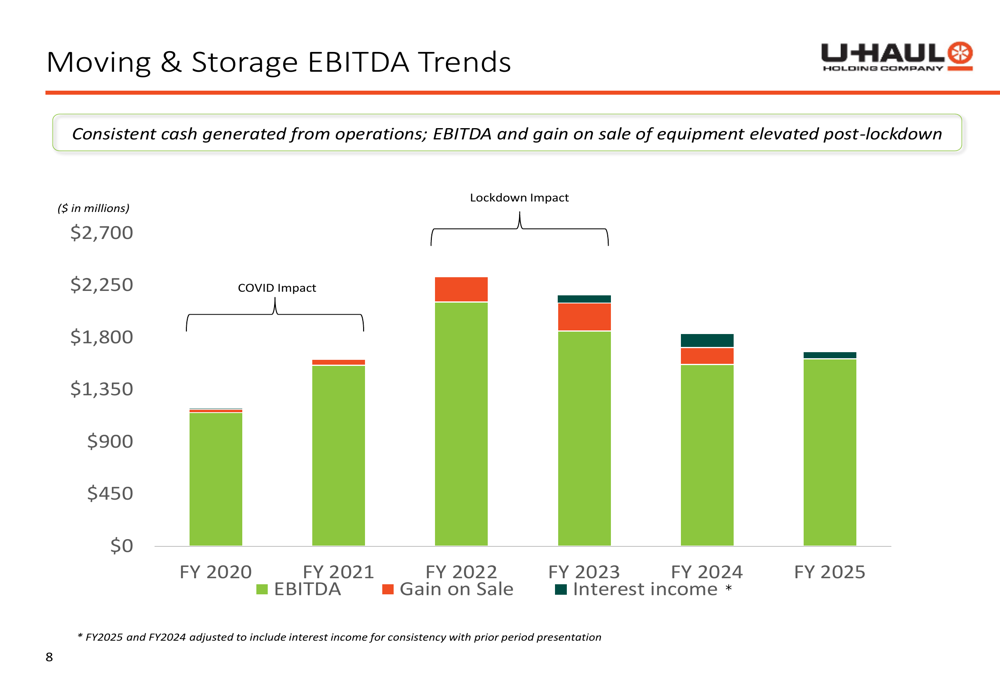

The company’s EBITDA trends show consistent cash generation from operations, though EBITDA has moderated from the elevated levels seen post-lockdown:

U-Haul’s strategic cash deployment for the trailing twelve months ending March 2025 shows significant investments in fleet maintenance and growth capital expenditures. The company generated $2.99 billion in operating cash flows while allocating substantial capital to growth initiatives.

According to the earnings call, U-Haul projects net fleet capital expenditures for FY2026 at $2.95 billion, indicating continued investment in its rental fleet despite financial pressures. This aligns with the company’s long-term focus on maximizing value through continued expansion and improvement of its product offerings.

Forward-Looking Statements

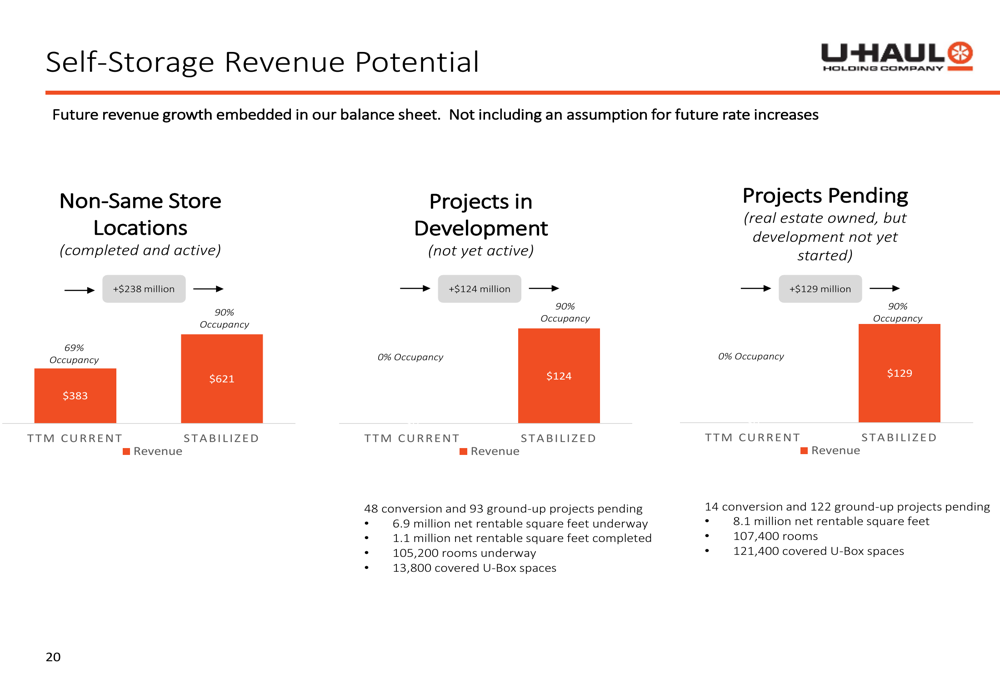

U-Haul sees significant future revenue potential embedded in its balance sheet. The company projects additional revenue of $238 million from non-same store locations when they reach stabilized occupancy of 90%. Projects in development and pending projects are expected to contribute an additional $124 million and $129 million in revenue, respectively, once completed and stabilized.

The following chart illustrates this revenue potential:

Despite these growth opportunities, U-Haul faces challenges with rising liability and personnel costs impacting profitability. According to InvestingPro data, the company is experiencing negative free cash flow yield of -18%, although it remains profitable over the trailing twelve months.

During the earnings call, Chairman Joe Schoen emphasized the persistent consumer need for moving services, stating, "Moving is a need for the consumer. That continues." Management expressed confidence in the company’s valuation, suggesting that greater market understanding of U-Haul’s business model could lead to higher valuations.

U-Haul’s self-storage growth compares favorably to competitors, with a 49% increase in rentable square feet compared to 31-34% for major competitors like Public Storage (NYSE:PSA) and CubeSmart (NYSE:CUBE). This aggressive expansion strategy positions the company for potential future growth but also contributes to its current financial pressures.

As U-Haul continues to balance growth investments with profitability concerns, investors will be watching closely to see if the company’s expansion strategy translates into improved financial performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.