U.S. stocks edge higher with consumer sentiment data, AI boom in focus

Introduction & Market Context

UMB Financial Corporation (NASDAQ:UMBF) released its first quarter 2025 results on April 29, showcasing the initial impact of its recently completed acquisition of Heartland Financial (NASDAQ:HTLF). The quarter marks a significant transition period for the company, with the acquisition closing on January 31, 2025, as previously announced during the company’s Q4 2024 earnings call.

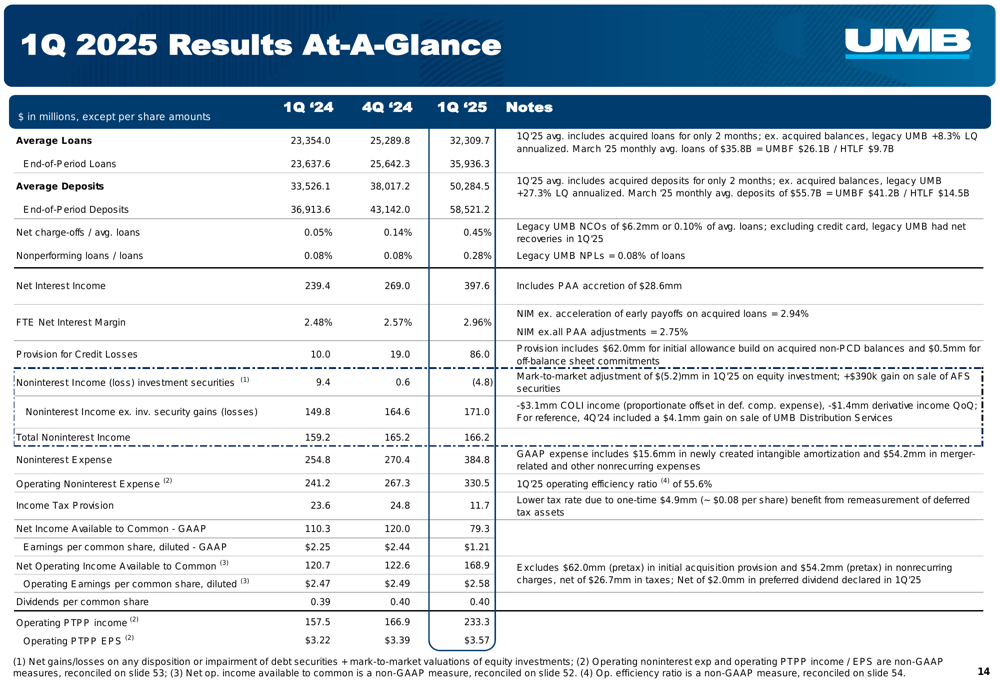

The financial services company reported earnings per share of $1.21 for Q1 2025, a notable decrease from the $2.49 reported in Q4 2024, primarily due to $54.2 million in merger-related and other nonrecurring costs. Despite these short-term expenses, UMB’s presentation emphasized the strategic benefits of the acquisition, which has significantly expanded its geographic footprint and scale.

Acquisition Integration Progress

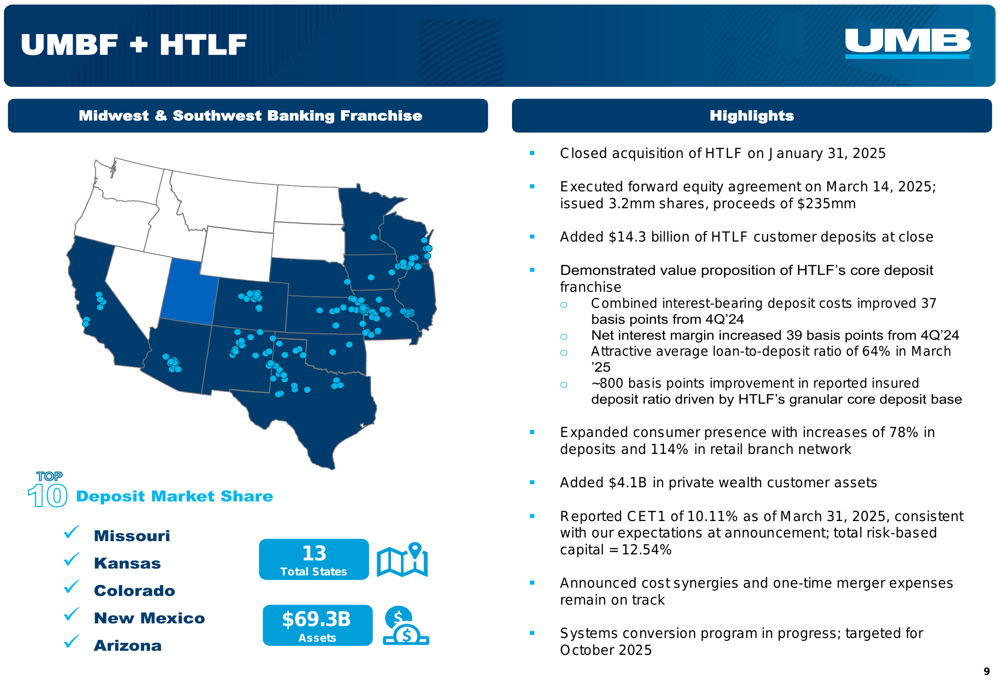

The acquisition of Heartland Financial represents a transformative move for UMB, substantially increasing its asset base and market presence across the Midwest and Southwest regions. The company closed the acquisition on January 31, 2025, and subsequently executed a forward equity agreement on March 14, 2025, issuing 3.2 million shares for proceeds of $235 million to support the transaction.

As shown in the following acquisition highlights, UMB added $14.3 billion of HTLF customer deposits at close, significantly expanding its banking franchise:

The acquisition has bolstered UMB’s market position, with the company now claiming top 10 deposit market share in Missouri, Kansas, Colorado, New Mexico, and Arizona. Total (EPA:TTEF) assets reached $69.3 billion as of March 31, 2025, with the company maintaining strong capital ratios including a Common Equity Tier 1 ratio of 10.11%.

Purchase accounting adjustments had a significant impact on the quarter’s results. The company recognized $28.6 million in contractual accretion in Q1 2025, with additional accretion projected through 2027:

"First quarter 2025 expense included $54.2 million in total merger-related and other nonrecurring costs," the company noted in its presentation, highlighting the short-term impact on profitability.

Quarterly Performance Highlights

UMB’s first quarter 2025 results reflect both the impact of the acquisition and the company’s underlying performance. The presentation provided a comprehensive overview of key financial metrics:

Net income available to common shareholders was $79.3 million for Q1 2025, with diluted earnings per share of $1.21. The company reported total revenue of $563.8 million, including net interest income of $397.6 million and noninterest income of $166.2 million.

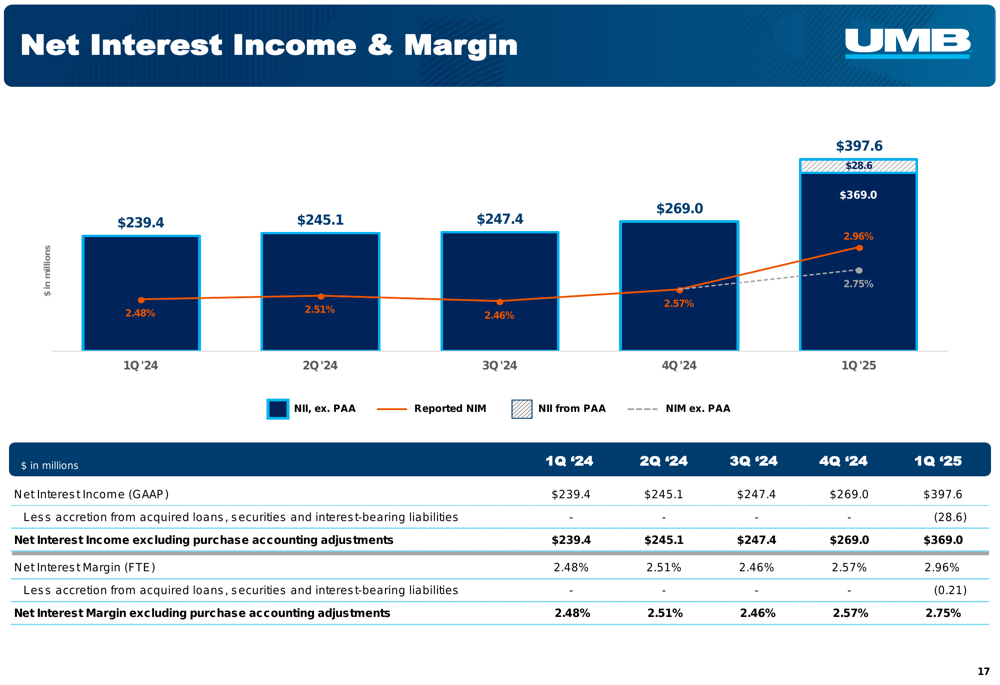

Net interest margin (NIM) was 2.96% for the quarter, or 2.75% excluding purchase accounting adjustments, representing an improvement from the 2.57% reported in Q4 2024. This expansion in margin reflects both acquisition impacts and the company’s ongoing asset-liability management strategies.

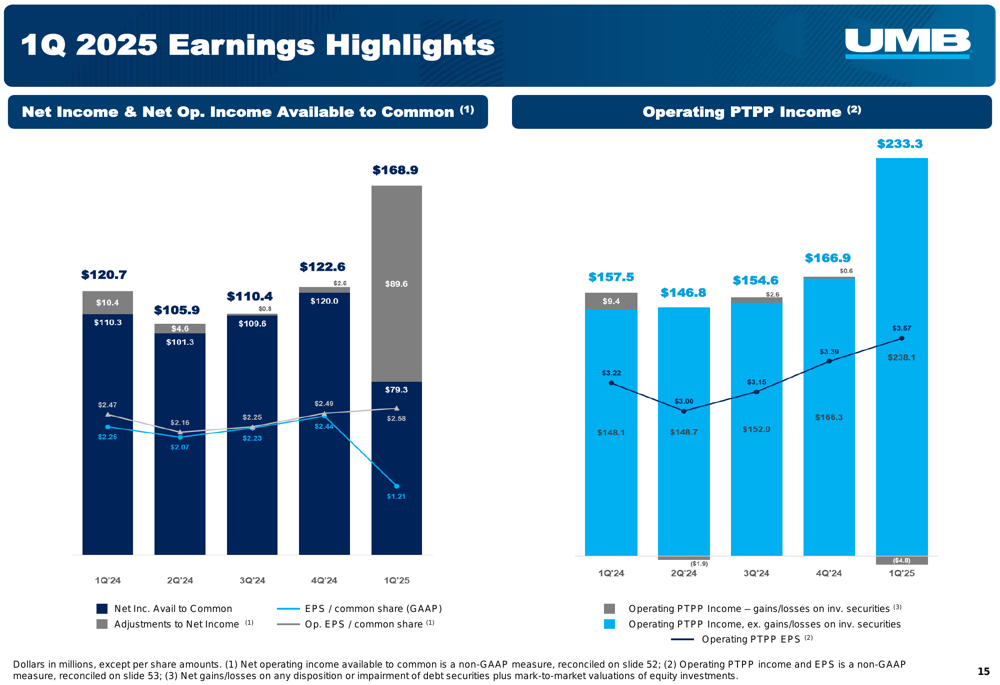

The following chart illustrates UMB’s earnings trends, showing the impact of the acquisition on reported results:

Detailed Financial Analysis

UMB’s net interest income reached $397.6 million in Q1 2025, or $369.0 million excluding purchase accounting adjustments. The company’s presentation highlighted the positive impact of the acquisition on net interest margin:

Noninterest income increased $1.0 million to $166.2 million for Q1 2025, representing 29.5% of total revenue. This diversified revenue stream has been a historical strength for UMB, providing stability across different interest rate environments.

On the expense side, noninterest expense increased $114.4 million to $384.8 million on a GAAP basis, primarily due to the HTLF acquisition. Excluding merger-related and other nonrecurring costs of $54.2 million, adjusted noninterest expense was $316.0 million.

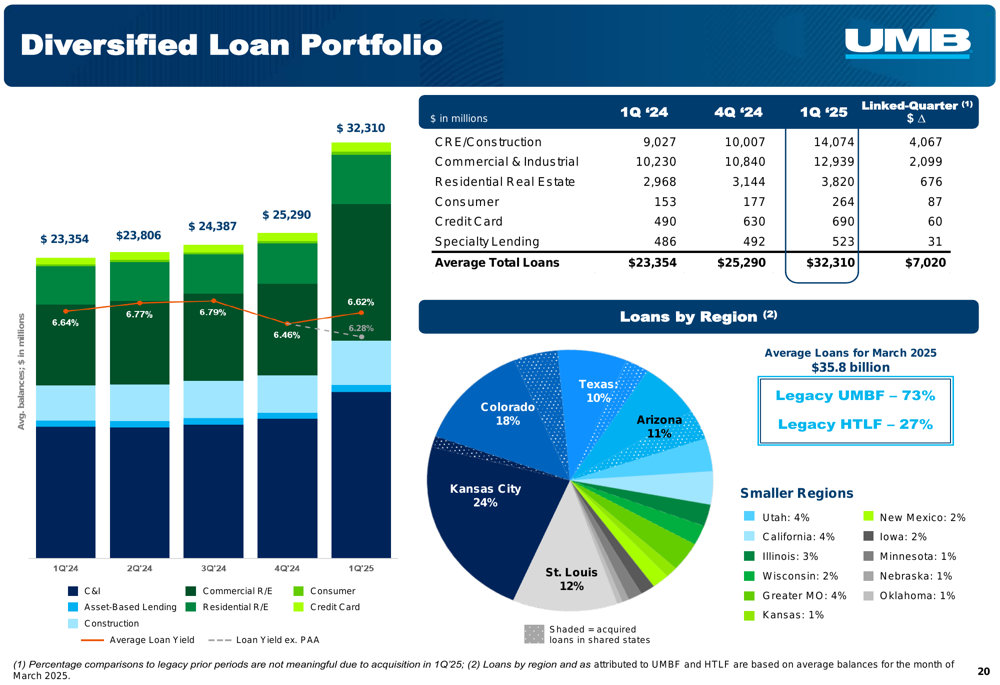

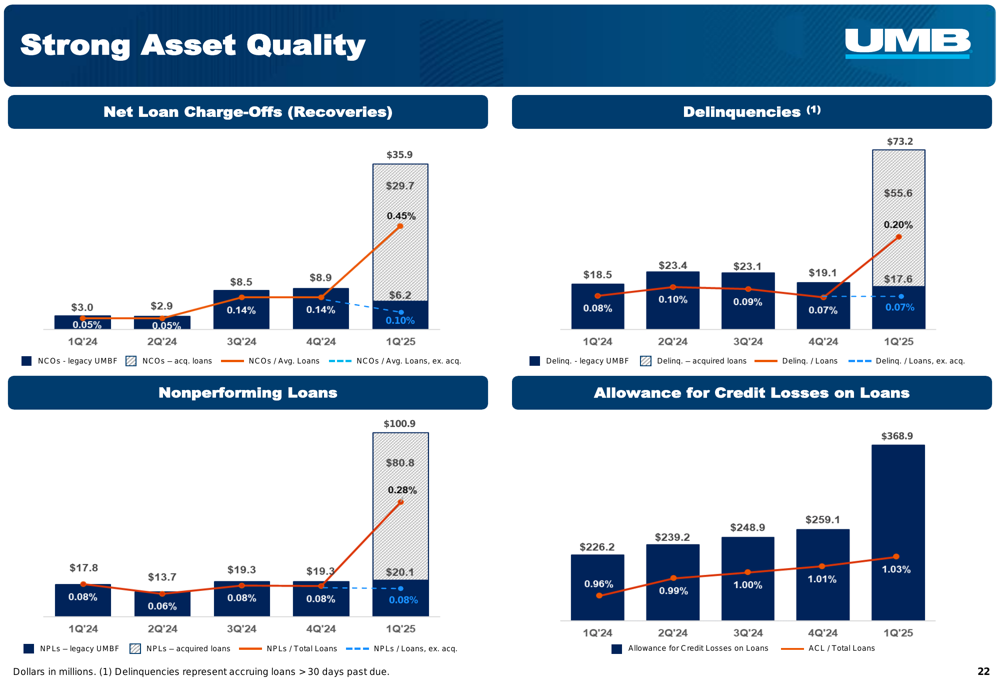

Asset Quality and Loan Portfolio

Despite the significant expansion of its loan portfolio through the acquisition, UMB maintained strong asset quality metrics. The company’s diversified loan portfolio totaled $35.9 billion as of March 31, 2025, with a healthy mix across commercial real estate, commercial and industrial, and residential real estate segments:

Net loan growth for the quarter was $10.3 billion, including $9.8 billion from acquired loans. Organic loan production was $1.2 billion, demonstrating continued growth momentum in UMB’s core lending activities.

Asset quality remained strong, with differentiated metrics between legacy UMB and the total portfolio:

The net loan charge-off ratio was 0.45% for the total portfolio, but only 0.10% for legacy UMB loans. Similarly, the nonperforming loan ratio was 0.28% for the total portfolio, compared to just 0.08% for legacy UMB. The allowance for credit losses to total loans stood at 1.03% as of March 31, 2025.

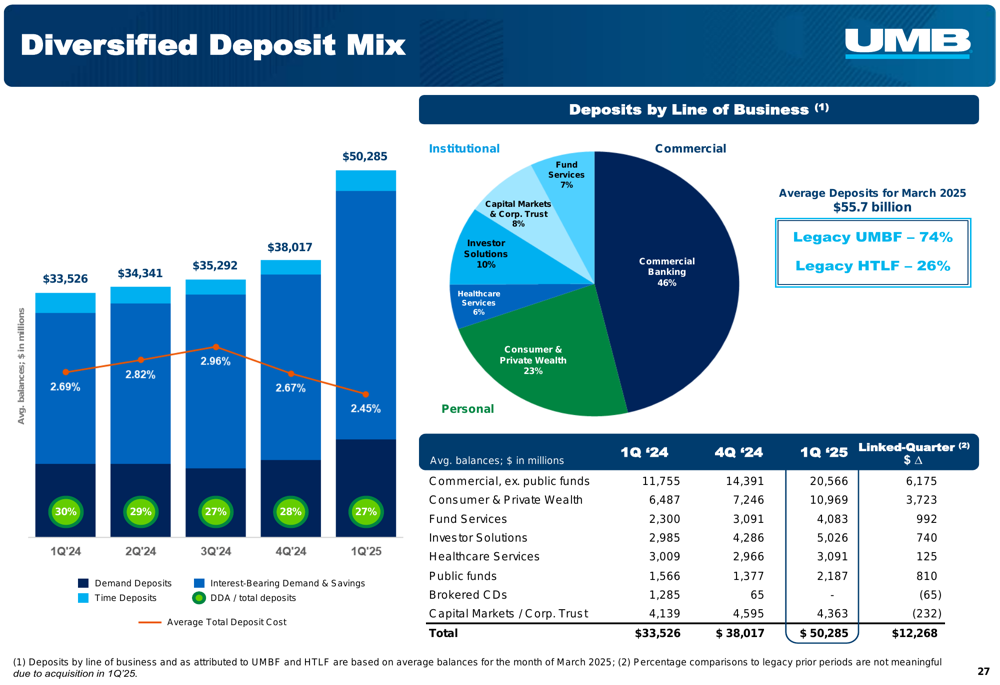

Deposit Base and Funding

UMB’s deposit base expanded significantly with the acquisition, with average deposits reaching $55.7 billion in March 2025. The company emphasized its diversified deposit mix across business lines and deposit types:

The presentation highlighted that no commercial sector represents more than 5% of total deposits, and 52% of deposit accounts have been with the company for over 10 years, underscoring the stability of UMB’s funding base.

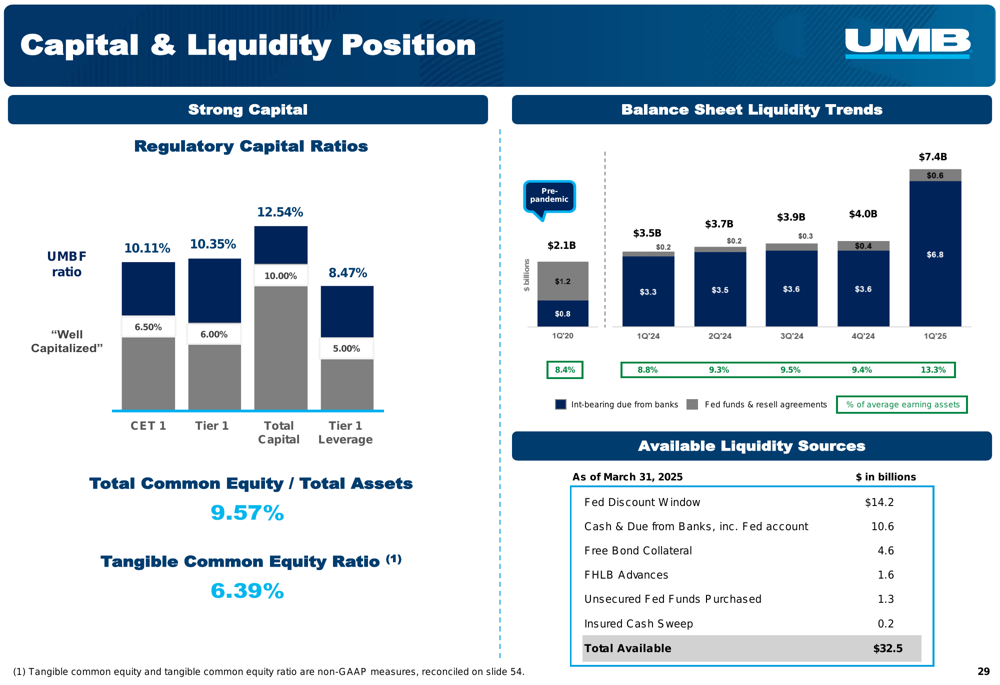

Capital Position and Liquidity

Despite the substantial acquisition, UMB maintained strong capital and liquidity positions:

The Common Equity Tier 1 ratio stood at 10.11%, while the total risk-based capital ratio was 12.54%. The company reported $32.5 billion in total available liquidity sources, providing ample flexibility for future growth opportunities.

Strategic Outlook

UMB’s presentation emphasized its diverse business model as a key strength, with operations spanning commercial, consumer, private wealth, and institutional banking services. The acquisition has enhanced the company’s scale and geographic reach, creating new opportunities for cross-selling and market penetration.

The company projects continued accretion benefits from the acquisition, with $33.0 million expected in Q2 2025, rising to $35.5 million in Q3 2025 before gradually declining. Total projected contractual accretion for 2026 and 2027 is $116.1 million and $93.5 million, respectively.

For 2025, UMB projects a dividend of $1.60 per share, reflecting its commitment to returning value to shareholders while maintaining capital for growth initiatives.

Forward-Looking Statements

While UMB’s presentation highlighted the strategic benefits of the HTLF acquisition, investors should note the near-term earnings pressure from integration costs. The stock closed at $95.93 on April 29, 2025, with after-hours trading at $97.00, down from the $122.56 reported after Q4 2024 earnings.

The company faces challenges in fully integrating HTLF’s operations and realizing projected synergies, while also managing potential credit quality differences between the legacy and acquired loan portfolios. However, UMB’s historically strong asset quality metrics and diversified business model position it well to navigate these challenges.

As the integration progresses, investors will be watching for improvements in operating efficiency and the realization of revenue synergies across the expanded footprint, which could drive long-term value creation despite the short-term costs.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.