NextEra Energy stock rises after Google power deal report

Introduction & Market Context

Unisys Corporation (NYSE:UIS) released its first quarter 2025 financial results on April 30, 2025, revealing a significant revenue decline but showing improvements in cash flow and new business metrics. The company’s stock rose 2.64% to $4.08 following the earnings announcement, as investors responded positively to better-than-expected earnings per share results and maintained full-year guidance.

Despite reporting a revenue decline of 11.4% year-over-year, Unisys beat earnings expectations with a non-GAAP EPS of -$0.05, significantly better than the forecasted -$0.21. This performance, coupled with strong new business signings, suggests potential for recovery in the second half of the year.

Quarterly Performance Highlights

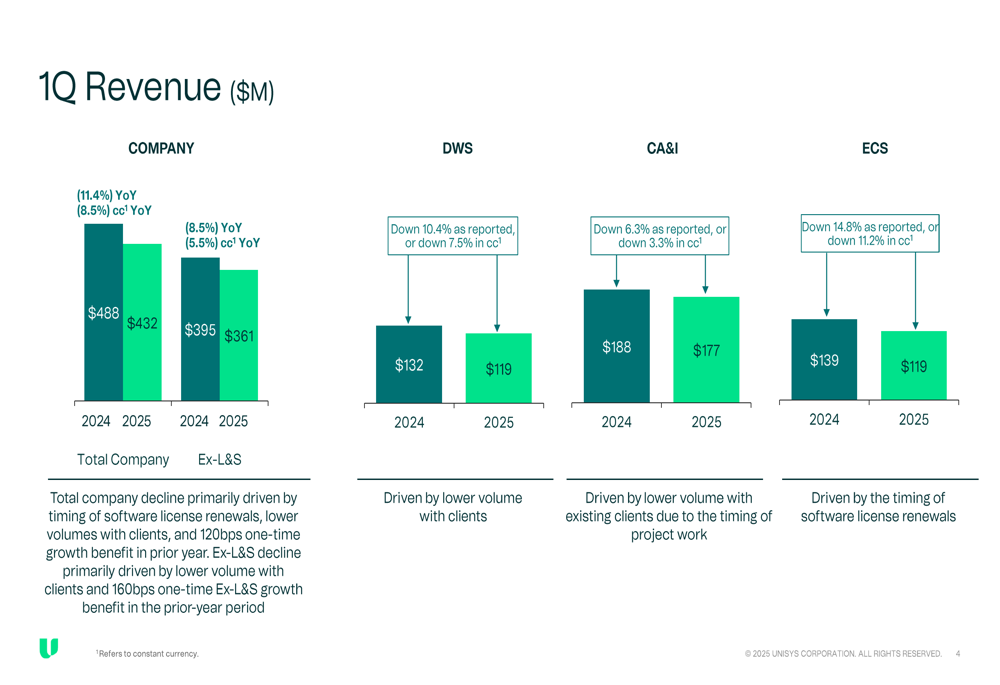

Unisys reported first-quarter revenue of $432.1 million, down 11.4% year-over-year (8.5% in constant currency). The company attributed this decline primarily to the timing of software license renewals in its Enterprise Computing Solutions (ECS) segment and lower volumes with existing clients in other segments.

As shown in the following quarterly revenue breakdown by segment:

Despite the overall revenue decline, Unisys highlighted several positive metrics, including a 17% year-over-year increase in Total (EPA:TTEF) Contract Value (TCV) to $434 million and an impressive 83% growth in Ex-License & Support (Ex-L&S) New Business TCV to $337 million, driven by new logo signings.

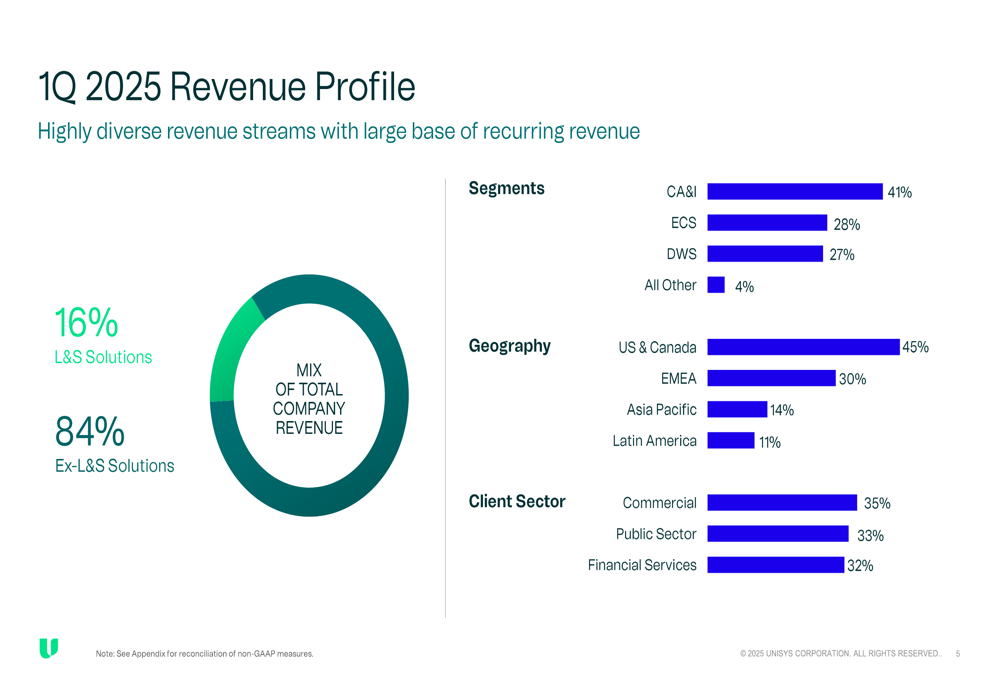

The company’s revenue profile for Q1 2025 shows a diversified business across segments, geographies, and client sectors:

Detailed Financial Analysis

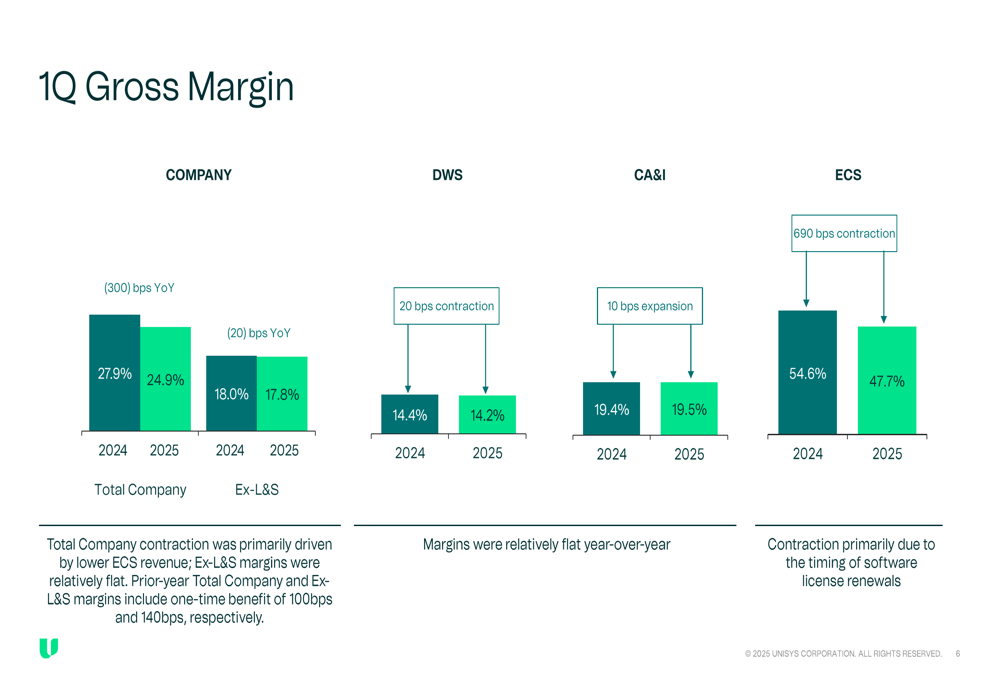

Gross margin for the quarter was 24.9%, down 300 basis points year-over-year, primarily due to the timing of software license renewals in the high-margin ECS segment. Excluding License & Support (L&S), gross margin was relatively stable at 17.8%, down just 20 basis points from the prior year.

The segment breakdown of gross margins shows the significant impact of lower ECS revenue on overall profitability:

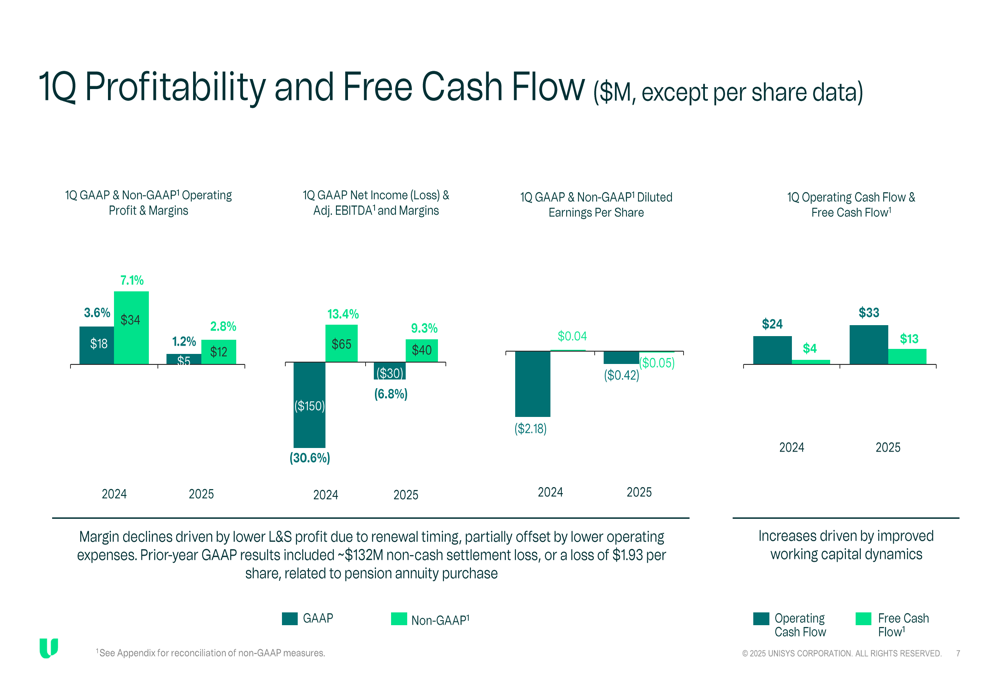

Despite margin pressure, Unisys showed improvement in cash flow metrics. Operating cash flow increased to $33.3 million from $23.8 million in the prior year period, while free cash flow rose to $13.2 million from $3.9 million. Pre-pension free cash flow reached $22.6 million, up $11 million year-over-year.

The following chart illustrates the company’s profitability and cash flow performance:

Strategic Initiatives

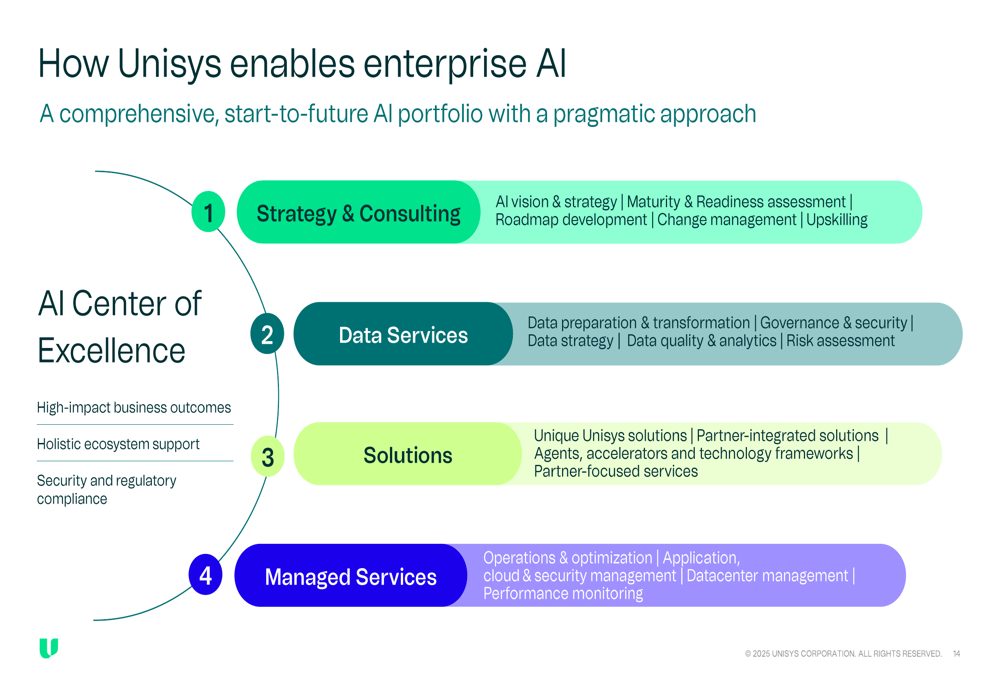

Unisys continues to execute its transformation strategy, focusing on AI enablement and modernization of its core platforms. The company’s AI strategy is centered around a comprehensive approach through its AI Center of Excellence:

The company also highlighted its portfolio of offerings across three main solution areas: Cloud, Applications & Infrastructure Solutions; Digital Workplace Solutions; and Enterprise Computing Solutions. This diversified portfolio positions Unisys to address evolving client needs in digital transformation and AI adoption.

As illustrated in the company’s portfolio overview:

A key element of Unisys’ strategy is the continued development of its ClearPath Forward platform, which provides high-margin license and support revenue. While this segment saw a decline in Q1, the company increased its full-year 2025 L&S revenue expectations to $410 million, up from the previous estimate of $390 million.

Forward-Looking Statements

Despite the Q1 revenue challenges, Unisys maintained its full-year 2025 guidance, projecting revenue growth of 0.5% to 2.5% in constant currency and a non-GAAP operating profit margin of 6.5% to 8.5%. This guidance suggests confidence in a stronger performance in the second half of the year.

The company’s full-year guidance and assumptions are detailed below:

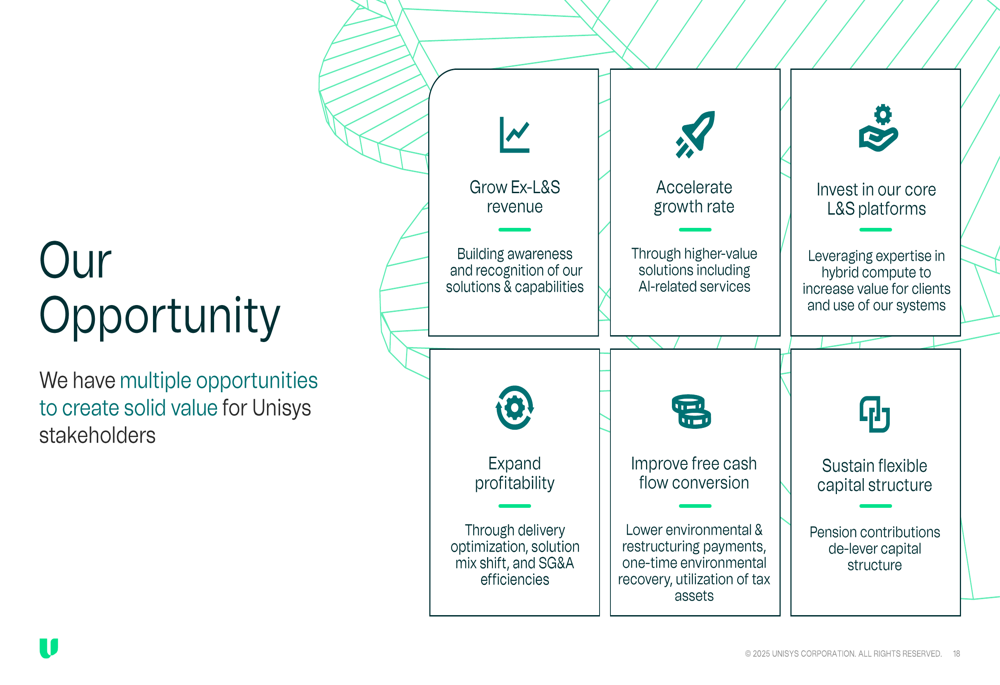

Unisys outlined its opportunity areas for future growth, focusing on expanding Ex-L&S revenue, accelerating growth through AI-related services, and improving profitability through delivery optimization and SG&A efficiencies:

Conclusion

While Unisys faced significant revenue headwinds in Q1 2025, the company’s improved cash flow metrics, strong new business signings, and maintained full-year guidance suggest potential for recovery in upcoming quarters. The strategic focus on AI enablement and continued investment in the high-margin ClearPath Forward platform provide a foundation for future growth.

Investors responded positively to the results, with the stock rising despite the revenue decline, reflecting confidence in the company’s ability to execute its transformation strategy and deliver improved performance in the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.