Intellia stock tumbles after pausing gene therapy trials on safety concerns

Introduction & Market Context

Valaris Limited (NYSE:VAL) presented its Q2 2025 investor deck on July 31, highlighting its position as the world’s largest offshore drilling contractor by fleet size. The presentation emphasized the company’s strategic focus on high-specification assets amid growing demand for offshore drilling services, particularly in deepwater markets.

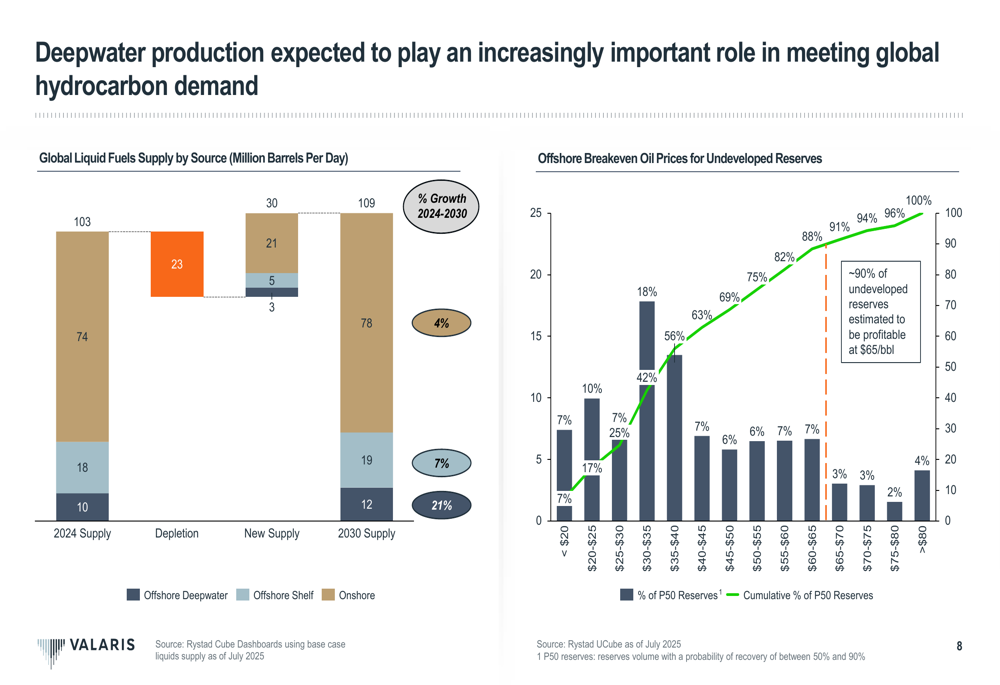

According to the company’s presentation, offshore deepwater production is expected to play a crucial role in meeting global energy needs, with projections showing continued growth in liquid fuels supply from deepwater sources through 2030.

As shown in the following chart detailing global liquid fuels supply sources, offshore deepwater production is projected to increase from 18 million barrels per day in 2024 to 19 million barrels per day by 2030:

Executive Summary

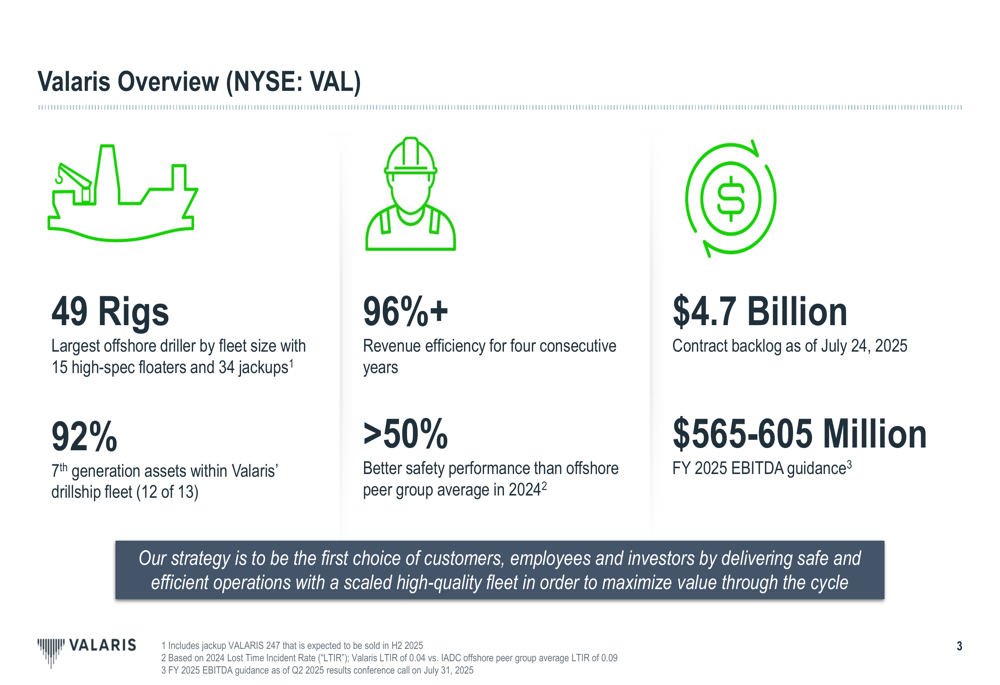

Valaris operates a fleet of 49 rigs, including 15 high-specification floaters and 34 jackups, with a contract backlog of $4.7 billion as of July 24, 2025. The company has provided full-year 2025 EBITDA guidance of $565-605 million, which aligns with the figures reported in its recent Q2 earnings results.

The company’s strategy centers on delivering safe and efficient operations with its high-quality fleet to maximize value throughout market cycles. Valaris has maintained revenue efficiency above 96% for four consecutive years while significantly outperforming industry peers on safety metrics.

This overview slide highlights Valaris’s key operational metrics and market position:

Operational Performance & Fleet Positioning

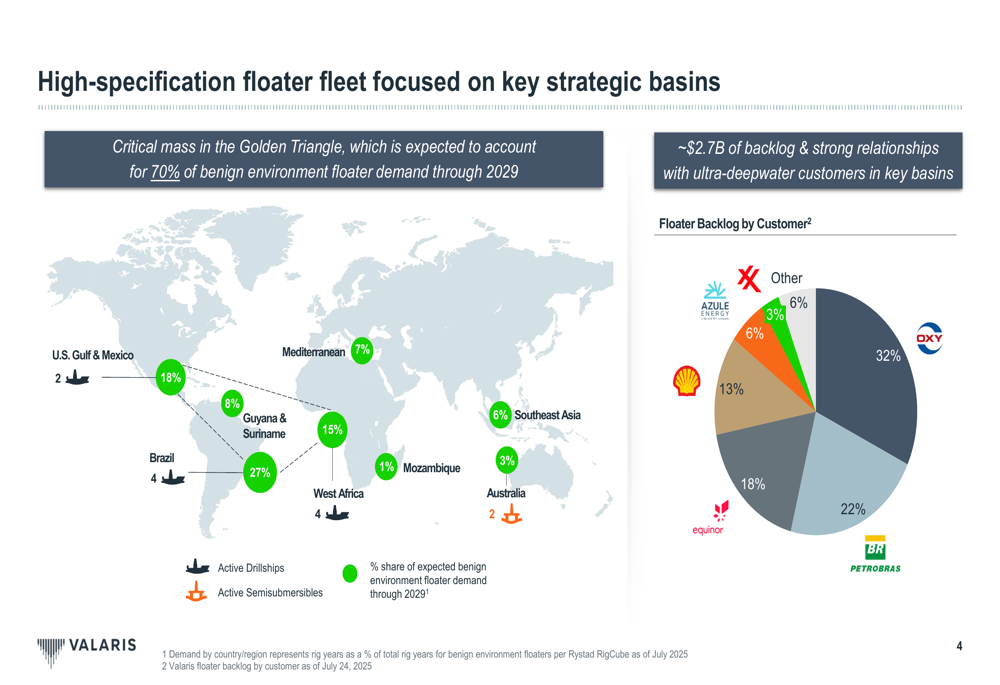

Valaris has strategically positioned its high-specification floater fleet in the "Golden Triangle" regions (Gulf of Mexico, Brazil, and West Africa), which are expected to account for 70% of benign environment floater demand through 2029. The company has secured $2.7 billion in backlog from ultra-deepwater customers in these key basins.

The company’s floater backlog is diversified across major customers, with OXY, Petrobras, and Equinor representing the largest shares:

Valaris has emphasized the technical advantages of its modern fleet, with 92% of its drillship fleet (12 of 13) being 7th generation assets. These advanced rigs feature dual blowout preventers, dual derricks with high hookload capacity, and enhanced thruster capabilities that enable more efficient operations for complex well programs.

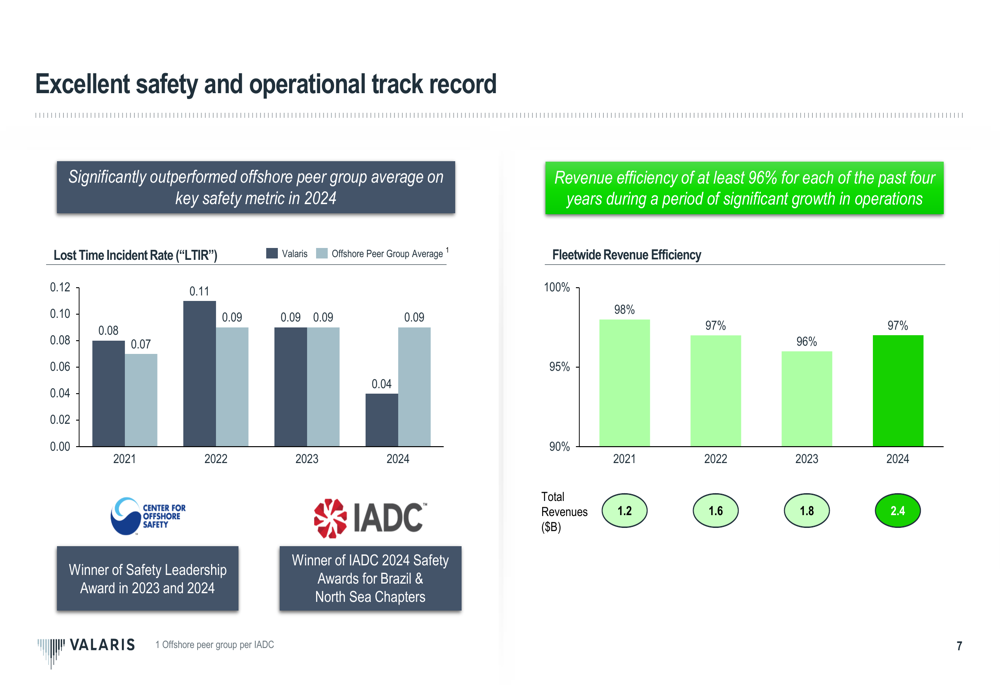

The company has also maintained a strong safety record, significantly outperforming the offshore peer group average on key safety metrics. Its consistent operational excellence is reflected in revenue efficiency of at least 96% for each of the past four years, even as total revenues have doubled from $1.2 billion in 2021 to $2.4 billion in 2024.

The following chart illustrates Valaris’s safety performance and revenue efficiency trends:

Financial Position & Capital Allocation

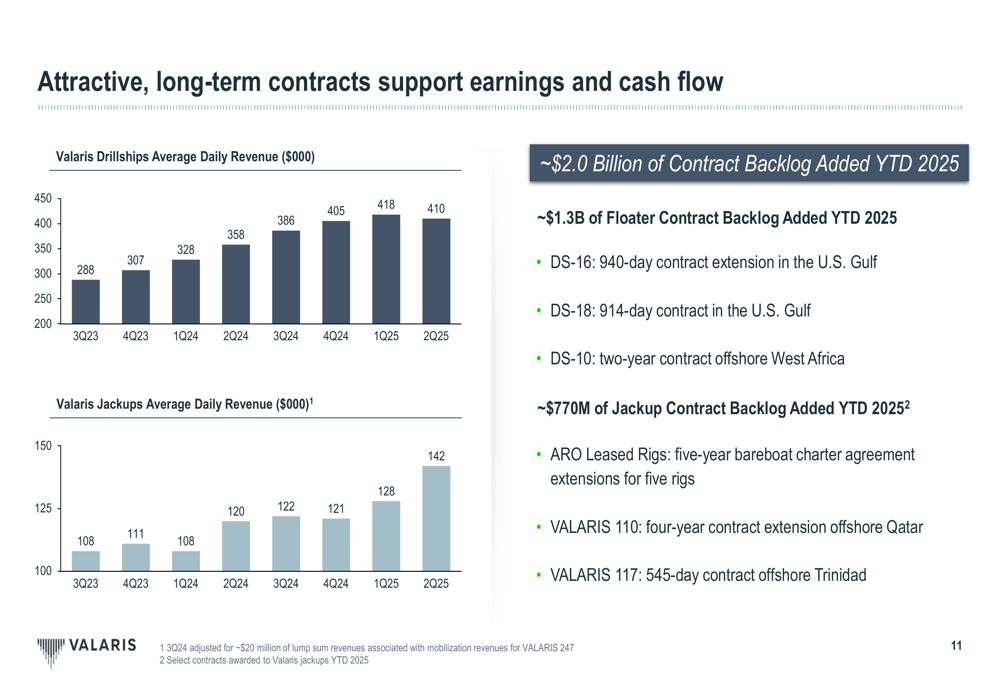

Valaris reported adding approximately $2.0 billion of contract backlog year-to-date in 2025, including $1.3 billion for floaters and $770 million for jackups. The company has seen increasing average daily revenue rates for both its drillships and jackup fleets since Q3 2023.

The contract additions include significant wins such as a 940-day drillship contract extension in the U.S. Gulf, a 914-day drillship contract in the U.S. Gulf, and a two-year drillship contract offshore West Africa. For jackups, the company secured five-year bareboat charter agreement extensions for five rigs and multi-year contracts offshore Qatar and Trinidad.

This chart shows the positive trend in average daily revenue rates for both drillships and jackups:

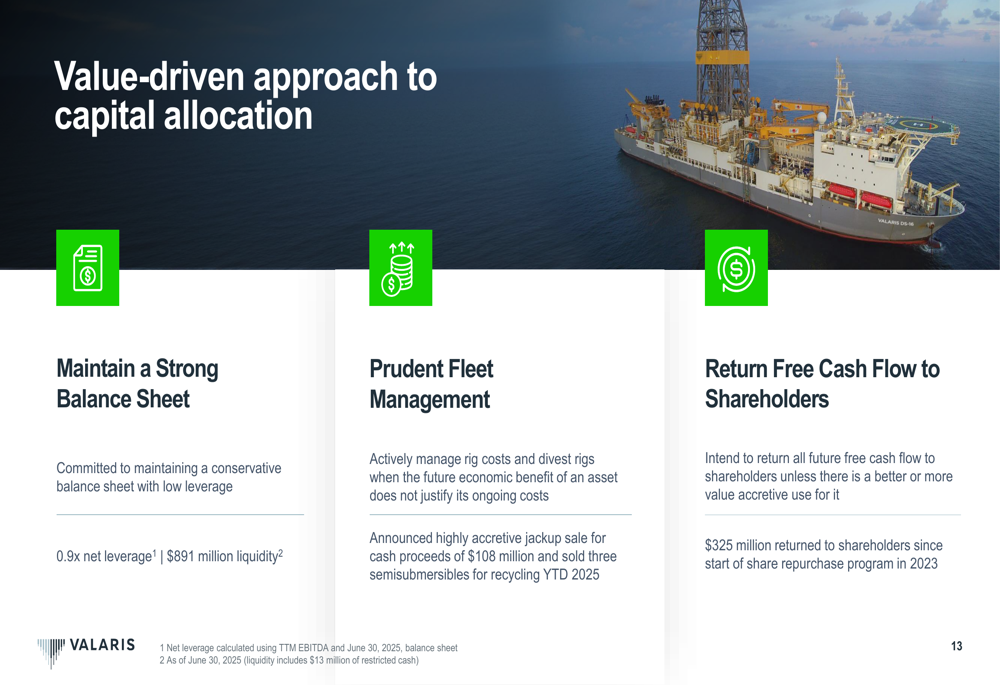

The company’s capital allocation strategy focuses on three key areas: maintaining a strong balance sheet, prudent fleet management, and returning free cash flow to shareholders. Valaris has maintained a conservative financial position with 0.9x net leverage and has returned $325 million to shareholders through share repurchases since 2023.

As part of its fleet management approach, Valaris announced a jackup sale for cash proceeds of $108 million and sold three semisubmersibles for recycling year-to-date in 2025.

Market Outlook & Growth Opportunities

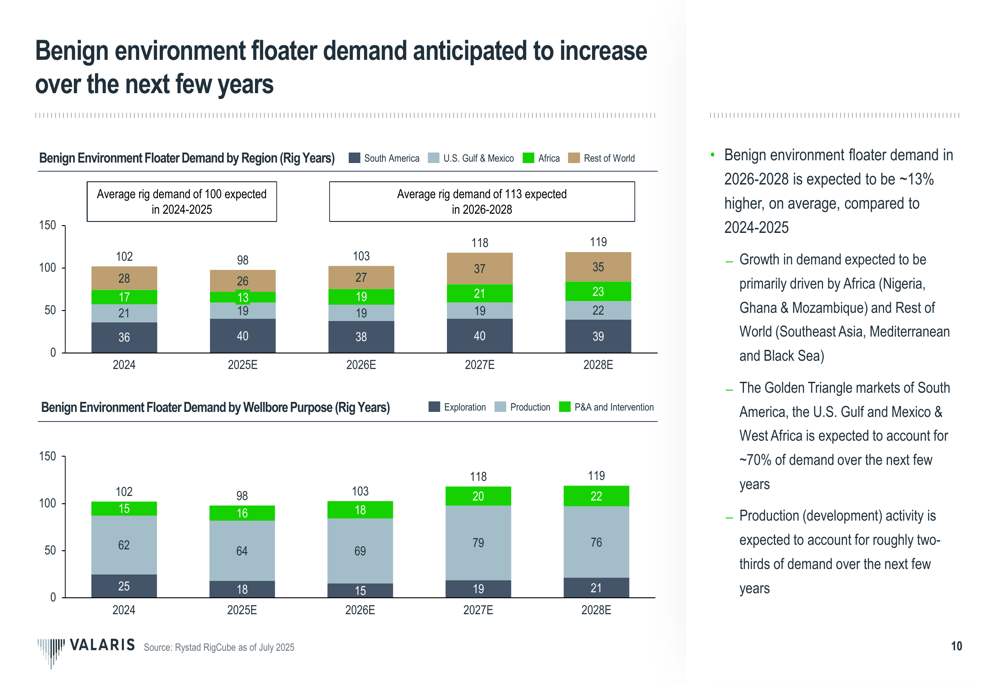

Valaris projects significant growth in offshore drilling demand, particularly in the deepwater segment. According to the presentation, benign environment floater demand is expected to be approximately 13% higher in 2026-2028 compared to 2024-2025, driven by increased exploration and production activities.

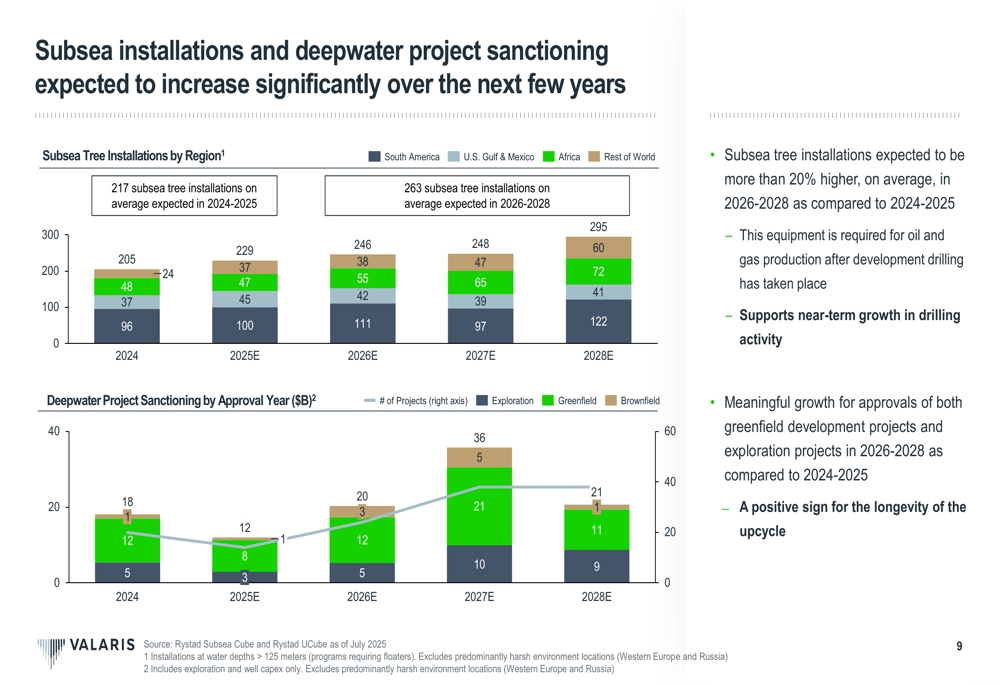

The company also anticipates more than 20% growth in subsea tree installations during 2026-2028 versus 2024-2025, with meaningful growth in approvals for both greenfield development projects and exploration projects.

This chart illustrates the projected increase in benign environment floater demand by region and wellbore purpose:

Supporting this outlook, the presentation highlighted expected growth in deepwater project sanctioning, with the number of projects and investment amounts increasing significantly from 2024 through 2028:

Forward-Looking Statements

Valaris expects offshore production, particularly in deepwater regions, to continue playing an important role in meeting global energy needs. The company believes it is well-positioned to capitalize on this demand with its high-specification fleet and strong operational track record.

According to its Q2 2025 earnings report, Valaris achieved total revenue of $615 million and adjusted EBITDA of $201 million for the quarter. The company’s cash position remains strong with $516 million in cash and cash equivalents and nearly $900 million in total liquidity.

Looking ahead, Valaris intends to focus on securing attractive long-term contracts, actively managing rig costs, and returning all future free cash flow to shareholders, maintaining its commitment to creating long-term value while operating with a conservative financial approach.

The company’s strategy appears well-aligned with market projections showing that approximately 90% of undeveloped offshore reserves are estimated to be profitable at an oil price of $65 per barrel, suggesting continued viability for offshore projects even in moderate price environments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.