TSX futures subdued as gold rally takes a breather

Introduction & Market Context

VAT Group AG (SIX:VACN) reported strong operational performance for the first half of 2025, with sales up 24% year-on-year despite significant foreign exchange headwinds. The company presented its H1 2025 results on July 23, 2025, highlighting robust execution in its semiconductor business amid continued technology transitions and AI-related investments.

The stock closed at CHF 321.40 following the presentation, down 2.6% from its previous close of CHF 330.20, as investors digested the mixed signals of strong operational performance against currency challenges and market uncertainties.

Quarterly Performance Highlights

VAT delivered substantial year-on-year growth in key financial metrics for H1 2025, though order intake showed some softness due to market uncertainties and adverse currency movements.

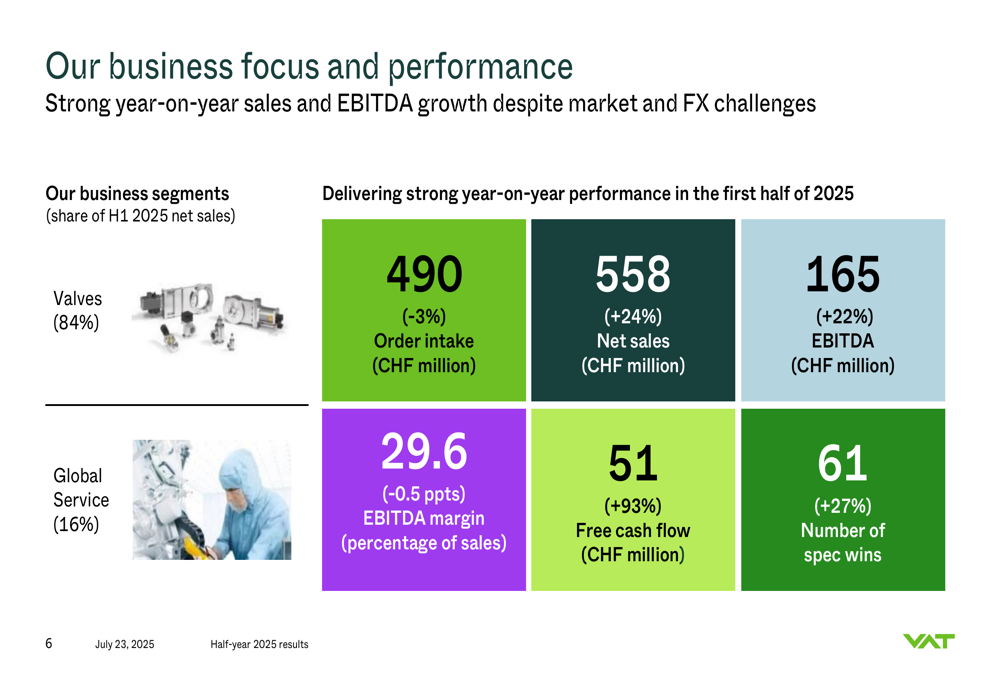

As shown in the following business focus and performance summary, VAT achieved strong growth in sales and EBITDA despite challenging market conditions:

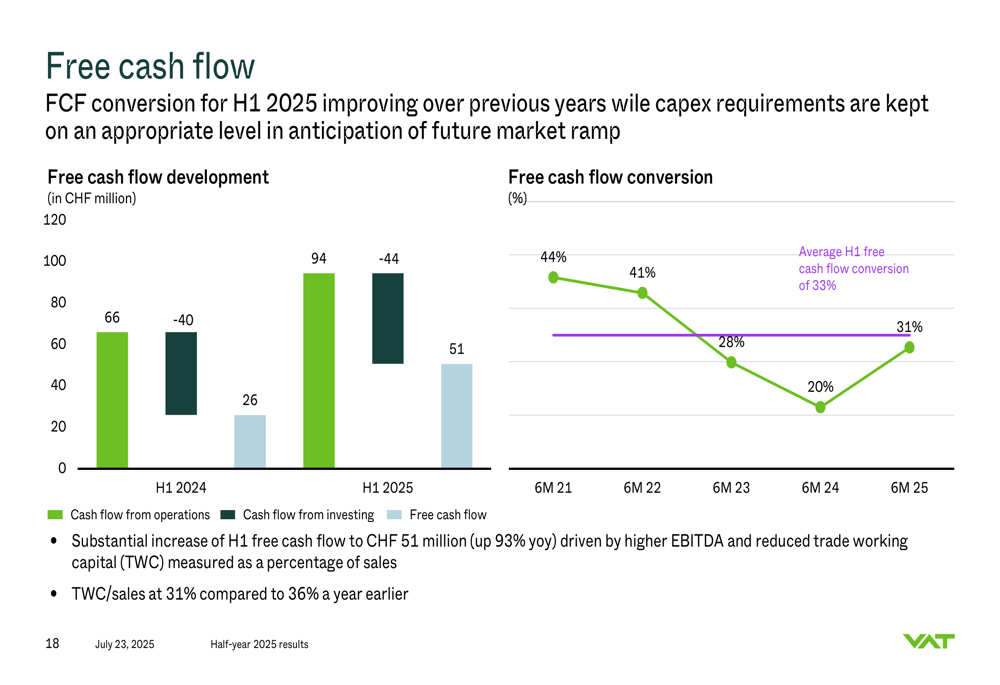

The company reported net sales of CHF 558 million in its Valves segment, representing a 24% increase year-on-year, while EBITDA grew 22% to CHF 165 million. Free cash flow showed remarkable improvement, jumping 93% to CHF 51 million compared to H1 2024.

Order intake remained relatively stable at CHF 489 million, down 3% year-on-year but flat at constant exchange rates. The company noted that customers are demanding shorter lead times and placing fewer advance orders, reflecting ongoing market uncertainties related to tariffs and geopolitical developments.

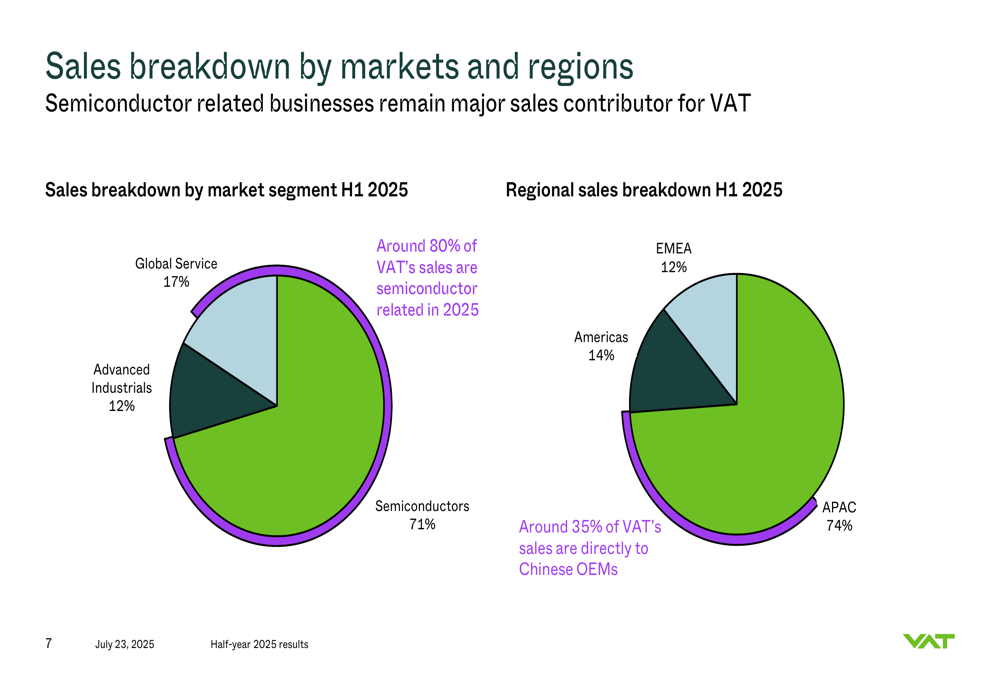

The sales breakdown by market segment and region reveals VAT’s strong position in the semiconductor industry and Asia-Pacific markets:

Semiconductors accounted for 71% of sales, followed by Global Service at 17% and Advanced Industrials at 12%. Geographically, APAC dominated with 74% of sales, while Americas and EMEA contributed 14% and 12% respectively. Notably, around 35% of VAT’s sales are directly to Chinese OEMs, underscoring the importance of this market despite ongoing geopolitical tensions.

Detailed Financial Analysis

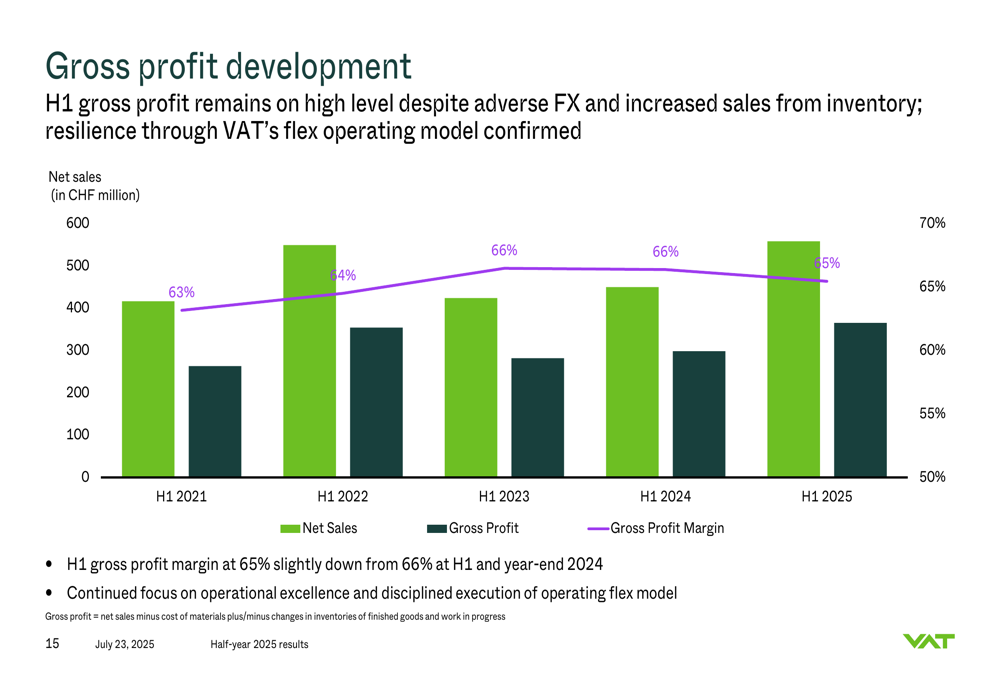

VAT maintained a strong gross profit margin of 65% in H1 2025, slightly down from 66% in the previous year. The company attributed this resilience to its flexible operating model and continued focus on operational excellence.

The following chart illustrates the gross profit development over recent years:

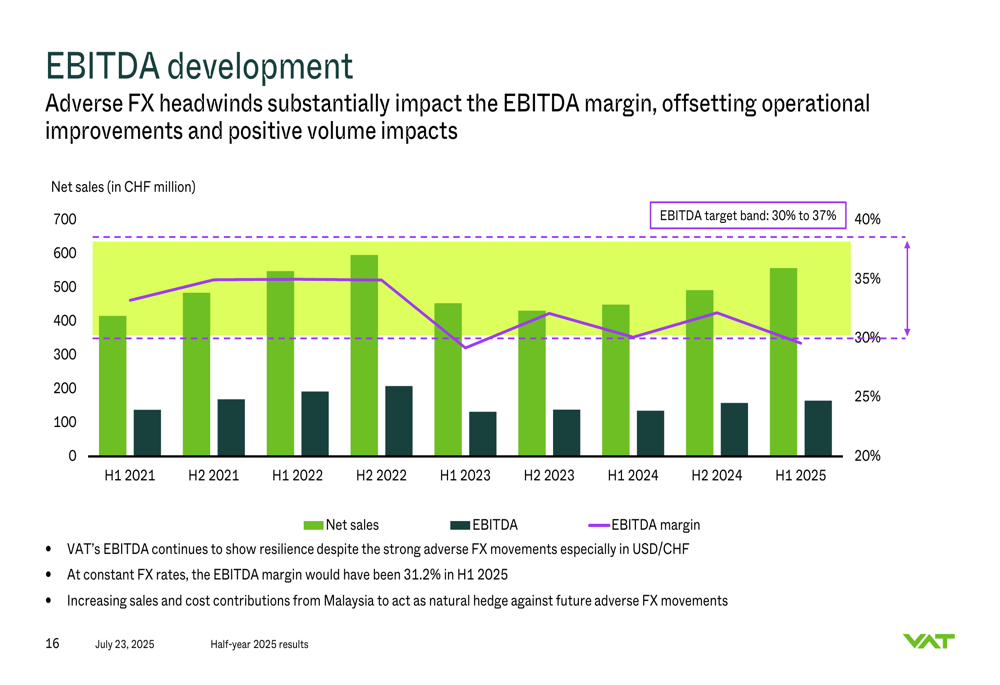

However, EBITDA margin was significantly impacted by adverse foreign exchange movements, particularly in the USD/CHF exchange rate. At constant FX rates, the EBITDA margin would have been 31.2% in H1 2025, compared to the reported 29.6%.

This impact is clearly visible in the EBITDA development chart:

Net income increased by 12% to CHF 105.6 million, though growth was hampered by negative finance results due to revaluation losses on cash balances and intercompany loans. The effective tax rate increased slightly to 18.5% from 18.0% in H1 2024.

Free cash flow showed substantial improvement, reaching CHF 51 million, up 93% year-on-year. This was driven by higher EBITDA and reduced trade working capital as a percentage of sales (31% compared to 36% a year earlier).

Strategic Initiatives

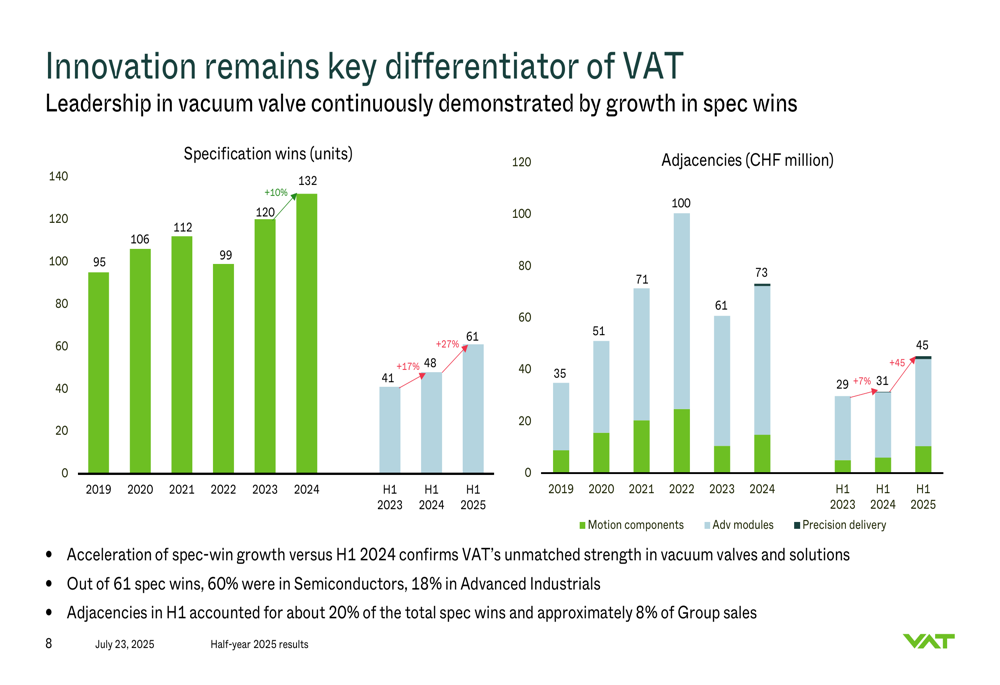

Innovation remains a key differentiator for VAT, with the company reporting a record number of specification wins in the first half of 2025. The company achieved 61 spec wins, up 27% year-on-year, with adjacencies showing particularly strong growth at 45%.

The following chart demonstrates VAT’s consistent track record in innovation:

Out of the 61 specification wins, 60% were in Semiconductors and 18% in Advanced Industrials. Adjacencies accounted for about 20% of total spec wins and approximately 8% of Group sales, highlighting VAT’s successful expansion beyond its core valve business.

The company continues to invest in capacity expansion and operational improvements to support future growth. Key initiatives include the completion of Factory 1B in Penang, Malaysia, the opening of a new factory in Romania, and the successful conclusion of ERP transformation in all production hubs.

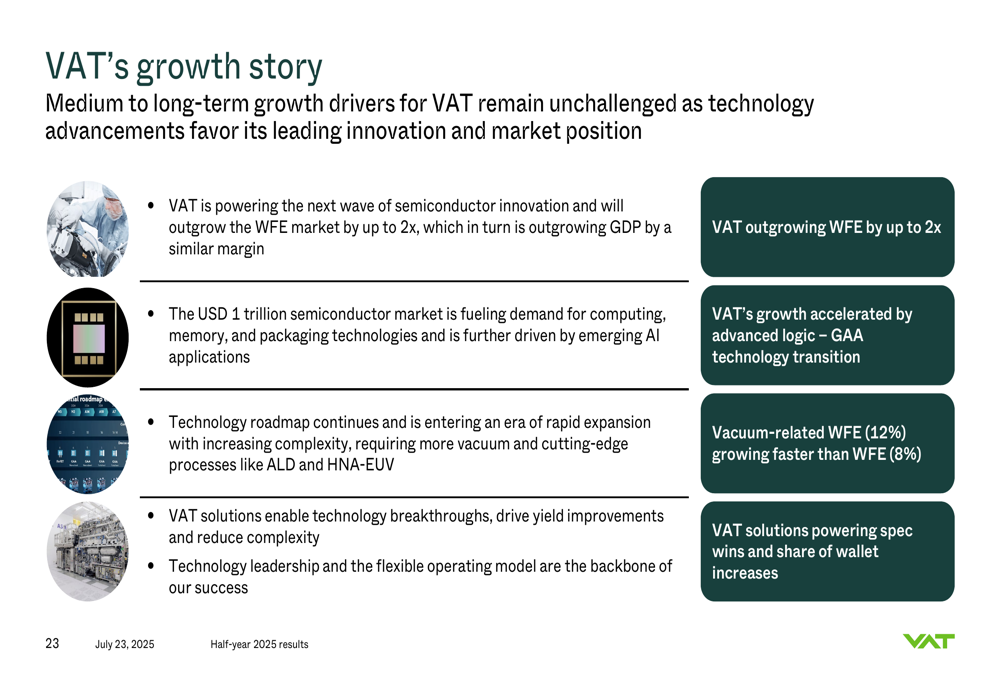

VAT’s growth strategy is firmly anchored in the semiconductor industry’s technology roadmap, with a focus on enabling next-generation chip manufacturing:

Forward-Looking Statements

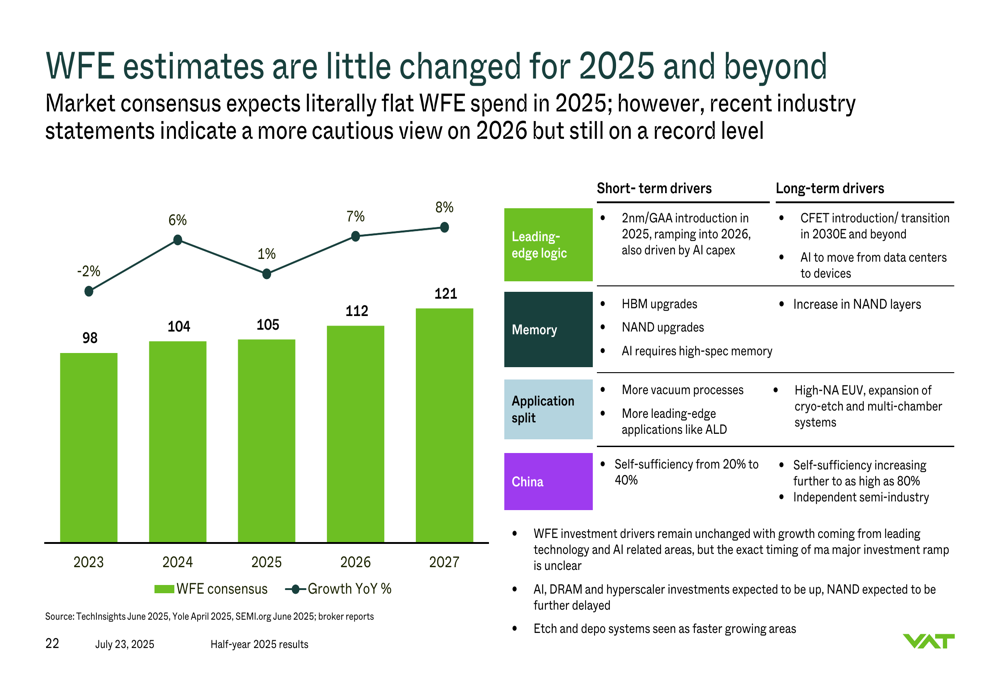

Looking ahead, VAT provided a positive outlook for the remainder of 2025, despite some market uncertainties. The company expects WFE (Wafer Fabrication Equipment) spending to remain at record levels, with consensus forecasts indicating around 1% growth in 2025 followed by stronger growth in 2026 and 2027.

The following chart shows WFE estimates for the coming years:

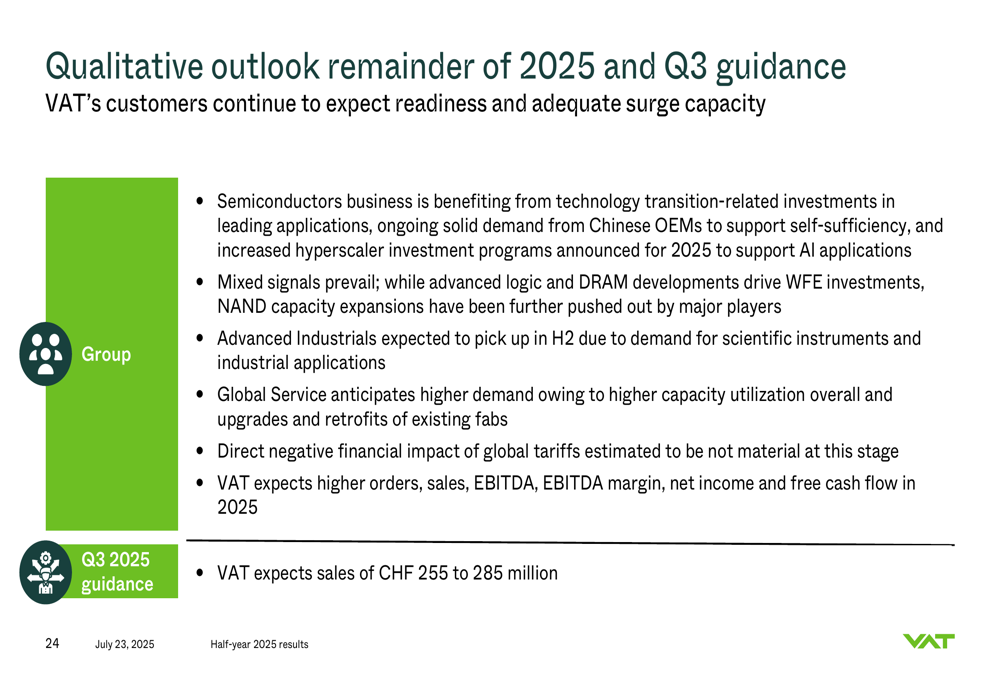

For Q3 2025, VAT expects sales of CHF 255-285 million, indicating continued growth momentum. For the full year 2025, the company anticipates higher orders, sales, EBITDA, EBITDA margin, net income, and free cash flow compared to 2024.

The company highlighted several growth drivers for the remainder of 2025:

The Semiconductors business is expected to benefit from technology transition-related investments in leading applications, ongoing solid demand from Chinese OEMs, and increased hyperscaler investment programs to support AI applications. However, mixed signals persist, with NAND capacity expansions being further delayed by major players.

Advanced Industrials is expected to pick up in H2 due to demand for scientific instruments and industrial applications, while Global Service anticipates higher demand owing to increased capacity utilization and upgrades of existing fabs.

Competitive Industry Position

VAT emphasized its strong competitive position in the semiconductor industry, which is on track toward a USD 1 trillion market by 2030. The company expects to outgrow the WFE market by up to 2x, which in turn is outgrowing GDP by a similar margin.

Advanced chip technologies for Artificial Intelligence continue to drive investment in both the logic and memory space, though NAND investments remain slow. The ongoing tariff discussions are considered financially non-material for VAT at this stage, and Chinese investments in chip manufacturing capacity remain at healthy levels.

Customer sentiment remains positive, with a more pronounced ramp generally expected, as evidenced by the demand for shorter lead times compared to previous years. VAT’s technology leadership and flexible operating model position it well to capitalize on these market trends and maintain its industry leadership.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.