Bank of America, Morgan Stanley, Nvidia and Dollar Tree rise premarket

Introduction & Market Context

Veracyte Inc (NASDAQ:VCYT) presented its third quarter 2024 business and financial results on November 6, 2024, showcasing exceptional performance with 29% year-over-year revenue growth. The cancer diagnostics company continues to strengthen its market position through expanding test volumes and improving profitability metrics, while simultaneously raising its full-year guidance for the third consecutive quarter.

The company’s stock has been trading between $19.73 and $47.32 over the past 52 weeks, reflecting investor confidence in Veracyte’s growth trajectory and market potential in the cancer diagnostics space.

Quarterly Performance Highlights

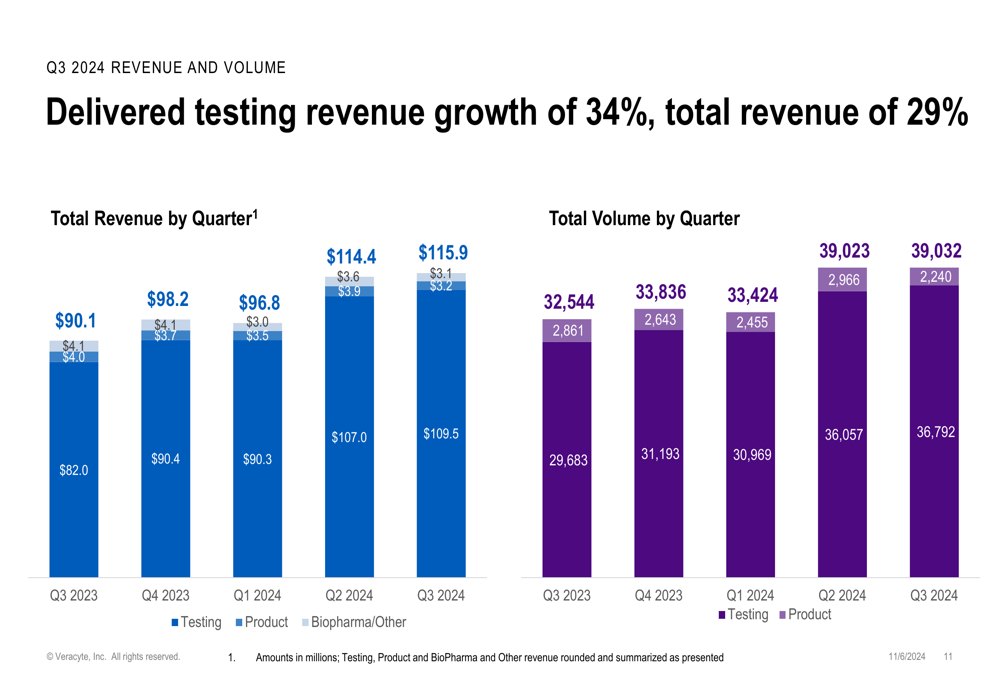

Veracyte reported total revenue of $115.9 million for Q3 2024, representing a 29% increase compared to the same period last year. This growth was primarily driven by the company’s testing segment, which generated $109.5 million in revenue, up 34% year-over-year.

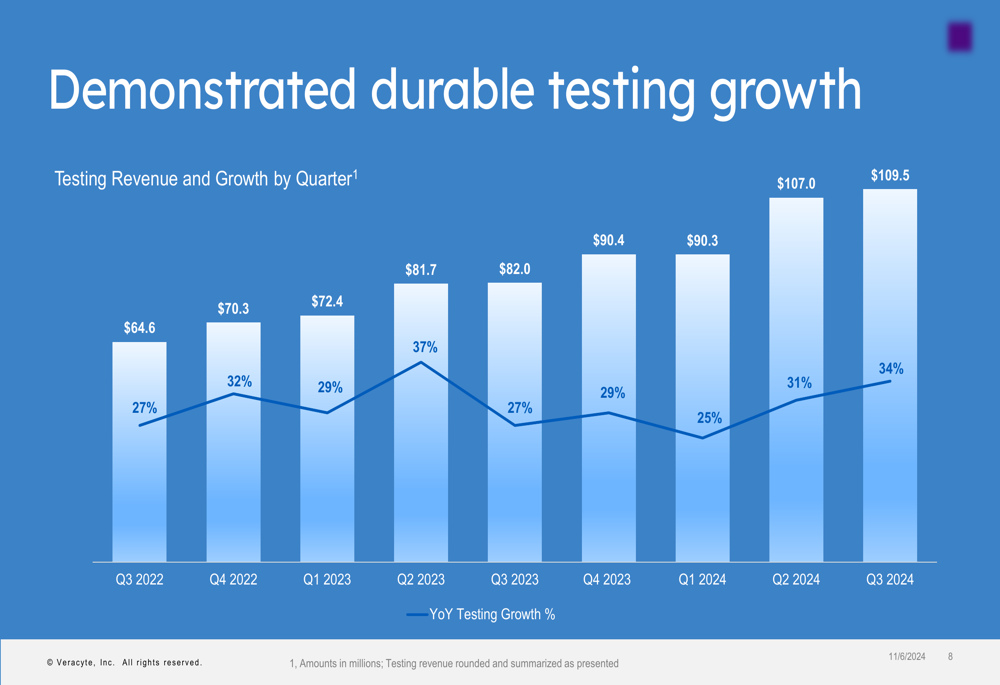

As shown in the following chart of quarterly testing revenue growth:

The company has maintained consistent year-over-year growth ranging from 25% to 37% over the past nine quarters, demonstrating the durability of its business model and strong market demand for its diagnostic tests.

Test volume also showed robust growth, with 36,792 tests performed in Q3 2024, representing a 24% increase year-over-year. Total (EPA:TTEF) volume, including product tests, grew 20% to 39,032 tests.

The breakdown of Veracyte’s revenue and volume by quarter illustrates the company’s consistent growth trajectory:

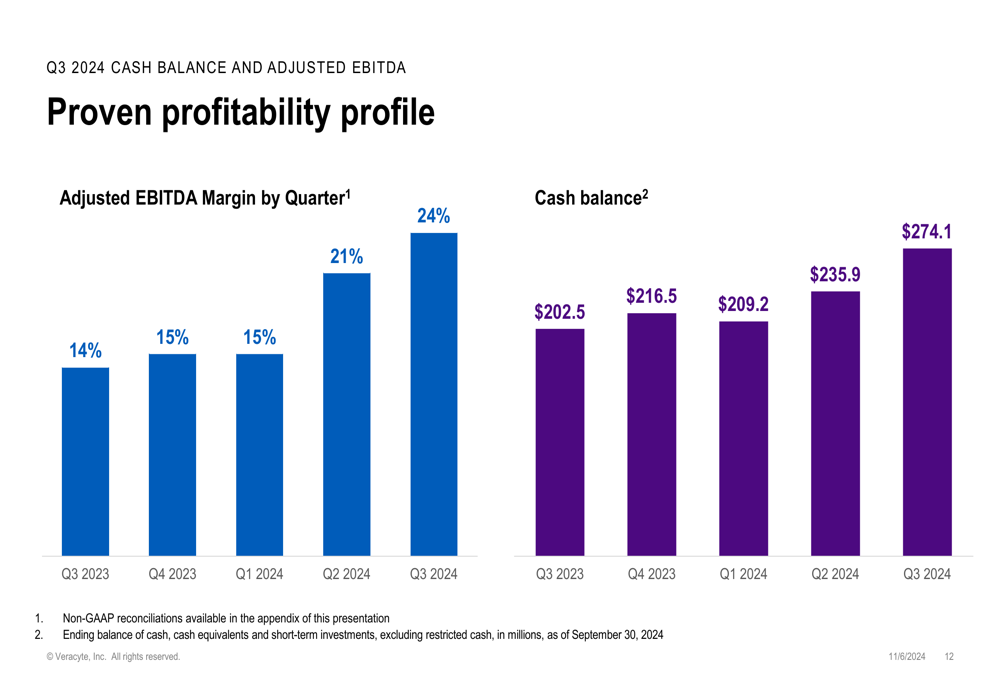

Profitability metrics showed significant improvement, with adjusted EBITDA margin reaching 24% in Q3 2024, up from 14% in Q3 2023. This progress brings the company closer to its 25% target margin. Additionally, Veracyte generated $38 million in cash during the quarter, with $30 million coming from operations, ending the period with a cash balance of $274.1 million.

The following chart illustrates Veracyte’s improving profitability and growing cash position:

Strategic Initiatives

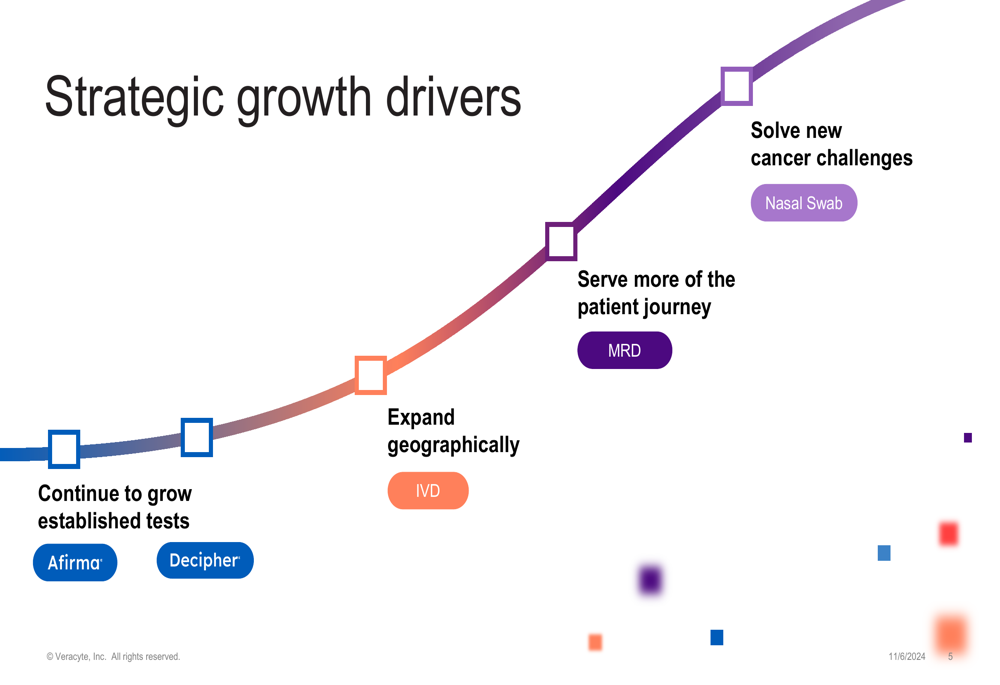

Veracyte’s growth strategy is built around four key drivers: growing established tests, expanding geographically, serving more of the patient journey, and solving new cancer challenges.

The company’s strategic roadmap is illustrated in this timeline:

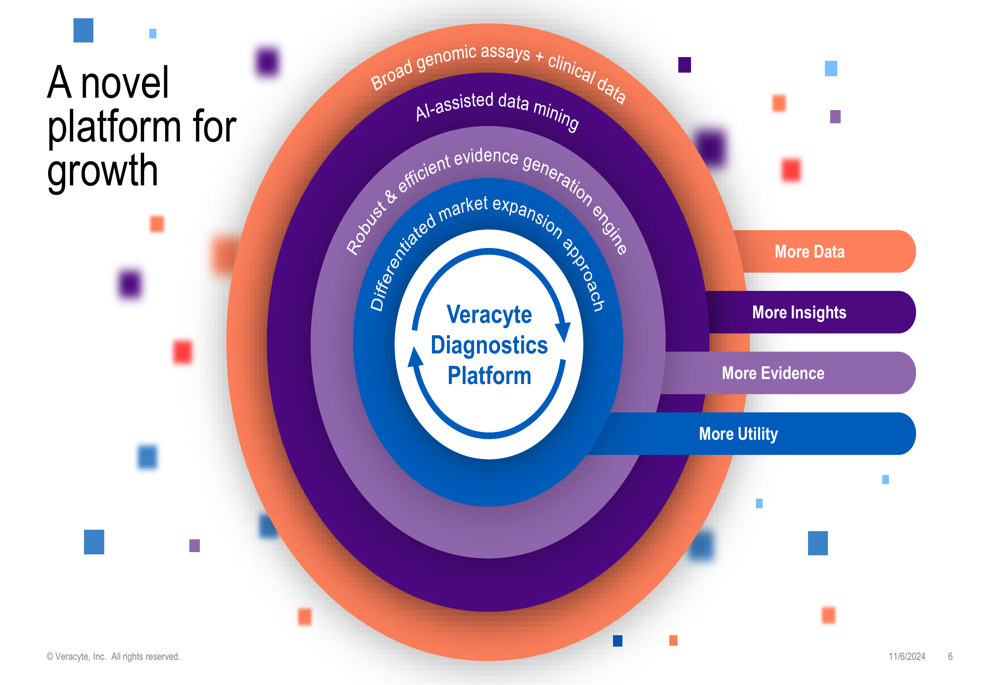

At the core of Veracyte’s competitive advantage is its proprietary diagnostics platform, which combines broad genomic assays with clinical data, AI-assisted data mining, and an evidence generation engine to deliver differentiated market expansion.

The company’s diagnostic platform architecture is visualized here:

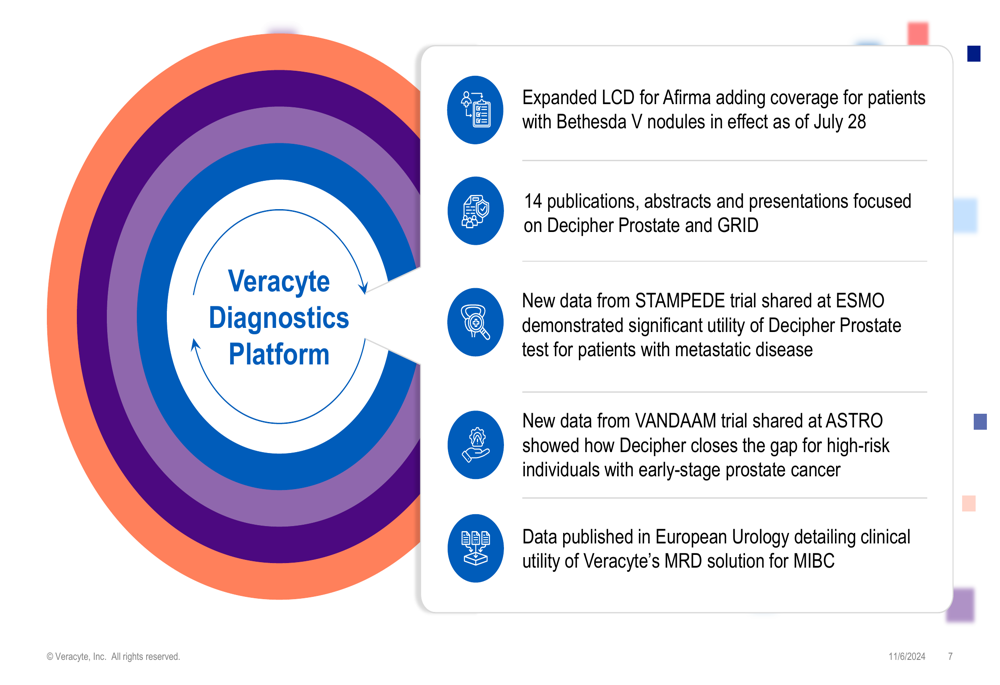

This platform has enabled several key developments during the quarter, including an expanded Local Coverage Determination (LCD) for Afirma, adding coverage for patients with Bethesda V nodules, effective July 28. The company also highlighted 14 publications, abstracts, and presentations focused on Decipher Prostate and GRID, reinforcing the clinical utility of its tests.

New data from the STAMPEDE trial presented at ESMO demonstrated significant utility of the Decipher Prostate test for patients with metastatic disease, while data from the VANDAAM trial showed how Decipher closes the gap for high-risk individuals with early-stage prostate cancer.

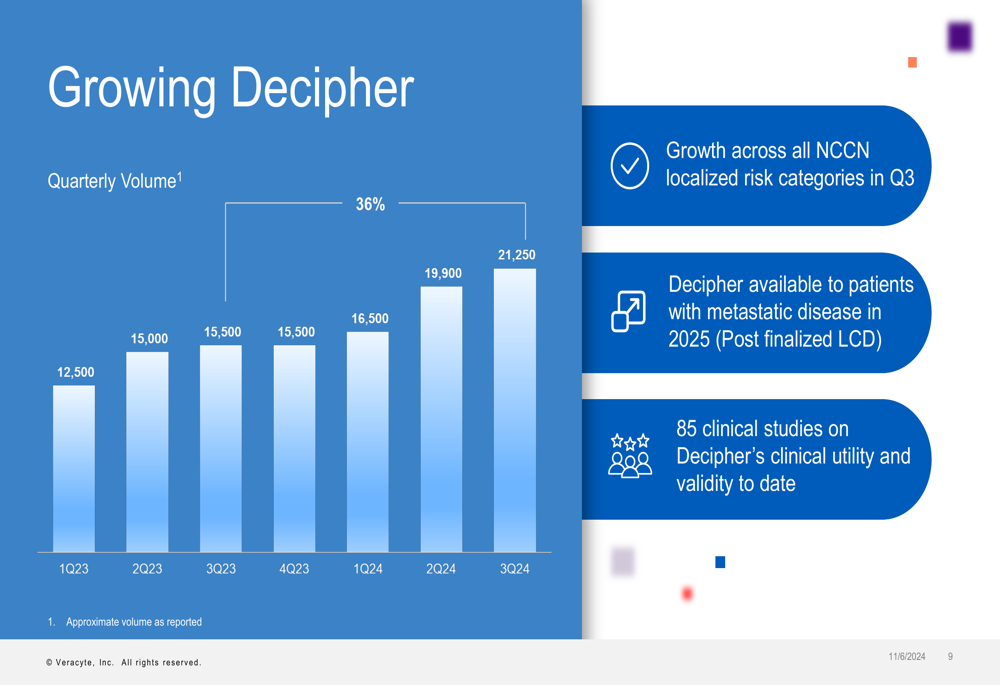

The growth in Decipher testing volume has been particularly strong, reaching 21,250 tests in Q3 2024, with growth across all NCCN localized risk categories:

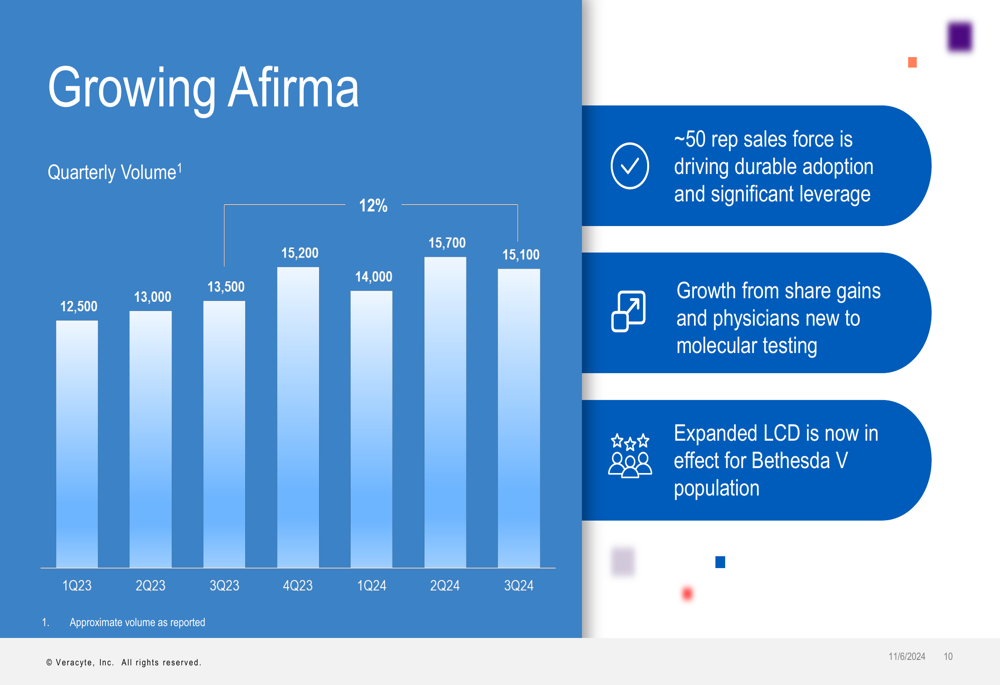

Similarly, Afirma testing volume has shown steady growth, reaching 15,100 tests in Q3 2024, driven by share gains and physicians new to molecular testing:

Forward-Looking Statements

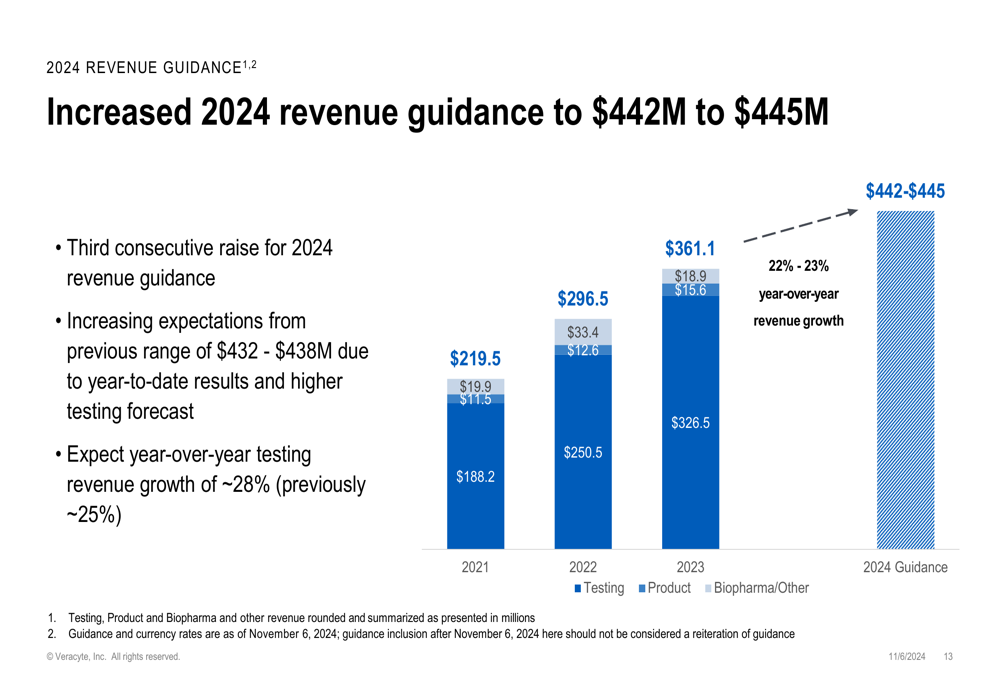

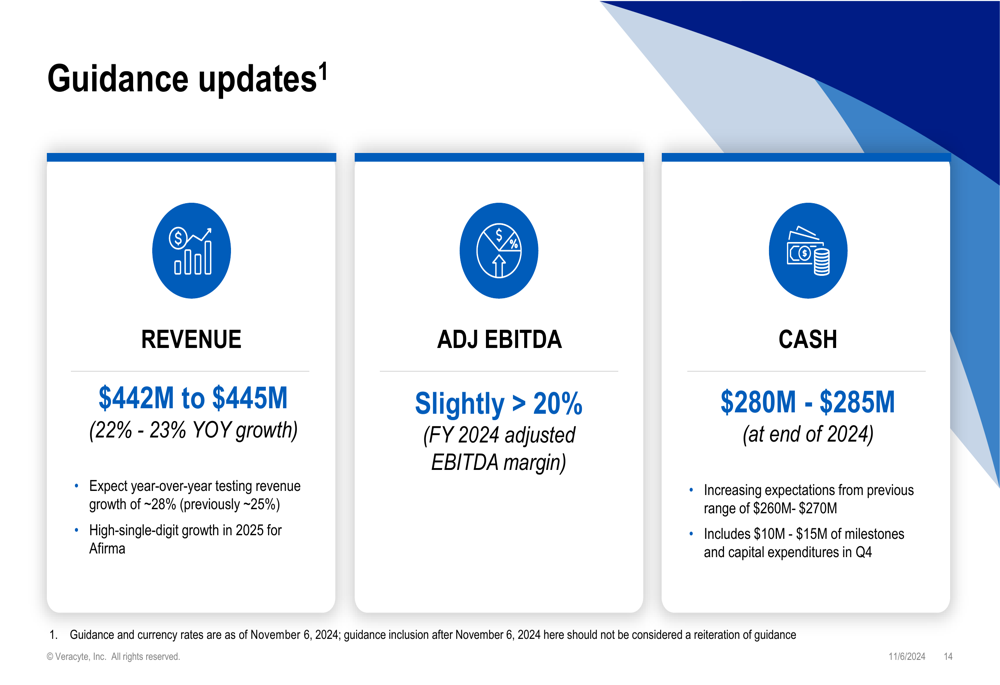

Based on its strong performance, Veracyte raised its 2024 revenue guidance for the third consecutive quarter to $442-445 million, representing 22-23% year-over-year growth. The company now expects year-over-year testing revenue growth of approximately 28%, up from the previous guidance of 25%.

The updated revenue guidance and historical performance are illustrated in this chart:

Veracyte also raised its 2024 year-end cash guidance to $280-285 million, up from the previous range of $260-270 million. The company expects its adjusted EBITDA margin for the full year 2024 to be slightly above 20%.

Looking ahead to 2025, Veracyte anticipates high-single-digit growth for Afirma and plans to make Decipher available to patients with metastatic disease following the finalization of the LCD.

Conclusion

Veracyte’s Q3 2024 presentation demonstrates the company’s strong execution across its business segments, with exceptional revenue growth, expanding test volumes, and improving profitability. The consistent performance has enabled the company to raise its full-year guidance for the third consecutive quarter, reflecting confidence in its strategic direction and market opportunity.

With a robust cash position of $274.1 million and continued investment in its diagnostic platform, Veracyte is well-positioned to pursue its vision of transforming cancer care for patients worldwide. The company’s focus on expanding its test menu, geographic reach, and clinical evidence base provides multiple avenues for sustained growth in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.