Microsoft’s data-center shortages to persist longer than expected - Bloomberg

Introduction & Market Context

Vericel Corporation (NASDAQ:VCEL) presented its first quarter 2025 financial results on May 8, 2025, reporting record revenue but facing profitability challenges. The cell therapy company’s stock dropped 6.1% in premarket trading to $38.00, reflecting investor concerns despite management’s optimistic outlook.

The company, which specializes in advanced cell therapies for sports medicine and severe burn care, continues to see strong adoption of its flagship MACI (matrix-induced autologous chondrocyte implantation) product, particularly following the recent launch of MACI Arthro. However, increased operating expenses have pressured bottom-line results.

Quarterly Performance Highlights

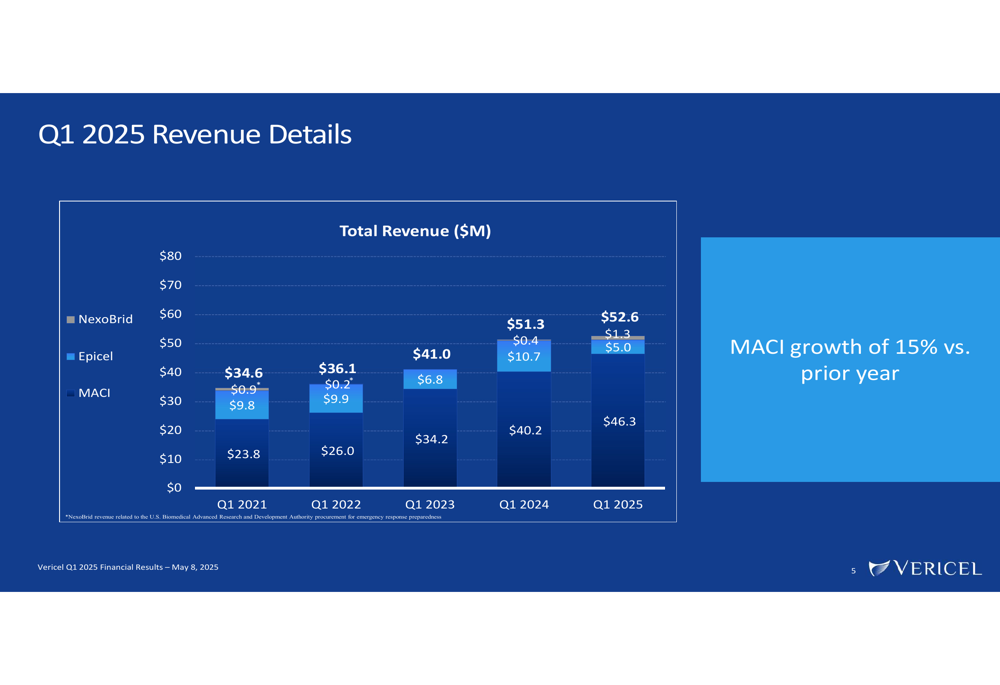

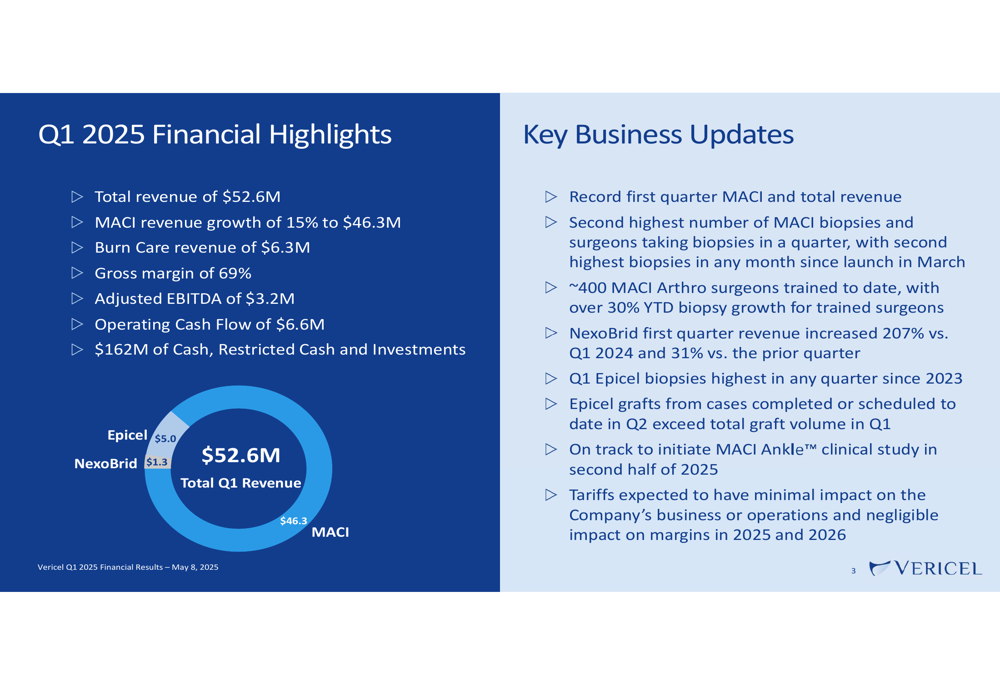

Vericel reported total revenue of $52.6 million for Q1 2025, a modest increase from $51.3 million in the same period last year. MACI remained the primary revenue driver, growing 15% year-over-year to $46.3 million and accounting for approximately 88% of total revenue.

As shown in the following revenue breakdown:

Burn care revenue, comprising Epicel and NexoBrid products, totaled $6.3 million. While NexoBrid showed impressive growth of 207% compared to Q1 2024, reaching $1.3 million, Epicel revenue decreased to $5.0 million from $10.7 million in the prior year period.

The company highlighted several operational achievements in its presentation:

MACI Arthro Launch Progress

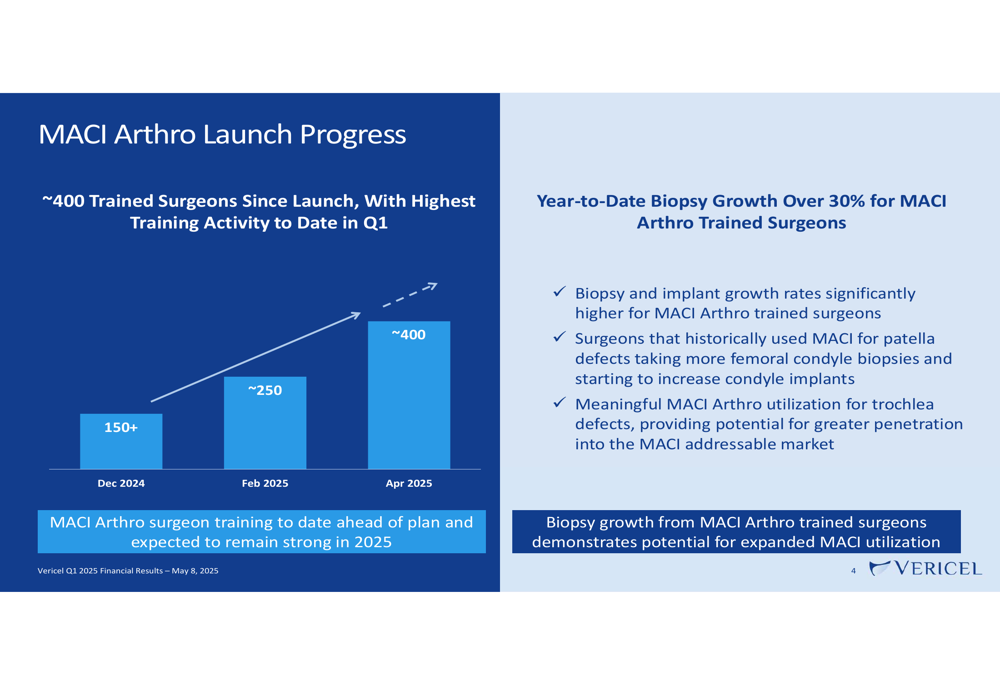

A significant focus of the presentation was the successful launch of MACI Arthro, with approximately 400 surgeons trained to date. The first quarter saw the highest training activity since launch, with surgeon adoption accelerating.

The company reported that surgeons trained on MACI Arthro are showing biopsy growth rates over 30% year-to-date, significantly outpacing untrained surgeons. Management noted that physicians previously using MACI primarily for patella defects are now taking more femoral condyle biopsies and beginning to increase condyle implants.

The following chart illustrates the rapid growth in trained surgeons:

Detailed Financial Analysis

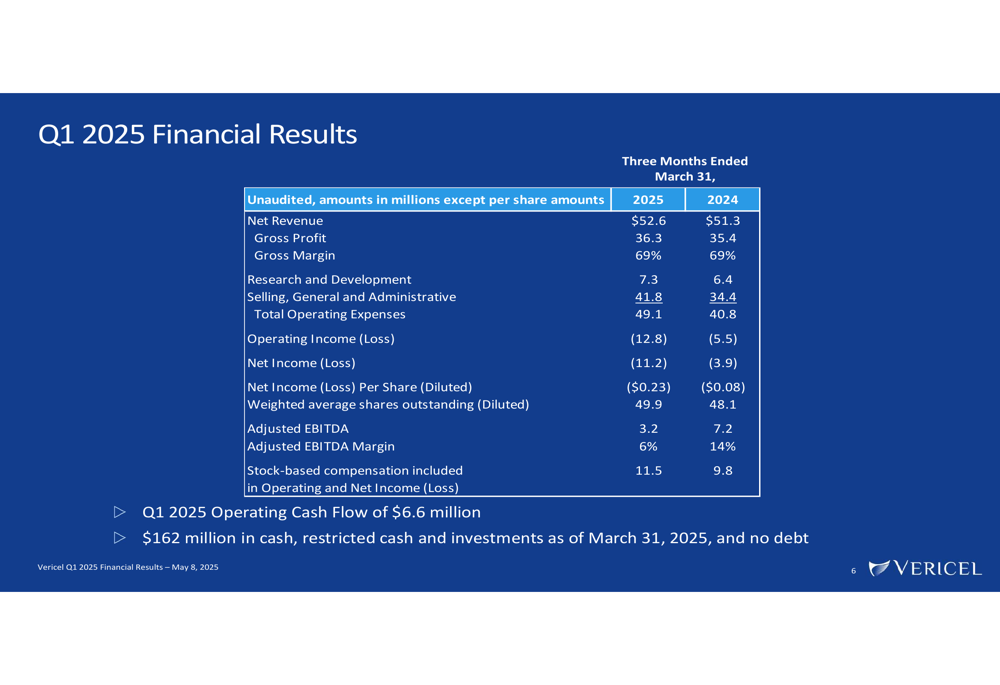

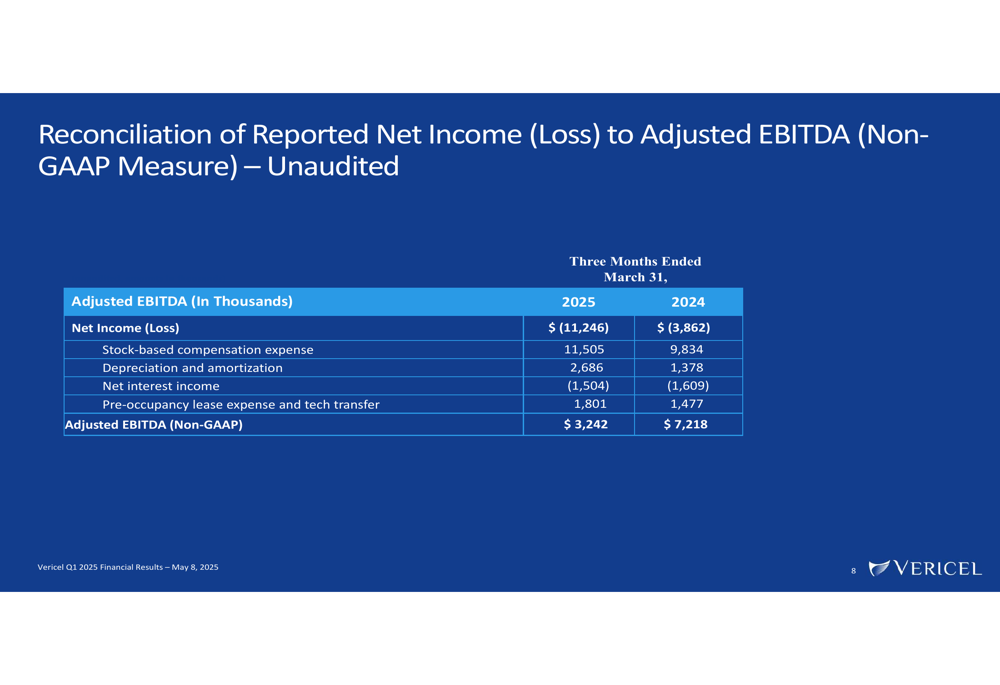

Despite the record revenue, Vericel’s financial results revealed profitability challenges. The company reported a net loss of $11.2 million for Q1 2025, compared to a net loss of $3.9 million in Q1 2024. This widening loss came primarily from increased operating expenses, which rose to $49.1 million from $40.8 million in the prior year period.

The comprehensive financial comparison shows:

Gross margin remained stable at 69%, while adjusted EBITDA declined to $3.2 million from $7.2 million in Q1 2024, representing a margin of 6% compared to 14% in the prior year period. The reconciliation of net loss to adjusted EBITDA reveals significant increases in stock-based compensation and depreciation expenses:

On a positive note, operating cash flow was strong at $6.6 million, and the company maintained a solid balance sheet with $162 million in cash, restricted cash, and investments as of March 31, 2025, with no debt.

Forward-Looking Statements & Guidance

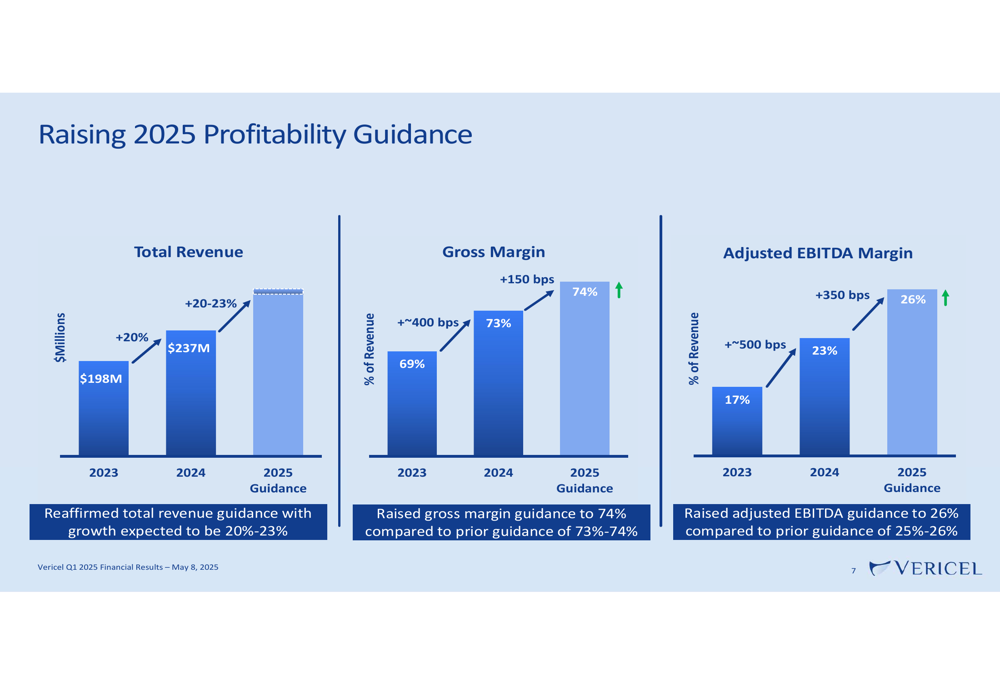

Despite the Q1 profitability challenges, Vericel raised its 2025 profitability guidance. The company reaffirmed its total revenue growth projection of 20-23% for the full year while increasing its gross margin guidance to 74% (from a previous range of 73-74%) and adjusted EBITDA margin to 26% (from a previous range of 25-26%).

The following chart illustrates the company’s projected financial trajectory:

Management expressed confidence in the company’s growth trajectory, citing several positive indicators:

- Record MACI biopsies and strong surgeon engagement

- Epicel biopsies reaching their highest level in any quarter since 2023

- Epicel grafts from cases completed or scheduled for Q2 already exceeding total graft volume in Q1

- Plans to initiate the MACI Ankle clinical study in the second half of 2025

This optimistic outlook aligns with the company’s Q4 2024 performance, when it reported a 20% year-over-year revenue increase to $237.2 million and achieved a record gross margin of 78% for that quarter. However, the widening Q1 2025 loss and increased operating expenses suggest the company is investing heavily in growth initiatives that have yet to translate to improved profitability.

As Vericel continues its expansion efforts, investors will be watching closely to see if the company can deliver on its raised profitability guidance while managing the increased operating expenses that impacted Q1 results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.