Nvidia AI chips targeted in China customs crackdown- FT

Introduction & Market Context

Verra Mobility Corporation (NASDAQ:VRRM) released its second quarter 2025 earnings presentation on August 6, 2025, reporting solid financial performance with total revenue of $236 million, representing a 6% year-over-year increase. The mobility technology company’s stock closed at $24.96, down 0.72% for the day.

The company, which provides road safety, toll management and parking solutions, continues to show resilience despite noting potential risks to its guidance due to uncertain travel demand outlook. Verra Mobility’s performance builds on its Q1 momentum, where it reported $223 million in revenue and $0.30 in adjusted earnings per share.

Quarterly Performance Highlights

Verra Mobility delivered strong financial results across key metrics in Q2 2025, with service revenue growth driving overall performance.

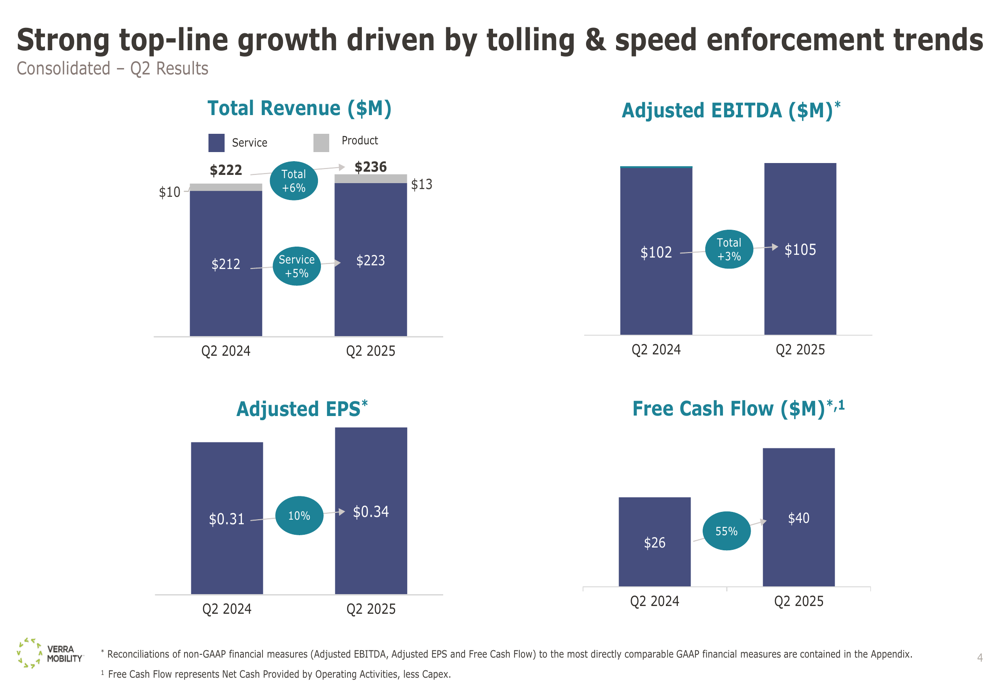

As shown in the following chart of quarterly financial performance:

Total (EPA:TTEF) revenue reached $236 million, up 6% from $222 million in Q2 2024, with service revenue growing 5% to $223 million. The company’s adjusted EBITDA increased 3% to $105 million, while adjusted EPS grew 10% to $0.34. Most notably, free cash flow surged 55% to $40 million compared to $26 million in the prior year period.

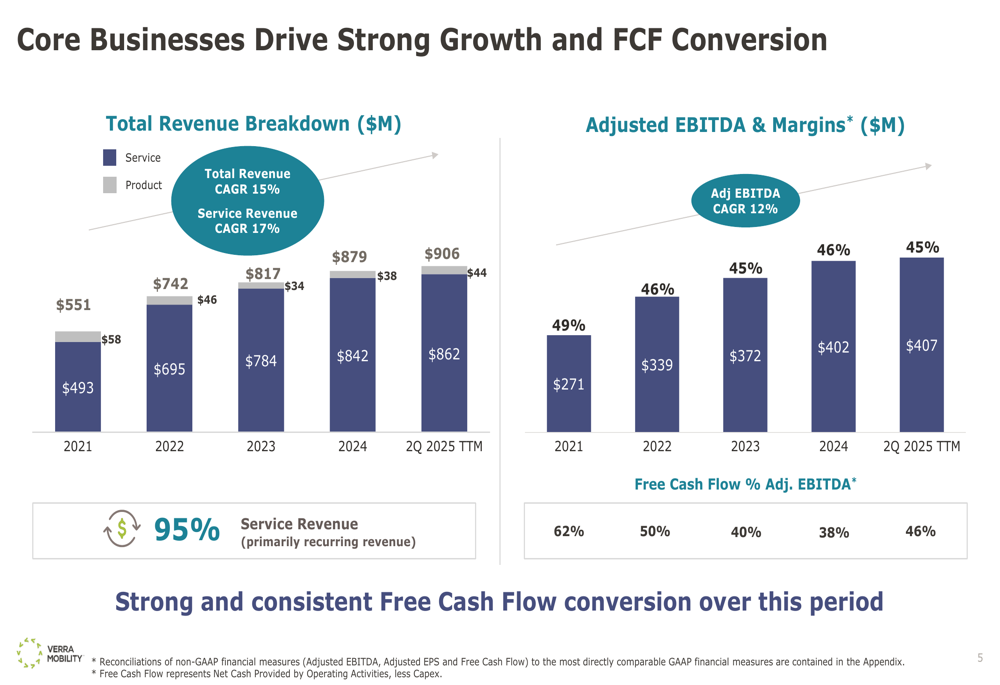

The company’s long-term growth trajectory remains impressive, with a 15% total revenue CAGR since 2021 and service revenue (primarily recurring) now accounting for 95% of total revenue.

The following chart illustrates this consistent growth pattern:

Segment Performance

Performance varied across Verra Mobility’s three business segments:

Commercial Services, which provides toll management solutions primarily to rental car companies, posted a 5% revenue increase to $109 million, with segment profit growing 4% to $72 million. Growth was driven by increased product adoption and tolling activity in rental car operations and European markets, partially offset by a decline in fleet management revenue.

Government Solutions, which provides traffic safety systems to municipalities, delivered the strongest growth with a 10% revenue increase to $107 million. Service revenue in this segment grew 7%, driven by 11% growth outside of New York City from new awards and expansion of existing programs. Segment profit remained flat at $30 million due to product mix and implementation costs.

The Parking Solutions segment (T2 Systems) was the only underperformer, with revenue declining 4% to $20 million. While recurring SaaS revenue showed low single-digit growth year-to-date, this was offset by an 18% decline in product sales and lower installation and professional services revenue.

Strategic Initiatives

Verra Mobility highlighted several strategic developments that position the company for future growth:

Colorado and Nevada signed School Bus Stop Arm Enforcement into law, opening a combined $40 million of incremental total addressable market for the company’s safety solutions.

Government Solutions bookings were strong in Q2, with potential for up to $21 million of incremental full run-rate annual recurring revenue, bringing the trailing twelve months total to approximately $60 million.

The Board of Directors authorized a new $100 million stock repurchase program available through November 2026, demonstrating confidence in the company’s financial position and commitment to returning value to shareholders.

Financial Position

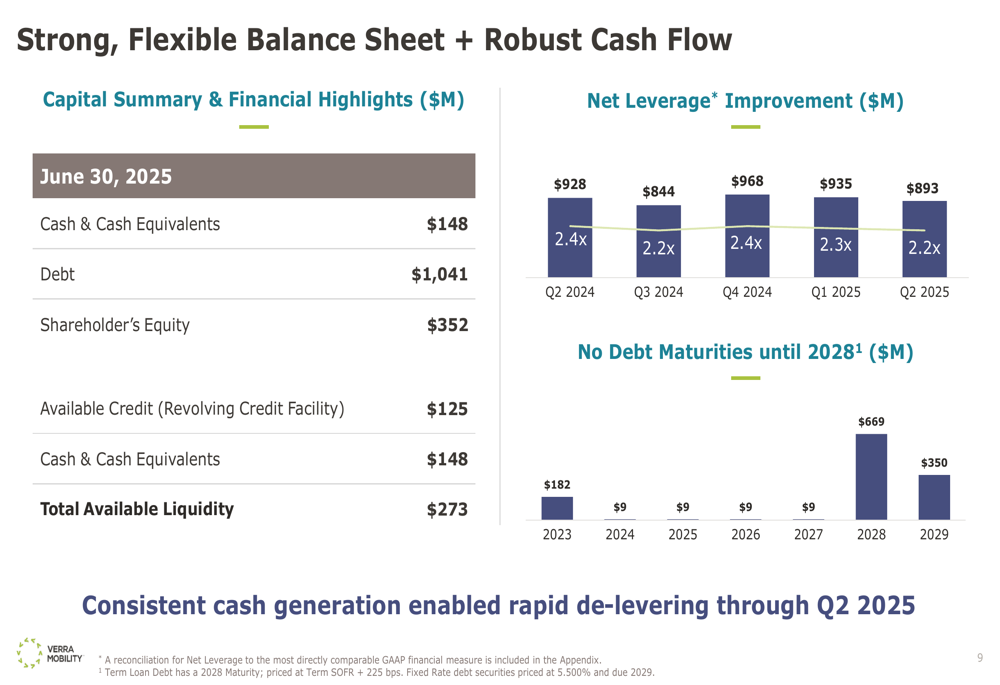

Verra Mobility continues to maintain a strong balance sheet with significant financial flexibility, as illustrated in the following chart:

As of June 30, 2025, the company reported $148 million in cash and cash equivalents, with total debt of $1,041 million. Net leverage improved to 2.2x from 2.4x in Q2 2024, reflecting the company’s strong cash generation and deleveraging efforts.

The company has no debt maturities until 2028, providing substantial financial flexibility. Available liquidity totaled $273 million, including $125 million from its revolving credit facility.

Forward-Looking Statements

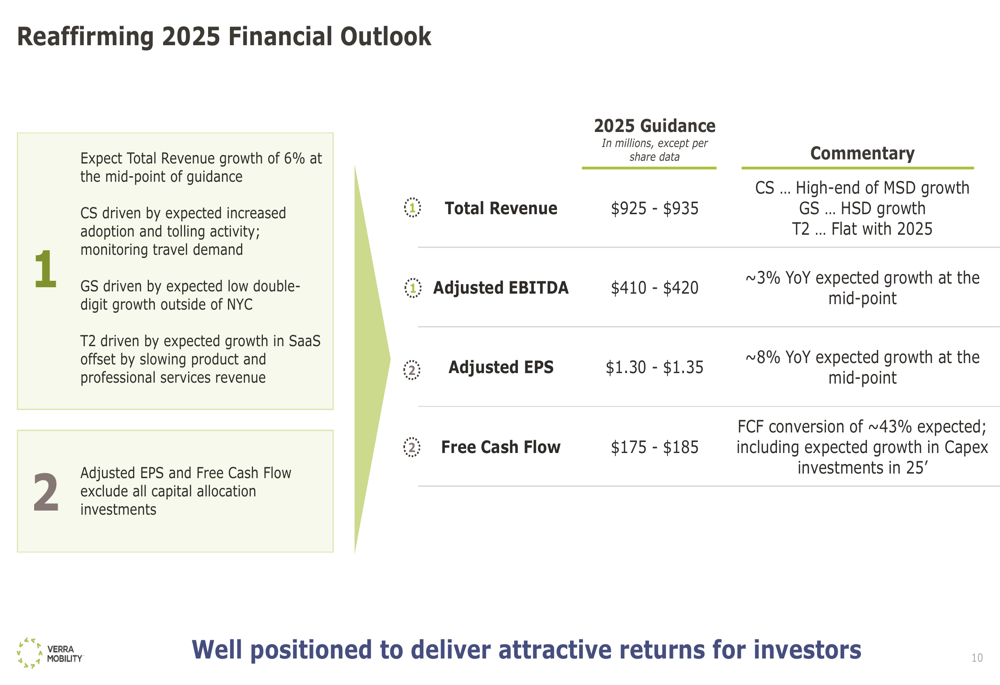

Despite noting risks related to travel demand, Verra Mobility reaffirmed its full-year 2025 guidance:

The company expects:

- Total revenue of $925-935 million

- Adjusted EBITDA of $410-420 million (approximately 3% year-over-year growth at the midpoint)

- Adjusted EPS of $1.30-1.35 (approximately 8% year-over-year growth at the midpoint)

- Free cash flow of $175-185 million (FCF conversion of approximately 43%)

Management noted potential risk to the lower end of guidance ranges due to uncertain outlook for travel demand, consistent with the cautious tone expressed in the Q1 earnings call.

Additional guidance assumptions include a fully diluted share count of approximately 163 million shares, an effective tax rate of 28.5-29.5%, and capital expenditures of approximately $110 million, which includes incremental investments for revenue-generating cameras in Government Solutions and ERP implementation.

Conclusion

Verra Mobility’s Q2 2025 results demonstrate the company’s ability to deliver solid growth despite challenging market conditions. The 6% revenue growth and impressive 55% increase in free cash flow highlight the company’s operational efficiency and strong recurring revenue model.

While maintaining a cautious outlook regarding travel demand, the company’s strategic initiatives, improved financial position, and new stock repurchase program position it well for continued growth. Investors will be watching closely to see if Verra Mobility can maintain this momentum through the second half of 2025, particularly given the uncertain travel environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.