Oklo stock tumbles as Financial Times scrutinizes valuation

Introduction & Market Context

Vertiv Holdings Co (NYSE:VRT) released its third-quarter 2025 results on October 22, showcasing exceptional performance driven by continued strong demand in the data center infrastructure market. The company’s shares rose 4.27% in pre-market trading following the announcement, reflecting positive investor sentiment about the results.

The critical digital infrastructure provider continues to benefit from the accelerating AI adoption trend, which is driving significant data center expansion globally. Vertiv’s strategic positioning in power, cooling, and services for high-density computing environments has allowed it to capitalize on this market momentum.

Quarterly Performance Highlights

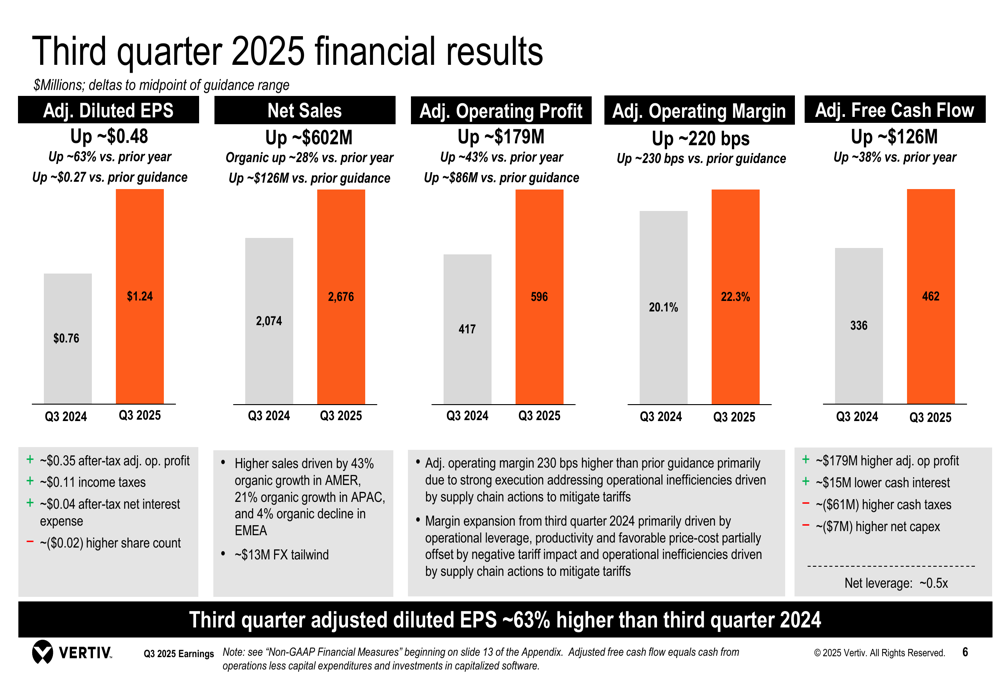

Vertiv reported impressive financial results for Q3 2025, significantly exceeding both guidance and prior year performance. Adjusted diluted earnings per share reached $1.24, up approximately 63% from Q3 2024, primarily driven by higher adjusted operating profit from the 28% organic net sales increase.

The company’s book-to-bill ratio stood at approximately 1.4x for the third quarter, with trailing twelve-month organic orders growth of about 21%. Third-quarter organic orders increased approximately 60% from the same period in 2024 and grew approximately 20% sequentially from the second quarter of 2025.

As shown in the following comprehensive financial results chart, Vertiv’s performance exceeded expectations across multiple metrics:

The adjusted operating margin reached 22.3% in Q3 2025, exceeding both guidance and prior year figures. This strong margin performance, combined with higher organic net sales, contributed to an adjusted operating profit of $596 million, up 43% from the prior year quarter. Adjusted free cash flow reached $462 million, up 38% from the prior year third quarter, driven by higher adjusted operating profit and working capital efficiency.

Regional Performance Analysis

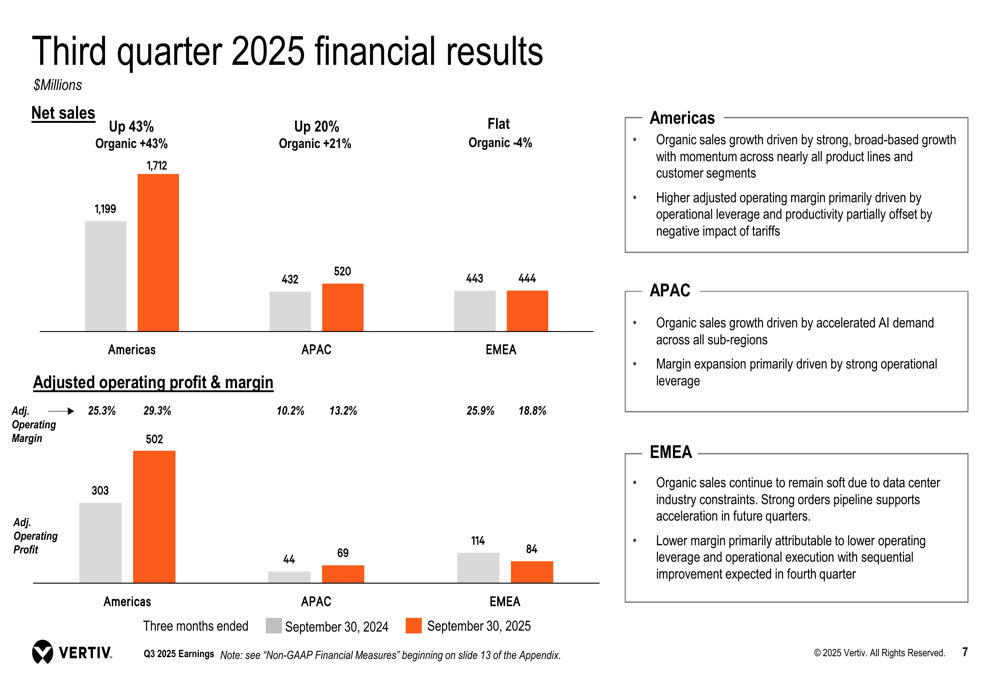

Vertiv’s performance varied significantly across regions, with the Americas and Asia Pacific showing robust growth while Europe, Middle East, and Africa (EMEA) experienced a slight decline. The following regional breakdown illustrates these differences:

The Americas region led growth with a 43% organic sales increase, driven by strong, broad-based momentum across nearly all product lines and customer segments. Adjusted operating profit in the Americas surged to $502 million, with margins expanding to 29.3% from 25.3% in the prior year period.

Asia Pacific delivered 21% organic sales growth, fueled by accelerated AI demand across all sub-regions. The region’s adjusted operating profit reached $69 million, with margins improving to 13.2% from 10.2% in the prior year quarter.

In contrast, EMEA experienced a 4% organic sales decline, with adjusted operating profit falling to $84 million and margins contracting to 18.8% from 25.9% in the prior year period. Vertiv noted that data center industry constraints continue to affect the region, though a strong orders pipeline supports expectations for acceleration in future quarters.

Strategic Initiatives and Future Outlook

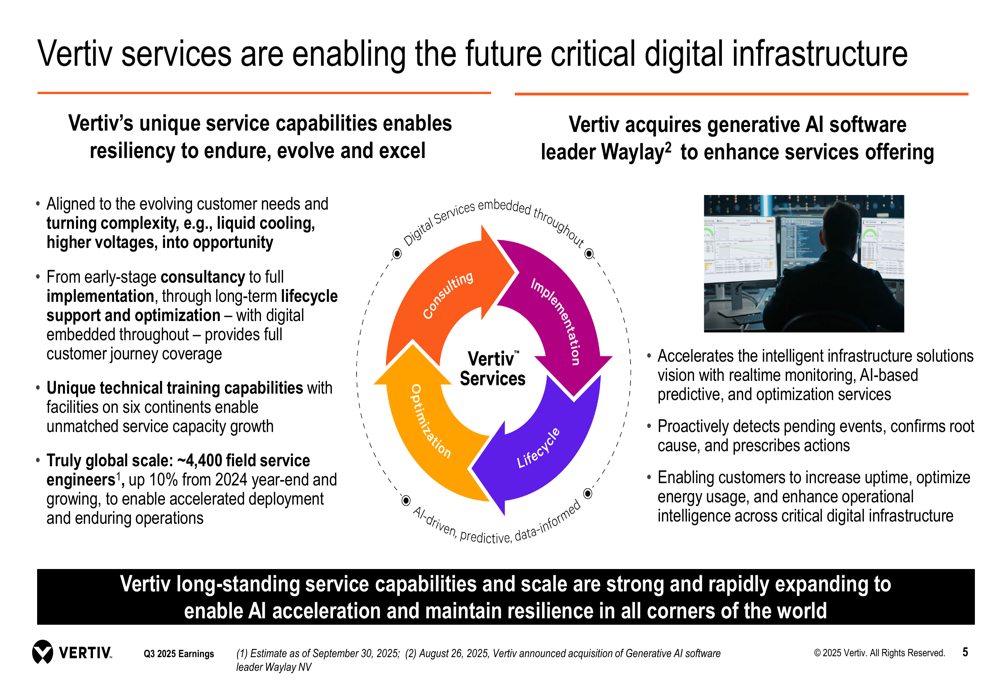

Vertiv is actively expanding its service capabilities to address evolving customer needs, particularly in complex areas like liquid cooling and higher voltage systems. The company’s global service network includes approximately 4,400 field service engineers, up 10% from 2024 year-end.

As illustrated in the following slide on Vertiv’s service strategy:

The company recently acquired Waylay, a generative AI software leader, to enhance its services offering. This acquisition accelerates Vertiv’s intelligent infrastructure solutions vision with real-time monitoring, AI-based predictive capabilities, and optimization services.

Vertiv also announced a collaboration with NVIDIA to advance 800 VDC platform designs for powering and cooling gigawatt-scale AI factories. This collaboration supports the ’unit of compute’ strategy to address the unprecedented power demands of AI workloads on NVIDIA Vera Rubin Ultra Kyber platforms, with the 800 VDC portfolio planned for release in the second half of 2026.

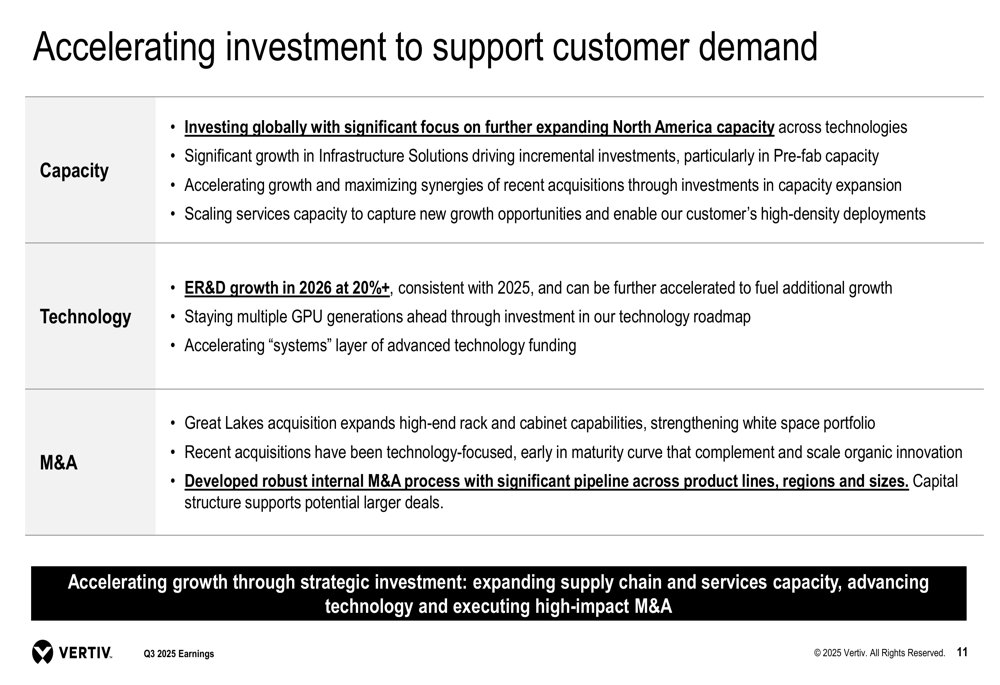

The company is accelerating investments to support customer demand, as outlined in this strategic overview:

Looking ahead to 2026, Vertiv expects AI-driven data center demand to remain strong. The company anticipates continued significant organic sales growth, supported by accelerated investments in supply chain and services capacity, including meaningful growth in capital expenditures.

Financial Guidance and Forward-Looking Statements

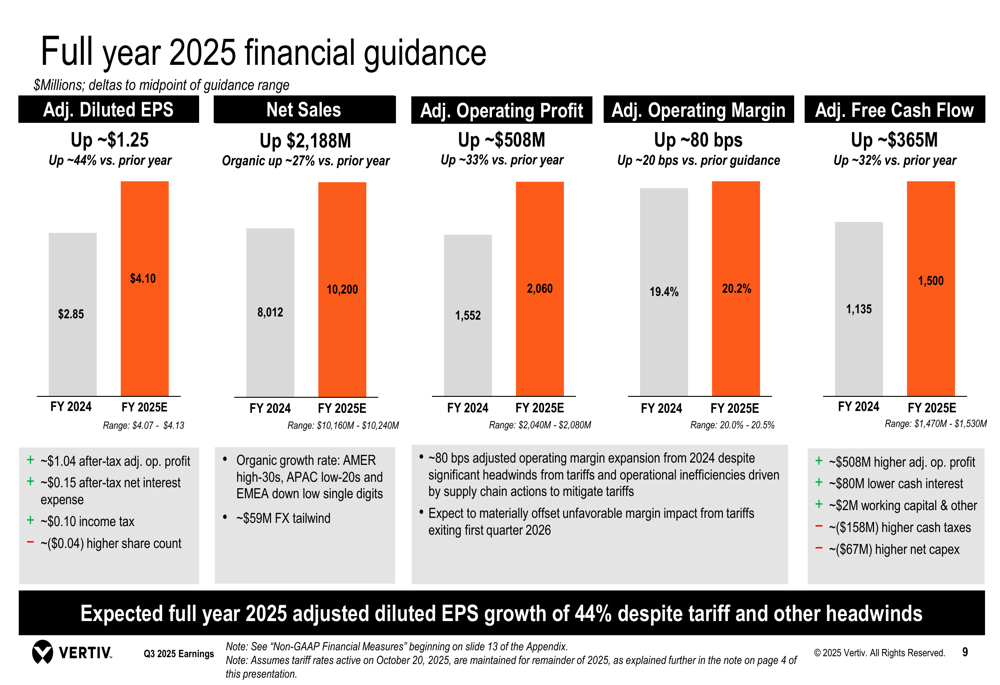

Based on strong Q3 results and continued robust demand, Vertiv has raised its full-year 2025 guidance across all key metrics:

For the full year 2025, Vertiv now expects adjusted diluted EPS of $4.10, up 44% from 2024, and adjusted operating profit of $2,060 million, up 33% from 2024. Net sales are projected to reach $10,160 million to $10,240 million, representing 27% organic growth from 2024. The company also raised its adjusted free cash flow guidance to $1,500 million.

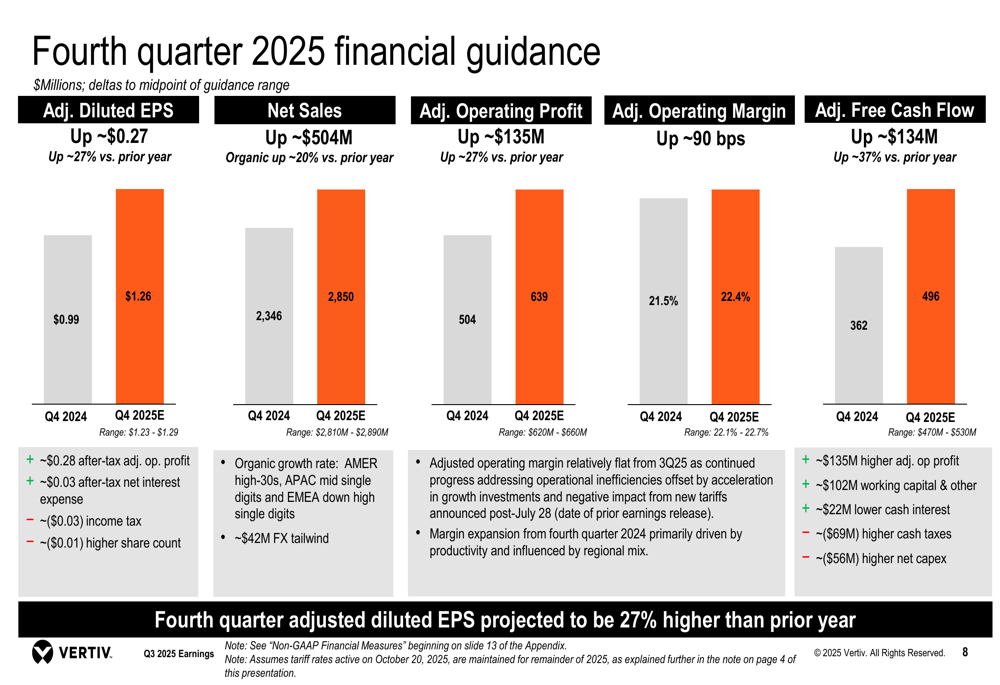

For the fourth quarter of 2025, Vertiv provided the following guidance:

Fourth-quarter adjusted diluted EPS is expected to be between $1.23 and $1.29, up approximately 27% from the prior year. Net sales are projected to be between $2,810 million and $2,890 million, representing approximately 20% organic growth from the fourth quarter of 2024.

While the tariff situation remains fluid and uncertain, Vertiv is executing countermeasures and expects to materially offset the impact by the end of the first quarter of 2026. The company anticipates that operating leverage will remain a key driver of operating margin expansion, further supported by continued gains in productivity and price-cost management.

Vertiv’s strong performance and raised guidance reflect the company’s effective execution in a high-demand market environment, positioning it well for continued growth in the expanding AI infrastructure space.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.