BETA Technologies launches IPO of 25 million shares priced $27-$33

Introduction & Market Context

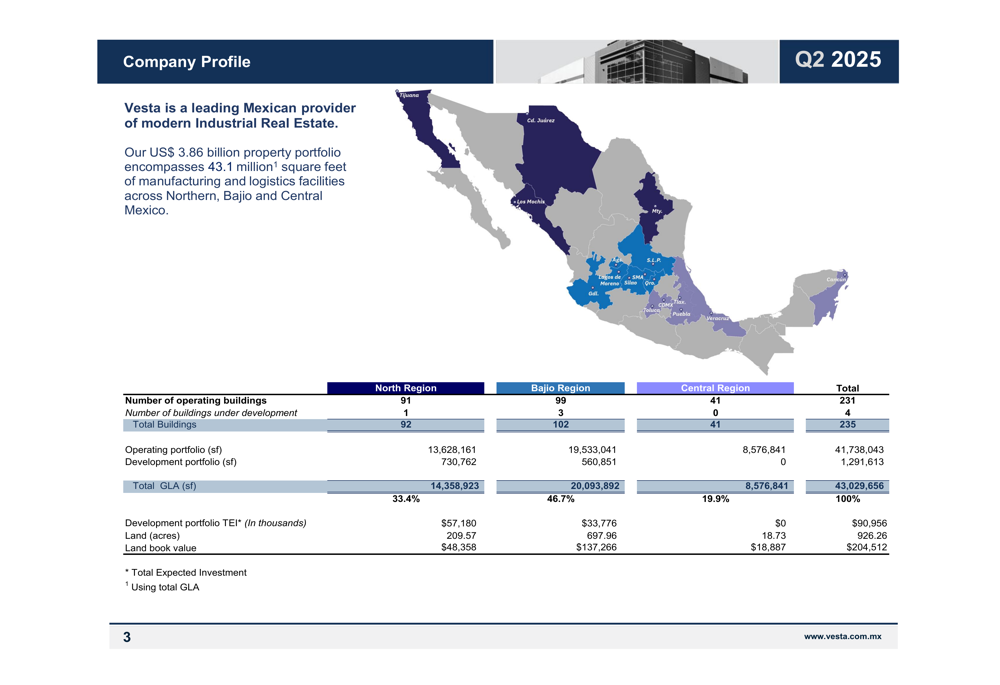

Corporacion Inmobiliaria Vesta (VESTA), a leading Mexican provider of industrial real estate, released its Q2 2025 supplementary presentation on July 25, showcasing a portfolio valued at US$3.86 billion. The company maintains a strategic presence across Northern, Bajio, and Central Mexico with 43.1 million square feet of manufacturing and logistics facilities, positioning itself to capitalize on nearshoring trends despite current market caution.

The company’s geographic distribution is clearly illustrated in its corporate presentation:

Quarterly Performance Highlights

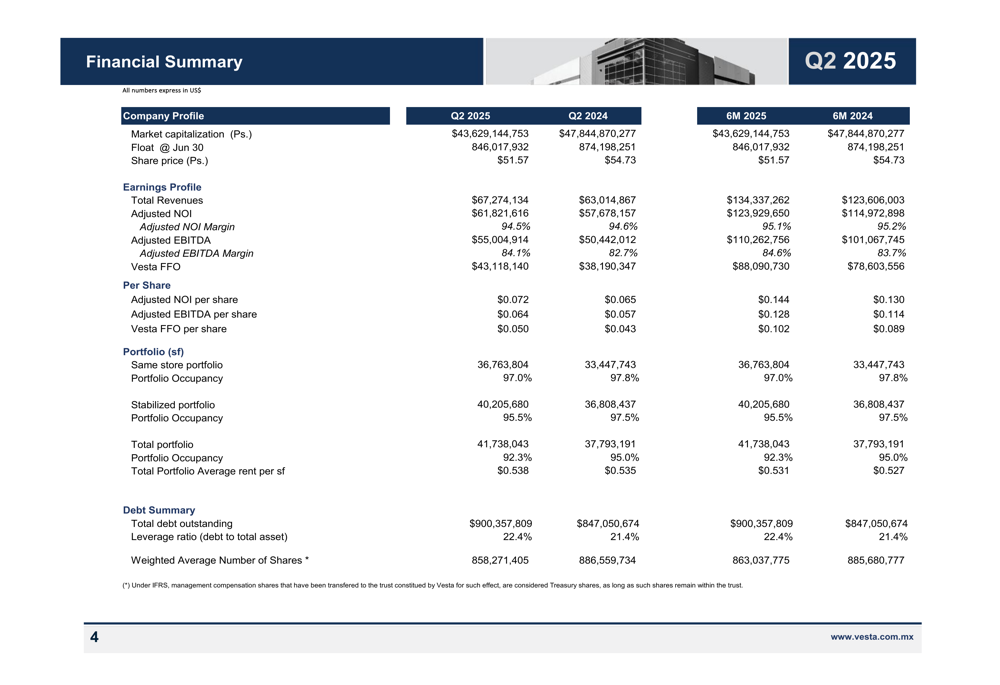

Vesta reported a 6.8% year-over-year increase in total revenues to $67.27 million in Q2 2025, up from $63.01 million in Q2 2024. Adjusted NOI grew 7.2% to $61.82 million, while Adjusted EBITDA rose 9.0% to $55.00 million. Despite these positive operational metrics, profit for the period decreased significantly by 74.6% to $27.72 million, compared to $109.30 million in the same period last year.

The financial summary below highlights the company’s key performance indicators:

This mixed financial performance aligns with CEO Lorenzo Berho’s characterization of 2025 as "a transitional year for the sector marked by caution and extended decision cycles," as noted in the company’s earnings call. The substantial drop in profit despite revenue growth suggests challenges in maintaining bottom-line performance amid changing market conditions.

Portfolio and Occupancy Analysis

Vesta’s occupancy metrics show a concerning trend across its portfolio categories. Total portfolio occupancy decreased to 92.3% in Q2 2025 from 95.0% in Q2 2024, while stabilized portfolio occupancy declined to 95.5% from 97.5%. Same store portfolio occupancy also experienced a slight decrease to 97.0% from 97.8%.

The following chart illustrates these occupancy trends over recent quarters:

Regional performance varied significantly, with the North region experiencing the steepest occupancy decline from 99.4% to 91.8%, while Bajio remained stable at 95.8%, and Central region decreased from 100.0% to 96.5%. Despite these occupancy challenges, rental revenues increased across all regions, with the North showing the most substantial growth of 40.4% year-over-year.

The regional performance breakdown provides additional context:

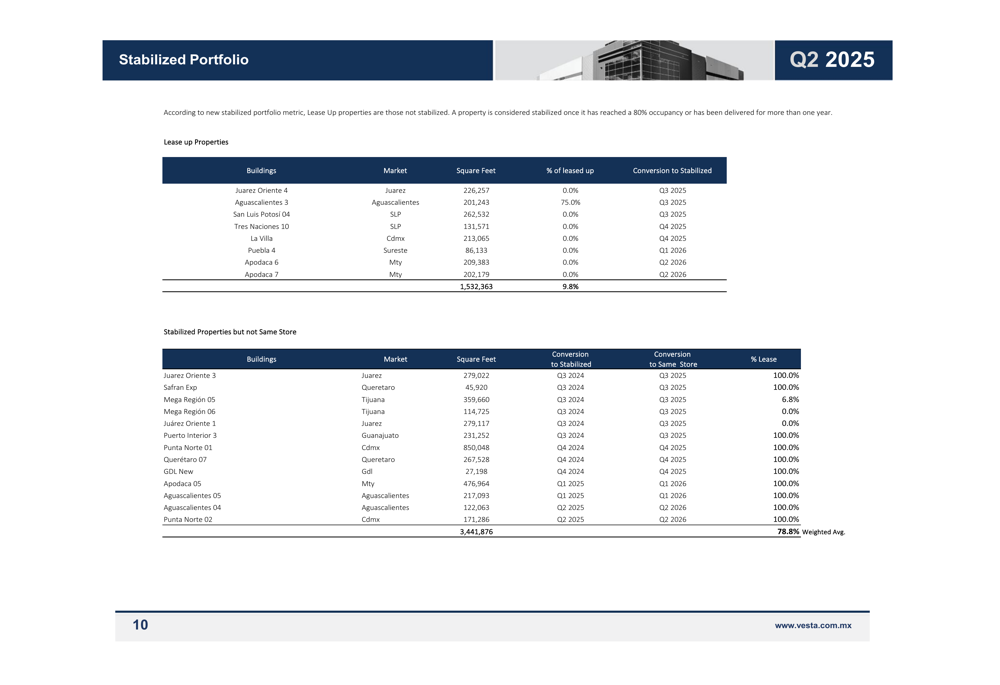

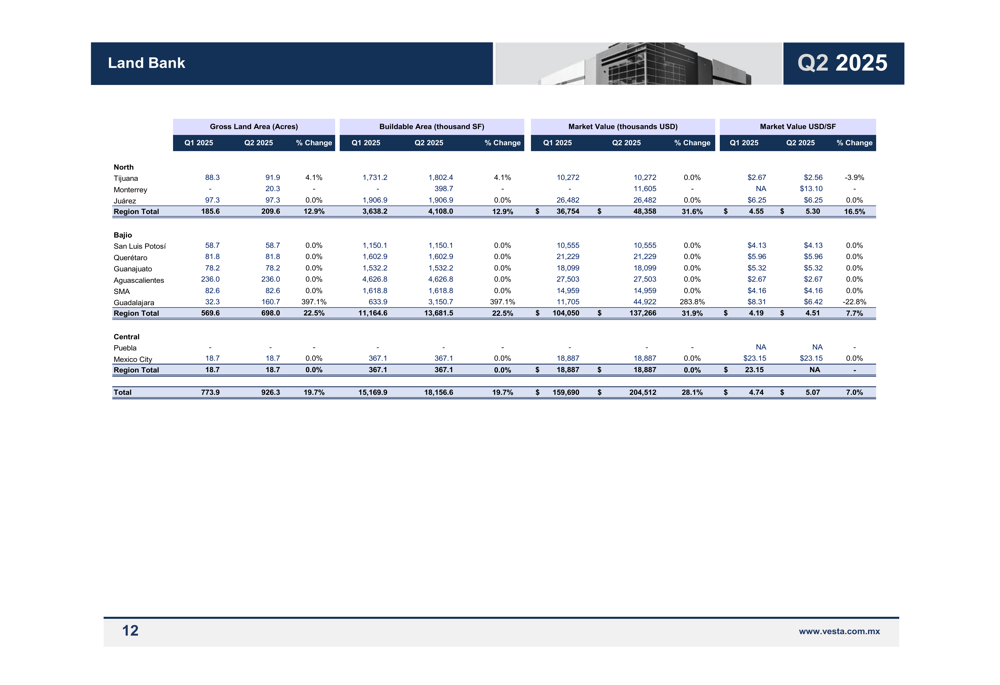

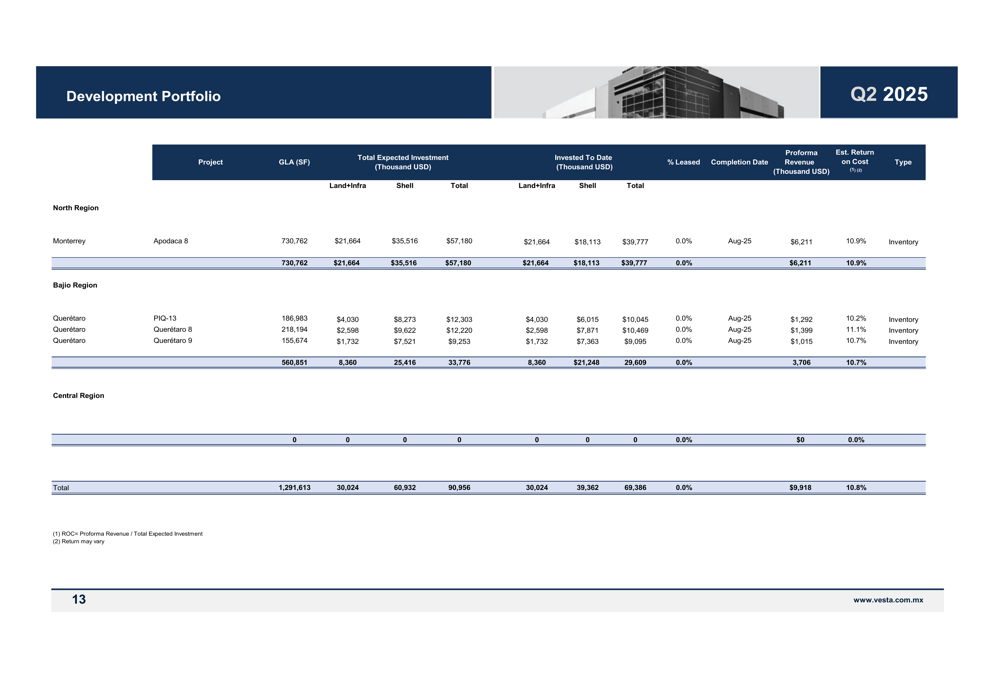

Development Pipeline and Land Bank

Vesta continues to invest in future growth through its development pipeline and strategic land acquisitions. The company’s land bank increased in value by 28.1% from Q1 2025 to Q2 2025, reaching $204.51 million. Notable projects under development include Apodaca 8 in Monterrey with 730,762 sqft and a total expected investment of $57.18 million, and PIQ-13 in Queretaro with 186,983 sqft and a $12.30 million investment.

The company’s development portfolio details are shown below:

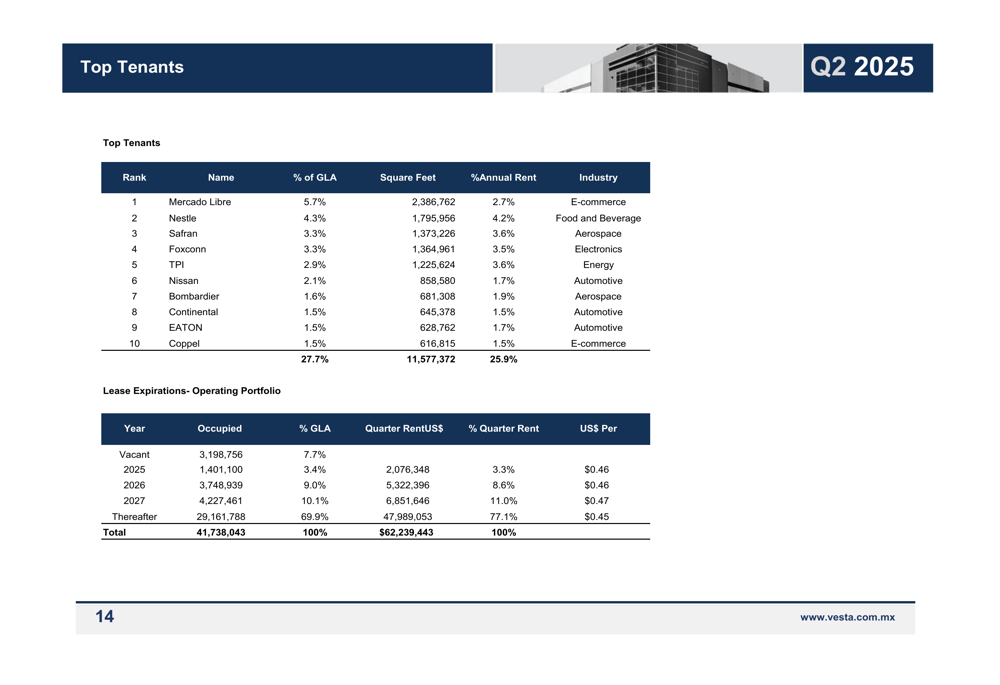

Vesta’s tenant diversification remains strong, with Mercado Libre representing the largest tenant at 5.7% of gross leasable area (GLA), followed by Nestle at 4.3% and Safran at 3.3%. Importantly, 69.9% of leases expire after 2027, providing revenue stability for the coming years.

The tenant distribution and lease expiration schedule are detailed here:

Analyst Perspectives

Despite the mixed financial results, analyst sentiment remains predominantly positive. Most analysts covering Vesta maintain "Buy" ratings, with price targets ranging from $43.00 to $72.90. Only Goldman Sachs has a "Sell" rating with a $43.00 target. This positive outlook suggests confidence in Vesta’s long-term strategy and market position despite current challenges.

The Net Asset Value (NAV) per share has shown consistent growth, reaching $3.58 in Q2 2025, with overall Net Asset Value increasing 1.9% year-over-year to $3.06 billion.

Forward-Looking Statements

Looking ahead, Vesta is focused on its Route 2030 strategy, with plans to renew approximately 4 million square feet of leases in 2026. The company anticipates potential rent increases of 20-30% on these renewals, supported by the positive leasing spread trend that increased to 13.7% in Q2 2025 from 7.7% in Q3 2024.

However, investors should consider several risks, including macroeconomic pressures affecting leasing momentum, supply chain disruptions impacting development timelines, and potential regulatory changes in Mexico. The company’s conservative leverage and strong liquidity position it to navigate these challenges while pursuing strategic growth opportunities.

With a market capitalization of approximately $2.1 billion and a stock price that saw a modest 0.66% increase following the earnings release, Vesta appears to be maintaining investor confidence despite the transitional market environment and declining occupancy metrics.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.