Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Vestjysk Bank (CPH:VJBA) presented its first half 2025 results on August 26, describing performance as "satisfactory" despite a year-over-year decline in profit. The Danish bank reported continued growth in both lending and deposits, extending its streak of loan growth to ten consecutive quarters. Following the presentation, Vestjysk Bank shares fell 2.29% to close at 5.01 DKK.

Quarterly Performance Highlights

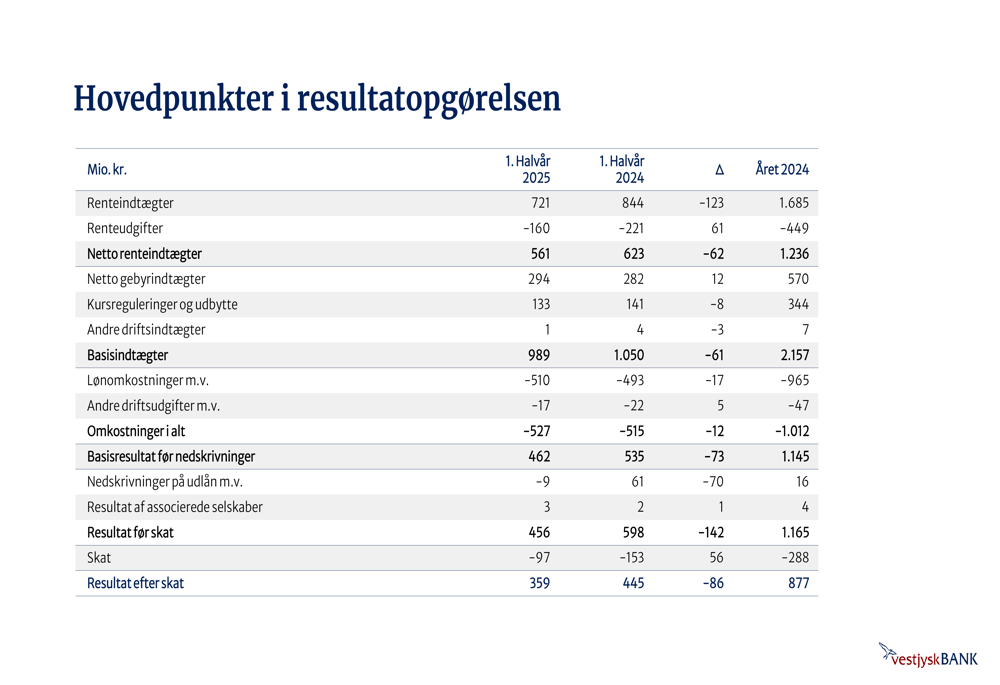

Vestjysk Bank reported a net profit of 359 million DKK for the first half of 2025, representing a 10.0% annual return on equity. This marks a 19.3% decrease from the 445 million DKK reported in the same period of 2024. The bank highlighted low impairment levels and positive contributions from price adjustments as factors supporting the results.

As shown in the detailed income statement below, net interest income declined to 561 million DKK from 623 million DKK in H1 2024, while net fee income increased slightly to 294 million DKK from 282 million DKK:

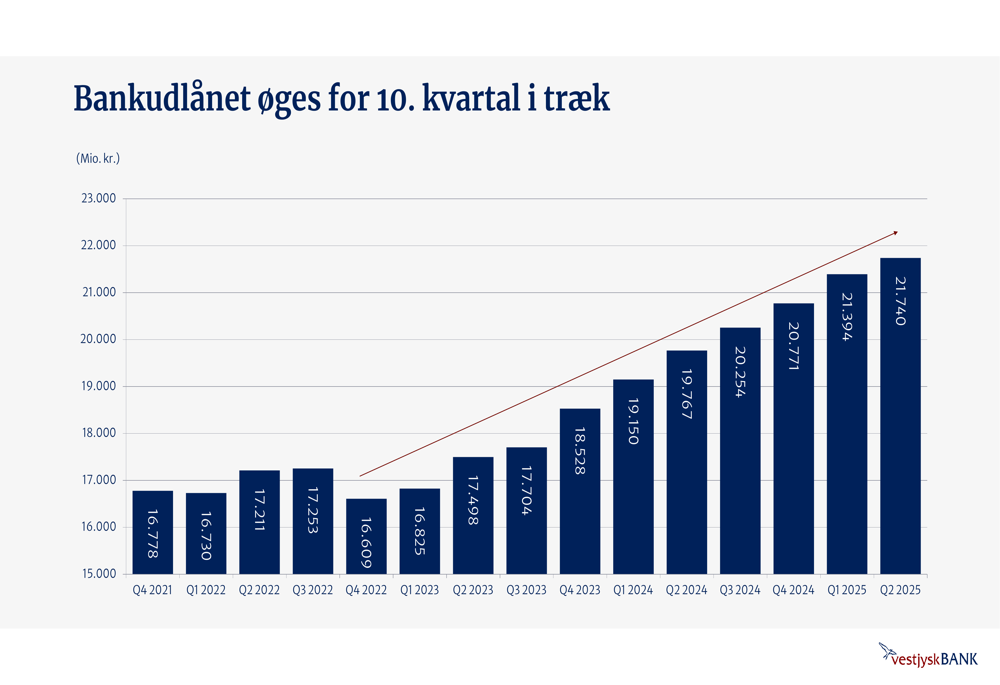

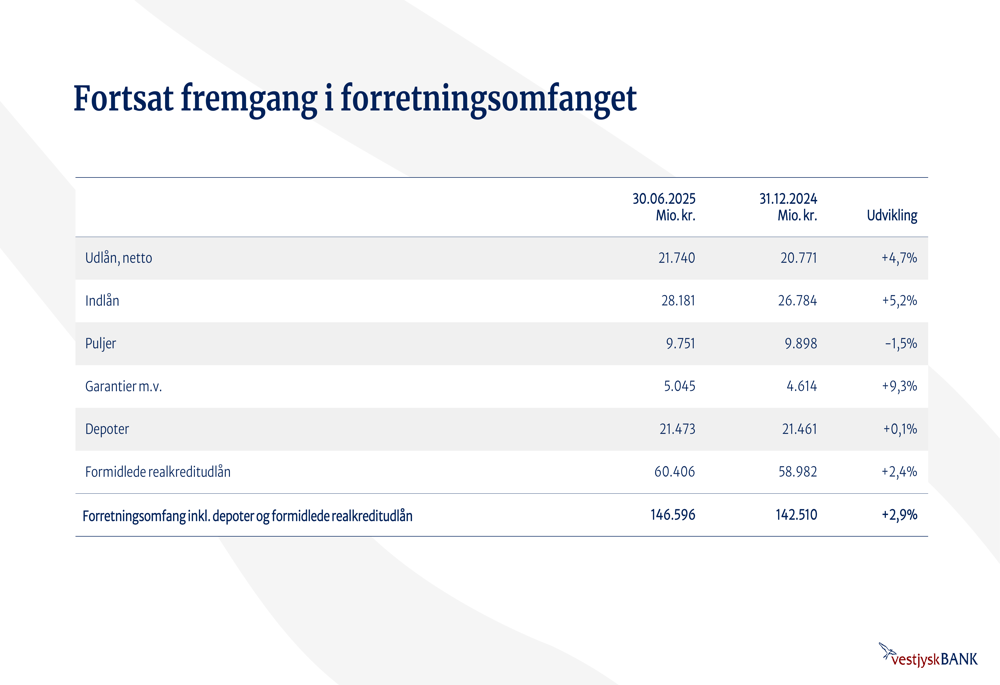

The bank’s lending volume reached 21,740 million DKK as of June 30, 2025, representing a 4.7% increase from year-end 2024. This growth continues a consistent upward trend spanning ten consecutive quarters, as illustrated in the following chart:

Deposit growth was even stronger at 5.2%, reaching 28,181 million DKK. The bank also reported acquiring more than 3,000 new customers during the period, contributing to a 2.9% increase in total business volume.

Detailed Financial Analysis

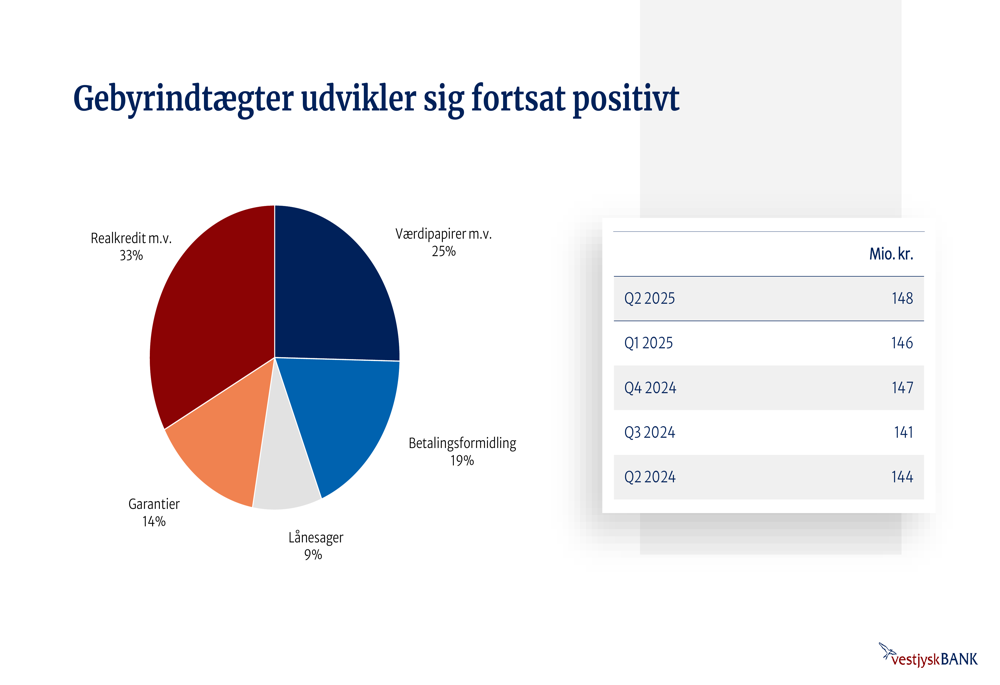

Fee income continued its positive development, with quarterly fee income reaching 148 million DKK in Q2 2025. Mortgage-related fees represented the largest category at 33% of total fee income, followed by securities (25%) and payment services (19%).

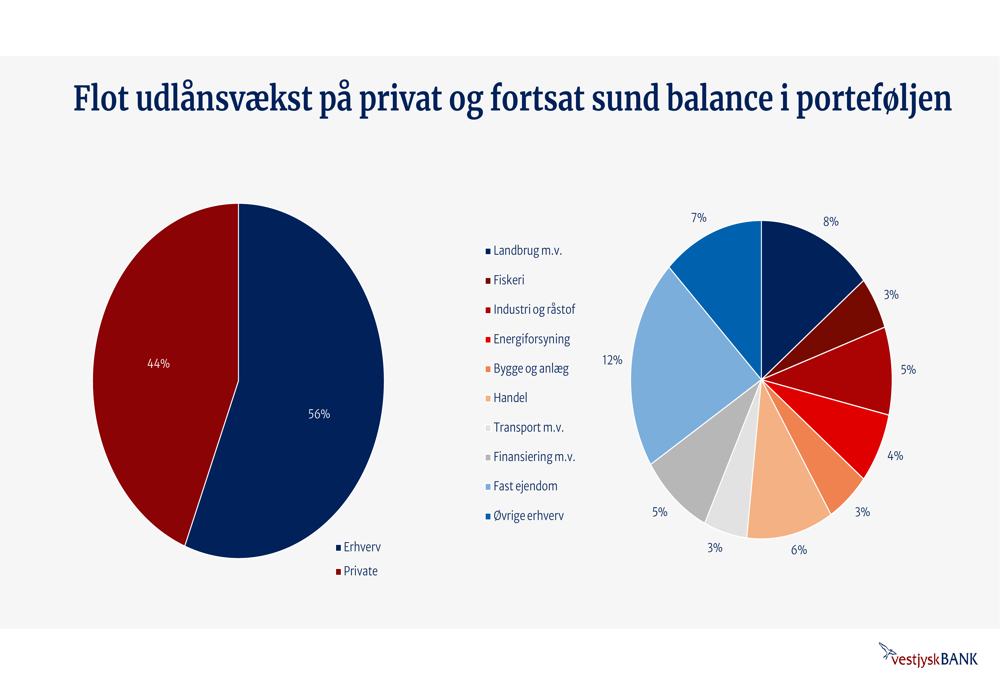

The bank maintains a balanced loan portfolio with 56% allocated to private customers and 44% to corporate clients. Within the corporate segment, financing represents the largest share at 12%, followed by agriculture at 7% and other corporate segments at 7%.

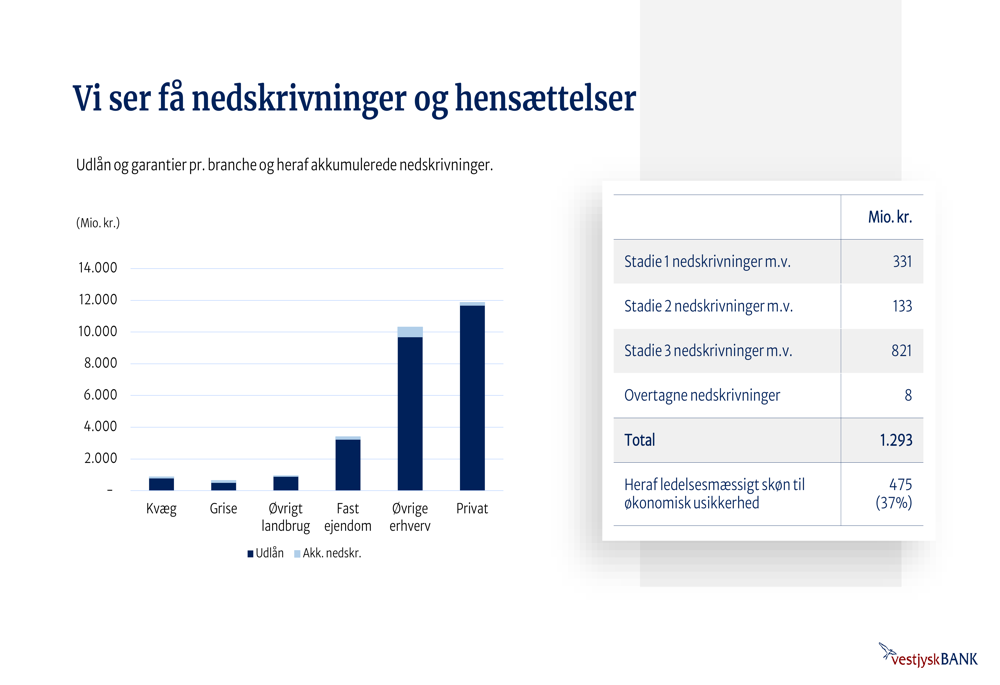

Impairments and provisions remained at low levels, with total accumulated write-downs of 1,293 million DKK. Of this amount, 37% (475 million DKK) represents management’s estimate for economic uncertainty.

Vestjysk Bank continues to maintain strong capital ratios, with Core Tier 1 capital at 20.8%, significantly exceeding both its financial target of 16.0% and the regulatory requirement of 12.1%. The bank’s total capital ratio stands at 25.1%, while its NEP capital ratio (for resolution purposes) is 36.1%.

Strategic Initiatives & Outlook

Vestjysk Bank’s Strategy 2030, branded as "Mere for flere" (More for more), focuses on five key pillars: delivering profitable growth, providing targeted advice, developing one culture, running an efficient business, and maintaining internal order.

Despite the year-over-year profit decline, management reaffirmed its outlook for the full year 2025, projecting a net profit between 600-800 million DKK. The bank also confirmed its financial targets, including a minimum 9.0% return on equity, a cost/income ratio below 50% (though the current ratio of 53.3% exceeds this target), a minimum core equity capital of 16.0%, and a dividend payout ratio of 25-50% of annual profit.

The bank’s ability to maintain loan growth for ten consecutive quarters demonstrates resilience in a challenging market environment. However, the rising cost-to-income ratio and declining net interest income present challenges that management will need to address to achieve its full-year targets and strategic objectives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.