Goldman Sachs chief credit strategist Lotfi Karoui departs after 18 years - Bloomberg

Introduction & Market Context

Victory Capital Holdings Inc . (NASDAQ:VCTR) presented its second quarter 2025 earnings results on August 8, 2025, showcasing substantial growth following its acquisition of Pioneer Investments and strategic transaction with Amundi. The asset manager reported significant increases in total client assets, revenue, and adjusted earnings, demonstrating the immediate impact of its recent strategic moves in a competitive industry landscape.

The presentation follows Victory Capital’s first quarter results, which showed resilience despite a revenue dip. The company’s stock closed at $67.12 on August 7, 2025, representing a 2.99% decline for the day, according to market data.

Quarterly Performance Highlights

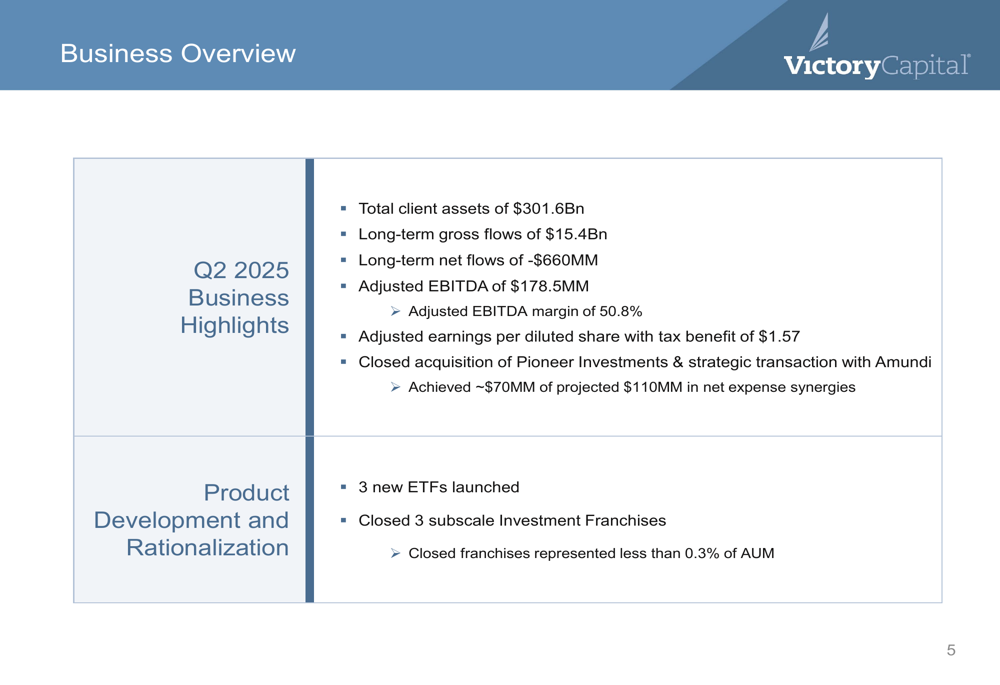

Victory Capital reported total client assets of $301.6 billion for Q2 2025, representing a dramatic 76% increase from $171.4 billion in the previous quarter. This substantial growth primarily reflects the impact of the Pioneer Investments acquisition. The company also highlighted strong long-term gross flows of $15.4 billion, which grew 66% compared to Q1 2025 and 165% versus the same quarter last year.

As shown in the following business highlights chart, the company achieved adjusted earnings per diluted share of $1.57 with tax benefit, alongside an adjusted EBITDA margin of 50.8%:

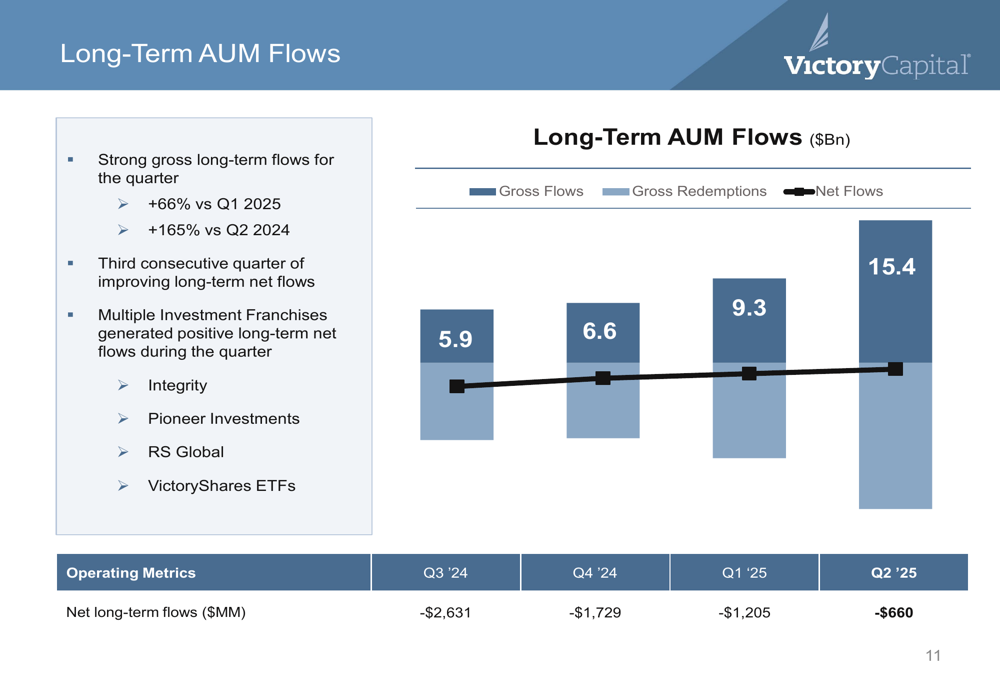

Long-term net flows, while still negative at -$660 million, showed continued improvement for the third consecutive quarter. This represents a significant reduction from -$1,205 million in Q1 2025 and -$2,631 million in Q3 2024. Multiple investment franchises generated positive long-term net flows during the quarter, including Integrity, Pioneer Investments, RS Global, and VictoryShares ETFs.

The following chart illustrates the improving trend in long-term AUM flows:

Investment Performance

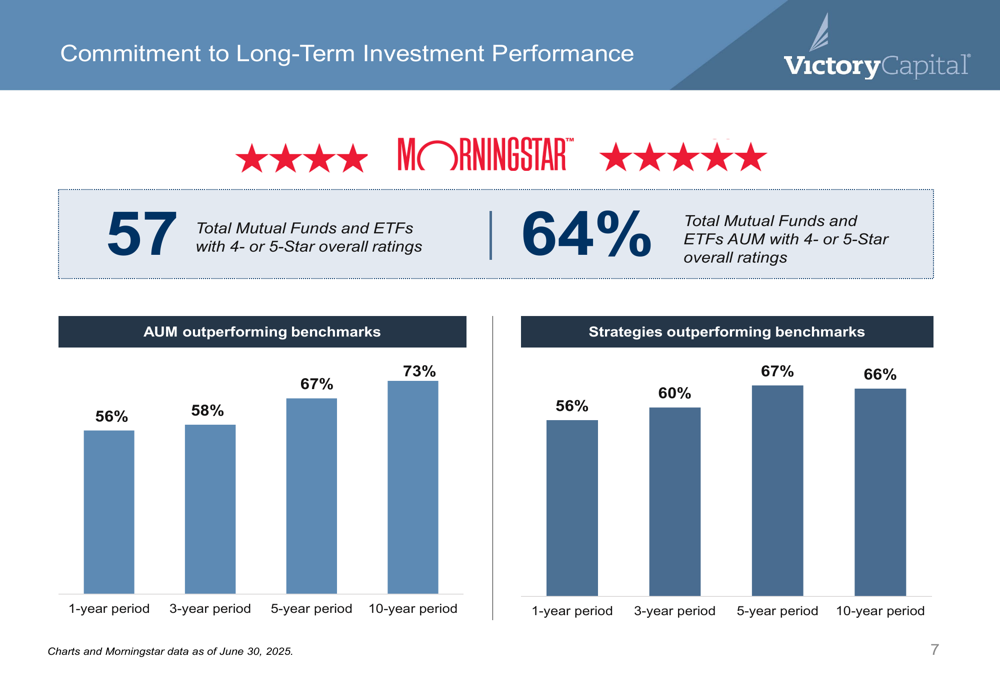

Victory Capital emphasized its commitment to long-term investment performance, reporting that 57 total mutual funds and ETFs have received 4- or 5-star overall ratings from Morningstar. Additionally, 64% of total mutual funds and ETFs AUM have 4- or 5-star overall ratings.

The company’s investment performance relative to benchmarks shows strength across various time periods, with 56% of AUM outperforming benchmarks over a 1-year period, increasing to 73% over a 10-year period. Similarly, 56% of strategies outperformed benchmarks over a 1-year period, rising to 66% over a 10-year period.

As illustrated in the following performance chart, the company’s long-term investment performance demonstrates consistent strength:

Financial Results

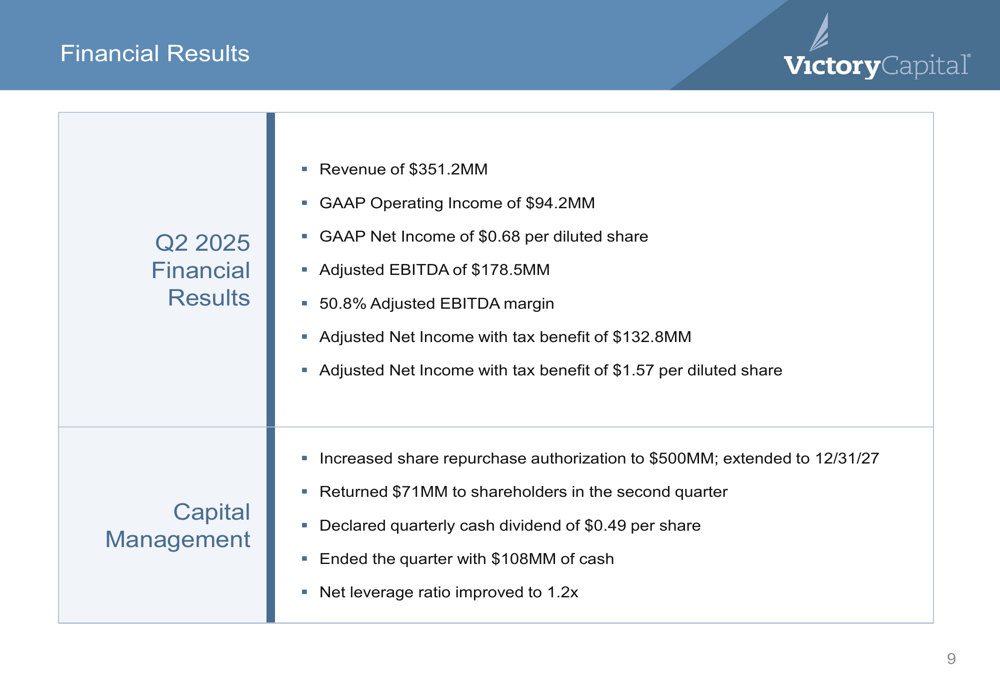

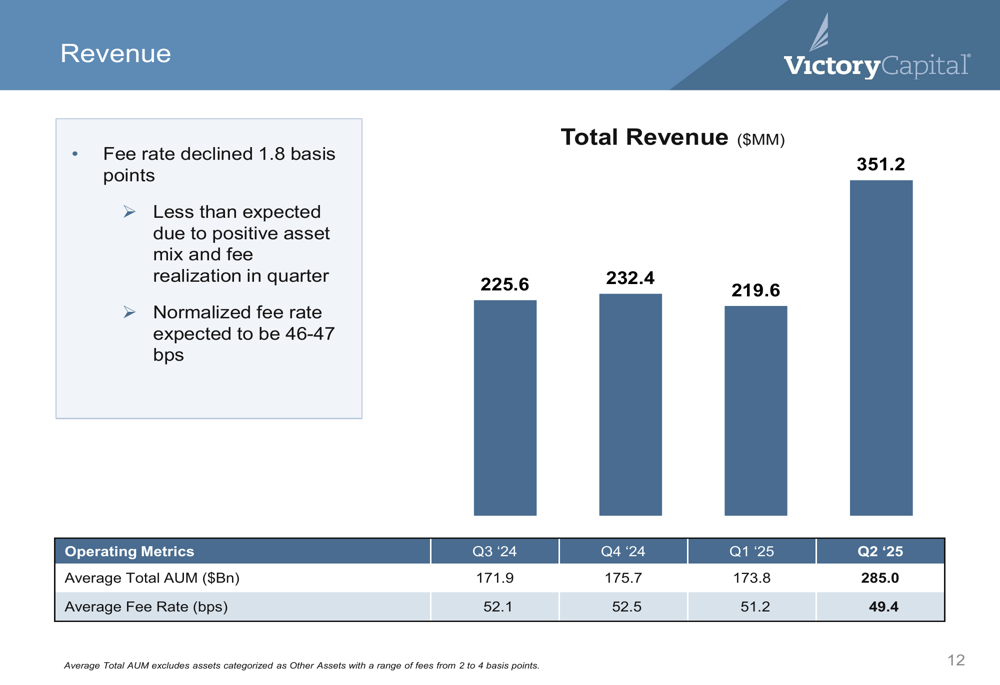

Victory Capital reported substantial financial growth in Q2 2025, with revenue increasing to $351.2 million, up 60% from $219.6 million in Q1 2025. This growth was primarily driven by the Pioneer Investments acquisition, which significantly expanded the company’s asset base.

The company’s adjusted EBITDA reached $178.5 million, up 53% from the previous quarter, while adjusted net income with tax benefit increased 51% to $132.8 million. These figures represent a significant improvement from Q1 2025, when the company reported an EPS of $1.36, slightly below analyst forecasts.

The following chart summarizes the key financial results for Q2 2025:

Revenue growth was accompanied by a slight decline in fee rate, which decreased by 1.8 basis points to 49.4 bps. The company noted that this decline was less than expected due to a positive asset mix and fee realization in the quarter, with a normalized fee rate expected to be 46-47 bps.

The following chart illustrates revenue trends and fee rates:

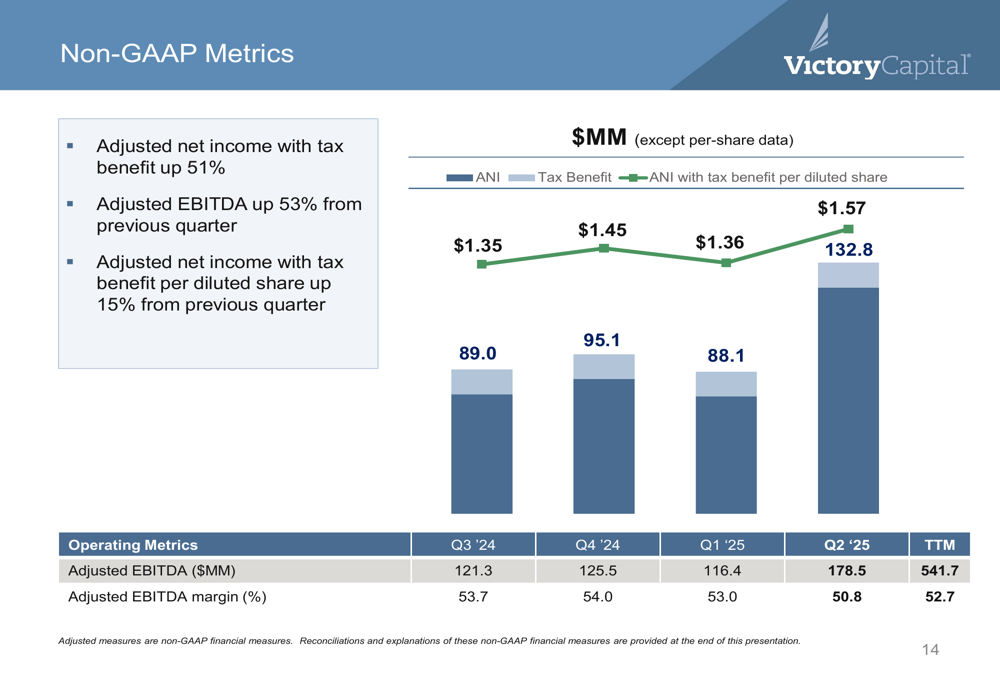

Non-GAAP metrics showed strong performance, with adjusted net income with tax benefit per diluted share increasing 15% from the previous quarter. The trailing twelve-month adjusted EBITDA reached $541.7 million with a margin of 52.7%.

As shown in the following chart of non-GAAP metrics:

Capital Management & Strategic Initiatives

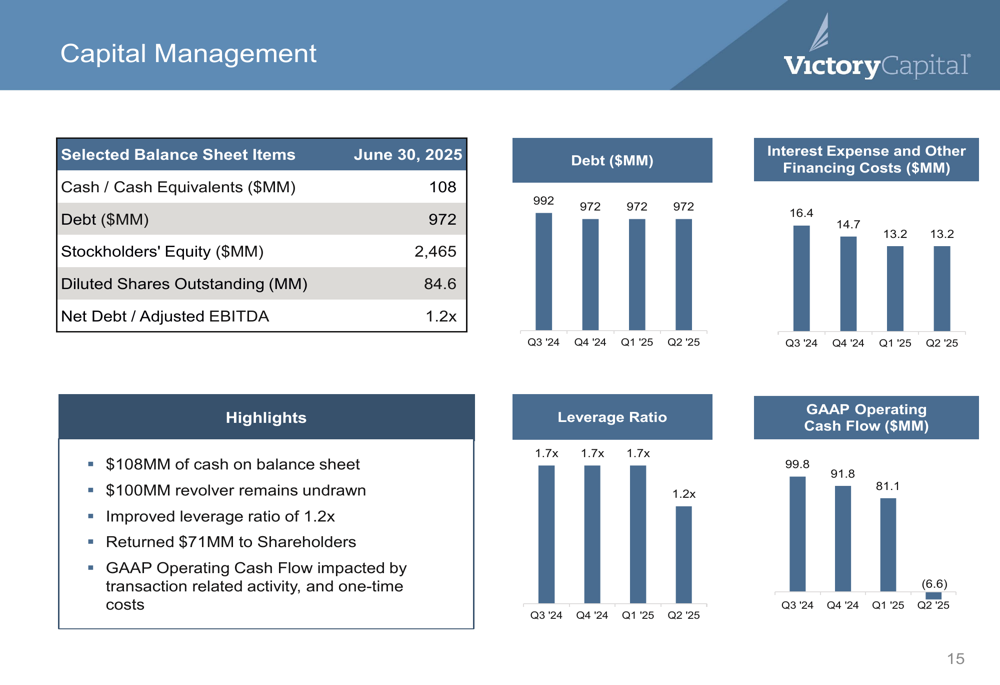

Victory Capital highlighted its capital management activities, reporting $108 million in cash and cash equivalents as of June 30, 2025, with total debt of $972 million. The company’s net leverage ratio improved to 1.2x from 1.7x in the previous quarter, reflecting stronger balance sheet flexibility.

During the quarter, Victory Capital returned $71 million to shareholders and declared a quarterly cash dividend of $0.49 per share. The company also increased its share repurchase authorization to $500 million, extended through December 31, 2027.

The following chart details the company’s capital management position:

Victory Capital reported that it has achieved approximately $70 million of the expected $110 million in total net expense synergies associated with the Amundi transaction. This progress aligns with the company’s previous guidance mentioned in its Q1 2025 earnings call.

The company also launched three new ETFs during the quarter while closing three subscale Investment Franchises that represented less than 0.3% of AUM, demonstrating its focus on optimizing its product offerings.

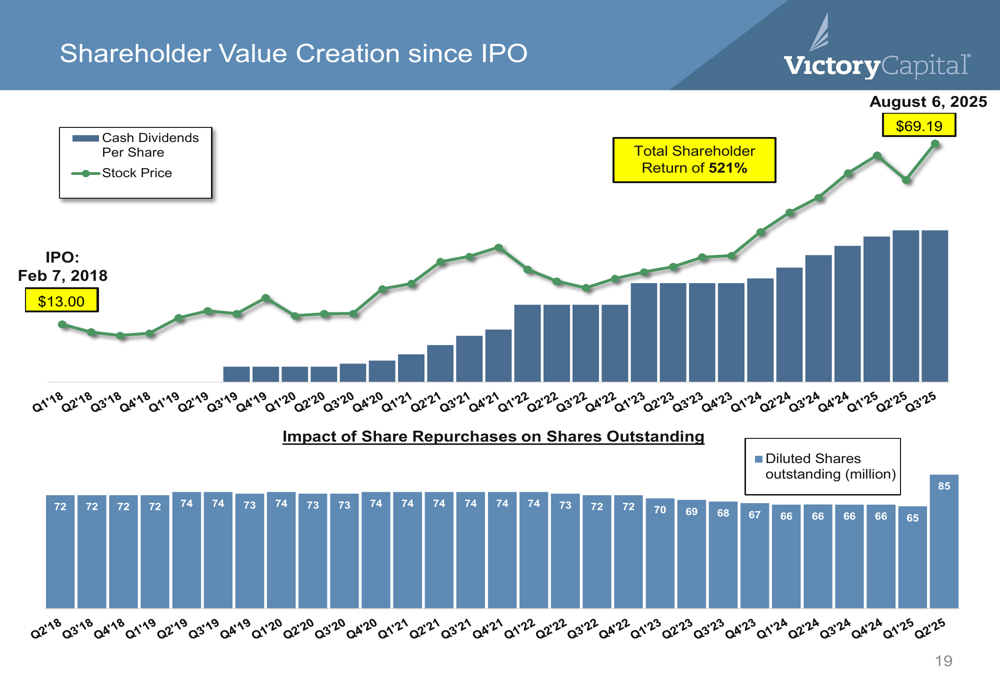

Since its IPO in February 2018, Victory Capital has delivered a total shareholder return of 521%, with the stock price increasing from $13.00 at IPO to $69.19 as of August 6, 2025, as illustrated in the following chart:

Forward-Looking Statements

Looking ahead, Victory Capital appears well-positioned for continued growth, with a strengthened balance sheet and improved operational efficiency. The company’s long-term growth strategy emphasizes enhancing shareholder value through strategic acquisitions, evolving its product set to drive organic growth, and gaining efficiency from its integrated platform.

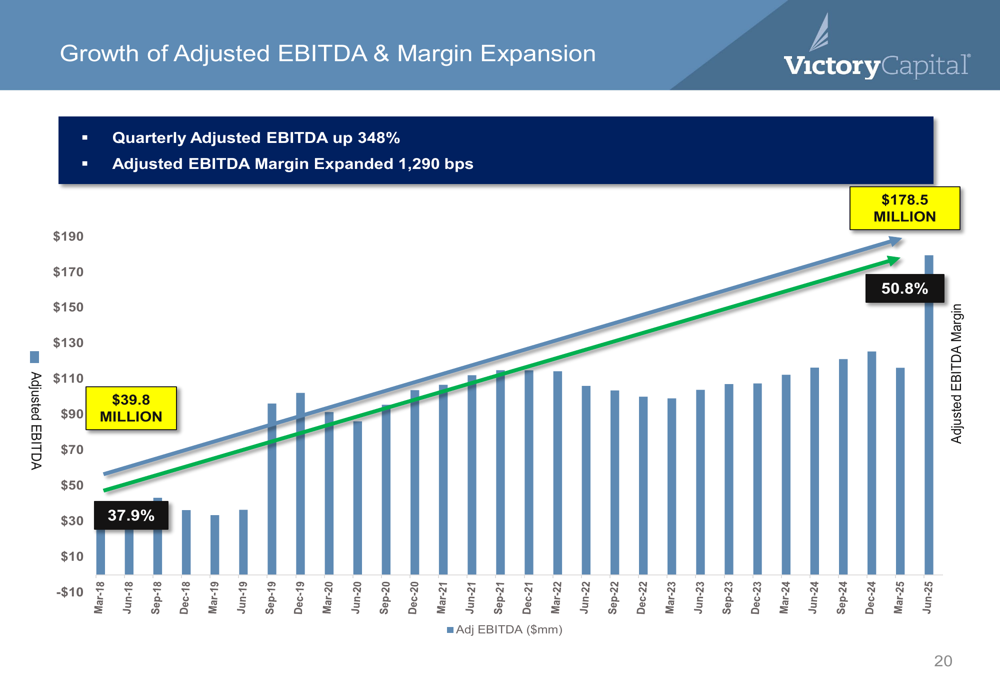

The company’s adjusted EBITDA has grown 348% since March 2018, with margin expansion of 1,290 basis points to 50.8%. This demonstrates Victory Capital’s ability to drive profitability while scaling its business, as shown in the following chart:

With its improved leverage ratio and strong cash position, Victory Capital is positioned to pursue additional strategic acquisitions while continuing to return capital to shareholders through dividends and share repurchases. The company’s focus on expanding its ETF offerings and leveraging Amundi’s global distribution network should support its organic growth initiatives.

While the company’s GAAP operating cash flow was impacted by transaction-related activity and one-time costs in Q2 2025, resulting in -$6.6 million compared to $81.1 million in Q1 2025, the long-term financial trajectory remains positive as synergies from recent acquisitions continue to materialize.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.