Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Viper Energy (NASDAQ:VNOM) released its Q1 2025 investor presentation on May 6, 2025, highlighting strong quarterly results and an optimistic outlook following its recent acquisition from parent company Diamondback Energy (NASDAQ:FANG). Despite the positive operational performance, Viper’s stock has faced pressure in recent trading, closing at $42.08 with a 1.59% decline, though showing signs of recovery with a 2.03% gain in after-hours trading.

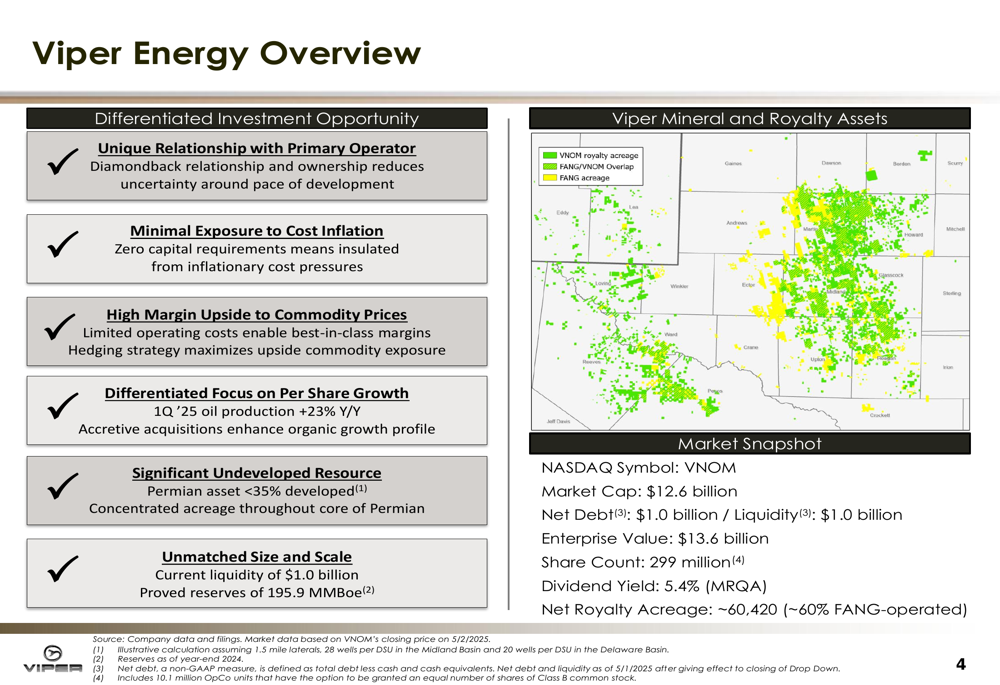

The royalty company, which owns mineral interests primarily in the Permian Basin, continues to position itself as a differentiated investment opportunity with high margins and significant upside to commodity prices. With an enterprise value of $13.6 billion and a market capitalization of $12.6 billion, Viper represents one of the largest pure-play royalty companies in the oil and gas sector.

Quarterly Performance Highlights

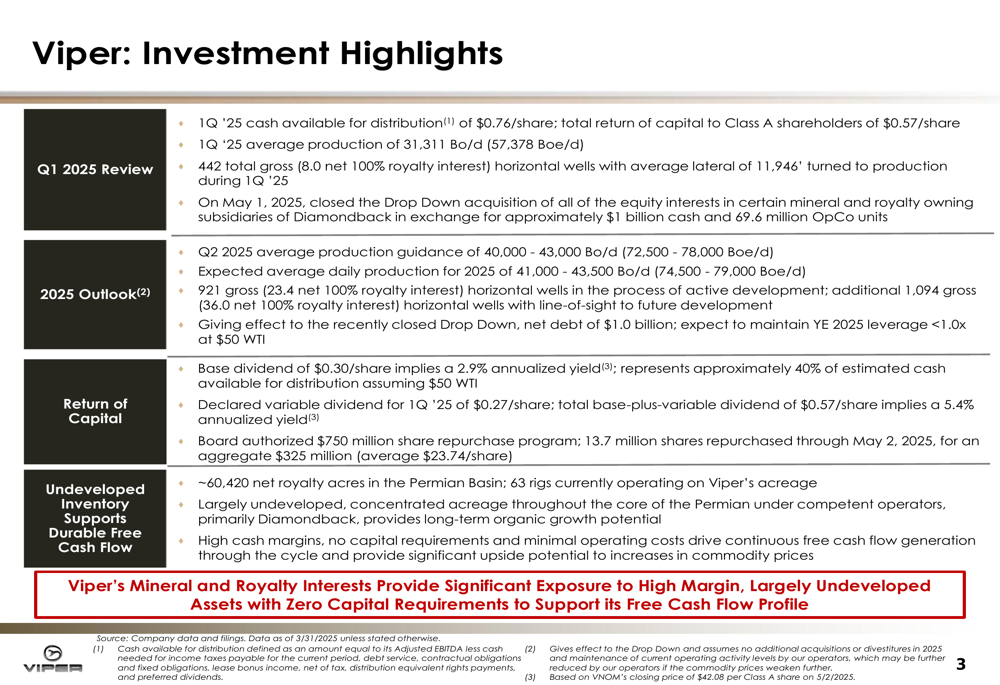

For Q1 2025, Viper reported cash available for distribution of $0.76 per share, supporting both its base and variable dividend programs. The company’s average production reached 31,311 barrels of oil per day (57,378 barrels of oil equivalent per day), slightly exceeding the guidance provided in its Q4 2024 earnings call.

The company saw 442 total gross horizontal wells turned to production during the quarter, contributing to its production growth. This development activity continues to be driven by both Diamondback and third-party operators, with 63 rigs currently operating on Viper’s acreage.

As shown in the following investment highlights slide, Viper maintains a strong financial position with expected year-end 2025 leverage below 1.0x at $50 WTI and net debt of $1.0 billion:

Strategic Initiatives

The most significant development highlighted in the presentation is the completion of the Drop Down acquisition from Diamondback Energy, which closed on May 1, 2025. This strategic transaction is expected to substantially increase Viper’s production profile, as reflected in the company’s updated guidance.

Viper’s business model continues to benefit from its unique relationship with Diamondback, which operates approximately 60% of Viper’s net royalty acreage. This alignment provides visibility into future development and helps mitigate operational risks.

The following slide illustrates Viper’s asset positioning and relationship with Diamondback:

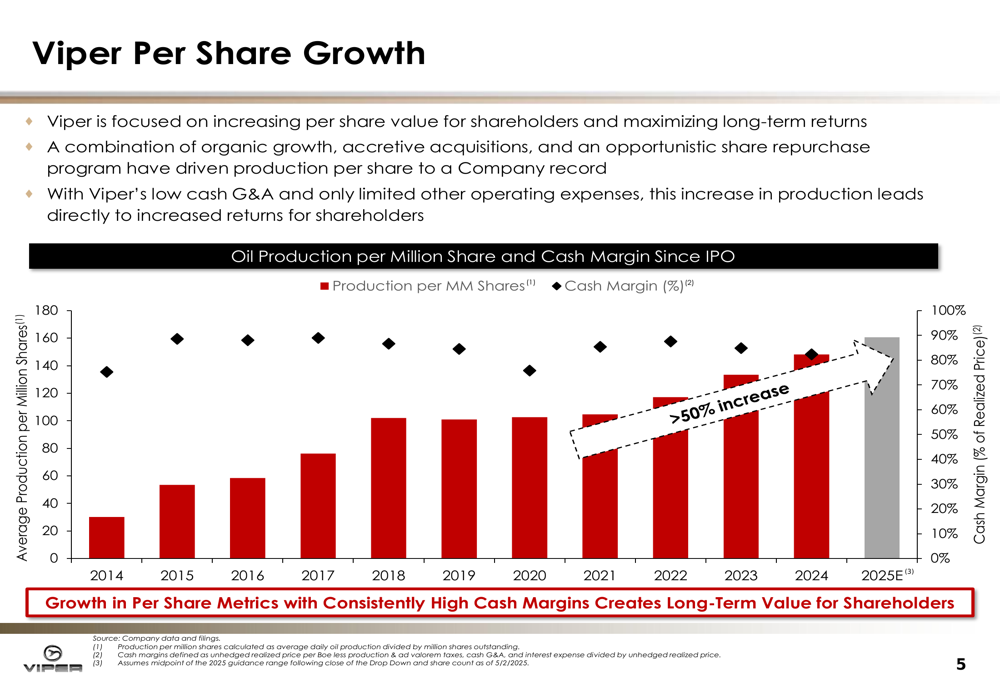

Viper has consistently focused on per-share growth through a combination of organic development, accretive acquisitions, and opportunistic share repurchases. This strategy has driven production per million shares to a company record, as illustrated in the following chart:

Forward-Looking Statements

Following the Drop Down acquisition, Viper has significantly increased its production guidance. For Q2 2025, the company expects average production of 40,000-43,000 barrels of oil per day (72,500-78,000 barrels of oil equivalent per day), representing a substantial increase from Q1 levels. For the full year 2025, Viper anticipates average daily production of 41,000-43,500 barrels of oil per day (74,500-79,000 barrels of oil equivalent per day).

The company’s near-term development visibility remains strong, with 921 gross horizontal wells in the process of active development across its acreage position. Additionally, Viper identified 1,094 gross line-of-sight wells that are not currently being developed but represent future production potential.

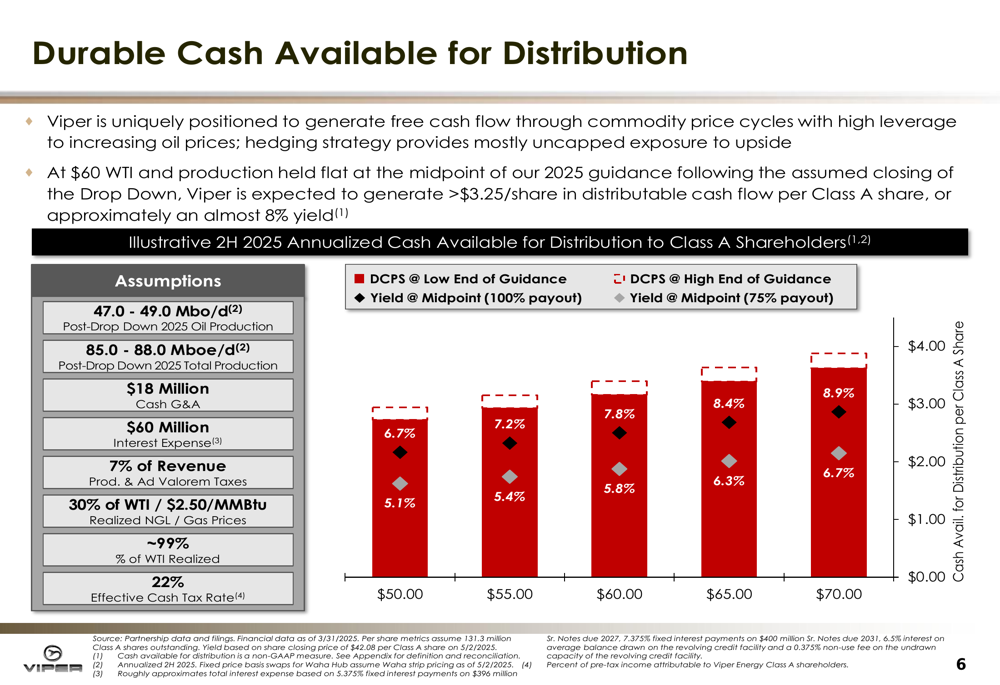

At various oil price scenarios, Viper projects robust cash available for distribution, as shown in the following chart:

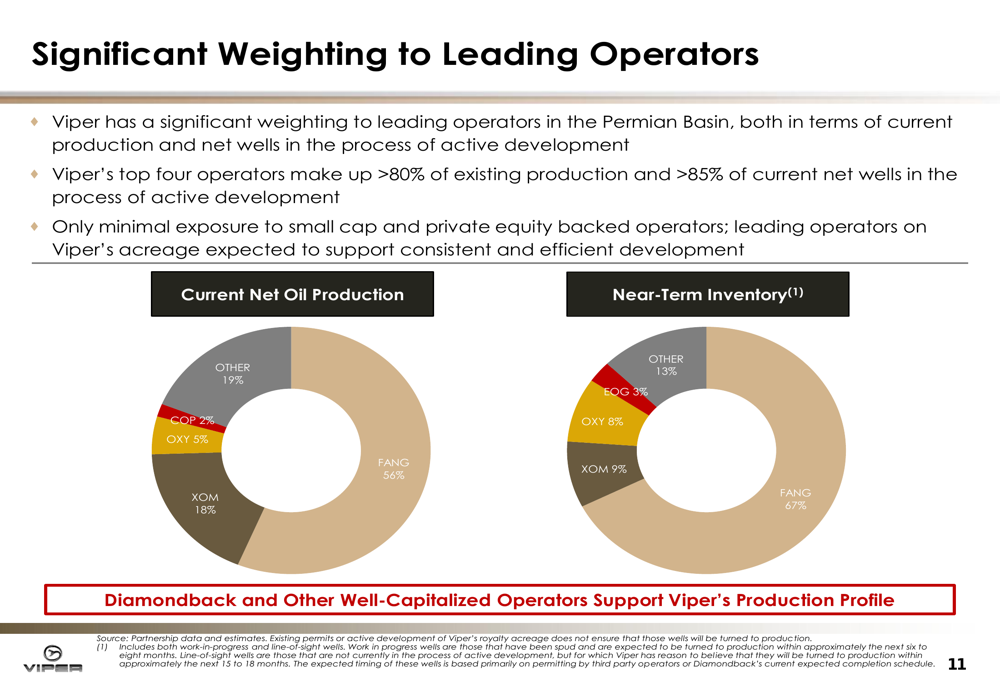

The company’s portfolio continues to be weighted toward leading operators in the Permian Basin, with Diamondback, ExxonMobil (NYSE:XOM), and Occidental Petroleum (NYSE:OXY) accounting for over 80% of existing production and over 85% of current net wells in active development:

Shareholder Returns

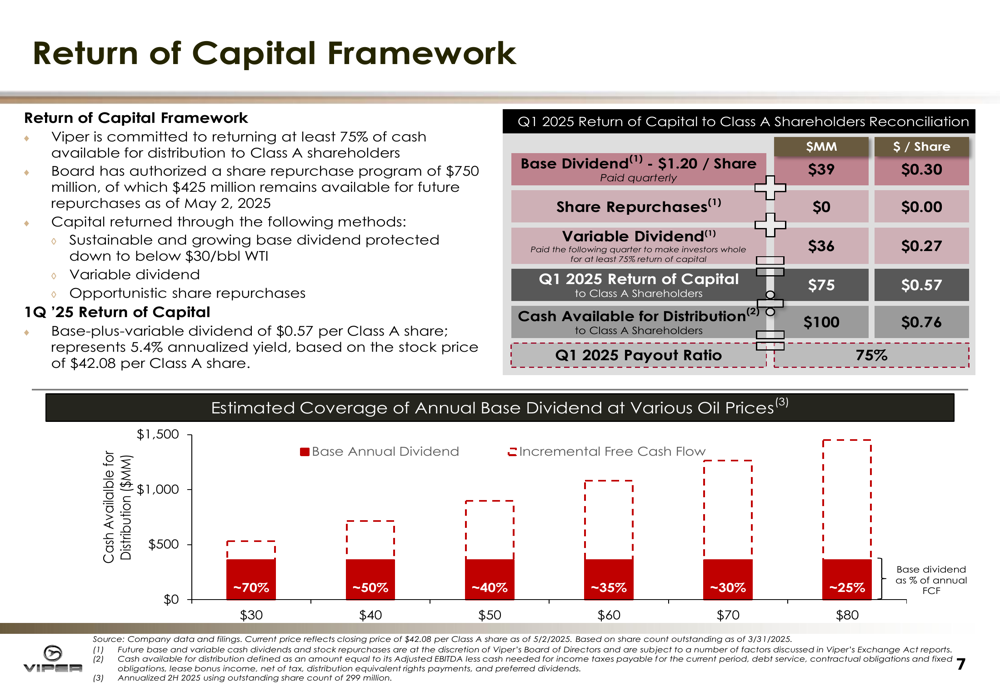

Viper maintains a commitment to returning capital to shareholders through a combination of base dividends, variable dividends, and share repurchases. For Q1 2025, the company declared a base dividend of $0.30 per share (implying a 2.9% annualized yield) and a variable dividend of $0.27 per share (implying a 5.4% annualized yield).

The company’s board has authorized a $750 million share repurchase program, with 13.7 million shares repurchased through May 2, 2025, at an average price of $23.74 per share. Viper is committed to returning at least 75% of cash available for distribution to Class A shareholders, as illustrated in the following return of capital framework:

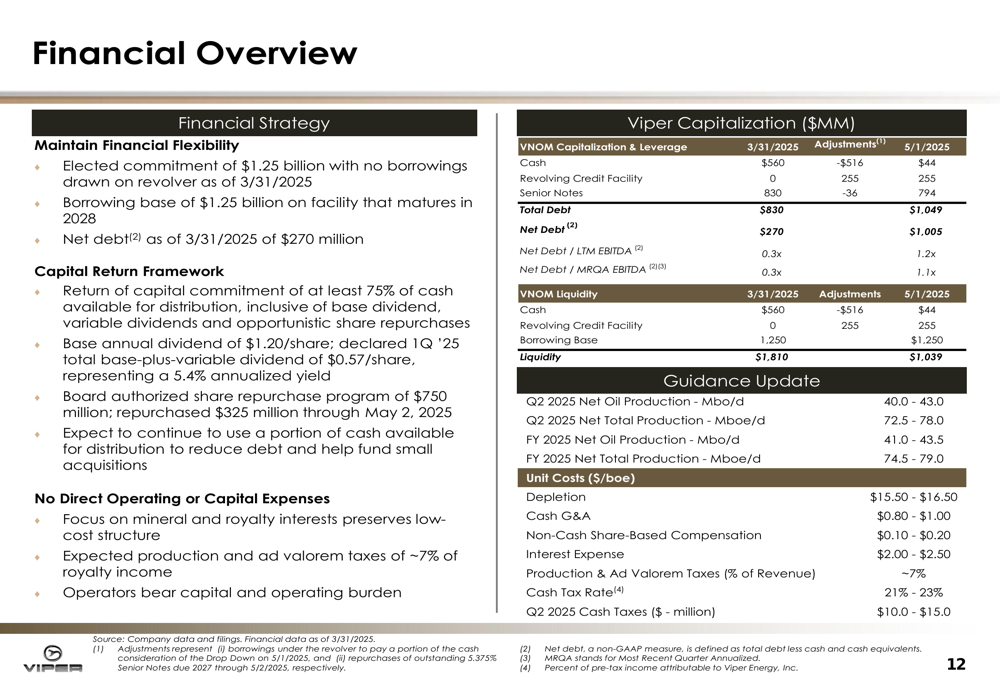

The company’s financial position remains strong, with $44 million in cash and $1,049 million in total debt as of May 1, 2025, following the Drop Down acquisition. Viper maintains financial flexibility with an elected commitment of $1.25 billion on its revolving credit facility, which matures in 2028.

Despite the positive operational outlook presented in the Q1 slides, Viper’s stock has underperformed relative to its strong Q4 2024 results, which saw earnings per share of $2.04 significantly exceeding the forecasted $0.45. This disconnect between operational performance and stock price movement suggests investors may be focusing on broader market conditions or other factors beyond the company’s core business fundamentals.

As Viper continues to execute on its growth strategy and capital return framework, investors will be watching closely to see if the increased production guidance following the Diamondback Drop Down acquisition translates into enhanced shareholder returns in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.