Novo Nordisk, Eli Lilly slide after Trump comments on weight loss drug pricing

Introduction & Market Context

Visteon Corporation (NYSE:VC) presented its second quarter 2025 earnings results on July 24, showing resilience in a challenging automotive market. The company reported $969 million in net sales with a 1% growth-over-market performance, despite significant headwinds in China. Visteon’s stock has shown strong performance year-to-date with a 27% return, though it closed at $112.43 on the earnings day, down 0.69% from the previous session.

The automotive supplier demonstrated confidence in its outlook by raising full-year guidance across all key metrics, highlighting its strategic shift toward diversification in both products and markets. This comes as vehicle production is forecasted to decline by 5% in the second half of 2025, presenting potential challenges for the industry.

Quarterly Performance Highlights

Visteon delivered solid financial results in Q2 2025, achieving $134 million in adjusted EBITDA with a 13.8% margin, representing a 40 basis point improvement over the prior year. The company generated $67 million in adjusted free cash flow and maintained a strong balance sheet with $361 million in net cash.

As shown in the following financial highlights slide:

Regional performance varied significantly across markets, with Europe and Rest of Asia each delivering 8% growth-over-market, while the Americas saw a 4% decline. Most notably, China experienced a 30% decrease in growth-over-market, which negatively impacted Visteon’s global performance by 5 percentage points.

The following regional breakdown illustrates these contrasting market dynamics:

Despite the challenges in China, Visteon demonstrated sequential growth in the region from new launches and SmartCore™ upgrades with Geely. In Europe, sales growth was driven by recent launches of cockpit electronics on both internal combustion engine vehicles and EVs, as well as engineering services acquisitions.

Strategic Initiatives

Visteon secured $3.9 billion in new business wins year-to-date, positioning the company to exceed its $6 billion full-year target. The breakdown shows a strategic focus on displays (53%) and clusters (29%), with SmartCore™ & Infotainment (12%) and Electrification & Other (6%) comprising the remainder.

The following chart illustrates this product mix in new business wins:

The company launched 21 new products across eight OEMs during the quarter, spanning passenger vehicles, commercial vehicles, and two-wheeler markets. These launches reflect Visteon’s strategic diversification beyond traditional automotive segments and include notable models such as the Volvo EX30 electric vehicle, Audi Q3, and Royal Enfield 350 two-wheeler.

The product launch highlights demonstrate this diversification strategy:

CEO Sachin Lawande expressed optimism about the company’s trajectory, stating in the earnings call, "We fully expect as we go forward to see more of a balancing to happen," highlighting Visteon’s strategic positioning for long-term growth.

Forward-Looking Statements

Based on its strong first-half performance, Visteon raised its full-year 2025 guidance across all key metrics. The company now expects sales between $3.70 billion and $3.85 billion, up from the previous range of $3.65 billion to $3.85 billion. Adjusted EBITDA guidance was increased to $475-$505 million from $450-$480 million, and adjusted free cash flow expectations were raised to $195-$225 million from $175-$205 million.

The revised guidance reflects Visteon’s confidence in its ability to navigate industry challenges, as shown in the following slide:

The company identified several industry factors affecting its outlook, including second-half customer production, tariff assumptions, and the phase-out of EV incentives. Despite these challenges, Visteon expects to maintain its growth trajectory through continued operational discipline and strategic initiatives.

Financial Analysis

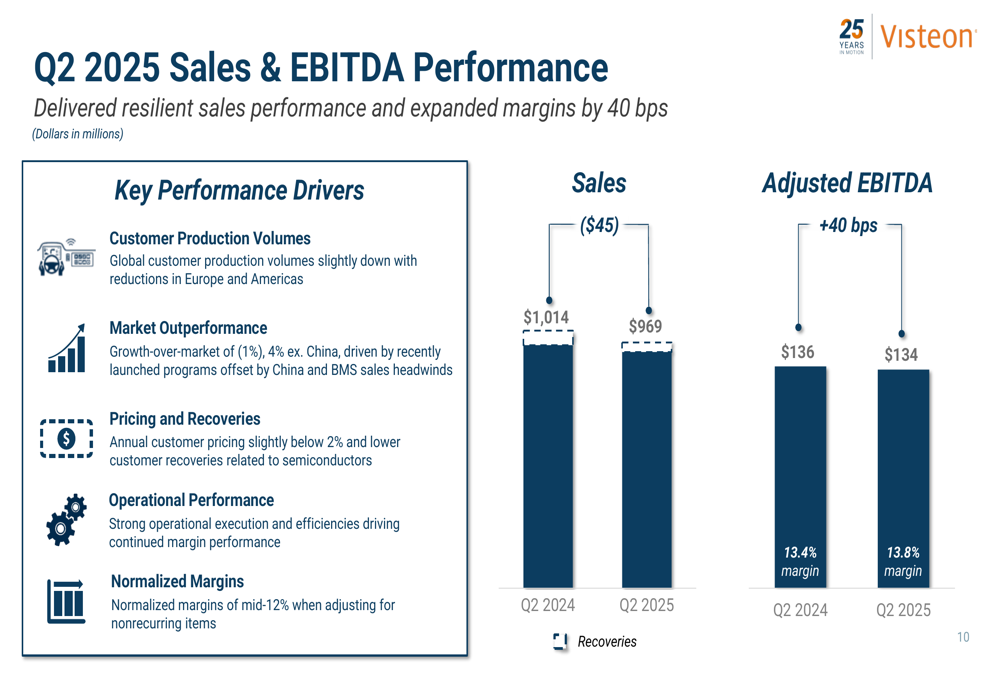

Visteon’s adjusted EBITDA margin expanded from 13.4% in Q2 2024 to 13.8% in Q2 2025, despite a decrease in sales from $1,014 million to $969 million year-over-year. This margin improvement demonstrates the company’s focus on operational efficiency and cost control.

The following chart illustrates the sales and EBITDA performance comparison:

Cash flow generation remained strong, with adjusted free cash flow of $105 million for the first half of 2025, compared to $62 million in the same period of 2024. This improvement was driven by higher adjusted EBITDA ($263 million vs. $238 million) and better working capital management.

CFO Jerome Rouquet emphasized the company’s financial strength during the earnings call, stating, "We are well positioned for long term top line growth, margin expansion, and free cash flow generation."

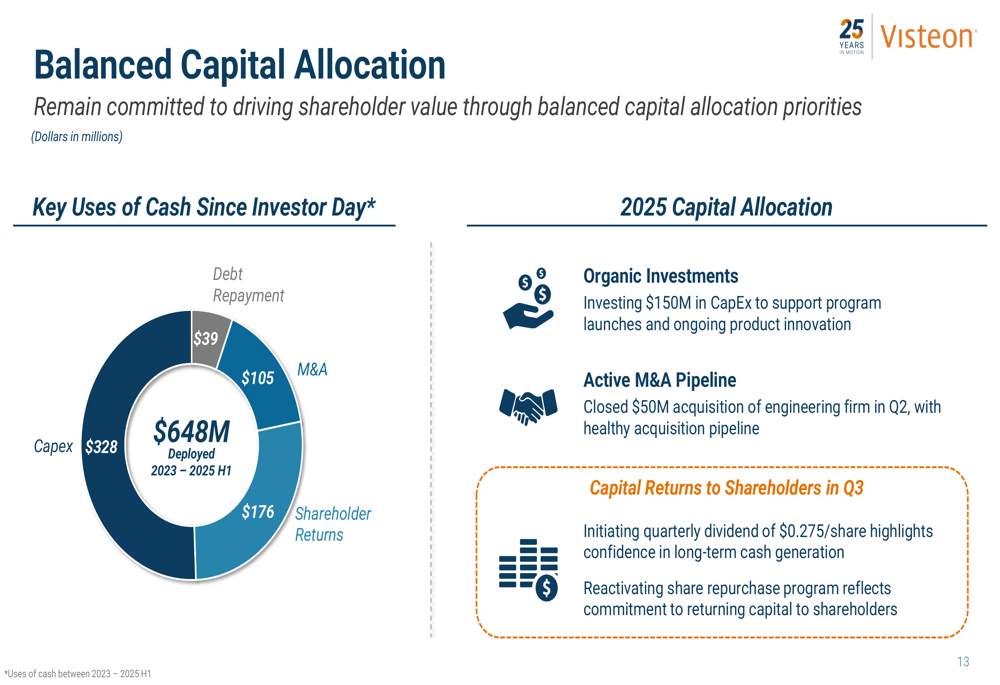

Visteon’s balanced capital allocation strategy includes organic investments, an active M&A pipeline, and capital returns to shareholders. Since its investor day, the company has deployed $648 million across debt repayment ($39 million), M&A ($105 million), shareholder returns ($176 million), and capital expenditures ($328 million).

The following chart shows this balanced approach to capital allocation:

The company has initiated a quarterly dividend of $0.27 per share, reflecting confidence in its sustainable cash generation capabilities. Additionally, Visteon completed its third acquisition as part of its growth strategy, further expanding its technological capabilities and market reach.

As Visteon navigates the evolving automotive landscape, its focus on digital cockpit electronics, innovative product portfolio, competitive cost structure, and balanced capital allocation positions it well for continued success despite regional challenges and industry headwinds.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.