Oracle launches unified health data exchange console

Introduction & Market Context

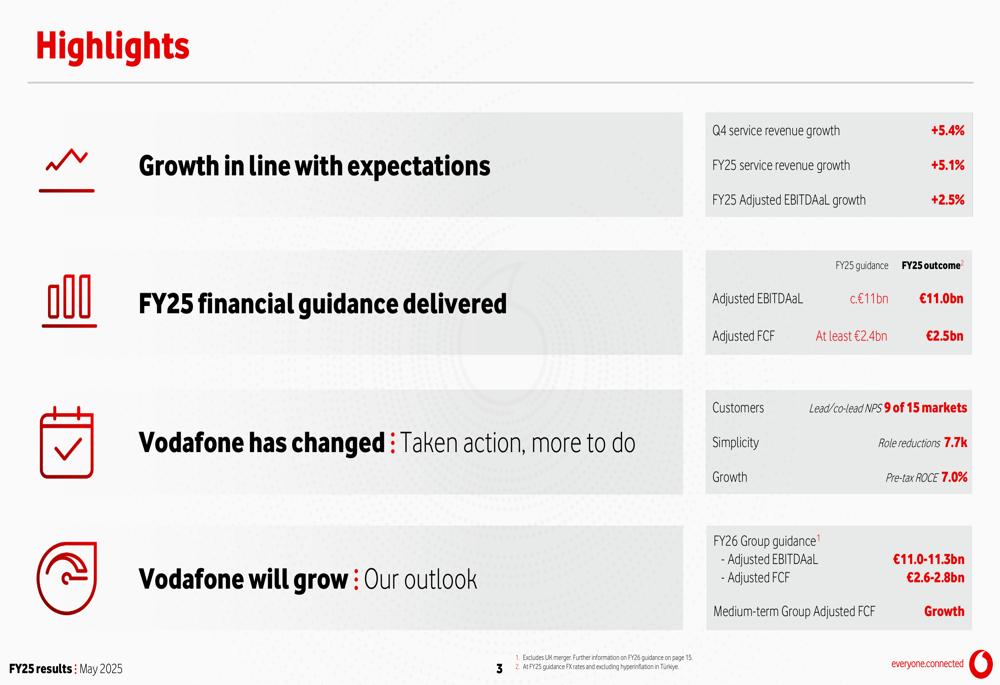

Vodafone Group (LON:VOD) Plc (NASDAQ:VOD) released its FY25 results presentation on May 20, 2025, reporting 5.1% service revenue growth and meeting its financial targets while continuing its strategic transformation. The telecommunications giant delivered adjusted EBITDAaL of €11.0 billion, in line with guidance, and exceeded its free cash flow target with €2.5 billion against guidance of at least €2.4 billion.

The company has made significant progress in reshaping its portfolio, completing the sales of its Spanish and Italian operations while securing approval for its UK merger with Three UK. These strategic moves come as Vodafone aims to focus on markets where it can achieve sustainable growth.

As shown in the following comprehensive overview of Vodafone’s FY25 performance:

Portfolio Restructuring

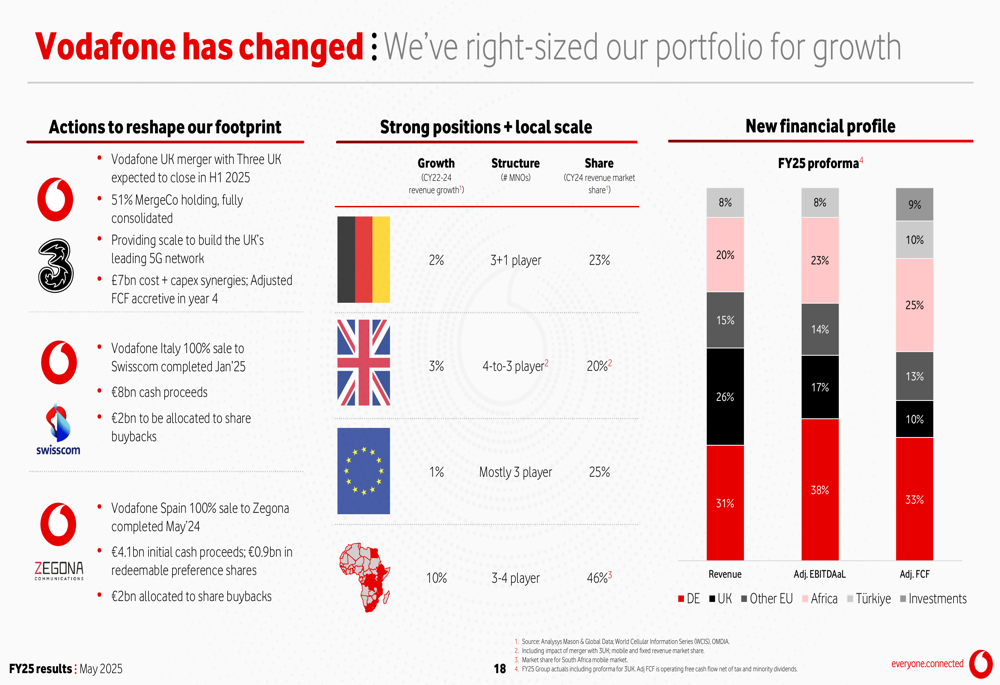

Vodafone has fundamentally reshaped its footprint over the past year, divesting underperforming assets and strengthening its position in growth markets. The company completed the sale of Vodafone Spain to Zegona in May 2024 and agreed to sell Vodafone Italy to Swisscom (SIX:SCMN). Additionally, Vodafone received approval for its UK merger with Three UK, which is expected to close in the first half of 2025.

These strategic moves have transformed Vodafone’s financial profile, with growth markets now representing 67% of Group Adjusted Free Cash Flow, while Germany, which is undergoing a turnaround, accounts for the remaining 33%.

The following image illustrates Vodafone’s portfolio restructuring and new financial profile:

The company has also significantly improved its capital structure, reducing net debt by approximately €11 billion over two years. The current Debt/Adjusted EBITDAAL ratio stands at 2.0x, down from 2.5x in FY24, providing Vodafone with greater financial flexibility.

Regional Performance

Vodafone’s performance varied significantly across regions, with strong results in the UK, Türkiye, and Egypt offsetting challenges in Germany.

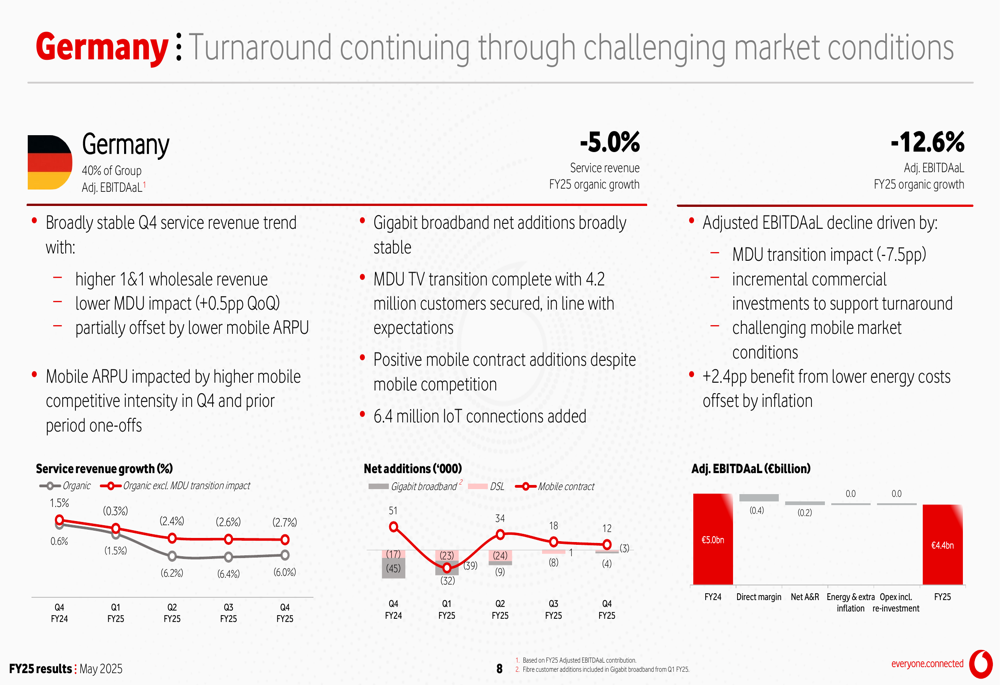

Germany, which contributes 40% of Group Adjusted EBITDAAL, faced significant headwinds with service revenue declining by 5.0% in FY25. The German operation’s Adjusted EBITDAAL fell from €5.0 billion to €4.4 billion, impacted by the MDU (Multi Dwelling Units) transition, incremental commercial investments, and challenging mobile market conditions. Despite these challenges, Vodafone reported operational improvements in Germany, including the lowest ever detractor scores and best ever NPS.

The following chart details Germany’s performance and turnaround efforts:

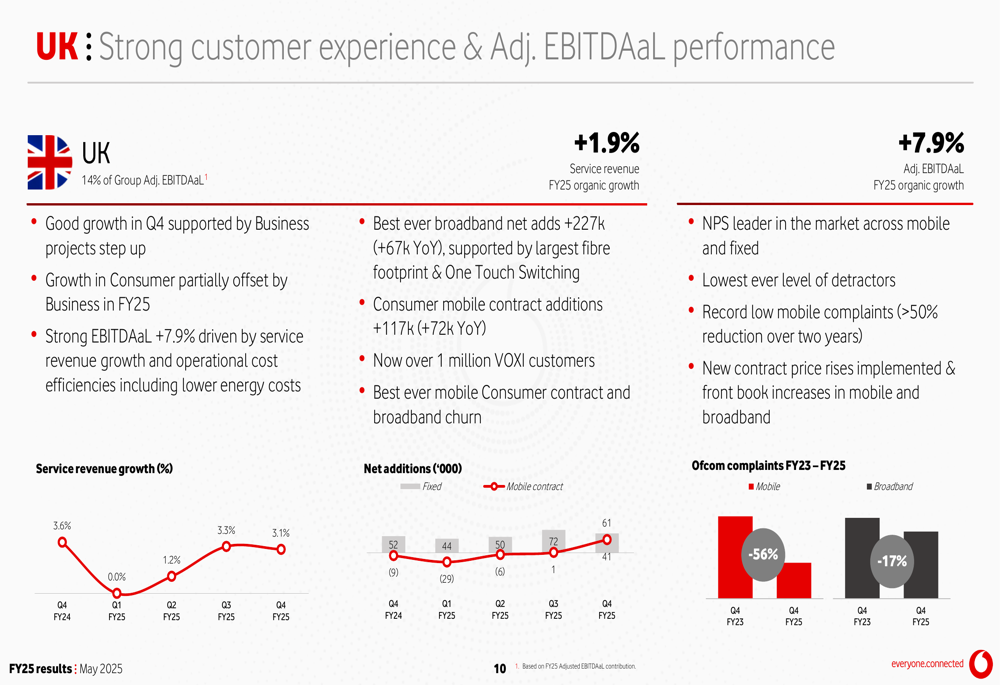

In contrast, the UK delivered strong results with 1.9% service revenue growth and impressive 7.9% Adjusted EBITDAAL growth. Customer experience improvements have led to significant decreases in Ofcom complaints, with mobile complaints down 56% and broadband complaints down 17% from FY23 to FY25.

As shown in the UK performance metrics:

Türkiye emerged as a standout performer with extraordinary 83.4% service revenue growth, while Egypt delivered 45.2% service revenue growth and 71.8% Adjusted EBITDAAL growth. Other European markets contributed 2.1% service revenue growth.

Digital Services & Business Performance

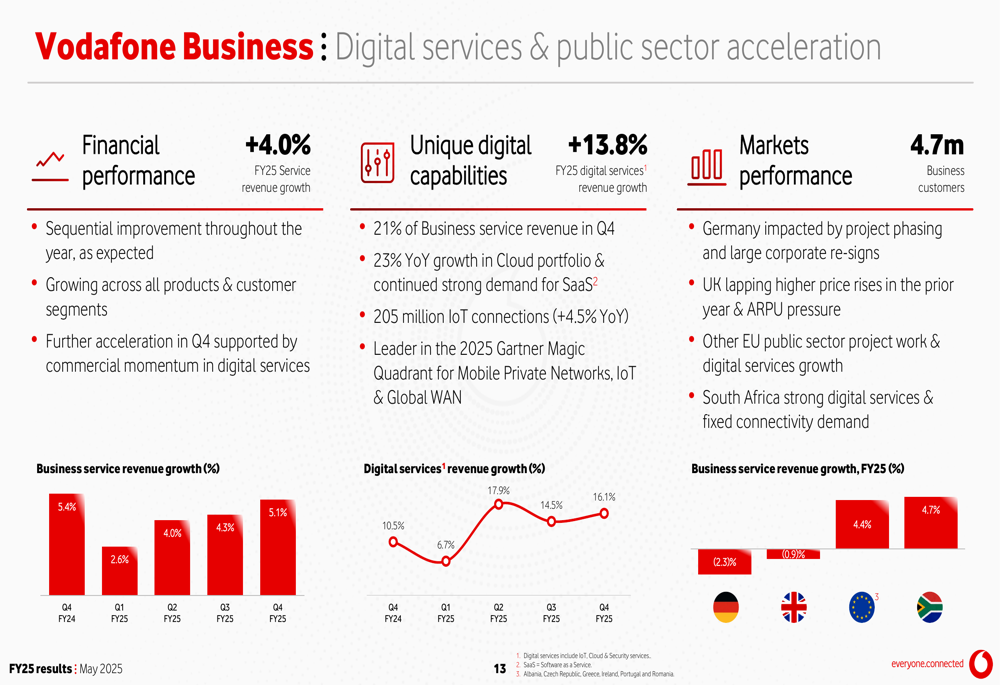

Vodafone Business delivered 4.0% growth in FY25, with digital services accelerating at 13.8%. These digital capabilities now represent 21% of Business service revenue in Q4, driven by 23% year-over-year growth in the Cloud portfolio and continued strong demand for Software (ETR:SOWGn) as a Service (SaaS).

The following chart illustrates Vodafone Business performance:

The company also reported strong growth in IoT connections, reaching 205 million connections, a 4.5% increase year-over-year. Financial services have shown robust growth, particularly through Vodacom, which now serves 88 million customers (25% growth) and processes US$1.2 billion in transactions daily.

Financial Analysis

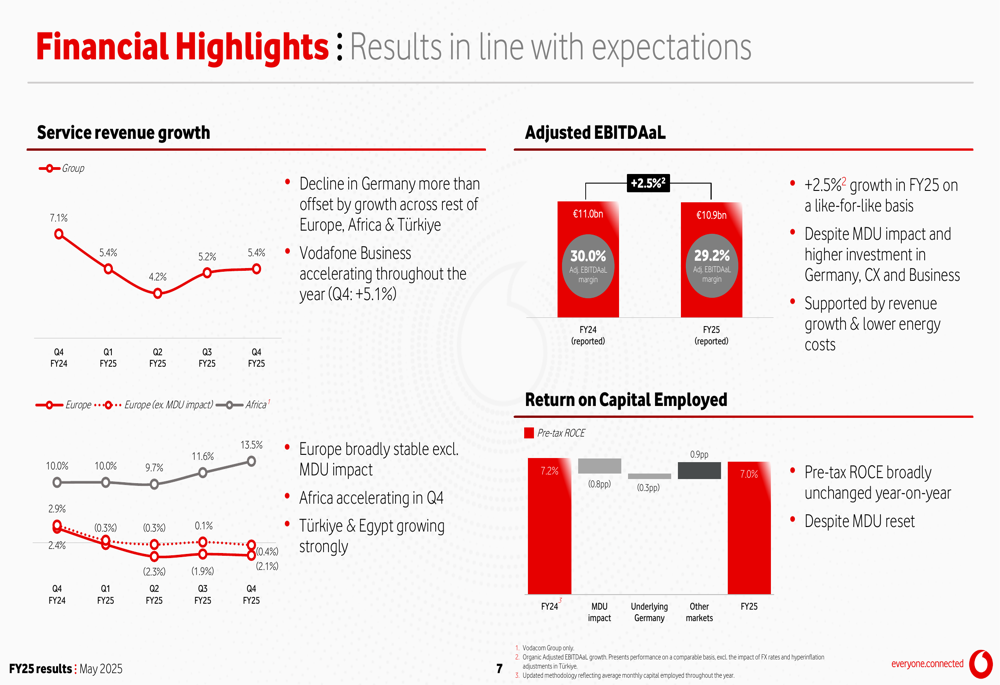

Vodafone’s service revenue growth has been consistent throughout FY25, with quarterly growth rates of 5.4% in Q1 and Q2, 5.2% in Q3, and 4.2% in Q4. The company achieved 2.5% growth in Adjusted EBITDAaL to €11.0 billion, with the margin improving to 30.0% from 29.2% in FY24.

The following chart shows the quarterly service revenue growth trends:

Pre-tax Return on Capital Employed (ROCE) declined slightly to 7.0% from 7.2% in FY24, primarily due to the MDU impact in Germany. Free cash flow remained strong at €2.5 billion, enabling Vodafone to pay a total ordinary dividend of 4.5 cents per share for FY25.

Forward-Looking Statements

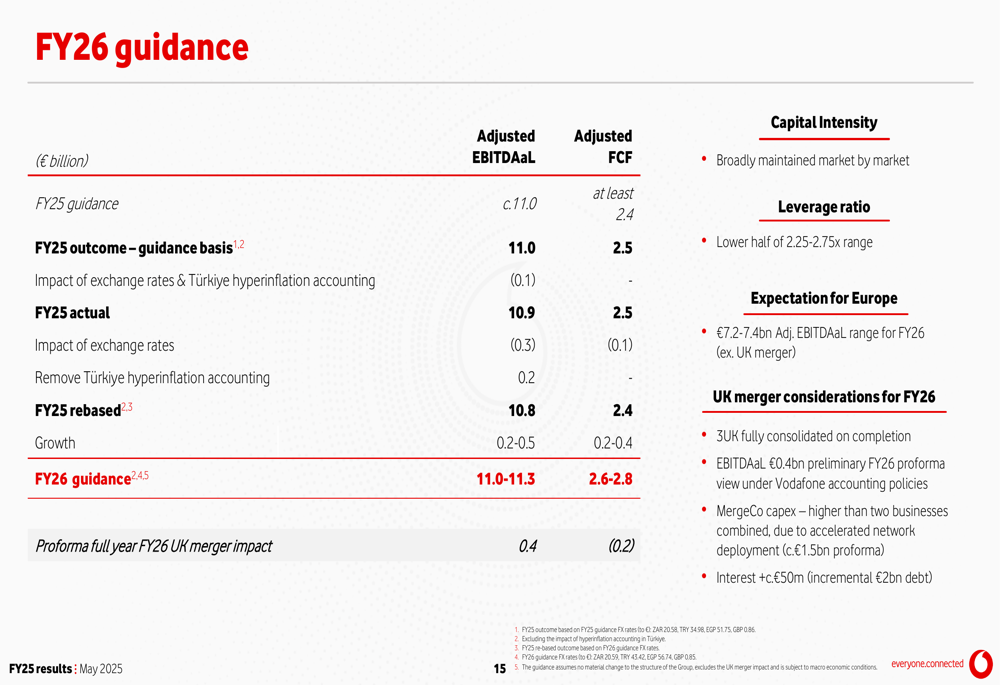

Looking ahead to FY26, Vodafone has provided guidance for Adjusted EBITDAAL of €11.0-11.3 billion and Adjusted Free Cash Flow of €2.6-2.8 billion, indicating confidence in continued growth. For Europe specifically, the company expects Adjusted EBITDAAL in the range of €7.2-7.4 billion for FY26.

The following slide details Vodafone’s FY26 guidance:

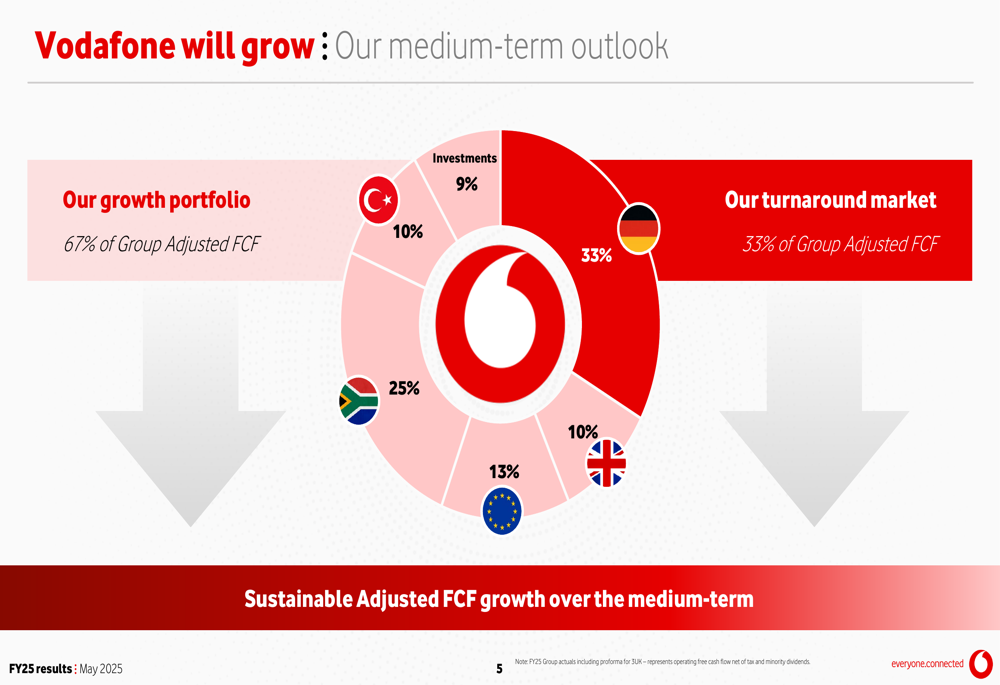

Vodafone’s medium-term outlook focuses on sustainable Adjusted Free Cash Flow growth, with its growth portfolio (South Africa, Türkiye, Other EU, and Vodafone Investments) expected to drive this performance while the company continues its turnaround efforts in Germany.

As shown in the following breakdown of Vodafone’s growth markets:

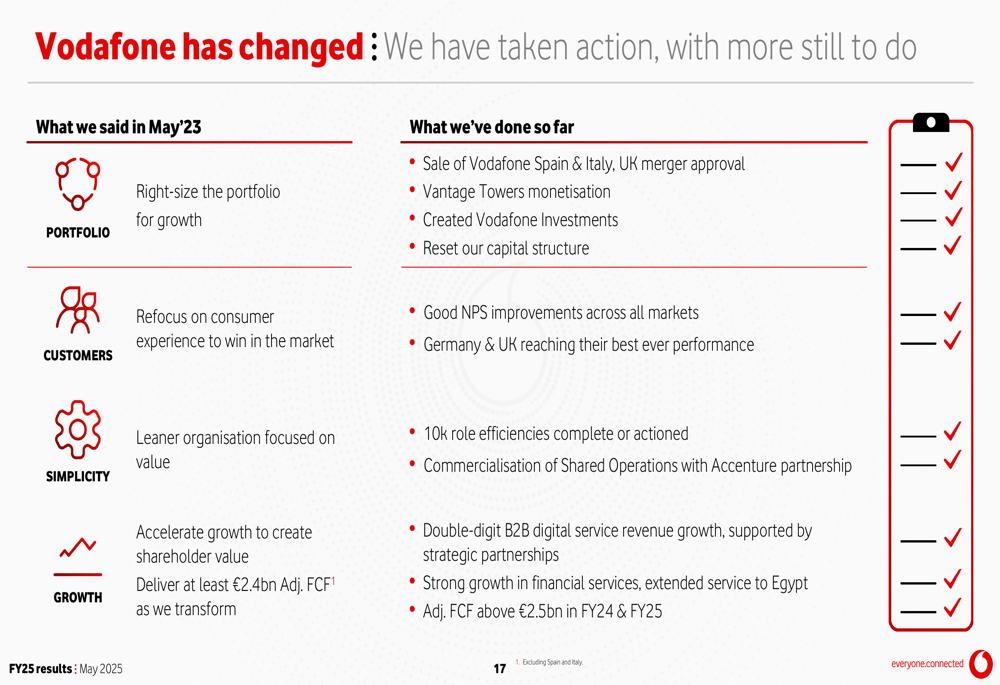

Strategic Initiatives

Vodafone has made significant progress on its transformation strategy announced in May 2023. The company has completed or actioned 10,000 role efficiencies as part of its simplification efforts and commercialized its Shared Operations through a partnership with Accenture (NYSE:ACN).

Customer experience has been a key focus, with approximately €300 million of incremental investment over the last two years resulting in a more than 20% reduction in detractors across the customer base (5 million fewer detractors) and the lowest ever deep detractors score across Europe.

Vodafone’s transformation strategy centers on four key pillars: portfolio optimization, customer experience, simplification, and growth acceleration. The company has made progress across all these areas, as illustrated in the following summary:

Conclusion

Vodafone’s FY25 results demonstrate that the company is delivering on its financial targets while executing a significant transformation of its business. The portfolio restructuring has positioned Vodafone to focus on markets where it can achieve sustainable growth, while operational improvements are addressing challenges in key markets like Germany.

With a stronger balance sheet, improved customer satisfaction, and growing digital services, Vodafone appears well-positioned to deliver on its FY26 guidance and medium-term growth objectives. However, the company still faces significant challenges in Germany, which remains a substantial portion of its business and will require continued turnaround efforts.

As Vodafone moves into FY26, investors will be watching closely to see if the company can maintain its momentum in growth markets while successfully executing its turnaround strategy in Germany.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.