Joby Aviation closes $591 million stock offering with full underwriter option

Introduction & Market Context

Swedish industrial group Volati AB (STO:VOLO) presented its Q1 2025 interim report on April 28, showing strong growth across key metrics despite lingering market uncertainties. The company’s stock responded positively, rising 2.63% following the presentation.

CEO Andreas Stenbäck and CFO Martin Aronsson outlined how the company has positioned itself for accelerated growth as market conditions gradually improve, with particular emphasis on strategic acquisitions and organic growth returning across most business segments.

"Volati is in a great position to show accelerated growth once markets normalise," the company stated in its presentation, highlighting its ongoing acquisition strategy and operational improvements.

Quarterly Performance Highlights

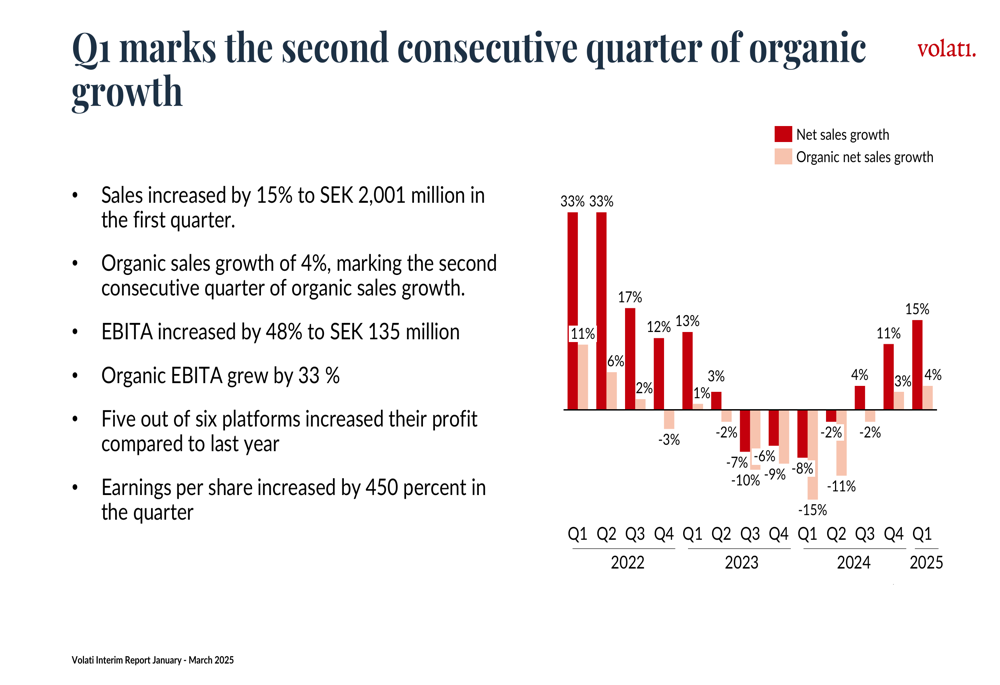

Volati reported impressive financial results for Q1 2025, with sales increasing 15% to SEK 2,001 million compared to SEK 1,747 million in Q1 2024. Notably, organic sales growth reached 4%, while EBITA surged 48% to SEK 135 million. The company also reported that earnings per share increased by an extraordinary 450% year-over-year.

Five out of six platforms increased their profit compared to the same period last year, demonstrating broad-based improvement across the organization.

As shown in the following chart of quarterly sales and organic growth trends:

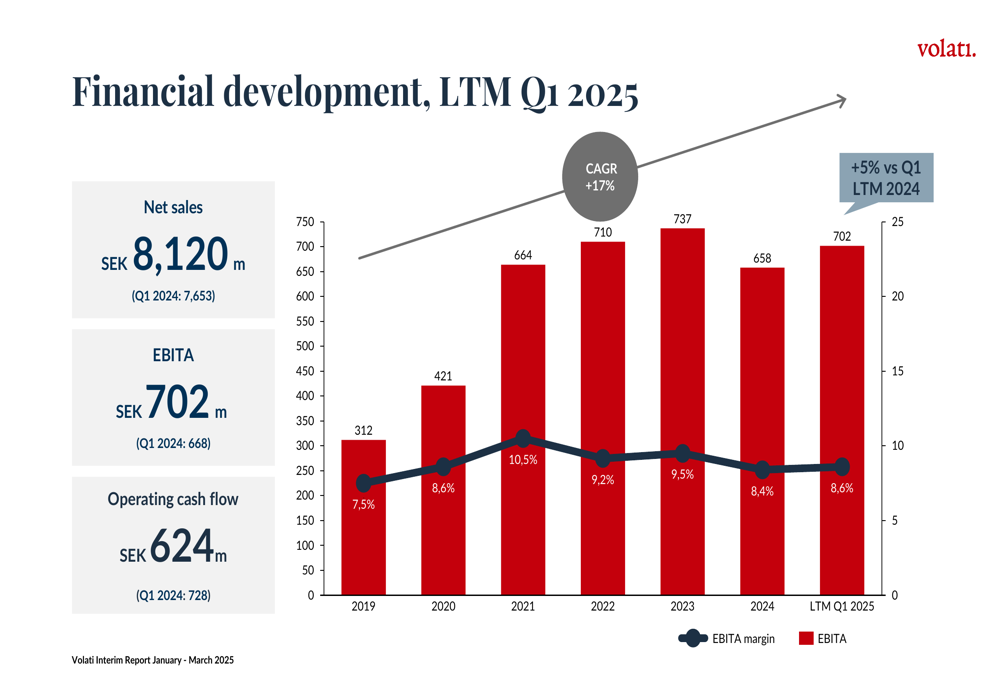

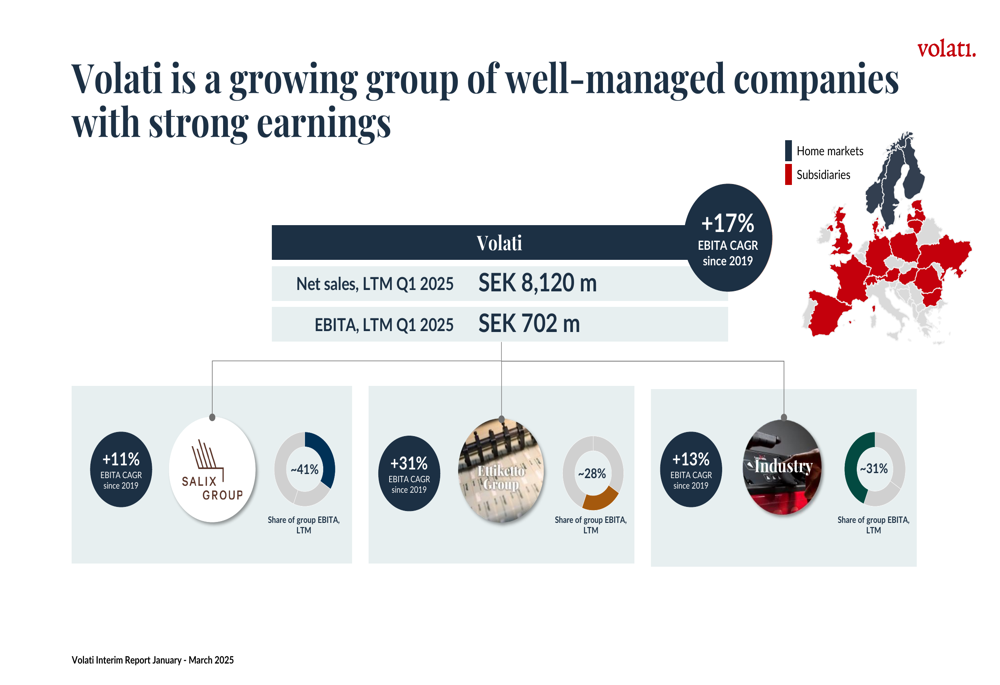

The company’s long-term performance remains strong, with EBITA showing a compound annual growth rate (CAGR) of 17% since 2019. For the last twelve months ending Q1 2025, Volati achieved net sales of SEK 8,120 million and EBITA of SEK 702 million.

The financial development over time illustrates the company’s consistent growth trajectory:

Business Segment Performance

Volati operates through three main business segments: Salix Group, Ettiketto Group, and Industry. Each segment showed distinct performance patterns in Q1 2025.

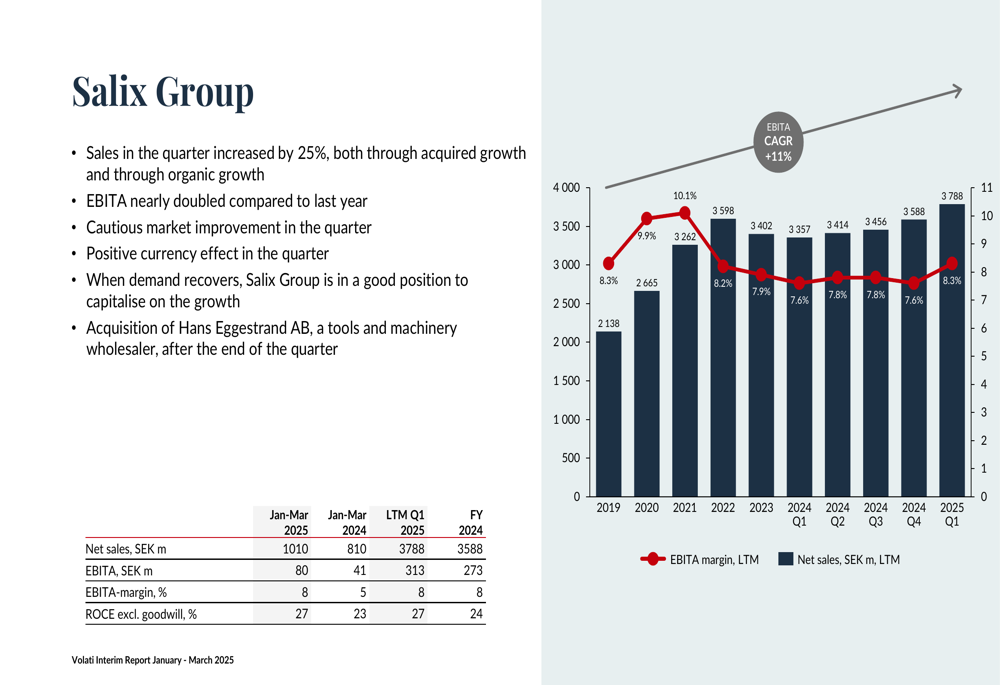

Salix Group, which offers products and materials for builder’s hardware, construction, and home & garden, delivered exceptional results with sales increasing by 25% to SEK 1,010 million. Even more impressive, the segment’s EBITA nearly doubled to SEK 80 million, representing an 8% margin. The company noted cautious market improvement and positive currency effects contributing to this performance.

The following chart illustrates Salix Group’s performance trends:

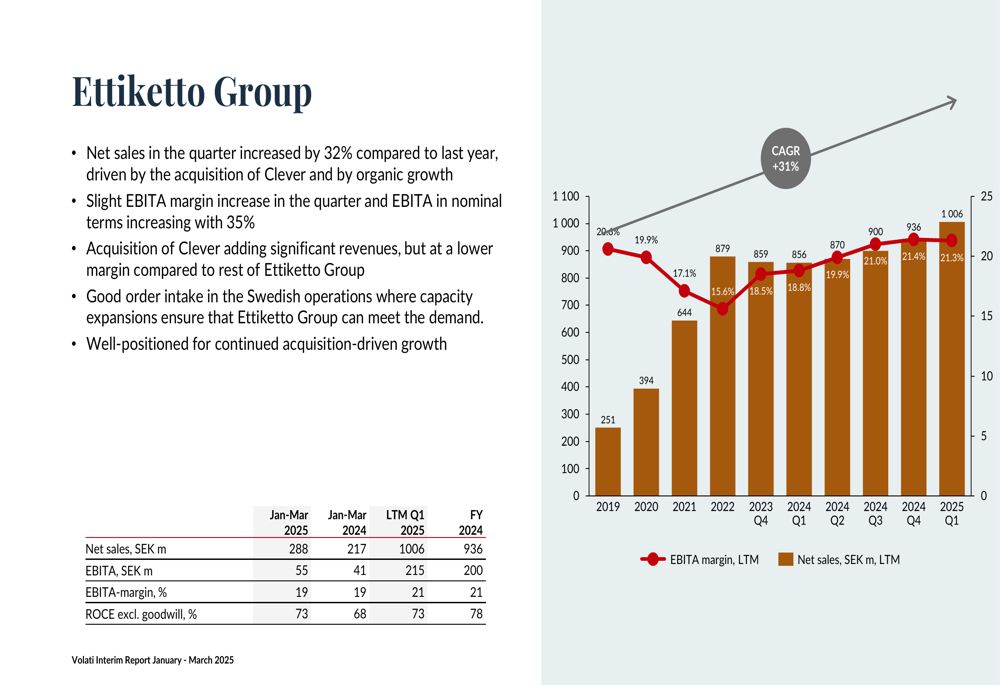

Ettiketto Group, specializing in self-adhesive labels and machines, also performed strongly with sales increasing by 32% to SEK 288 million in Q1 2025. EBITA rose to SEK 55 million, maintaining a robust 19% margin. This segment has demonstrated remarkable growth with a 31% EBITA CAGR since 2019.

The Ettiketto Group’s financial performance is visualized here:

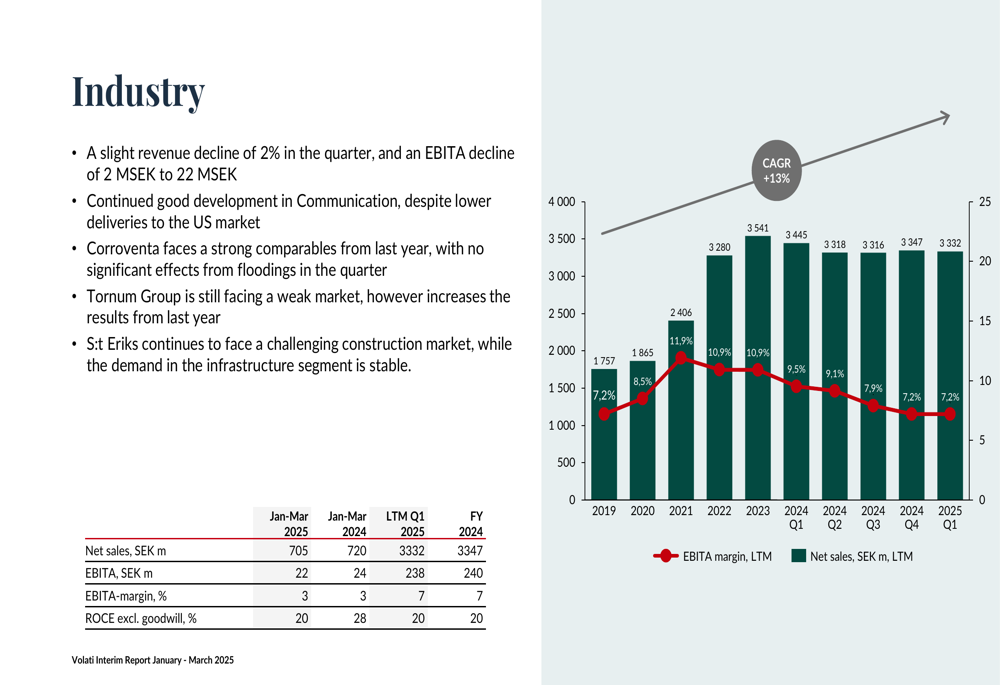

The Industry segment, which encompasses four businesses with leading market positions in their niches, experienced a slight revenue decline of 2% to SEK 705 million and an EBITA decline of SEK 2 million to SEK 22 million in Q1 2025. The company attributed this to challenging comparables and market conditions, particularly in the Communication division.

Acquisition Strategy

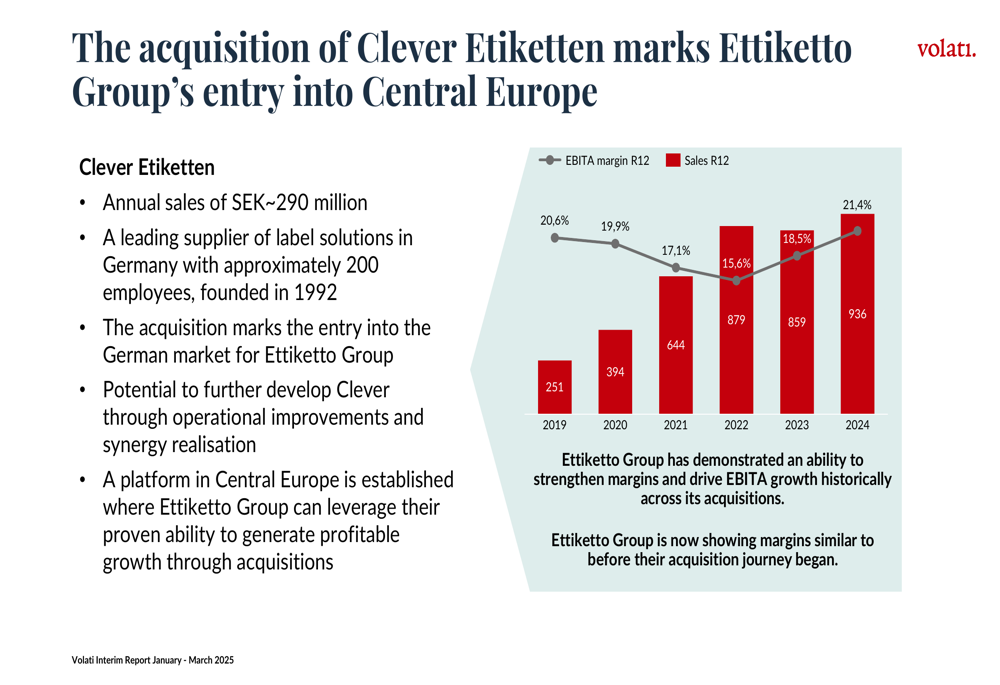

Acquisitions remain a cornerstone of Volati’s growth strategy. The company has completed 27 acquisitions since 2020, adding SEK 4.2 billion in annual sales. In Q1 2025 alone, Volati acquired Clever Etiketten and Eggestrand, adding SEK 330 million in annual revenue.

The acquisition of Clever Etiketten represents a strategic entry into Central Europe, providing Ettiketto Group with access to the German market. Clever Etiketten generates annual sales of approximately SEK 290 million and is a leading supplier of label solutions in Germany.

As illustrated in the following strategic acquisition overview:

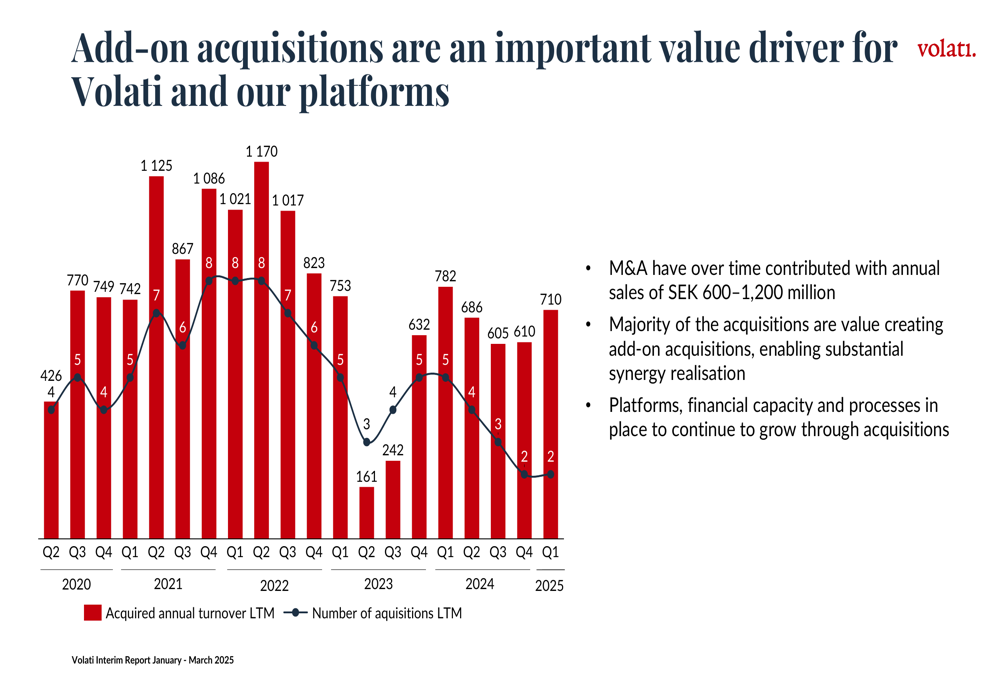

Volati has maintained a consistent acquisition pace, with 16 companies acquired since 2022 totaling SEK 2.4 billion in yearly revenue. The company emphasized that most acquisitions are value-creating, enabling synergy realization.

The chart below shows the value derived from acquisitions over time:

Financial Position and Outlook

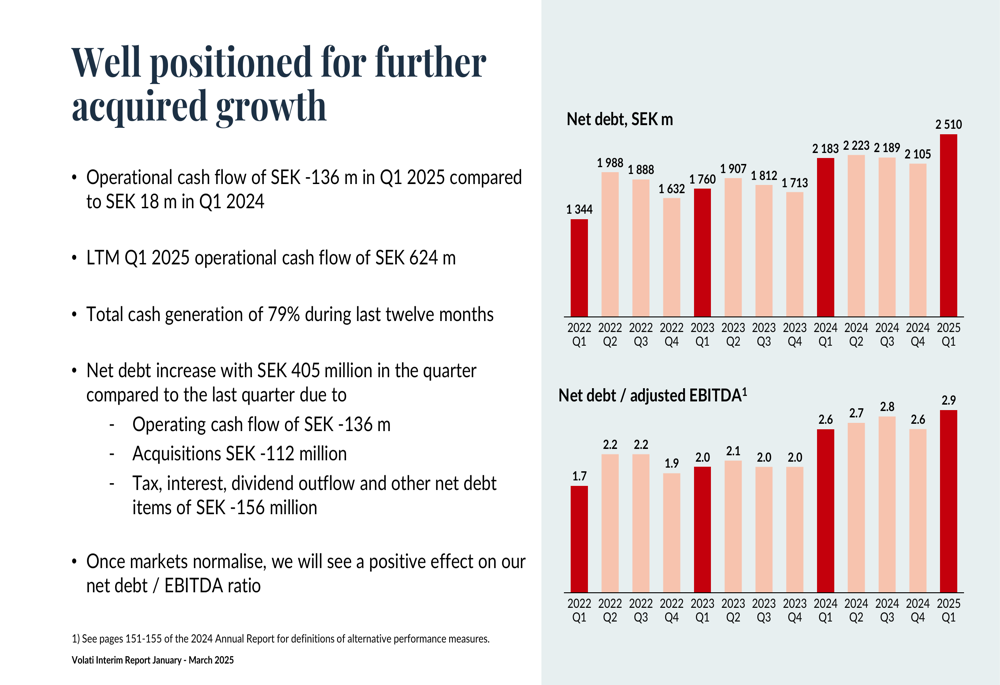

Despite strong operational performance, Volati’s financial position shows some mixed signals. Operating cash flow turned negative at SEK -136 million in Q1 2025, compared to positive SEK 18 million in Q1 2024. However, the last twelve months’ operating cash flow remained strong at SEK 624 million, though down from SEK 728 million in the prior period.

The company’s leverage increased slightly, with net debt/adjusted EBITDA ratio rising to 2.9x from 2.6x in Q1 2024, though still within the target range of 2-3x. This increase reflects the company’s continued investment in acquisitions.

The following chart shows the development of Volati’s net debt position:

Looking ahead, Volati has expanded its credit facilities with Nordea and SEB to support future growth. The company maintains its financial goal of increasing EBITA by 15% annually, though the current LTM growth in EBITA per ordinary share stands at 5%, up from -13% in Q1 2024.

Volati’s management expressed confidence in the company’s positioning for future growth, noting that market conditions are slowly improving and that trade tariff concerns are expected to have limited direct impact on operations. The company believes it is well-positioned to accelerate growth once markets fully normalize, with platforms in place for acquisitive growth in the latter half of the year.

With a return on adjusted equity of 17% against a long-term target of 20%, Volati continues to demonstrate strong operational efficiency while pursuing its ambitious growth strategy through both organic initiatives and strategic acquisitions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.