Joby Aviation closes $591 million stock offering with full underwriter option

Introduction & Market Context

Voyager Technologies Inc (NYSE:VOYG) presented its second quarter 2025 earnings results on August 5, highlighting strong revenue growth despite ongoing profitability challenges. The company’s stock has experienced significant volatility following the earnings release, currently trading at $34.99, down 1.19% and hovering near its 52-week low of $32.35 – far below its 52-week high of $73.95.

The space and defense technology company, which completed its IPO earlier this year, is positioning itself at the intersection of defense, national security, and commercial space markets. While revenue growth remains robust, investors appear concerned about the company’s path to profitability, as reflected in the stock’s recent performance.

Quarterly Performance Highlights

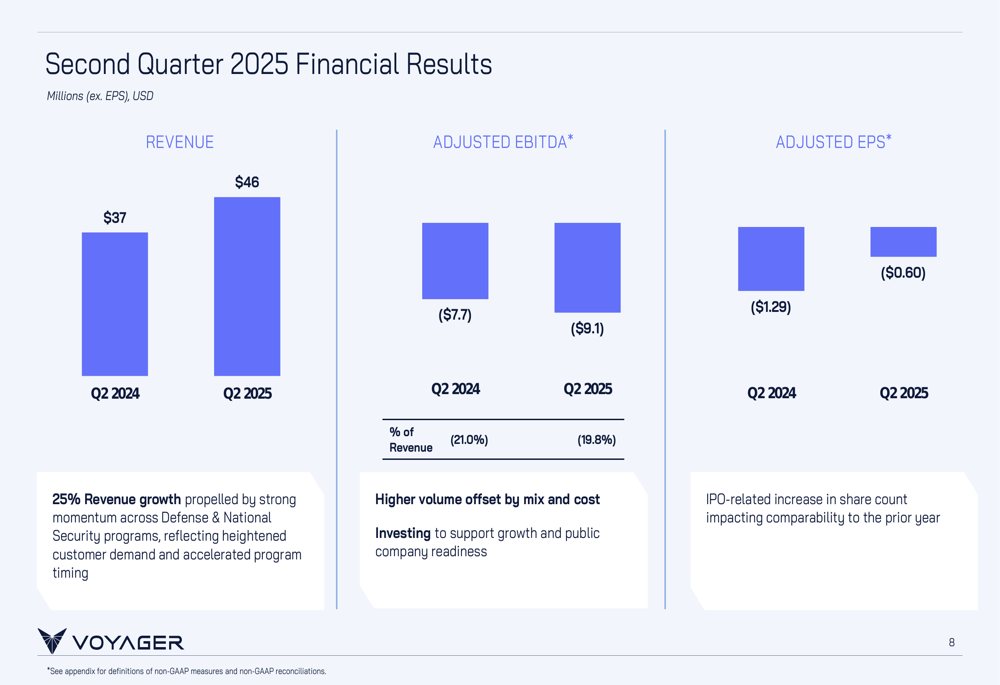

Voyager reported Q2 2025 revenue of $46 million, representing a 25% year-over-year increase from $37 million in Q2 2024. Despite this growth, the company posted an adjusted EBITDA loss of $9.1 million, compared to a loss of $7.7 million in the same period last year. Adjusted earnings per share showed improvement at -$0.60, up from -$1.29 in Q2 2024.

The company’s presentation highlighted these key financial metrics, showing the mixed results of strong top-line growth against continued operational losses:

Voyager completed its IPO during the quarter, issuing 14.2 million shares at $31 per share and raising $440 million before fees. The company also established a $200 million revolving credit facility, significantly strengthening its financial position. Additionally, Voyager completed strategic acquisitions of LEOcloud and Optical Physics Company to enhance its technological capabilities.

Segment Performance Analysis

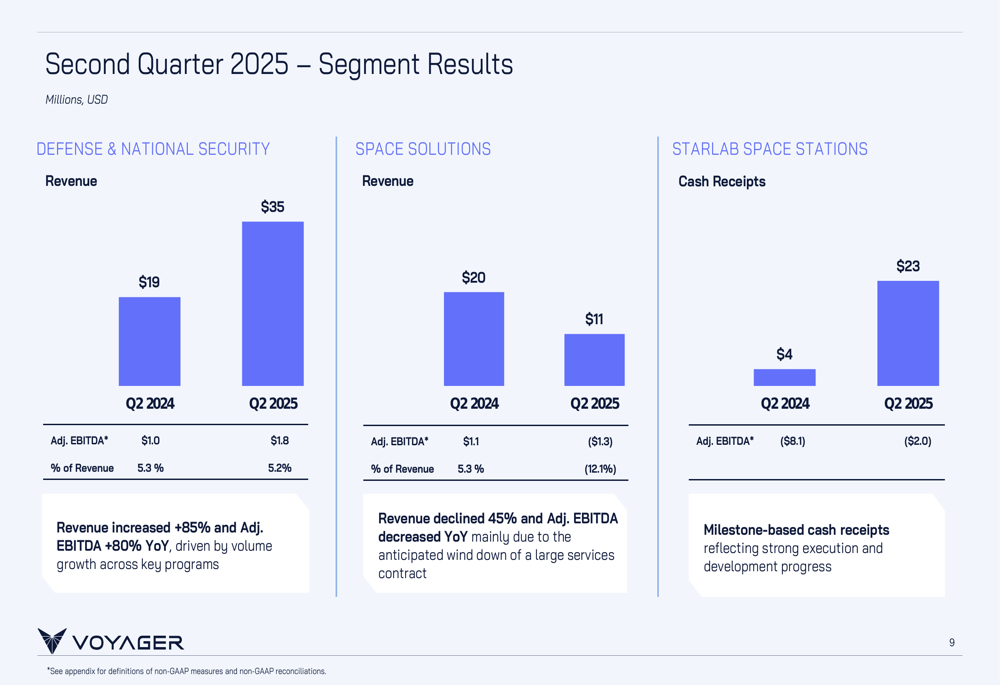

Voyager’s performance varied significantly across its three business segments. The Defense & National Security segment was the standout performer, with revenue surging 85% year-over-year from $19 million to $35 million. This segment also improved its adjusted EBITDA from $1.0 million to $1.8 million.

In contrast, the Space Solutions segment experienced a decline, with revenue dropping from $20 million to $11 million and adjusted EBITDA falling from $1.1 million to -$1.3 million. The Starlab Space Stations segment showed progress with cash receipts increasing substantially from $4 million to $23 million, while its adjusted EBITDA loss narrowed from -$8.1 million to -$2.0 million.

The following chart from the presentation illustrates these segment results:

Strategic Initiatives & Acquisitions

Voyager outlined three strategic priorities in its presentation: high growth platform, rapid innovation, and Starlab development. The company is targeting organic growth exceeding 25% CAGR with additional upside from mergers and acquisitions.

A key strategic development highlighted in the presentation was the successful Critical Design Review for the Next (LON:NXT) Generation Interceptor (NGI), described as a national priority designed to counter emerging ballistic and hypersonic threats. Voyager is delivering the NGI Second Stage Roll Control System, which represents a multi-year, $1 billion+ revenue opportunity for the company.

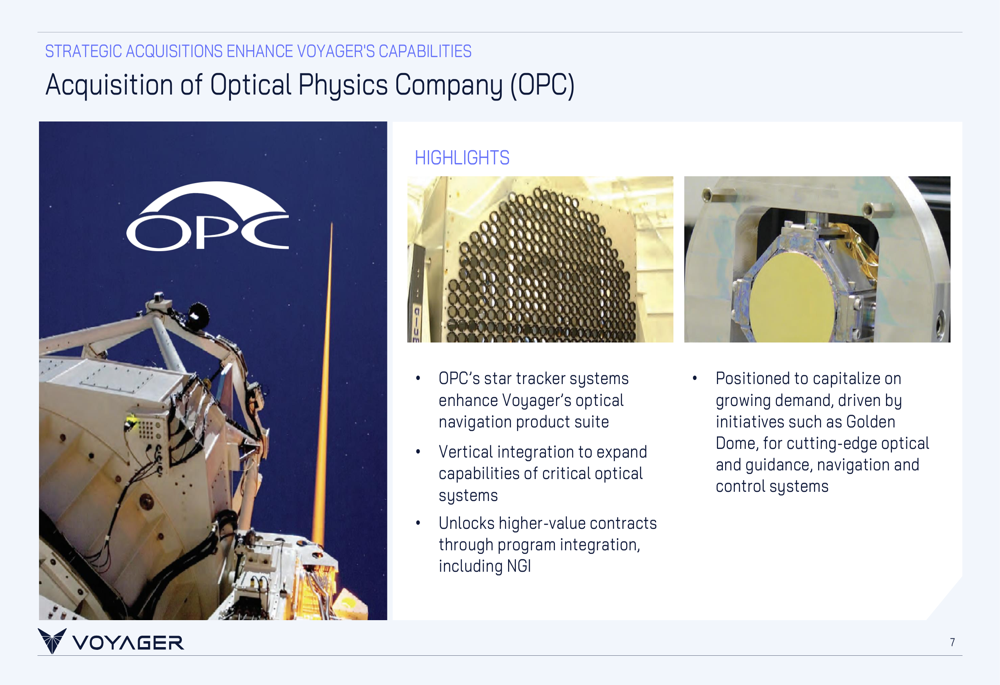

The acquisition of Optical Physics Company (OPC) was another strategic move detailed in the presentation. This acquisition enhances Voyager’s optical navigation capabilities, enables vertical integration of critical optical systems, and positions the company to capitalize on growing demand for cutting-edge optical and guidance, navigation, and control systems.

Balance Sheet & Financial Position

Voyager emphasized its strong financial position, describing it as a "Fortress Balance Sheet" that supports both organic investments and accretive M&A opportunities. As of June 30, 2025, the company reported $469 million in cash, zero debt, and an undrawn credit facility of $200 million, providing total liquidity of $669 million.

The company’s financial strength is particularly notable given its capital-light business model. However, investors appear concerned about the widening operational losses despite the strong cash position, as reflected in the stock’s performance following the earnings release.

Forward Guidance & Outlook

For the full year 2025, Voyager maintained its revenue guidance of $165-170 million and adjusted EBITDA guidance of -$63 to -$60 million. The company expects sequential growth of approximately 9% in the second half of 2025, with revenue reaching about $87 million. Gross profit and adjusted EBITDA margins are projected to be modestly higher in the second half compared to the first half of 2025, with the fourth quarter outperforming the third quarter.

The company’s backlog of $170 million as of June 30, 2025, provides visibility into the second half of the year. Voyager’s presentation emphasized its positioning to capitalize on industry tailwinds, highlighting its role as a leading provider of mission-critical solutions with high innovation spend (18% of revenue) and flexible multi-use technology solutions.

Despite the optimistic outlook presented by management, the market reaction suggests investors remain cautious about Voyager’s ability to translate its strategic positioning and revenue growth into sustainable profitability. The company’s focus on high-growth markets and strategic acquisitions will need to demonstrate a clearer path to positive earnings to regain investor confidence in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.