Navitas stock soars as company advances 800V tech for NVIDIA AI platforms

Introduction & Market Context

Wabash National Corporation (NYSE:WNC) reported its second quarter 2025 earnings on July 25, revealing continued challenges in the transportation equipment sector. The company posted a GAAP loss per share of $(0.23) and a non-GAAP adjusted loss of $(0.15) per share. Following the release, Wabash shares fell 5.25% in after-hours trading, extending a difficult year that has seen the stock decline over 56% in the past twelve months.

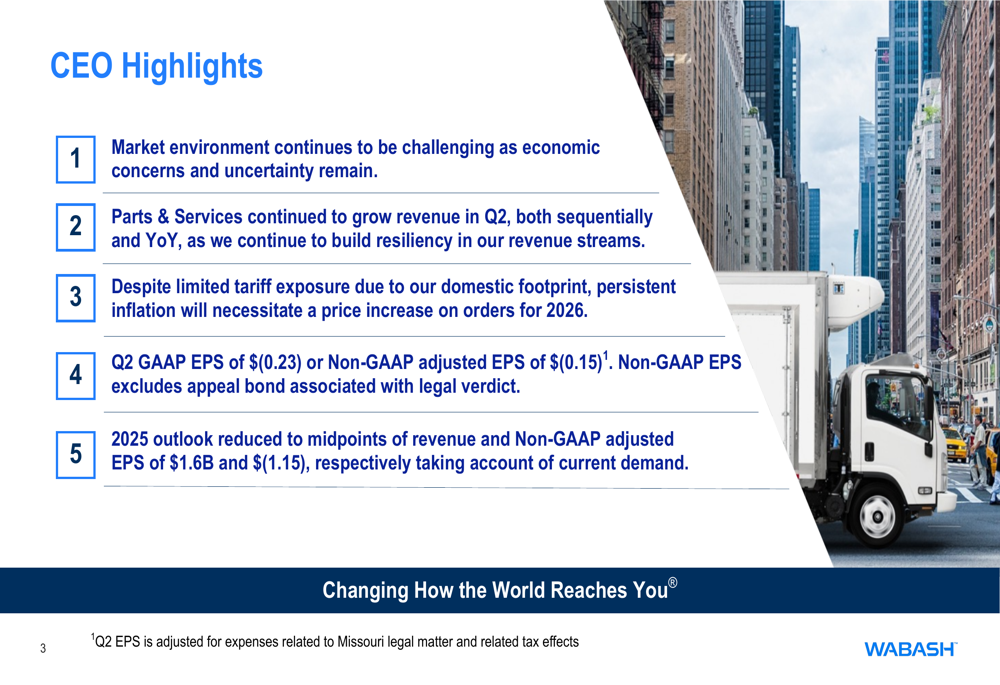

The earnings presentation highlighted persistent headwinds facing the company, with CEO commentary noting "the market environment remains challenging due to economic concerns and uncertainty." This follows a disappointing first quarter where Wabash missed earnings expectations by a significant margin, posting an EPS of $(0.58) against forecasts of $(0.26).

Quarterly Performance Highlights

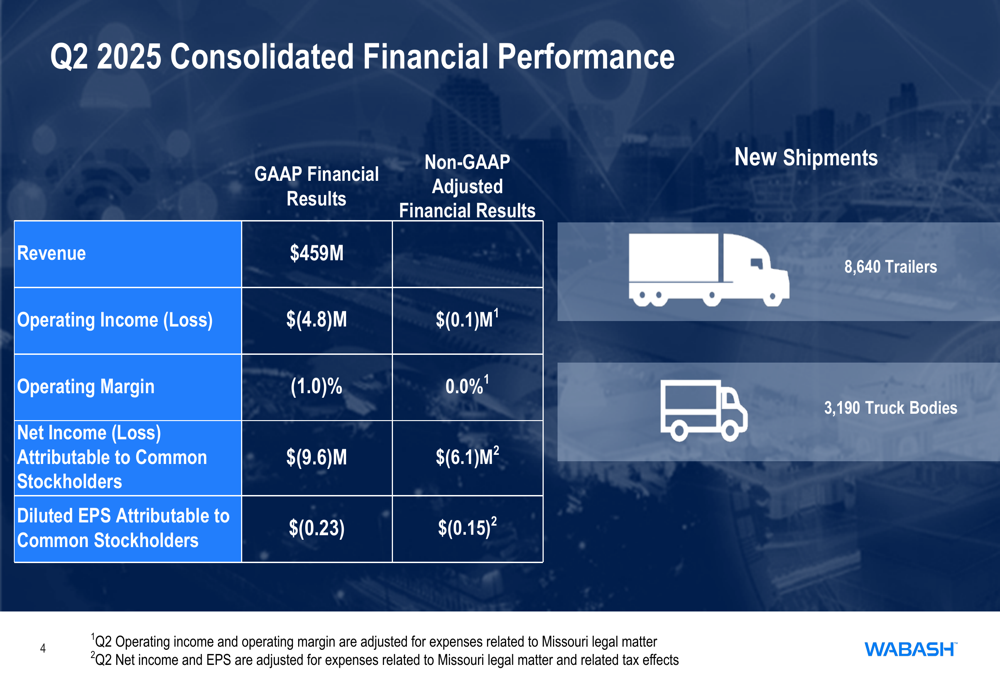

Wabash reported Q2 2025 revenue of $459 million, with an operating loss of $(4.8) million on a GAAP basis and $(0.1) million on an adjusted basis. The company shipped 8,640 trailers and 3,190 truck bodies during the quarter.

The adjusted figures exclude expenses related to a Missouri legal matter, which the company noted in its reconciliation statements. Net loss attributable to common stockholders was $(9.6) million on a GAAP basis and $(6.1) million on an adjusted basis.

Despite the challenging environment, management emphasized its focus on building revenue stream resiliency, particularly through the Parts & Services segment, which showed growth both sequentially and year-over-year. The company also noted that persistent inflation has necessitated price increases for 2026 orders, though it highlighted limited tariff exposure.

Segment Performance Analysis

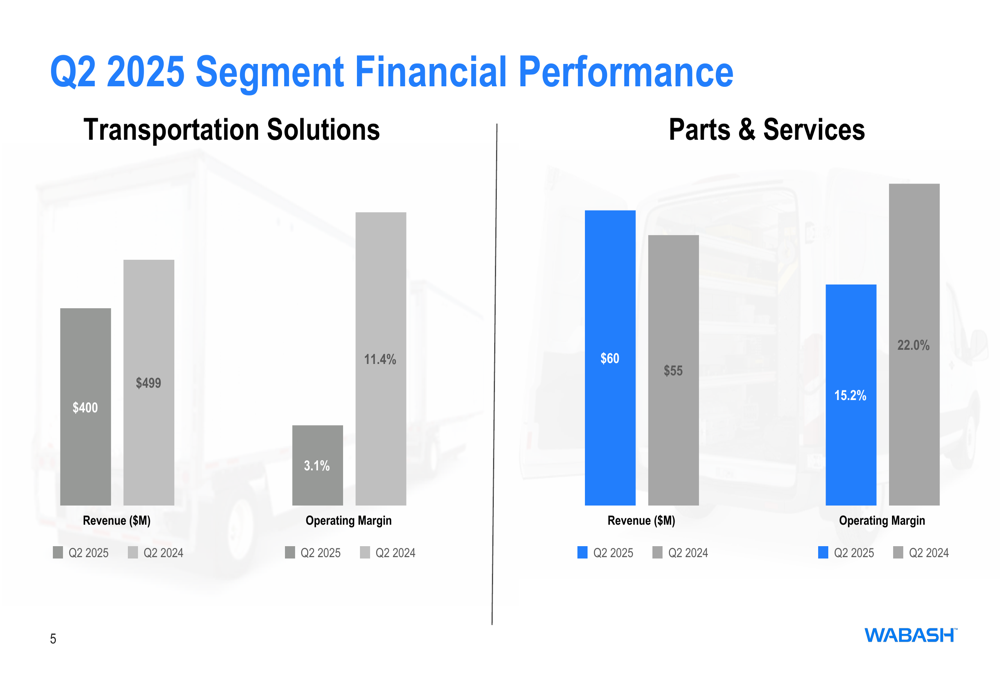

Wabash’s business is divided into two primary segments: Transportation Solutions and Parts & Services. The Transportation Solutions segment, which represents the bulk of the company’s revenue, saw a significant year-over-year decline, with Q2 2025 revenue of $400 million compared to $499 million in Q2 2024. More concerning was the dramatic drop in operating margin for this segment, falling to 3.1% from 11.4% in the prior year period.

The Parts & Services segment offered a bright spot, with revenue increasing to $60 million from $55 million in Q2 2024. However, even this growth segment experienced margin pressure, with operating margin declining to 15.2% from 22.0% in the prior year. The company has been strategically focusing on building this segment to provide more stable revenue streams and reduce cyclicality in its business model.

This segment performance aligns with commentary from the Q1 earnings call, where executives emphasized the importance of "building parts and services capabilities that deliver for our customers regardless of what’s happening in the broader economy."

Cash Flow and Capital Allocation

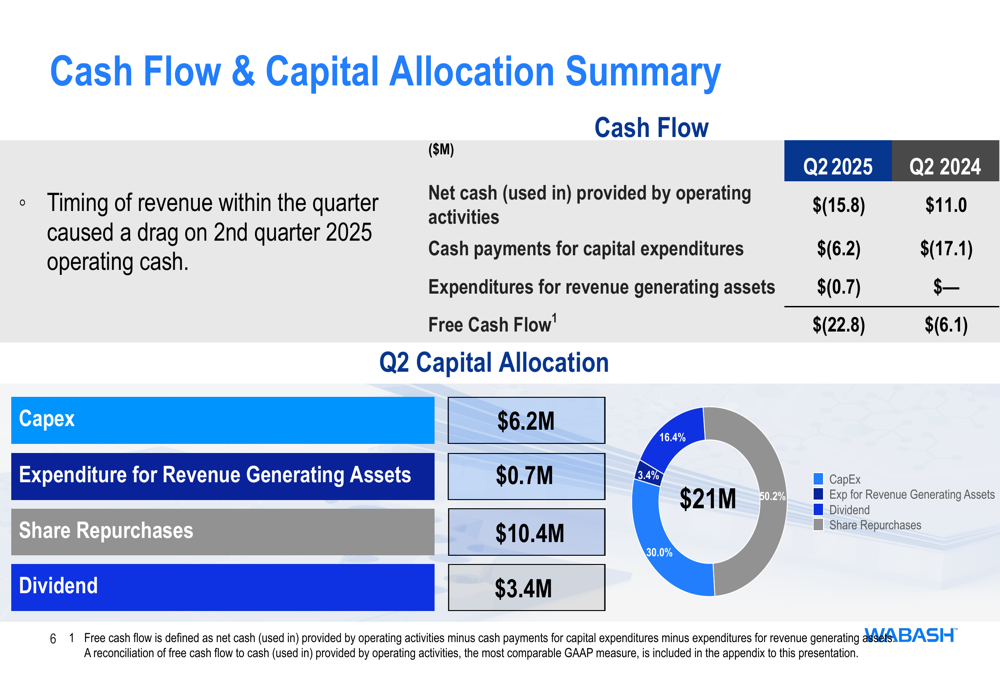

Wabash’s cash flow metrics showed deterioration compared to the prior year. The company reported negative operating cash flow of $(15.8) million in Q2 2025, compared to positive $11.0 million in Q2 2024. Free cash flow worsened to $(22.8) million from $(6.1) million in the prior year period.

Despite these challenges, Wabash maintained its capital allocation strategy, with $6.2 million allocated to capital expenditures (30% of total allocation), $10.4 million to share repurchases (50.2%), and $3.4 million to dividends (16.4%). The company also allocated $0.7 million to revenue generating assets (3.4%).

The continued share repurchases despite negative free cash flow suggests management’s confidence in the long-term value of the company, though this approach may face scrutiny given the challenging operating environment and declining financial performance.

Revised 2025 Outlook

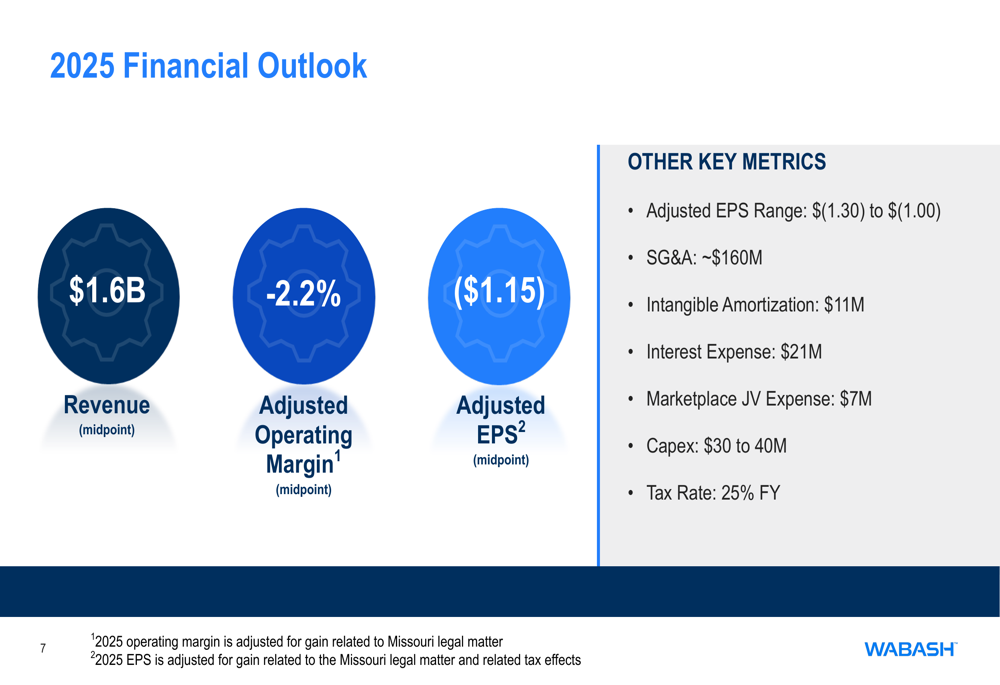

In perhaps the most significant development from the presentation, Wabash substantially reduced its full-year 2025 guidance. The company now expects revenue of approximately $1.6 billion, down from the previous guidance of $1.8 billion provided during the Q1 earnings report. Similarly, the adjusted EPS outlook has been lowered to $(1.15), compared to the previous range of $(0.85) to $(0.35).

Additional guidance metrics include:

- Adjusted operating margin of approximately -2.2%

- SG&A expenses of approximately $160 million

- Interest expense of $21 million

- Capital expenditures between $30-40 million

- Tax rate of 25% for the full year

This revised outlook represents a significant deterioration from the company’s previous expectations and suggests that management anticipates continued challenges throughout the remainder of 2025.

Market Reaction and Conclusion

The market responded negatively to Wabash’s Q2 results and reduced guidance, with shares falling 5.25% in after-hours trading to $10.10, following a 6.47% decline during the regular trading session. The stock is now trading near its 52-week low of $6.78, reflecting investor concerns about the company’s near-term prospects.

While Wabash continues to face significant headwinds in its core Transportation Solutions segment, the growth in the Parts & Services business provides some optimism for the company’s strategic direction. Management’s focus on building this more resilient revenue stream could help stabilize performance over time, though the immediate outlook remains challenging.

As CFO Pat Kesselin noted during the Q1 earnings call, "While 2025 is shaping up to be a more difficult year than anyone assumed, we’ve been through cycle troughs before." Investors will be watching closely to see if the company’s strategic initiatives can help weather the current downturn and position Wabash for recovery when market conditions improve.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.