Futures slip, bank earnings ahead, Powell to speak - what’s moving markets

Wabash National Corporation (NYSE:WNC) shares plunged over 13% in premarket trading after the company’s first quarter 2025 earnings presentation revealed significant operational challenges despite reporting a large GAAP profit due to a legal settlement. The transportation equipment manufacturer reduced its full-year outlook amid softening market conditions and tariff uncertainties.

Quarterly Performance Highlights

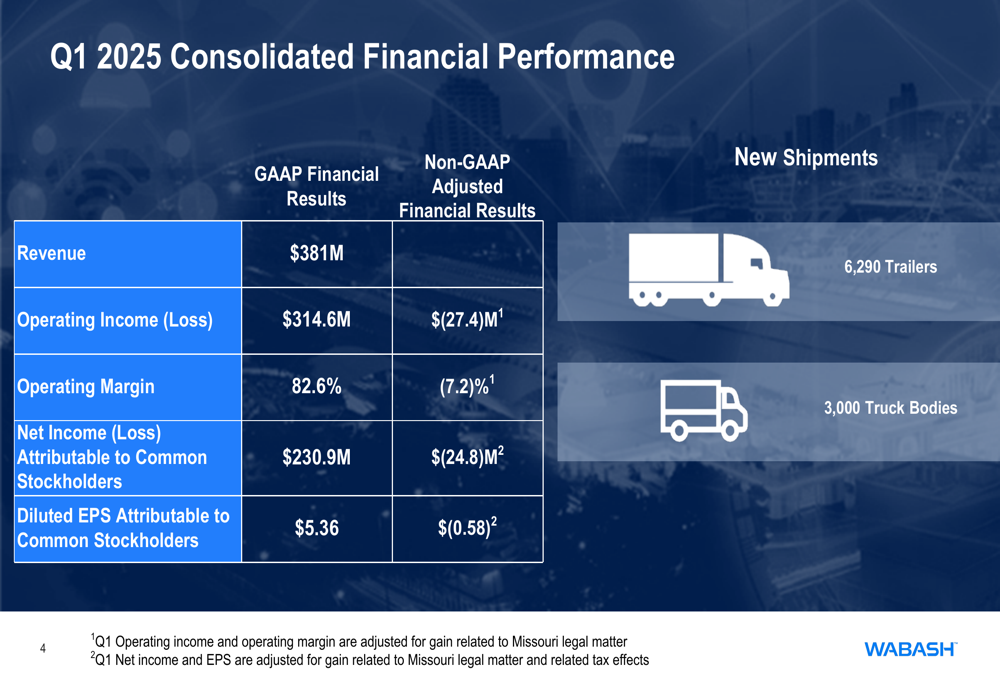

Wabash reported Q1 2025 revenue of $381 million, a substantial 26% decline from $515 million in the same period last year. While GAAP earnings per share reached $5.36, this figure was heavily influenced by a gain related to a legal settlement in Missouri. Excluding this one-time gain, the company posted a non-GAAP adjusted loss of $0.58 per share.

The company’s CEO highlighted that market conditions have softened as customers delay equipment purchasing decisions due to tariff uncertainty. Despite limited direct exposure to tariffs due to Wabash’s domestic manufacturing footprint, second-order effects on demand have proven more significant.

As shown in the following consolidated financial performance summary:

The stark contrast between GAAP and non-GAAP results underscores how the legal settlement masked underlying business challenges. Operationally, the company shipped 6,290 trailers and 3,000 truck bodies during the quarter, down from 8,500 trailers in Q1 2024.

Segment Performance Analysis

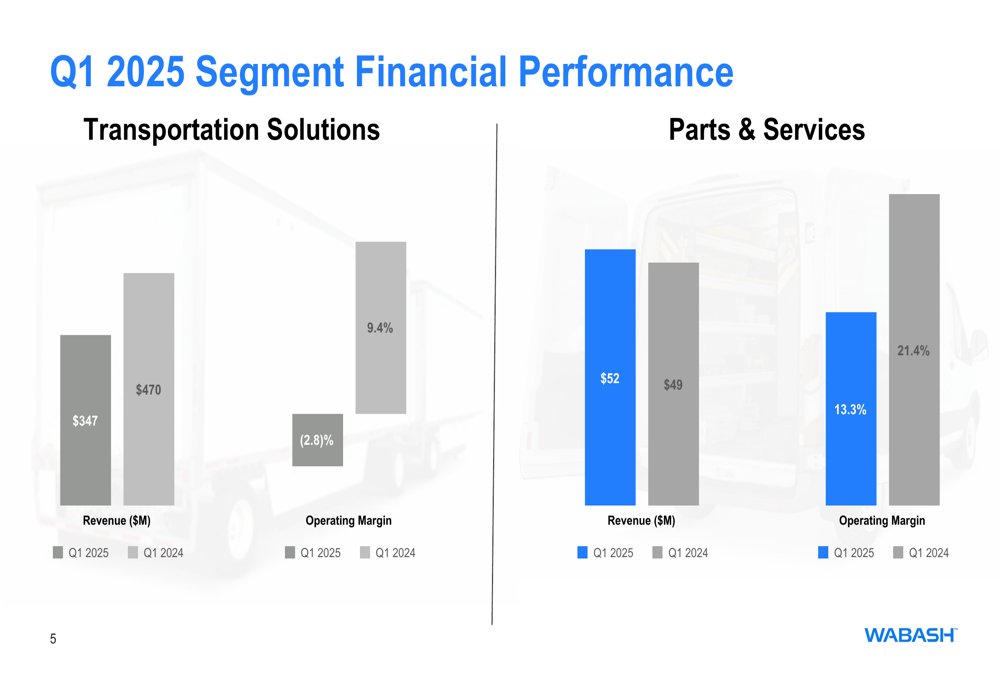

Wabash’s business segments showed divergent performance trends, with both facing margin pressure. The Transportation Solutions segment, which represents the bulk of the company’s revenue, saw particularly concerning results with revenue declining to $347 million from $470 million year-over-year. More troubling was the segment’s operating margin, which fell to -2.8% from a positive 9.4% in Q1 2024.

The Parts & Services segment showed more resilience with revenue increasing to $52 million from $49 million in Q1 2024, though operating margin contracted significantly to 13.3% from 21.4% a year earlier. Management noted that Parts & Services revenue continued to grow, with Upfit volumes doubling year-over-year and Transportation-as-a-Service (TaaS) expanding.

The segment breakdown illustrates these contrasting trends:

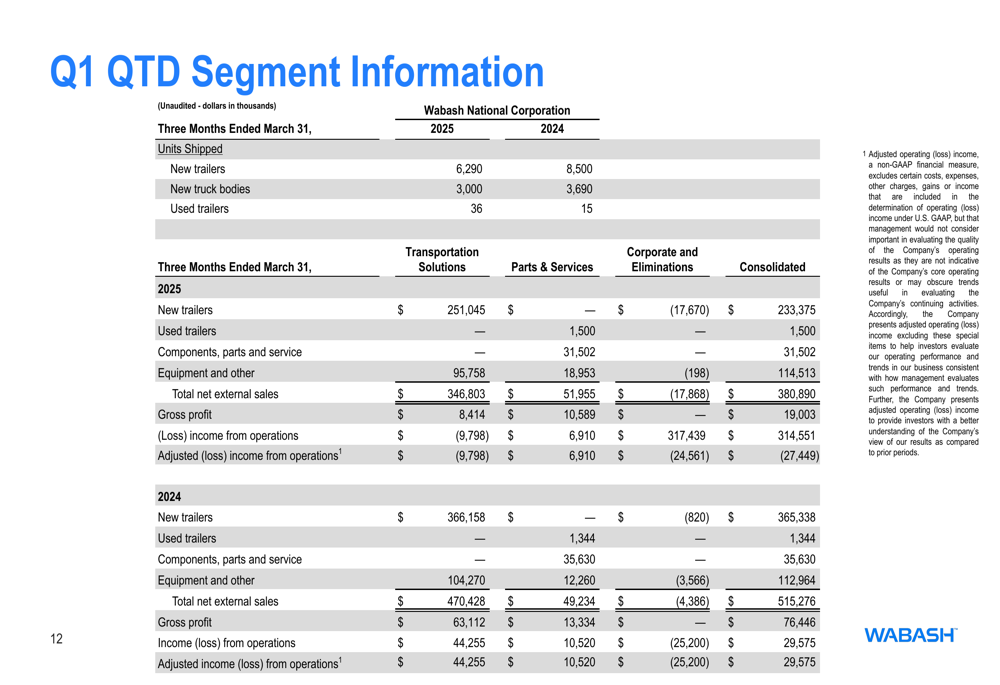

Further segment detail reveals the depth of the challenges facing the Transportation Solutions business:

Cash Flow and Capital Allocation

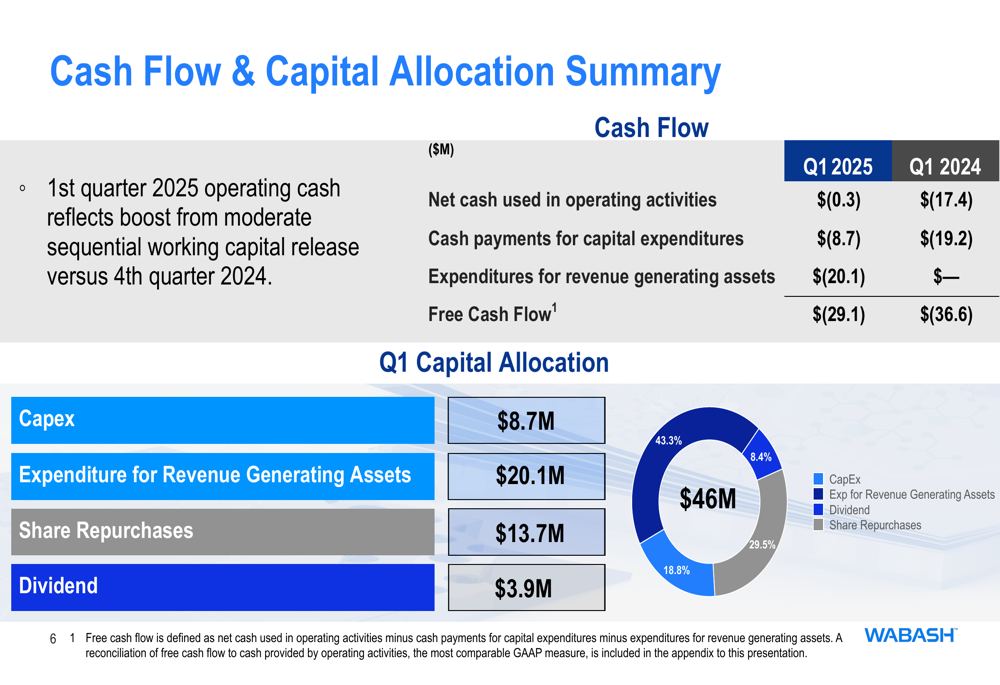

Despite operational headwinds, Wabash showed some improvement in cash management. Net cash used in operating activities improved to $(0.3) million in Q1 2025 compared to $(17.4) million in Q1 2024. The company reported free cash flow of $(29.1) million, slightly better than $(36.6) million in the prior-year period, though still negative.

Capital allocation during the quarter reflected Wabash’s continued investment in future growth despite current challenges. The company allocated $20.1 million to revenue-generating assets, $8.7 million to capital expenditures, $13.7 million to share repurchases, and $3.9 million to dividends.

The following chart illustrates Wabash’s capital allocation priorities:

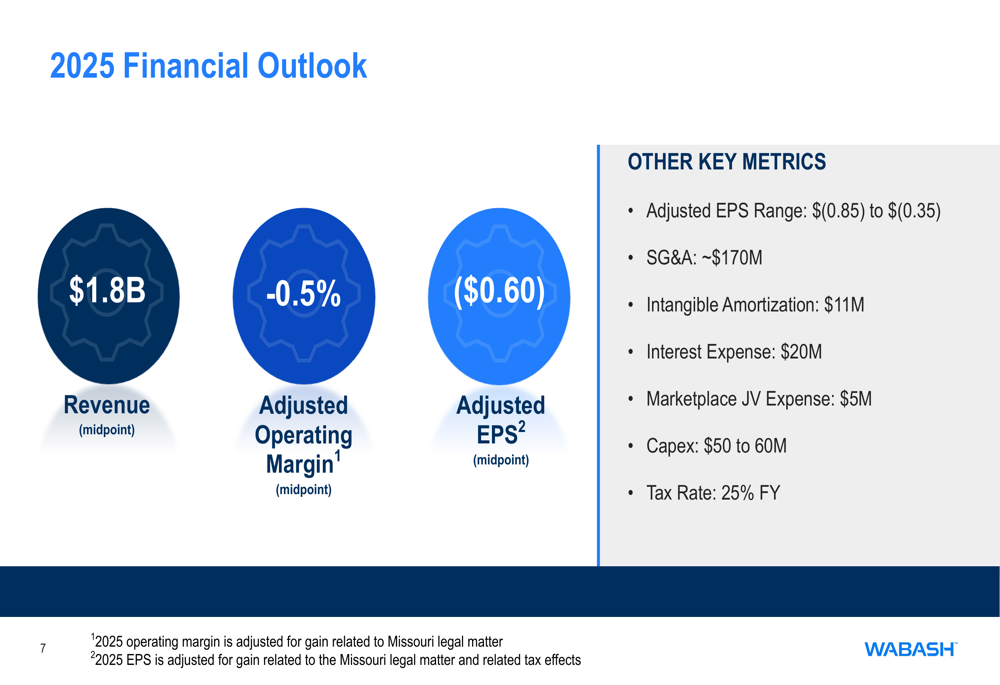

Revised 2025 Outlook

In response to current market conditions, Wabash significantly reduced its full-year 2025 guidance. The company now expects:

- Revenue of approximately $1.8 billion (midpoint)

- Adjusted operating margin of -0.5% (midpoint)

- Adjusted EPS of $(0.60) (midpoint), with a range of $(0.85) to $(0.35)

This represents a substantial downward revision from previous guidance mentioned in the company’s Q4 2024 earnings call, which had projected EPS of $0.85-$1.05 for 2025.

Additional guidance metrics include:

The revised outlook reflects management’s assessment of continued market softness and tariff-related uncertainties affecting customer purchasing decisions throughout 2025.

Market Reaction and Conclusion

The market’s strongly negative reaction to Wabash’s earnings presentation—with shares down over 13% in premarket trading to $8.65—reflects investor concerns about the company’s operational challenges and reduced outlook. The stock had already been trading near its 52-week low of $8.99 before this latest decline.

While the legal settlement provided a significant one-time boost to GAAP results, investors appear focused on the underlying business fundamentals, which show deteriorating margins and weakening demand in the company’s core transportation solutions segment.

Management’s emphasis on the growth in Parts & Services and potential long-term benefits from US manufacturing revitalization offers some positive notes. However, the near-term outlook suggests Wabash faces significant headwinds as it navigates through 2025, with particular challenges in the first half of the year before any potential market stabilization.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.