Wall St futures flat amid US-China trade jitters; bank earnings in focus

Introduction & Market Context

Wag! Group Co (NASDAQ:PET) presented its first quarter 2024 results on May 12, 2025, highlighting record quarterly revenue and strategic expansion plans. The presentation painted an optimistic picture for the pet services company, which has since experienced significant challenges. With shares currently trading at just $0.15, down dramatically from their 52-week high of $2.46, the company’s Q1 optimism stands in stark contrast to its subsequent performance.

Quarterly Performance Highlights

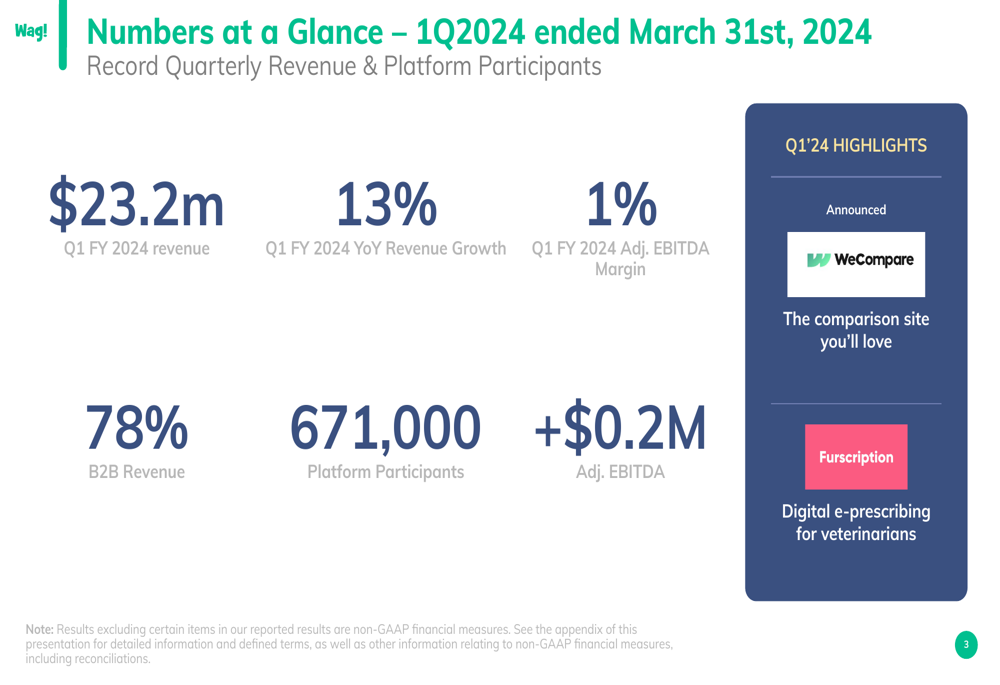

Wag! reported record quarterly revenue of $23.2 million for Q1 2024, representing a 13% year-over-year increase. The company also achieved positive adjusted EBITDA of $0.2 million with a 1% margin, signaling a potential path to profitability. Business-to-business revenue comprised 78% of total revenue, indicating the company’s successful pivot toward enterprise partnerships.

As shown in the following financial highlights slide:

The company reported 671,000 platform participants in Q1, though this metric would later decline as indicated in the full-year earnings report. The presentation also highlighted two new product announcements: WeCompare, a comparison site for insurance products, and Furscription, a digital e-prescribing platform for veterinarians.

Operational Efficiency

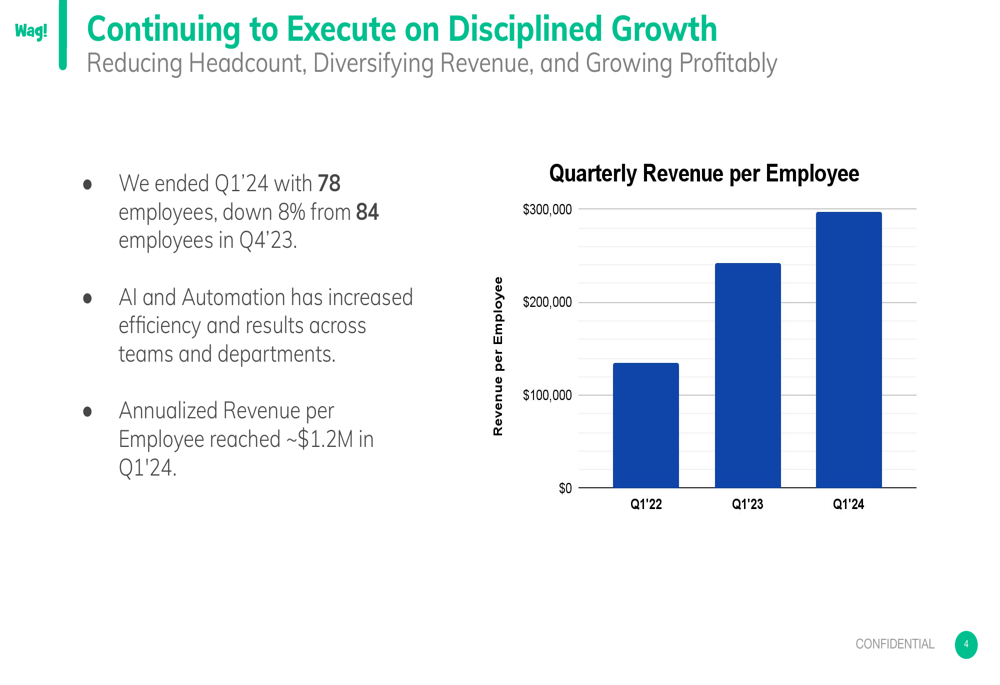

A key focus of Wag!’s Q1 presentation was its drive toward operational efficiency. The company reduced headcount from 84 employees in Q4 2023 to 78 employees in Q1 2024, an 8% reduction. Simultaneously, Wag! increased its annualized revenue per employee to approximately $1.2 million, attributing these efficiency gains to AI implementation and automation across departments.

The following chart illustrates this efficiency trend:

Strategic Initiatives

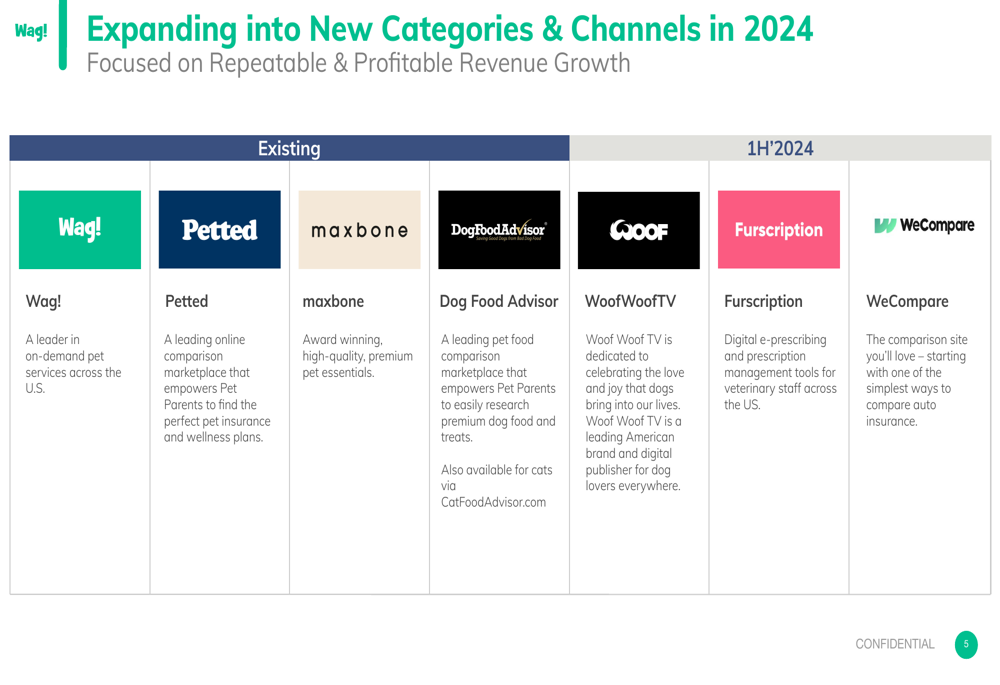

Wag! outlined an ambitious expansion strategy beyond its core pet services business, showcasing a portfolio of existing and planned brands. The company positioned itself as building a comprehensive ecosystem of pet-related services and products, with new ventures launching in the first half of 2024.

This expansion strategy is illustrated in the following slide:

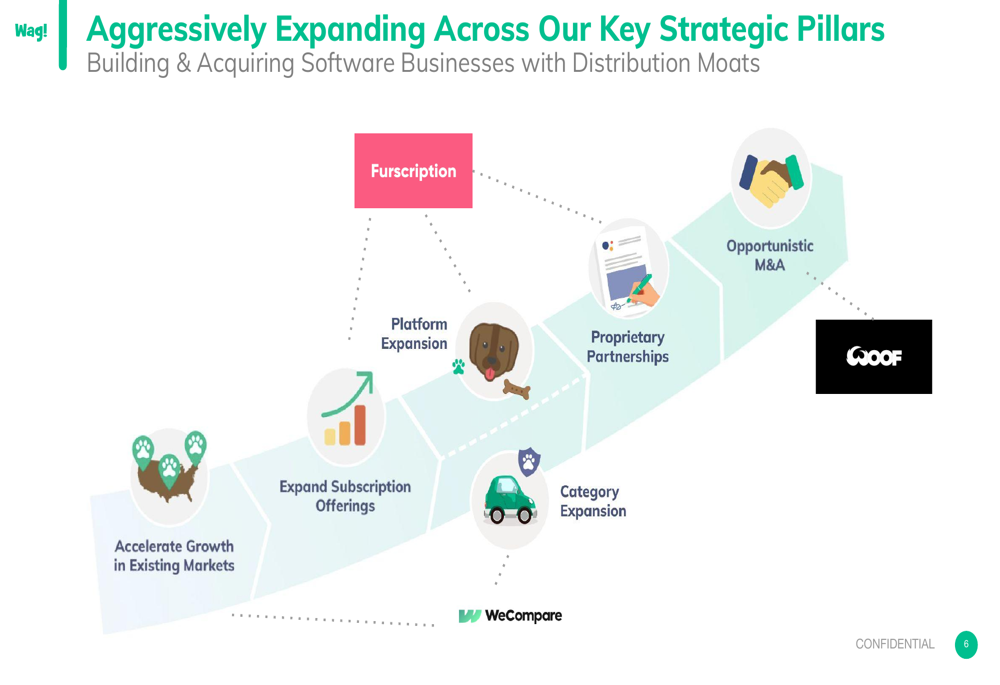

The company’s strategic growth pillars emphasized accelerating growth in existing markets while expanding into new categories through both organic development and acquisitions. Wag! particularly highlighted its focus on building and acquiring software businesses with strong distribution capabilities.

The strategic roadmap was presented as follows:

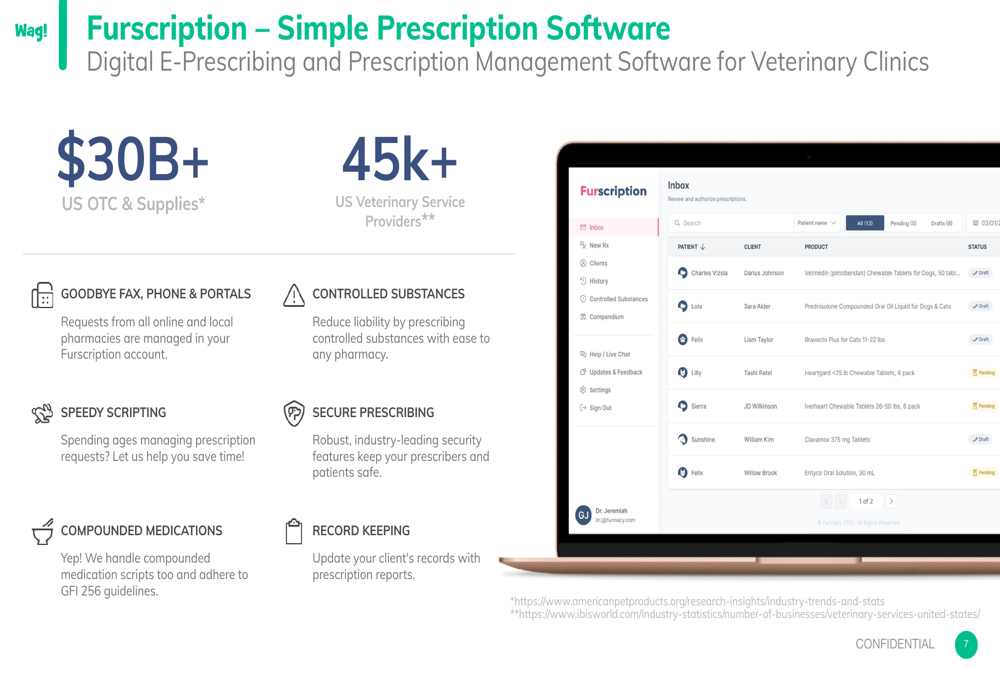

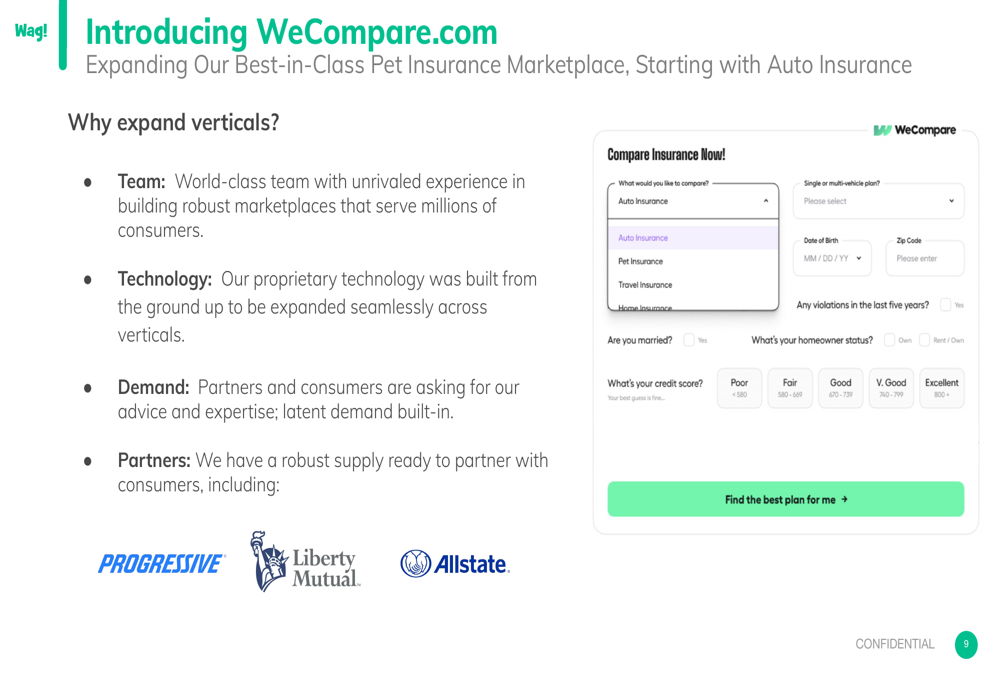

New Product Launches

A significant portion of the presentation was dedicated to new product launches, particularly Furscription and WeCompare. Furscription was positioned as a digital solution for veterinary clinics to manage prescriptions, targeting a $30+ billion U.S. market with over 45,000 veterinary service providers.

The Furscription product was showcased as follows:

Similarly, WeCompare was introduced as Wag!’s expansion into insurance marketplaces, beginning with auto insurance before expanding to pet insurance. The company highlighted partnerships with major insurers including Progressive, Liberty Mutual, and Allstate (NYSE:ALL).

The WeCompare product was presented as follows:

Forward-Looking Statements vs. Actual Results

Perhaps the most striking aspect of the Q1 2024 presentation, in retrospect, is the gap between projected and actual performance. Wag! forecasted 2024 revenue of $105-115 million, representing 31% year-over-year growth, and adjusted EBITDA of $2-6 million with a 4% margin.

The company’s optimistic financial outlook was presented as follows:

However, according to the earnings report, Wag! actually experienced a 16% decline in full-year 2024 revenue to $70.5 million, far below the projected range. Instead of achieving positive adjusted EBITDA of $2-6 million, the company reported an adjusted EBITDA loss of $1.1 million for 2024.

Current Outlook

Despite the significant underperformance in 2024, Wag! has provided a more optimistic outlook for 2025, projecting revenue between $84 million and $88 million with adjusted EBITDA of $2-4 million. The company is focusing on new distribution partnerships in the wellness segment to drive growth.

With a current market capitalization of just $12.26 million and trading below its fair value according to some analysts, Wag! faces significant challenges in rebuilding investor confidence. The company’s financial health score remains weak at 1.63, with concerning cash burn rates and a current ratio of 0.62.

The stark contrast between the optimistic Q1 2024 presentation and the actual full-year results underscores the challenges of the pet services market and the company’s struggle to execute on its ambitious expansion strategy. As Wag! attempts to pivot toward profitability in 2025, investors will be closely watching whether the company can deliver on its latest projections or if history will repeat itself.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.