SoFi shares rise as record revenue, member growth drive strong Q3 results

Introduction & Market Context

Wärtsilä Corporation (HEL:WRT1V) presented its third-quarter 2025 results on October 28, revealing a mixed performance characterized by declining sales but significantly improved profitability. The Finnish marine and energy solutions provider saw its stock decline by 2.32% following the announcement, trading at €26.91 as investors weighed strong operational improvements against revenue challenges.

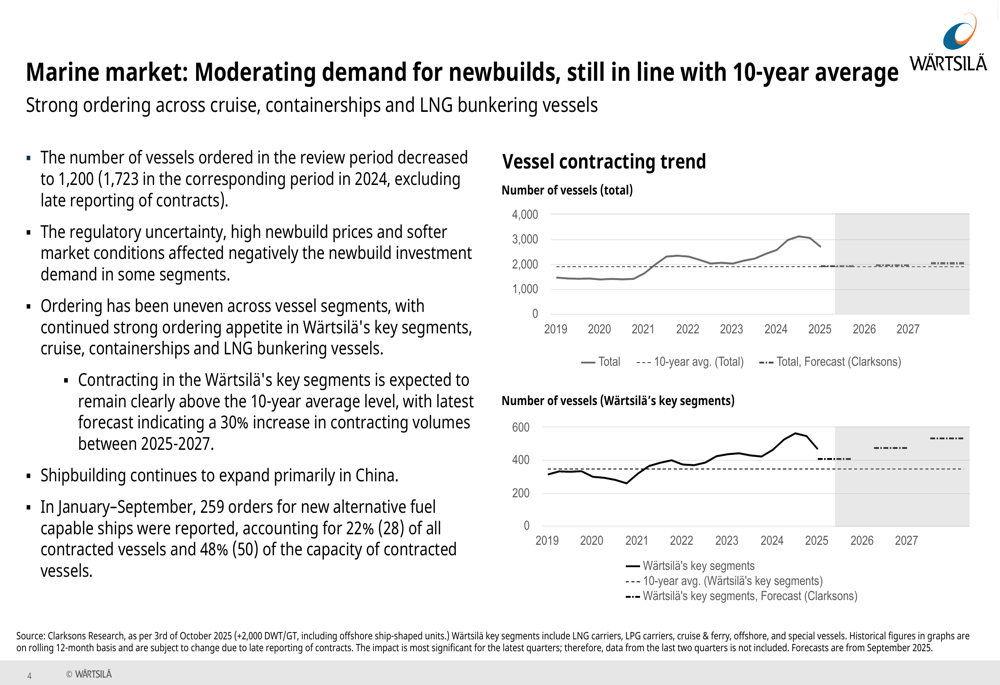

The company operates in a complex market environment with moderating demand in the marine sector, though still in line with the 10-year average, while the energy sector continues to see strong investment in renewables and grid infrastructure. Geopolitical uncertainties and regulatory changes, particularly in the energy storage sector, have created headwinds in certain segments of Wärtsilä’s business.

Quarterly Performance Highlights

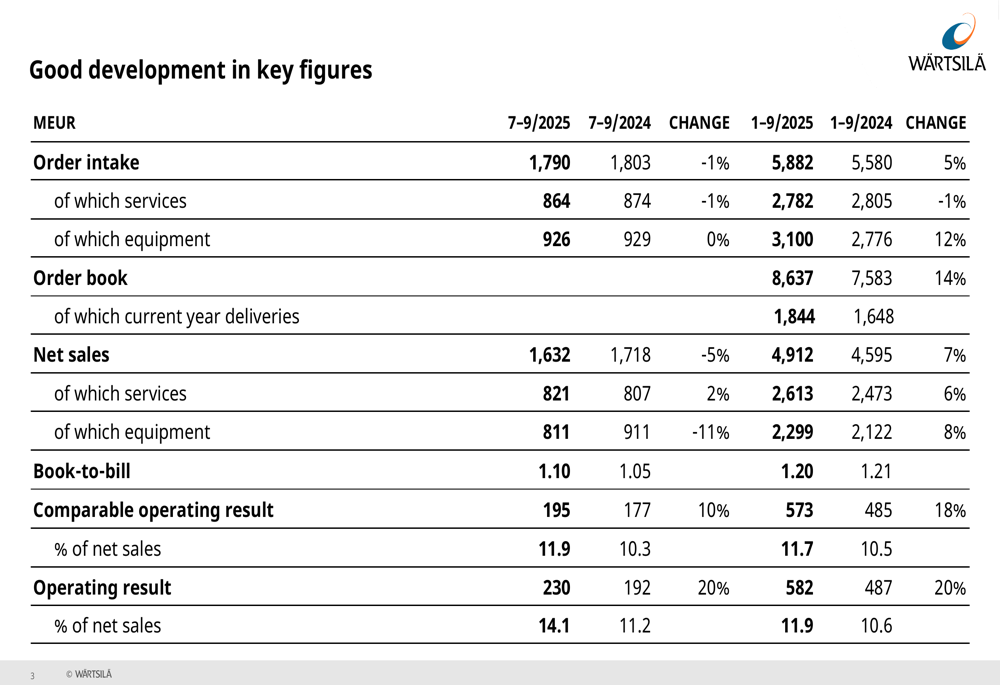

Wärtsilä reported stable order intake at €1,790 million for Q3 2025, while net sales decreased by 5% year-over-year to €1,632 million. Despite this revenue decline, the company achieved significant improvements in profitability, with comparable operating result increasing by 10% to €195 million, representing 11.9% of net sales. The operating result showed an even stronger improvement, rising 20% to €230 million or 14.1% of net sales.

As shown in the following comprehensive overview of key financial metrics:

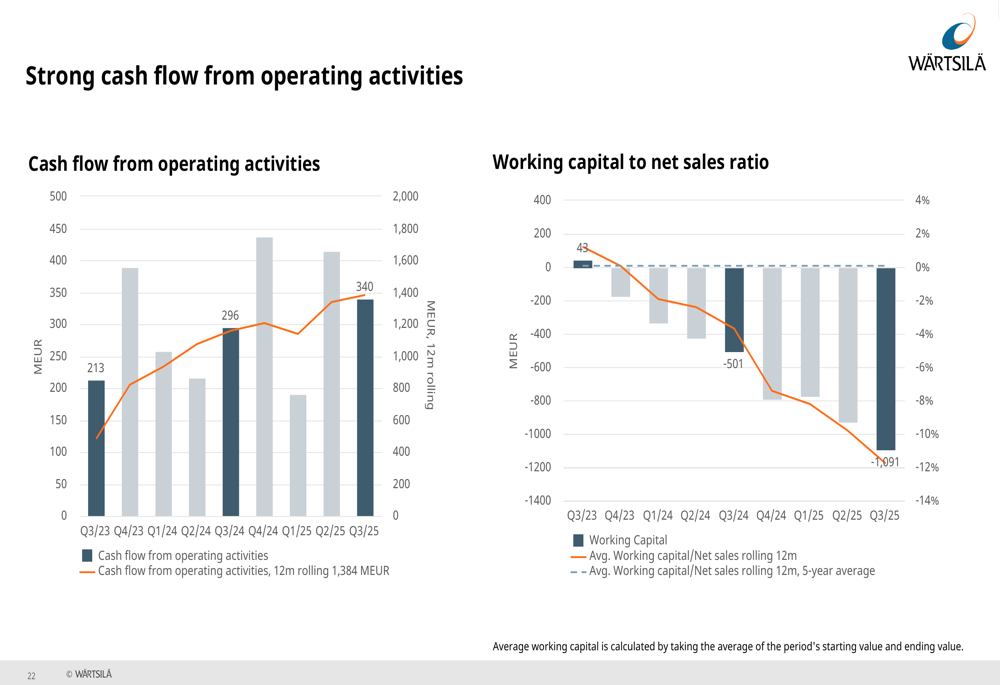

The company generated exceptionally strong cash flow from operating activities of €340 million, which CEO Håkan Agnevall noted was "at least the highest cash flow in the last 15 years." This cash generation helped strengthen Wärtsilä’s financial position, though the company still maintains a negative net interest-bearing debt of €1,415 million.

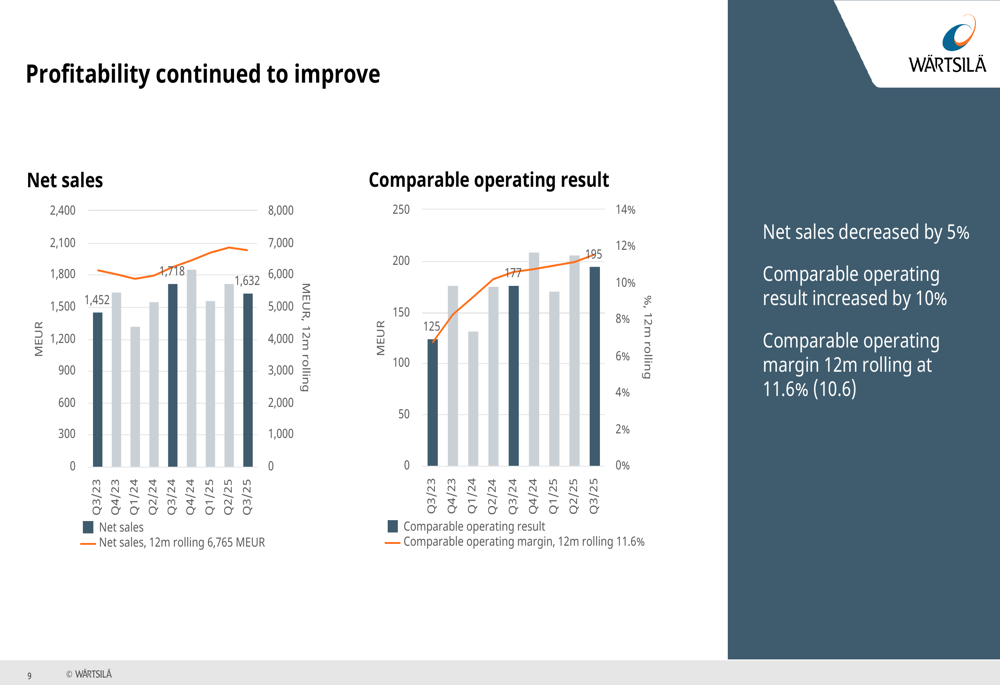

The following chart illustrates the company’s profitability improvement trend:

Segment Analysis

Marine

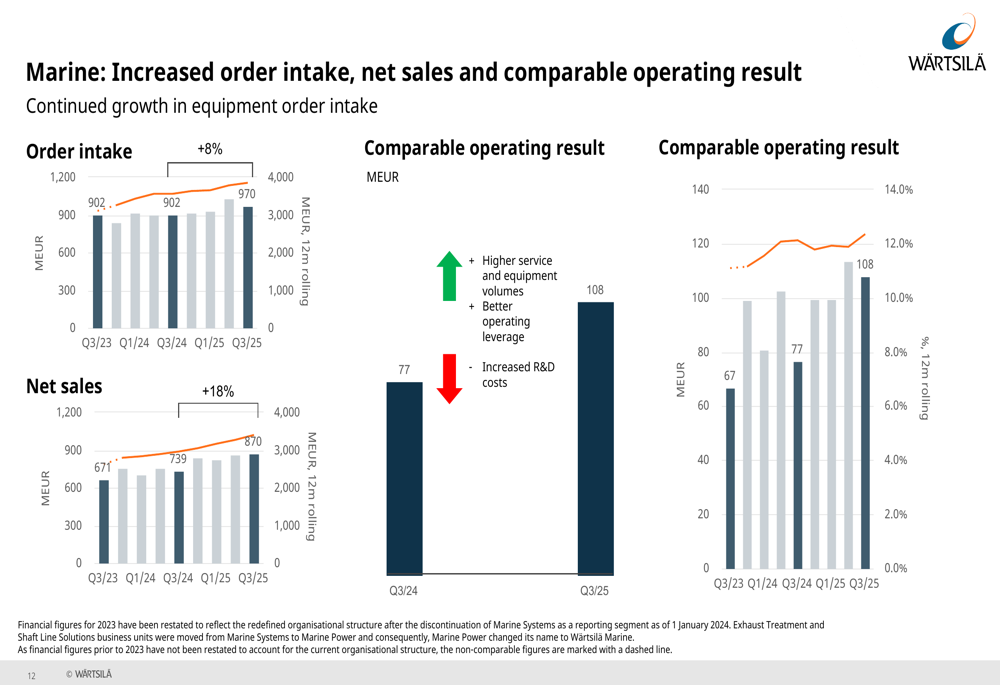

The Marine division delivered strong results, with order intake increasing by 8% and net sales rising by 18% compared to the same period last year. The book-to-bill ratio in Marine services remained well above 1, indicating healthy future revenue streams. According to the presentation, vessel contracting in Wärtsilä’s key segments is expected to remain above the 10-year average, with a 30% increase forecast between 2025-2027.

The marine market overview reveals moderating but still healthy demand:

The division’s performance metrics show consistent improvement:

Energy

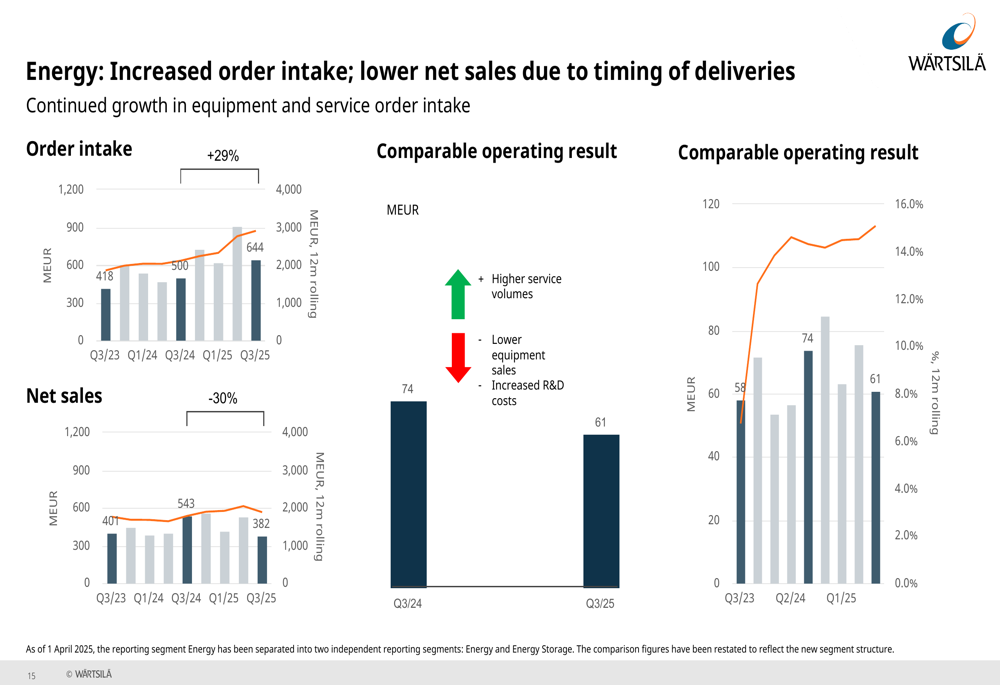

The Energy division showed mixed results with order intake increasing by 29% but net sales decreasing by 30% due to the timing of deliveries. The company noted that demand remains strong for equipment and services for engine power plants, with baseload engine power plants expected to remain stable and growth anticipated in data center applications.

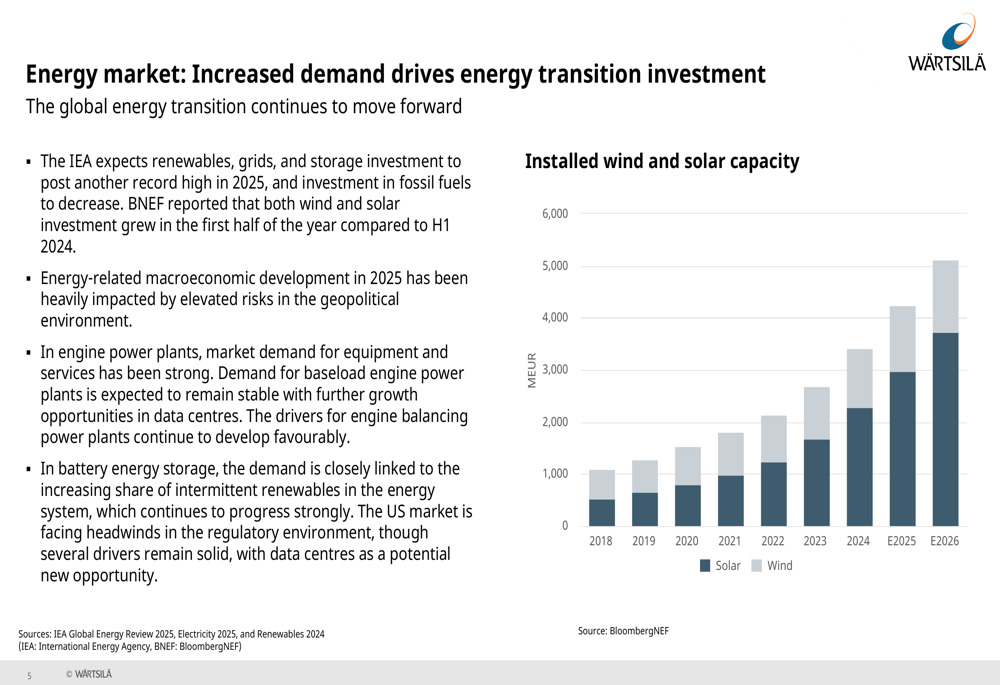

The energy market continues to see significant investment in renewables:

Despite lower net sales, the Energy division maintained solid performance metrics:

Energy Storage

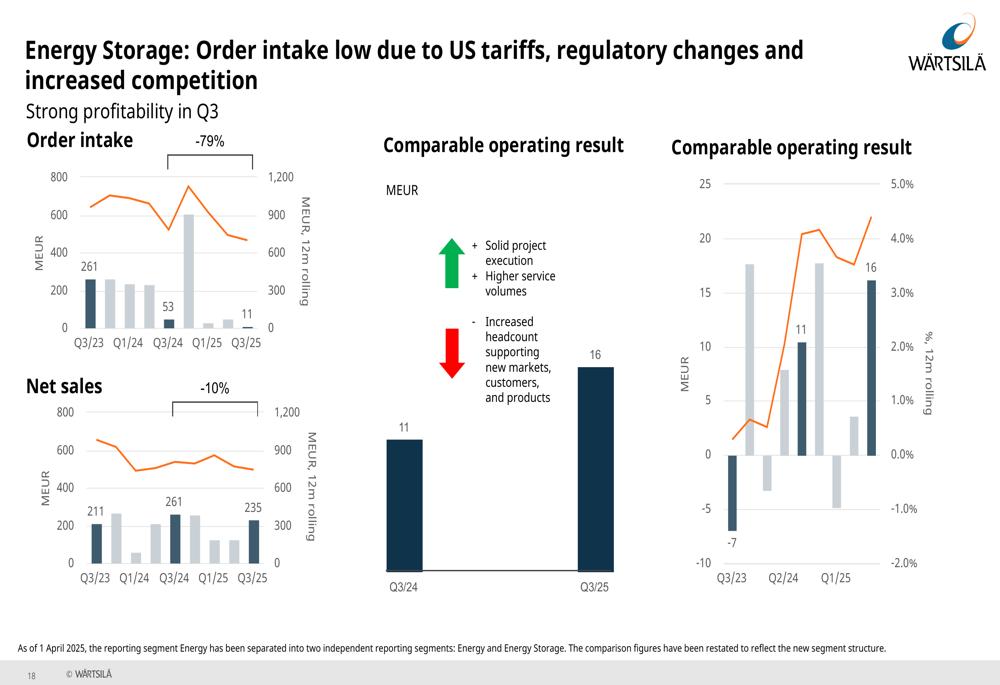

The Energy Storage segment faced significant challenges, with order intake decreasing by 79% and net sales declining by 10%. Wärtsilä attributed these difficulties to U.S. tariffs, regulatory changes, and increased competition. Despite these headwinds, the company expects the demand environment to improve in the coming quarters, though geopolitical uncertainty may affect growth.

The following chart illustrates the challenging situation in Energy Storage:

Strategic Initiatives and Outlook

Wärtsilä continues to reshape its portfolio through strategic divestments. The company completed the divestment of its Automation, Navigation and Control Systems (ANCS) business to Solix on July 1, which had a positive impact of €34 million on the Q3 results. Additionally, Wärtsilä announced plans to divest its Marine Electrical Systems business to Vinci Energies, with the transaction expected to close in Q4 2025.

The company’s cash flow performance has been particularly strong, as illustrated in this chart:

Looking ahead, Wärtsilä provided the following outlook for the next 12 months:

- Marine: Demand environment expected to be better than in the comparison period

- Energy: Demand environment expected to be similar to the comparison period

- Energy Storage: Demand environment expected to be better than in the comparison period, though geopolitical uncertainty may affect growth

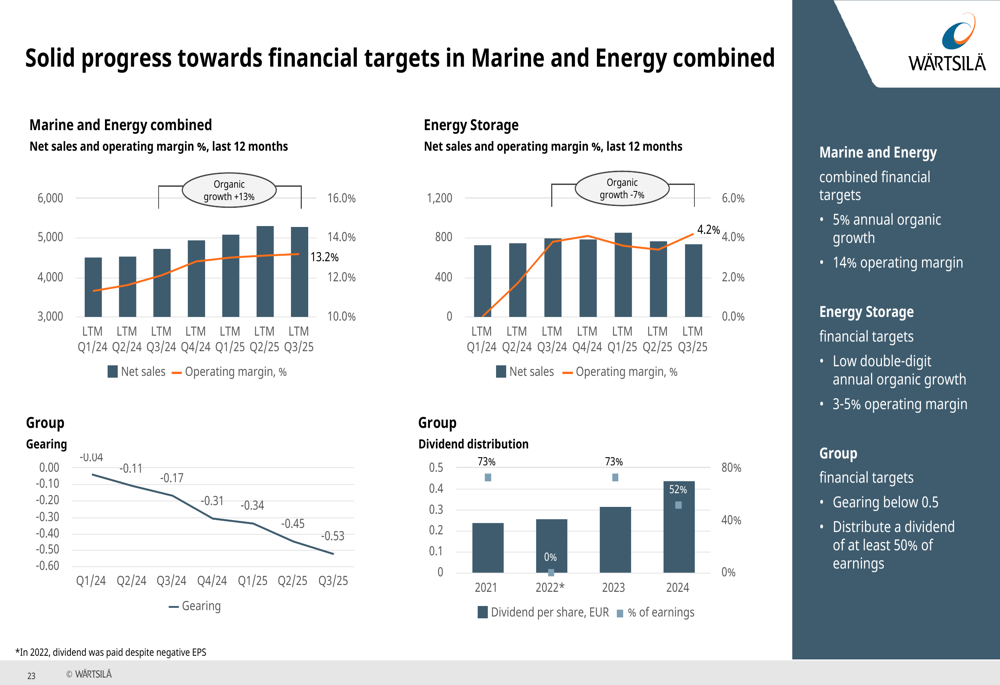

The company continues to make progress toward its financial targets, as shown in this comprehensive overview:

Market Reaction and Analyst Perspectives

Wärtsilä’s stock declined by 2.32% following the earnings announcement, reflecting investor concerns about the revenue decline despite improved profitability. According to the earnings call transcript, analysts showed significant interest in the company’s data center power generation capabilities, particularly in the 50-400 megawatt range.

The company maintains a "GREAT" financial health score of 3.36, according to InvestingPro data, supported by strong revenue growth of 14.68% over the last twelve months. Despite recent volatility, the stock has delivered an impressive 62.27% return over the past six months.

Wärtsilä’s strategic focus on innovation, including the launch of a marine carbon capture solution and expansion into data center power generation, underscores its commitment to sustainable growth in its core markets. However, the negative net cash position and continued revenue challenges in certain segments remain areas of concern for investors evaluating the company’s long-term prospects.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.