Street Calls of the Week

Introduction & Market Context

WashTec AG (ETR:WSU), a leading provider of car wash solutions, presented its first half 2025 financial results on August 5, 2025, reporting solid growth despite regional disparities. The company’s stock closed at €40.60 on August 4, up 3.31% ahead of the earnings release, suggesting positive market expectations.

H1 2025 Performance Highlights

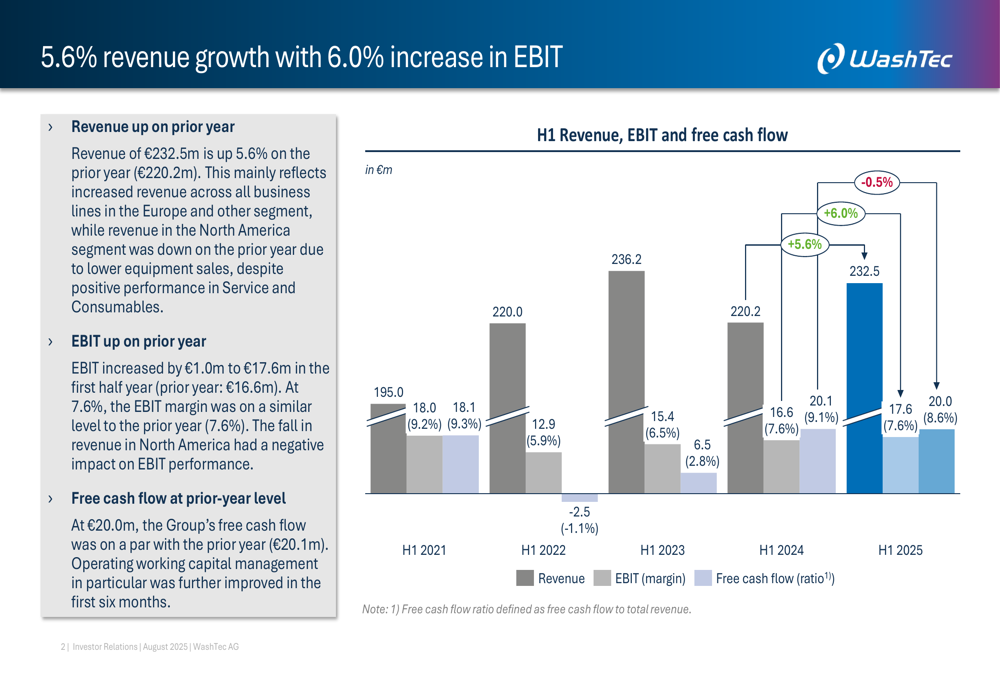

WashTec delivered revenue of €232.5 million in the first half of 2025, representing a 5.6% increase from €220.2 million in the same period last year. EBIT rose by 6.0% to €17.6 million, maintaining a stable EBIT margin of 7.6%. Free cash flow remained nearly unchanged at €20.0 million compared to €20.1 million in H1 2024.

As shown in the following chart of WashTec’s H1 performance over the past five years, the company has maintained consistent revenue growth since 2021, with the exception of a dip in 2024:

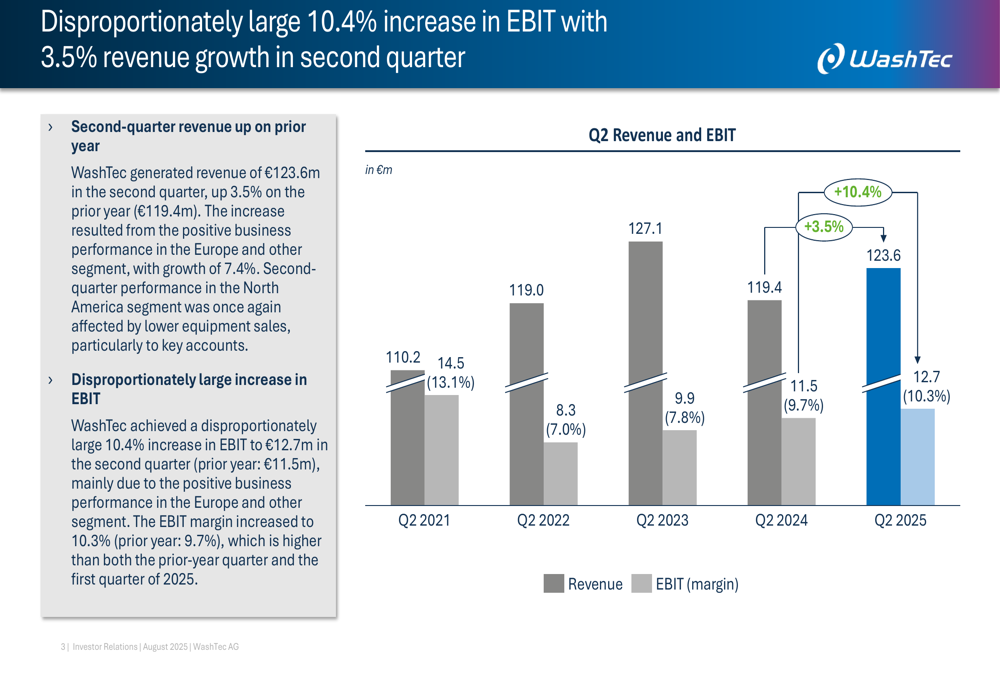

The second quarter showed particularly strong profitability improvement, with EBIT increasing by 10.4% to €12.7 million on a more modest 3.5% revenue growth to €123.6 million. This resulted in an EBIT margin expansion to 10.3% from 9.7% in Q2 2024.

The following chart illustrates WashTec’s Q2 performance trends:

Segment Performance Analysis

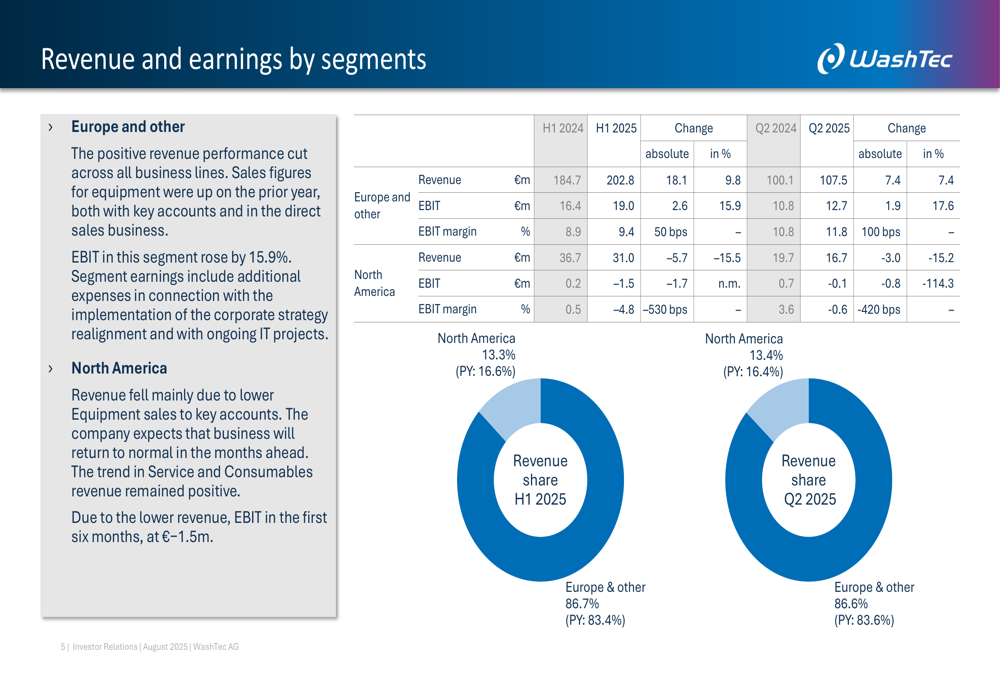

WashTec’s performance revealed a stark contrast between its geographical segments. The Europe & Other segment demonstrated robust growth with revenue increasing 9.8% to €202.8 million and EBIT rising 15.9% to €19.0 million. This resulted in an improved EBIT margin of 9.4%, up from 8.9% in H1 2024.

In contrast, the North American segment faced significant challenges, with revenue declining 15.5% to €31.0 million and EBIT falling to -€1.5 million from €0.2 million in the prior year. This resulted in a negative EBIT margin of -4.8%, a substantial deterioration from the 0.5% margin in H1 2024.

The following breakdown illustrates the geographical performance disparities:

Business Line Breakdown

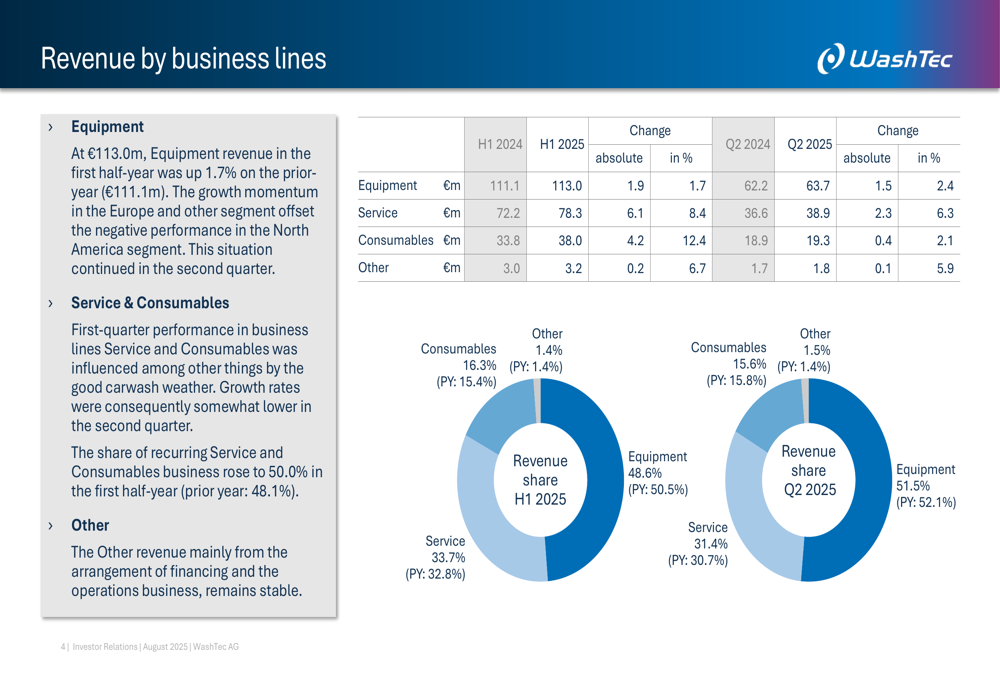

A notable strategic development is the growing importance of WashTec’s recurring revenue streams. Service and Consumables businesses now account for 50.0% of the company’s first-half revenue, providing greater stability to the overall business model.

Equipment sales, which remain the largest revenue contributor at 48.6% of H1 2025 revenue, grew modestly by 1.7% to €113.0 million. Service revenue increased by 8.4% to €78.3 million, while Consumables saw the strongest growth at 12.4% to €38.0 million.

The following chart provides a detailed breakdown of revenue by business lines:

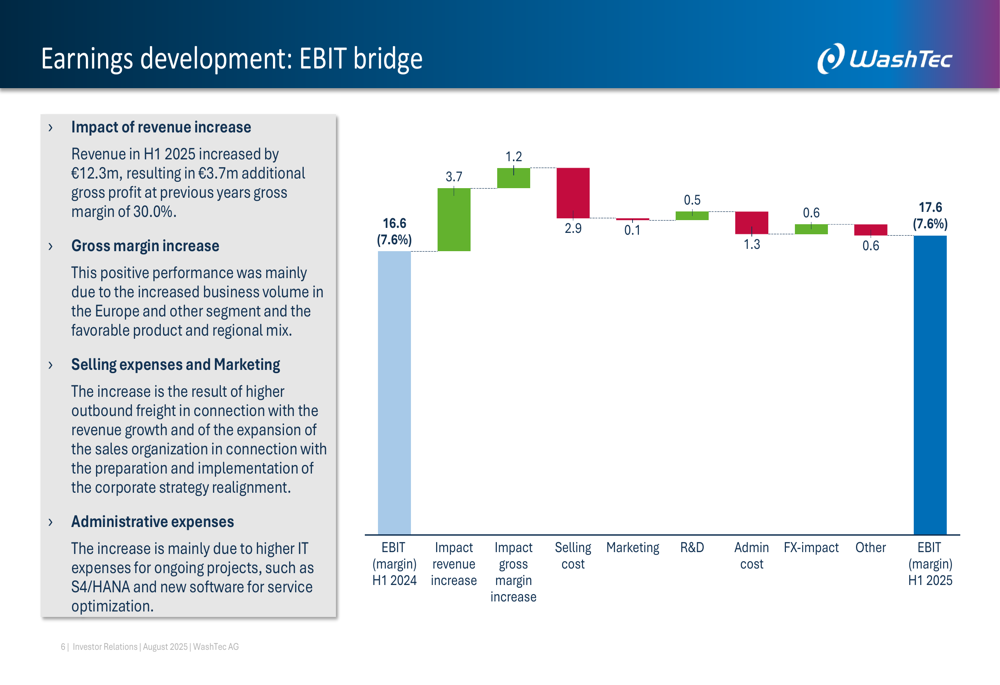

WashTec’s EBIT development was influenced by several factors. While increased revenue and improved gross margins contributed positively, these gains were partially offset by higher selling, R&D, and administrative costs:

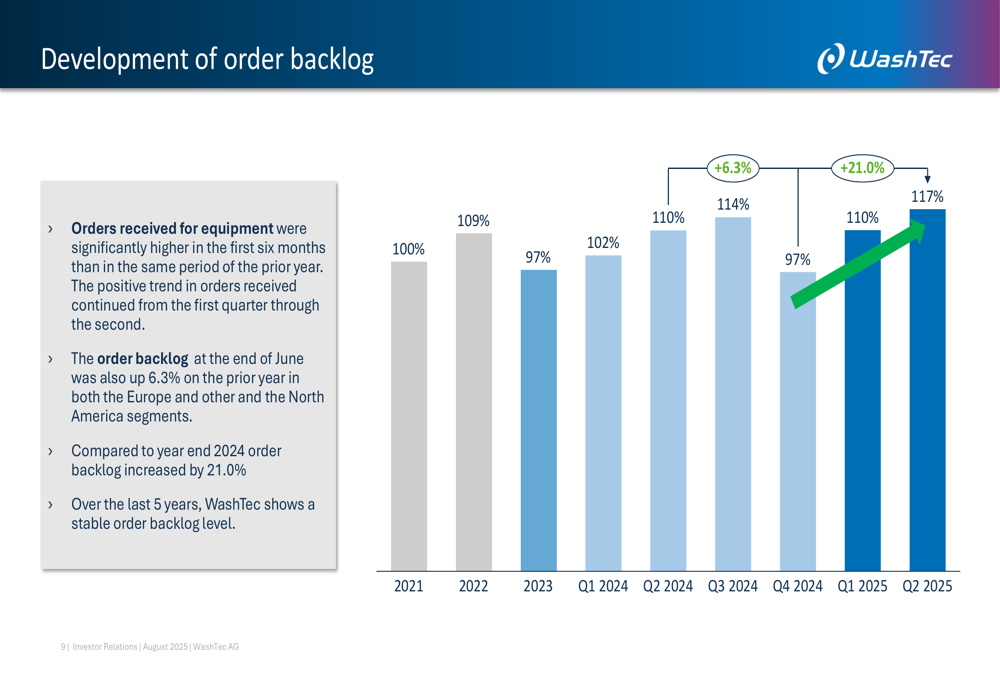

Order Backlog and Future Outlook

WashTec reported a significant improvement in its order backlog, which increased by 6.3% compared to the prior year and by 21.0% from year-end 2024. This positive trend suggests strong demand for the company’s equipment and provides good visibility for future revenue.

As illustrated in the following chart, the order backlog has shown consistent growth since Q2 2024:

The company also reported an increase in its workforce, adding 110 employees since June 2024 to reach a total of 1,808. Most of these additions were in Service (+77) and Sales (+15) roles, aligning with the company’s focus on growing its service business.

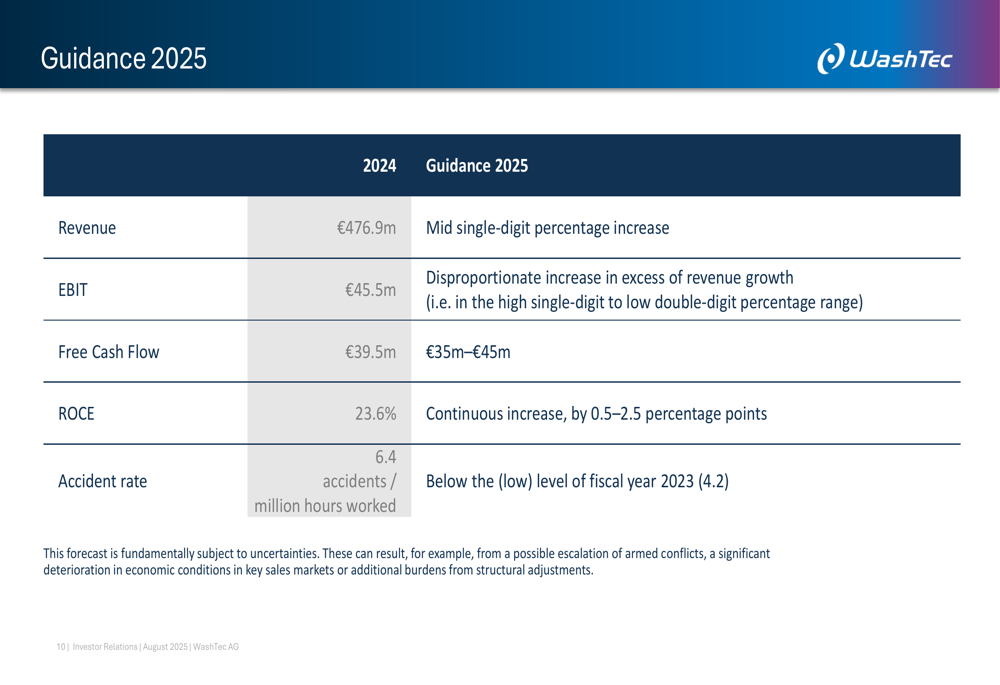

Guidance for 2025

Based on its first-half performance and growing order backlog, WashTec maintained its positive outlook for the full year 2025. The company expects a mid-single-digit percentage increase in revenue compared to 2024’s €476.9 million, with EBIT growing at a faster rate in the high single-digit to low double-digit percentage range.

Free cash flow is projected to be between €35 million and €45 million, compared to €39.5 million in 2024. The company also anticipates a continuous increase in ROCE by 0.5-2.5 percentage points from the 23.6% achieved in 2024.

The following table summarizes WashTec’s guidance for 2025:

While WashTec’s overall performance remains solid, the company will need to address the challenges in its North American segment to maintain its growth trajectory. The increasing share of recurring revenue from Service and Consumables provides a positive foundation for more stable future performance, potentially offsetting volatility in equipment sales.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.