Buy tech sell-off, Wedbush’s Ives says: ’this is a 1996 moment, not 1999’

Introduction & Market Context

Watts Water Technologies, Inc. (NYSE:WTS) presented its first quarter 2025 earnings results on May 8, 2025, highlighting better-than-expected performance despite challenging macroeconomic conditions. The company demonstrated resilience in the face of headwinds including fewer shipping days, ongoing weakness in European markets, and the looming impact of tariffs.

The water solutions provider maintained its full-year outlook while emphasizing its proactive approach to mitigating tariff impacts through strategic pricing, supply chain adjustments, and leveraging its U.S. manufacturing footprint. This comes as the company navigates a complex economic environment characterized by lower global GDP forecasts and interest rates remaining higher for longer.

Quarterly Performance Highlights

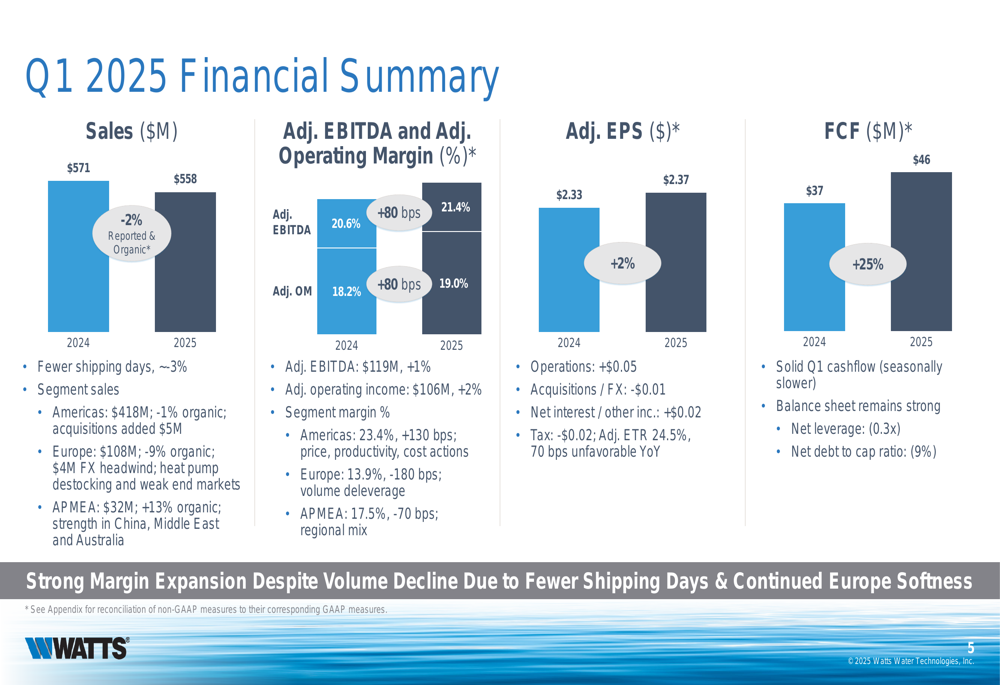

Watts Water reported Q1 2025 sales of $558 million, representing a 2% decrease both on a reported and organic basis compared to the prior year. Despite this decline, the company achieved a record adjusted operating margin of 19.0%, an expansion of 80 basis points year-over-year.

As shown in the following financial summary:

Adjusted earnings per share increased 2% to $2.37, while free cash flow grew impressively by 25% to $46 million. The company’s performance varied significantly by region, with Americas showing relative stability with a 1% organic sales decline, Europe continuing to struggle with a 9% organic drop, and APMEA (Asia-Pacific, Middle East, and Africa) delivering strong 13% organic growth driven by strength in China, the Middle East, and Australia.

The company’s ability to expand margins despite volume declines demonstrates effective cost control and operational efficiency. This performance allowed Watts Water to announce a substantial 21% dividend increase, underscoring management’s confidence in the company’s financial strength and future prospects.

Strategic Initiatives

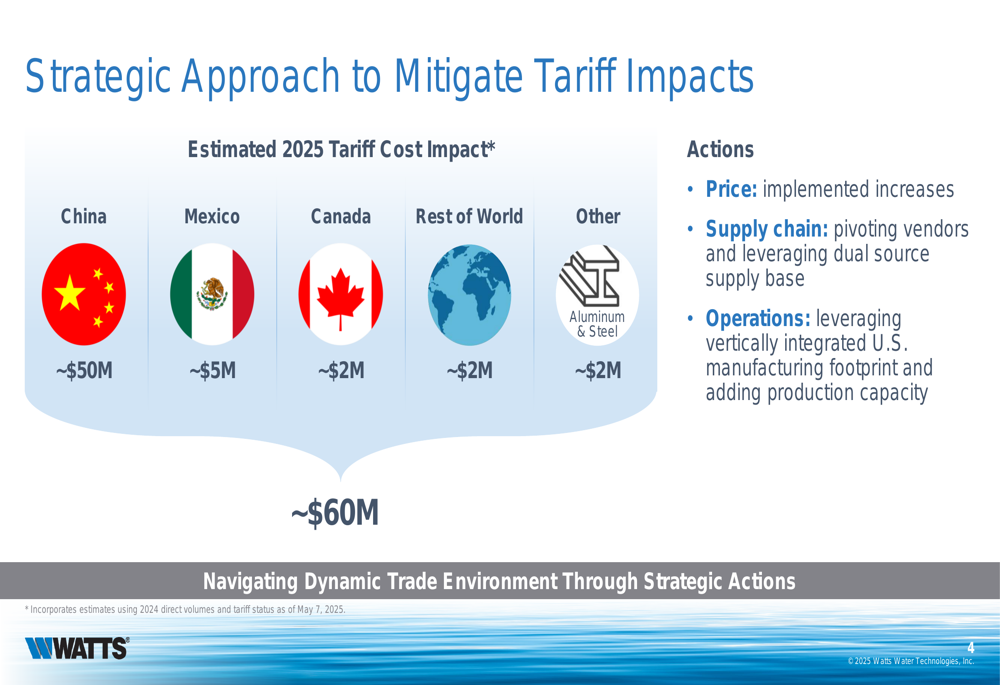

A central focus of Watts Water’s presentation was its comprehensive strategy to address the estimated $60 million impact from tariffs in 2025. The company outlined a three-pronged approach to mitigate these effects:

With approximately 83% of the tariff impact coming from China, Watts Water is implementing price increases, pivoting vendors, leveraging its dual-source supply base, and capitalizing on its vertically integrated U.S. manufacturing capabilities. The company is also adding production capacity to ensure supply chain resilience.

Beyond tariff mitigation, Watts Water continues to advance other strategic initiatives including:

1. Driving productivity and restructuring actions

2. Proceeding with a scheduled site closure in France

3. Progressing well with the integration of I-CON

4. Continuing investments in new product development and digital strategy

These initiatives align with the company’s long-term focus on innovation and profitable growth, as highlighted in their key themes:

Detailed Financial Analysis

Watts Water’s financial performance in Q1 2025 demonstrated the company’s ability to drive profitability even amid volume challenges. Adjusted EBITDA increased to $119 million, representing 21.4% of sales (an 80 basis point improvement), while adjusted operating income grew 2% to $106 million.

The company’s balance sheet remains exceptionally strong, with a net debt to capitalization ratio of -9%, indicating more cash than debt. This financial flexibility provides Watts Water with ample liquidity for strategic investments, acquisitions, and shareholder returns.

Segment performance varied considerably:

- Americas: $418 million in sales (-1% organic), with acquisitions adding $5 million

- Europe: $108 million (-9% organic), with a $4 million FX headwind and continued heat pump destocking

- APMEA: $32 million (+13% organic), showing strength across multiple markets

Segment margins also reflected these disparities, with Americas achieving a robust 23.4% adjusted operating margin, Europe at 13.9%, and APMEA at 17.5%.

Forward-Looking Statements

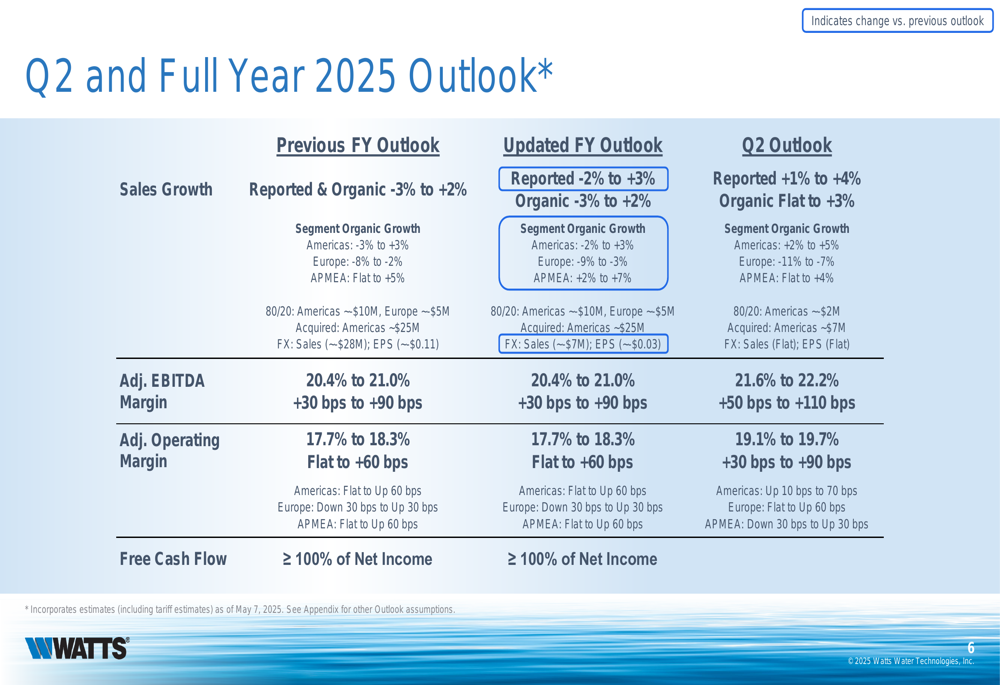

Looking ahead, Watts Water maintained its full-year 2025 outlook despite the challenging environment:

For Q2 2025, the company projects reported sales growth of 1% to 4% and organic sales growth of flat to 3%. The full-year outlook anticipates reported sales between -2% and +3%, with organic sales between -3% and +2%.

Management identified several positive factors supporting their outlook, including Q1 performance, pricing actions, mega project activity, and favorable foreign exchange. These are balanced against negative factors such as lower global GDP forecasts, potential tariff impacts on second-half demand, higher-for-longer interest rates, and continued destocking in Europe.

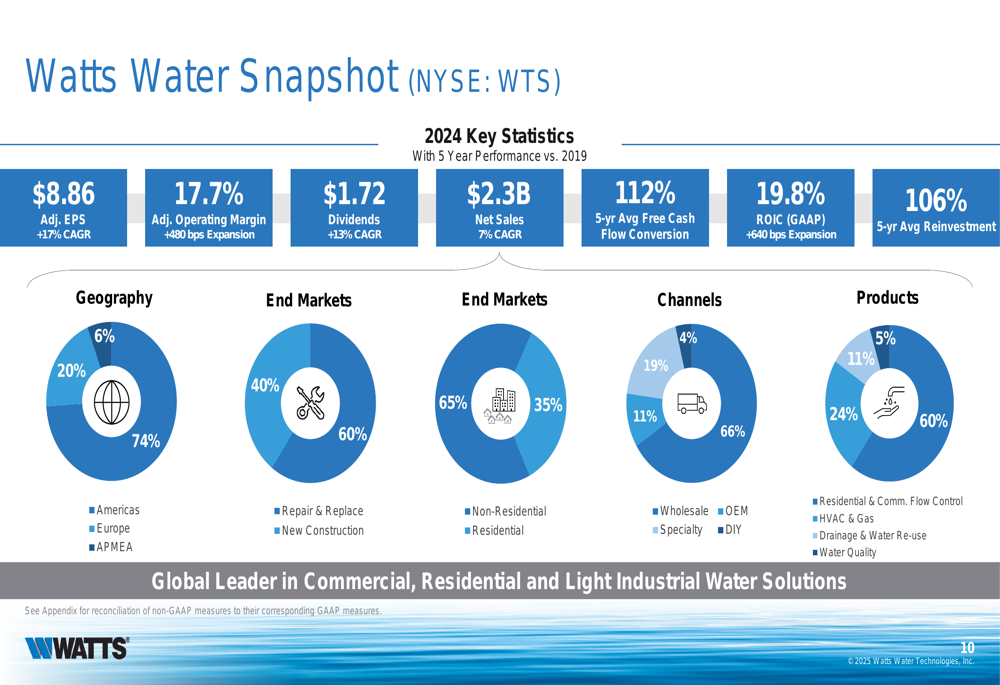

The company’s 2025 snapshot highlights its long-term performance trajectory, with impressive 5-year growth metrics:

Conclusion

Watts Water Technologies’ Q1 2025 results demonstrate the company’s operational resilience and strategic agility in navigating a complex economic environment. Despite volume challenges, the company achieved record margins and maintained its full-year outlook while proactively addressing significant tariff headwinds.

The regional performance disparities highlight both challenges and opportunities, with Europe continuing to struggle while APMEA delivers strong growth. With a robust balance sheet, strong cash flow generation, and clear strategic initiatives, Watts Water appears well-positioned to manage near-term headwinds while advancing its long-term growth objectives.

Investors will be watching closely to see if the company’s tariff mitigation strategies prove effective and whether European markets begin to recover in the coming quarters. The maintenance of full-year guidance suggests management confidence in the company’s ability to execute despite the challenging backdrop.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.