Novo Nordisk, Eli Lilly slide after Trump comments on weight loss drug pricing

Introduction & Market Context

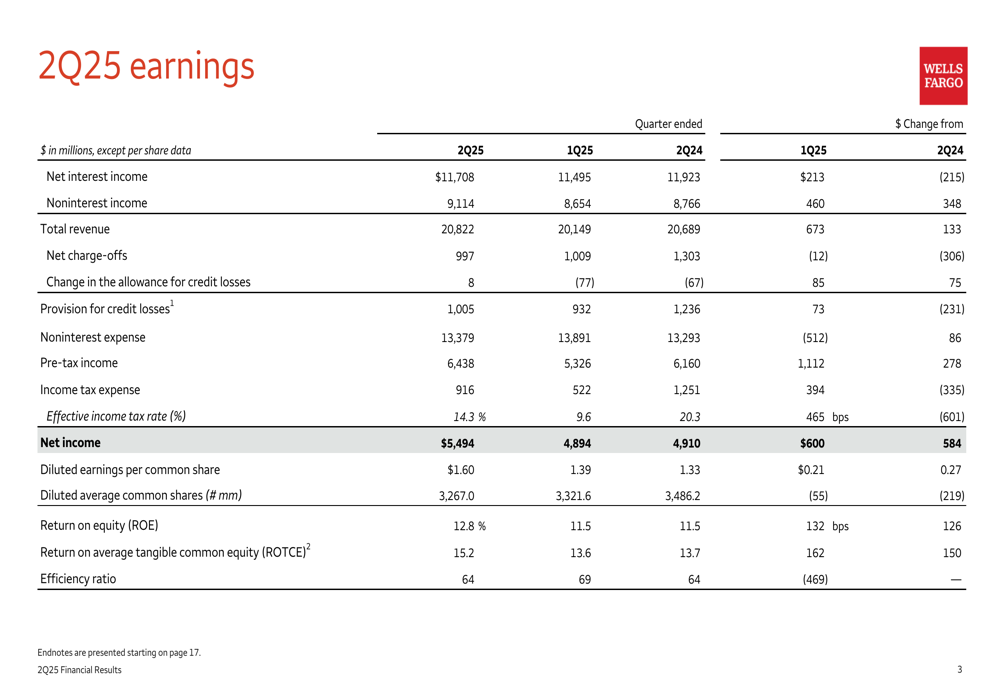

Wells Fargo & Company (NYSE:WFC) reported second-quarter 2025 financial results on July 15, showing improved performance with earnings per share rising to $1.60, up from $1.39 in the first quarter and $1.33 a year ago. The bank’s shares were down 1.11% in premarket trading to $82.50, following a 1.07% gain to $83.43 in the previous session.

The Q2 results demonstrate Wells Fargo’s continued progress in improving efficiency and profitability despite ongoing challenges in the interest rate environment. The bank’s performance builds on its Q1 2025 results, which exceeded EPS expectations but fell short on revenue projections.

Quarterly Performance Highlights

Wells Fargo reported net income of $5.5 billion for the second quarter, representing a significant improvement from $4.9 billion in both Q1 2025 and Q2 2024. The results included a $253 million gain associated with the acquisition of the remaining interest in the bank’s merchant services joint venture.

As shown in the following comprehensive earnings summary, Wells Fargo delivered improved performance across several key metrics compared to both the previous quarter and the same period last year:

Total (EPA:TTEF) revenue reached $20.8 billion, up 1% year-over-year and 3.3% from the first quarter. This represents a notable improvement from Q1 2025, when the bank reported revenue of $20.15 billion, falling short of analyst expectations.

Return on equity (ROE) improved to 12.8% from 11.5% in both Q1 2025 and Q2 2024, while return on average tangible common equity (ROTCE) increased to 15.2% from 13.6% in Q1 2025 and 13.7% in Q2 2024. The efficiency ratio improved to 64% from 69% in the previous quarter, matching the 64% reported in Q2 2024.

Detailed Financial Analysis

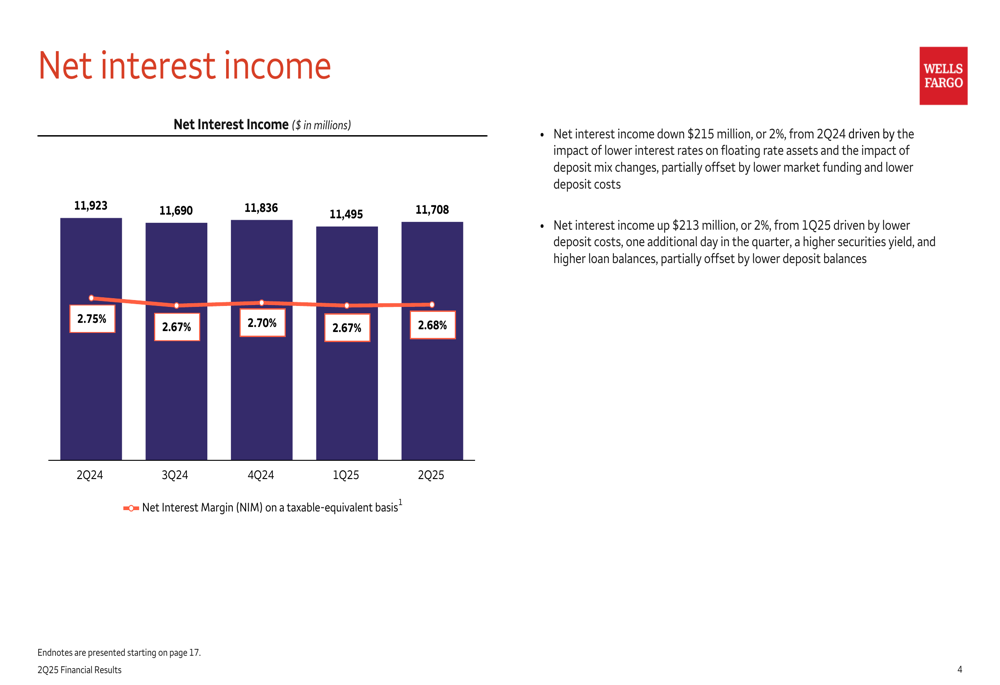

Net interest income totaled $11.7 billion, down 2% year-over-year but up 2% from the first quarter. The sequential improvement was driven by lower deposit costs, one additional day in the quarter, a higher securities yield, and higher loan balances, partially offset by lower deposit balances.

As illustrated in the following chart, net interest margin slightly improved to 2.68% from 2.67% in Q1 2025, though still down from 2.75% in Q2 2024:

Noninterest income increased to $9.1 billion, up 4% year-over-year and 5% from the previous quarter. The growth was driven by higher investment advisory fees, increased card fees following the merchant services joint venture acquisition, and higher investment banking fees.

On the expense front, noninterest expense totaled $13.4 billion, up 1% year-over-year but down 4% from Q1 2025. The sequential decrease was primarily due to lower personnel expenses, partially offset by higher litigation accruals.

Credit Quality and Capital Position

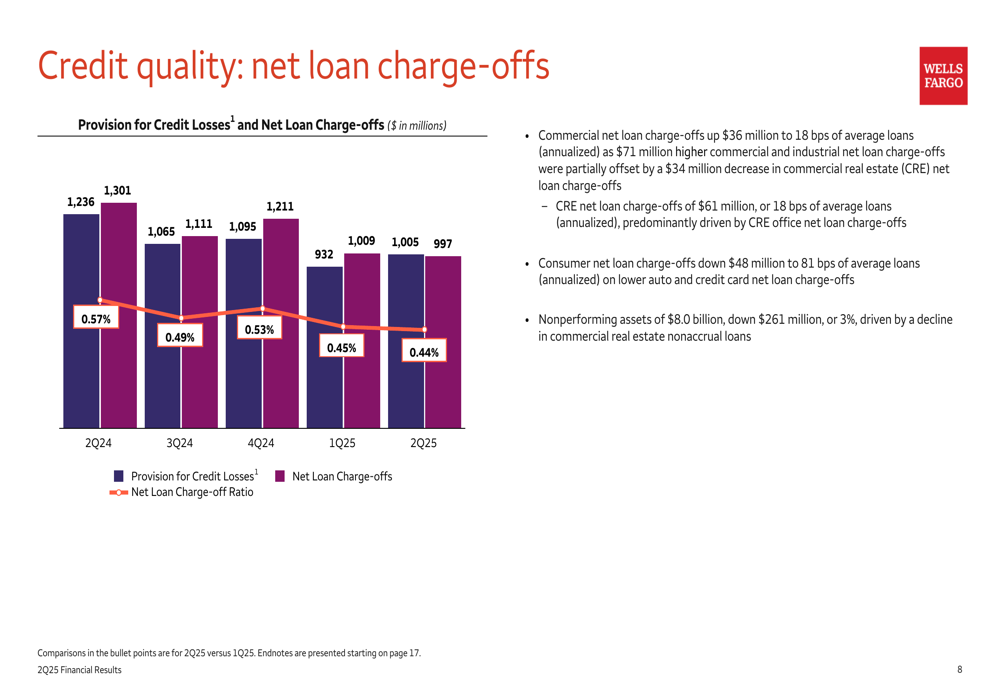

Credit quality showed improvement with net loan charge-offs of $1.0 billion, down $304 million from Q2 2024. The net loan charge-off ratio decreased to 0.44% of average loans (annualized), compared to 0.57% a year ago.

The following chart illustrates the improving trend in credit quality metrics:

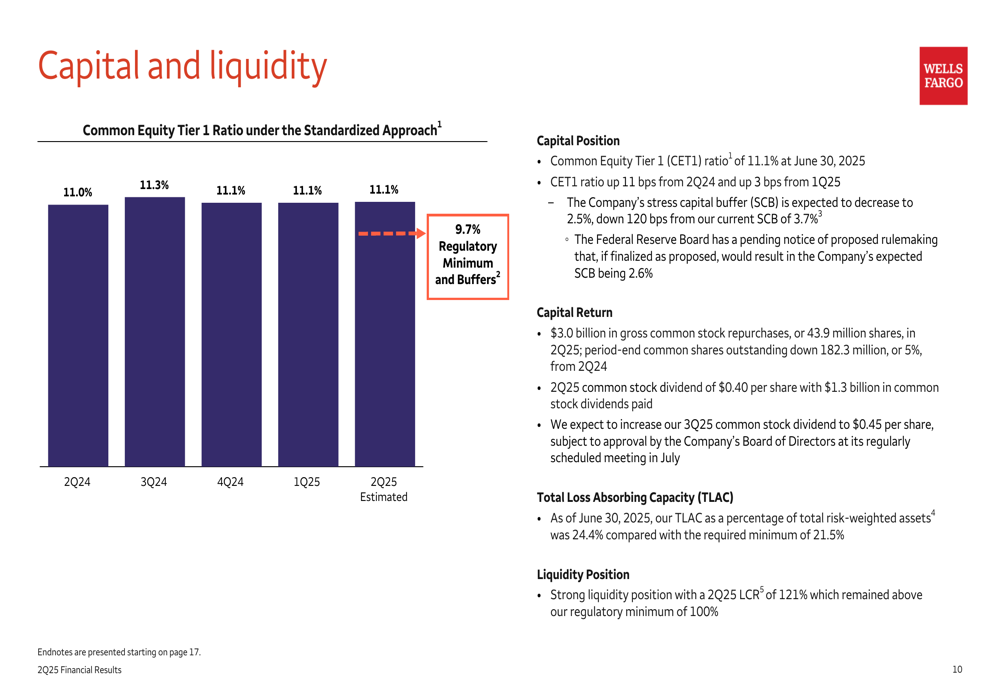

Wells Fargo maintained a strong capital position with a Common Equity Tier 1 (CET1) ratio of 11.1% under the Standardized Approach, up 11 basis points from Q2 2024 and 3 basis points from Q1 2025. The bank’s stress capital buffer is expected to decrease to 2.5%, down 120 basis points from the current 3.7%.

The bank continued its significant capital return to shareholders with $3.0 billion in gross common stock repurchases (43.9 million shares) in Q2 2025 and $1.3 billion in common stock dividends paid. Period-end common shares outstanding decreased by 182.3 million, or 5%, from Q2 2024.

Business Segment Performance

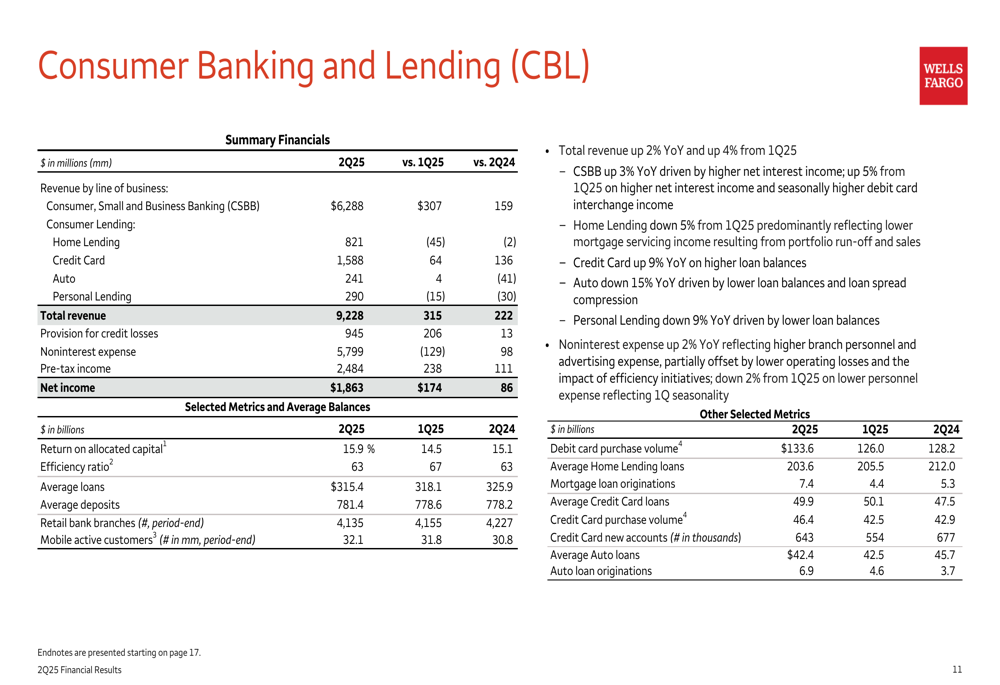

Wells Fargo’s Consumer Banking and Lending segment reported total revenue of $9.2 billion, up 2% year-over-year and 4% from Q1 2025. The segment’s net income reached $1.9 billion, reflecting strong performance in consumer lending activities.

As shown in the following segment breakdown, Consumer Banking and Lending remains the largest contributor to Wells Fargo’s revenue:

The Wealth and Investment Management segment demonstrated particularly strong performance with a 28.7% return on allocated capital. Total revenue for this segment reached $3.9 billion, up 1% both year-over-year and quarter-over-quarter.

Commercial Banking also performed well with a 15.8% return on allocated capital, though total revenue declined 6% year-over-year while remaining relatively stable compared to Q1 2025. The decline was primarily driven by lower net interest income due to the impact of lower interest rates.

Corporate and Investment Banking reported total revenue of $4.7 billion, down 3% year-over-year and 8% from Q1 2025. The decline was driven by lower banking revenue and reduced activity in the commercial real estate sector.

Strategic Initiatives & Outlook

Wells Fargo’s acquisition of the remaining interest in its merchant services joint venture contributed positively to results, generating a $253 million gain and boosting card fee revenue. This strategic move aligns with the bank’s focus on expanding fee-based revenue streams.

The bank continues to implement efficiency initiatives across all business segments, which helped offset higher operating costs and contributed to the improved efficiency ratio in Q2 2025.

Looking forward, Wells Fargo expects 2025 net interest income to be roughly in line with 2024’s $47.7 billion, a revision from previous guidance that projected a 1-3% increase. This change primarily reflects lower net interest income in the Markets business, which is largely offset by higher noninterest income.

The bank maintained its noninterest expense guidance of approximately $54.2 billion for 2025, unchanged from prior guidance, reflecting continued discipline in expense management.

Capital Management and Shareholder Returns

Wells Fargo’s strong capital position has enabled significant returns to shareholders. The bank’s capital and liquidity metrics remain well above regulatory requirements, as illustrated in the following chart:

With a Total Loss-Absorbing Capacity (TLAC) ratio of 24.4% compared to the required minimum of 21.5% and a Liquidity Coverage Ratio (LCR) of 121% versus the regulatory minimum of 100%, Wells Fargo maintains substantial financial flexibility.

The expected reduction in the stress capital buffer to 2.5% could potentially allow for increased capital returns to shareholders in future quarters, though the bank did not provide specific guidance on this front.

Overall, Wells Fargo’s Q2 2025 results demonstrate continued progress in improving profitability and efficiency while navigating a challenging interest rate environment. The bank’s strategic initiatives, including the merchant services acquisition and ongoing efficiency measures, are contributing positively to performance despite headwinds in certain business segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.