United Homes Group stock plunges after Nikki Haley, directors resign

Introduction & Market Context

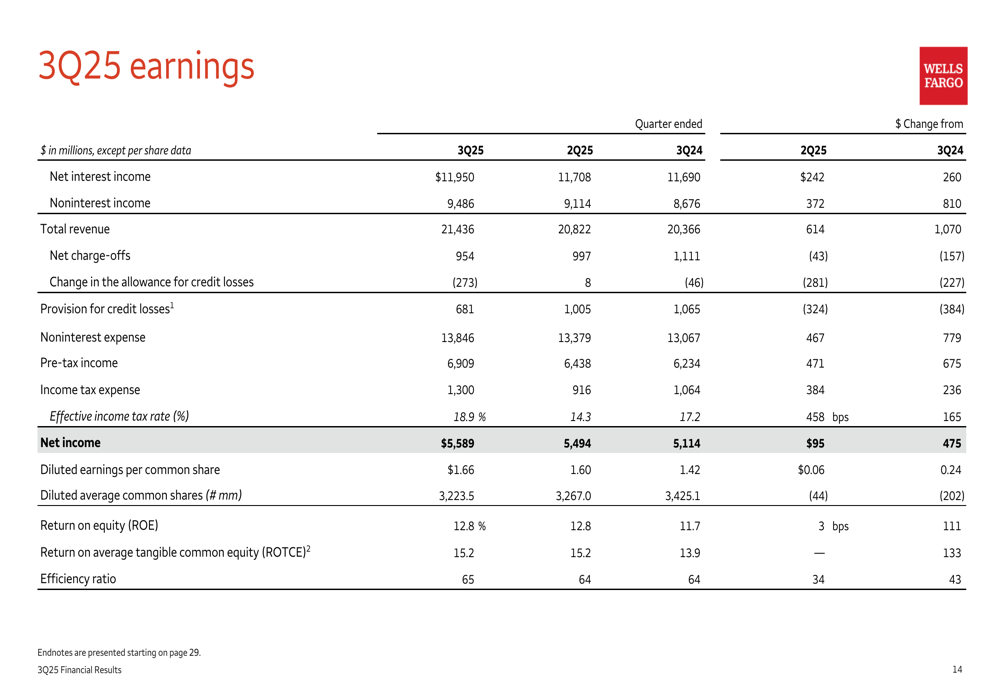

Wells Fargo & Company (NYSE:WFC) delivered strong third-quarter 2025 results on October 14, beating analyst expectations with earnings per share of $1.66 compared to the forecasted $1.55. The bank’s U.S.-centric strategy appears to be paying off, with revenue reaching $21.4 billion, up 5% year-over-year. Following the earnings announcement, Wells Fargo’s stock rose 6.72% to close at $84.22, with pre-market trading showing a 4% gain.

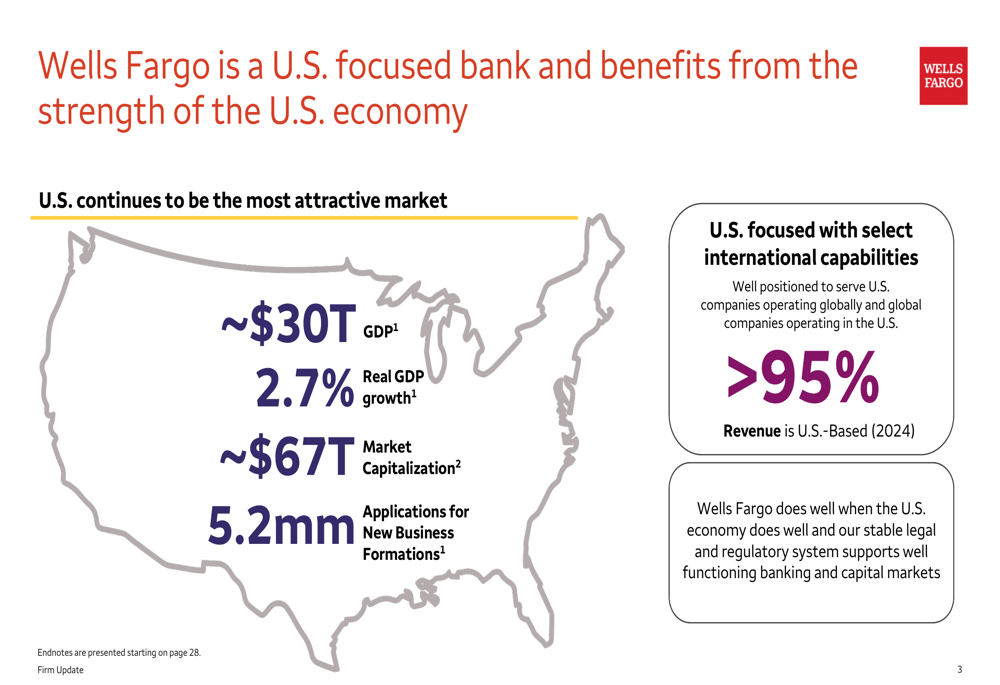

The bank’s presentation emphasized its strategic focus on the U.S. market, where over 95% of its revenue is generated. This positioning allows Wells Fargo to capitalize on the strength of the U.S. economy, which boasts a GDP of approximately $30 trillion and 2.7% real GDP growth.

As shown in the following image highlighting Wells Fargo’s U.S. focus:

Quarterly Performance Highlights

Wells Fargo reported net income of $5.6 billion ($1.66 per share) for Q3 2025, representing a 9% increase from the same period last year. Revenue growth was driven by both net interest income, which rose 2% year-over-year to $12.0 billion, and noninterest income, which increased 9% to $9.5 billion.

The bank’s Q3 2025 earnings statement reveals consistent improvement across key financial metrics:

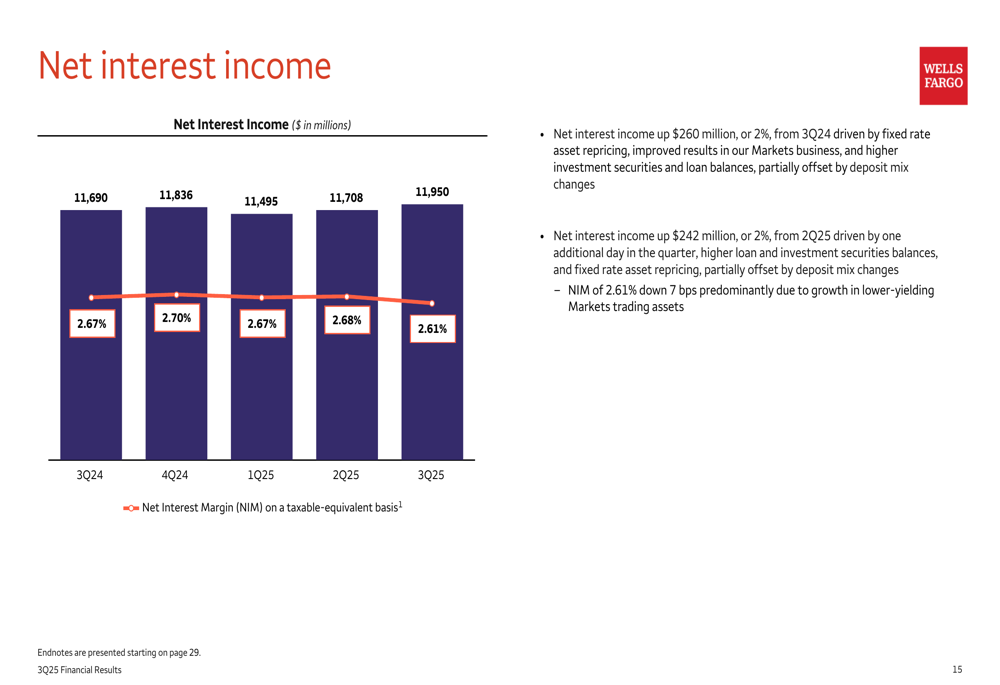

Net interest income benefited from fixed rate asset repricing, improved results in the Markets business, and higher investment securities and loan balances, partially offset by deposit mix changes. The net interest margin (NIM) stood at 2.61%, down 7 basis points primarily due to growth in lower-yielding Markets trading assets.

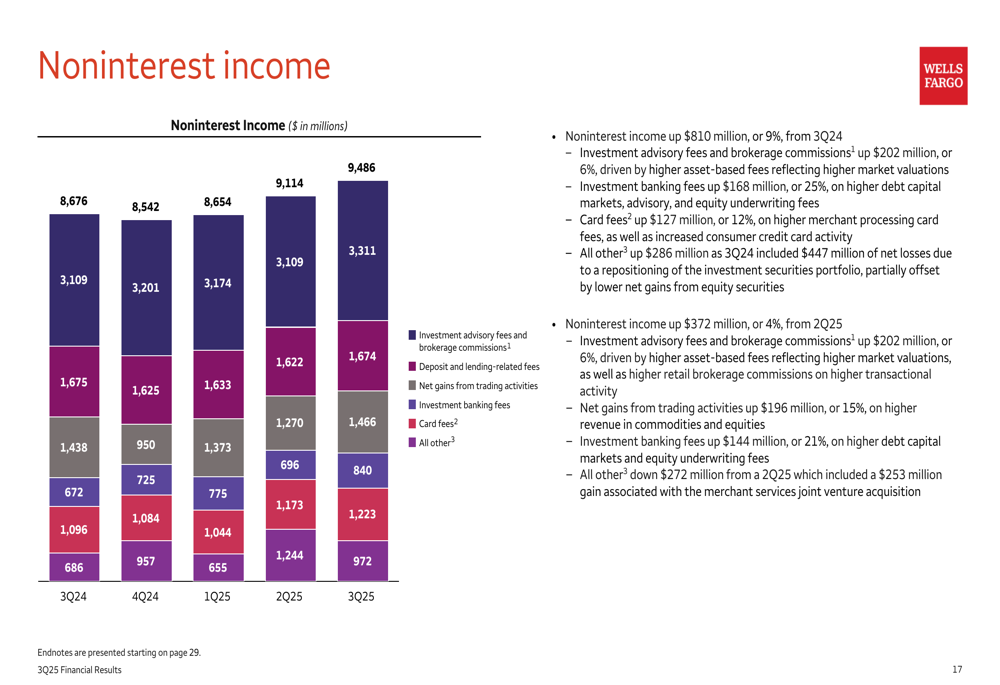

Noninterest income saw significant growth, up $810 million or 9% from Q3 2024, with investment advisory fees and brokerage commissions increasing by $202 million (6%). This growth reflects the bank’s efforts to diversify revenue streams beyond traditional lending.

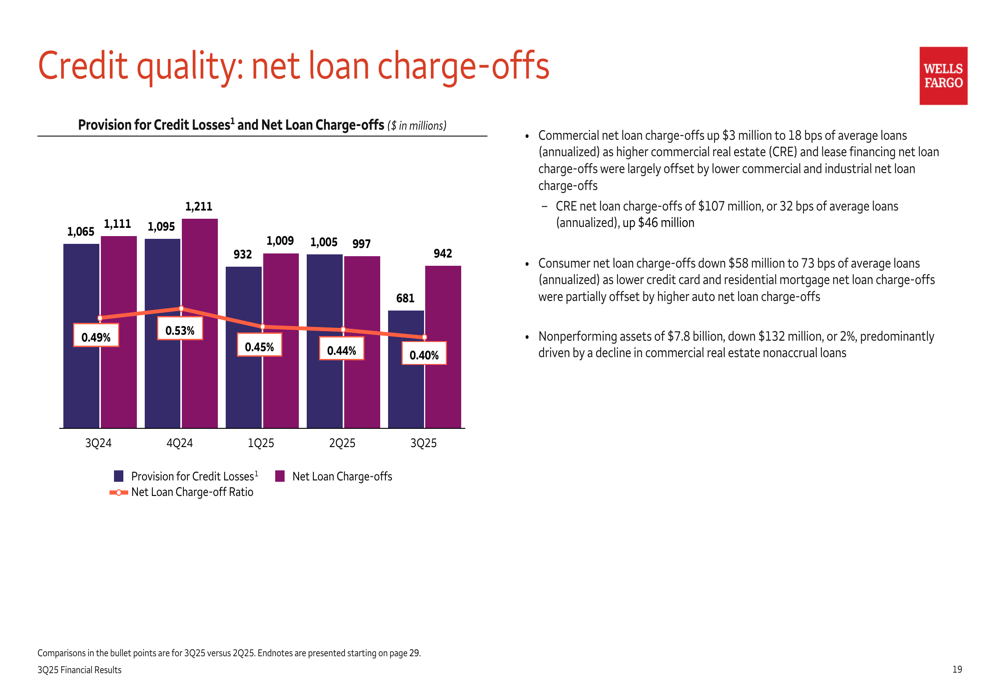

Credit quality remained solid, with nonperforming assets decreasing by $132 million to $7.8 billion. Commercial net loan charge-offs increased slightly by $3 million to 18 basis points of average loans, while consumer net loan charge-offs decreased by $58 million to 73 basis points of average loans.

Strategic Initiatives

Wells Fargo’s presentation highlighted its ongoing transformation through business simplification, expense reduction, and strategic investments. Since 2019, the bank has sold 12 businesses, including Asset Management, Corporate Trust Services, and its Student Lending portfolio, allowing it to focus on core strengths and improve efficiency.

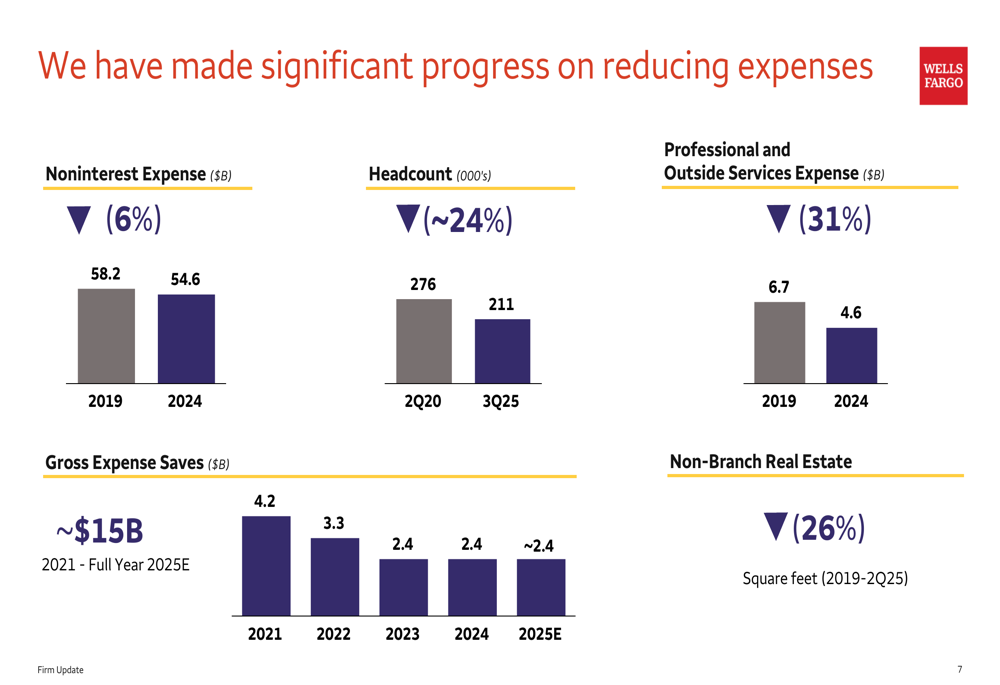

The bank has made significant progress in reducing expenses, with noninterest expense decreasing by 6% from $58.2 billion in 2019 to $54.6 billion in 2024. Headcount has been reduced by approximately 24%, from 276,000 in Q2 2020 to 211,000 in Q3 2025.

The following chart illustrates Wells Fargo’s expense reduction progress:

While streamlining operations, Wells Fargo has simultaneously invested in growth areas. The bank has diversified its revenue streams, with card fees increasing from $4.0 billion in 2019 to $4.3 billion in 2024, investment banking fees rising from $1.8 billion to $2.7 billion, and markets revenue growing from $4.8 billion to $6.9 billion.

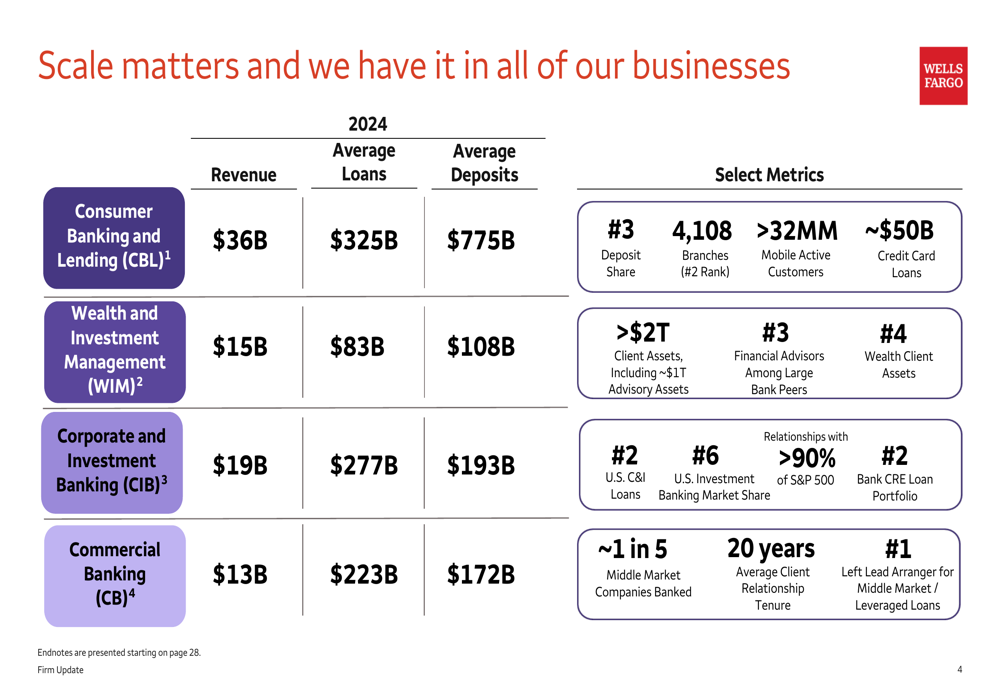

The presentation also emphasized the bank’s scale across its four main business segments: Consumer Banking and Lending, Wealth and Investment Management, Corporate and Investment Banking, and Commercial Banking. This scale provides competitive advantages in the U.S. financial services market.

As shown in the following image detailing the scale of Wells Fargo’s businesses:

CEO Charlie Scharf highlighted the transformative changes within Wells Fargo during the earnings call, stating, "Wells Fargo, without the regulatory constraints and with the changes we have made, is a significantly more attractive company than what we were several years ago." He described the company’s financial services franchise as "one of the most enviable in the world."

Forward-Looking Statements

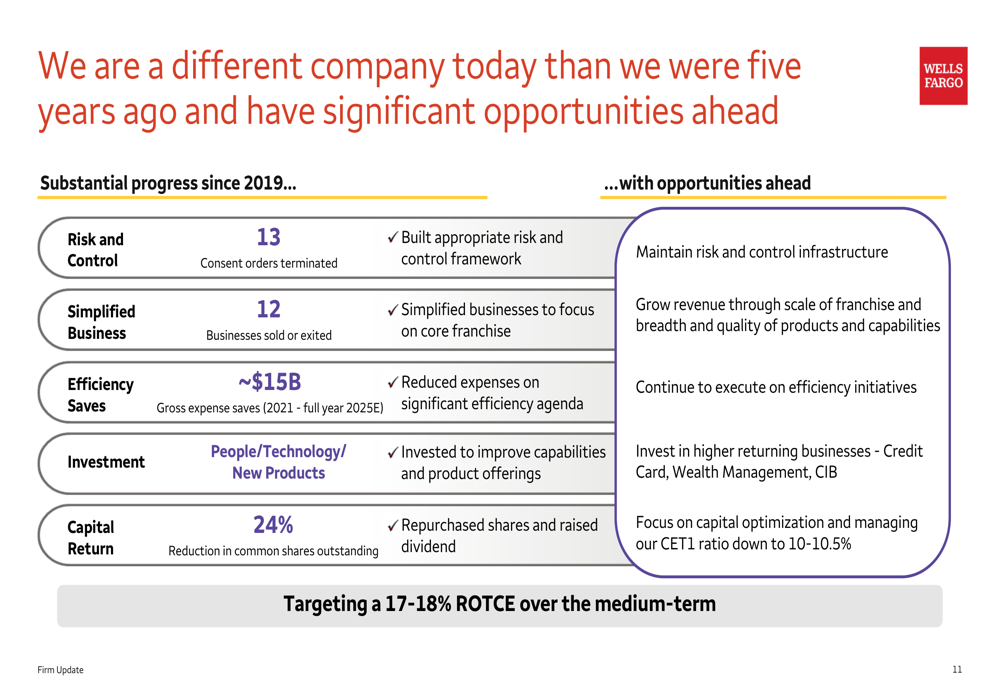

Wells Fargo is targeting a return on tangible common equity (ROTCE) of 17-18% over the medium term, up from 15% in 2025 year-to-date and significantly higher than the 8% reported in Q4 2020. The bank aims to achieve this through continued revenue growth, efficiency initiatives, and optimized capital management, targeting a CET1 ratio of 10-10.5%.

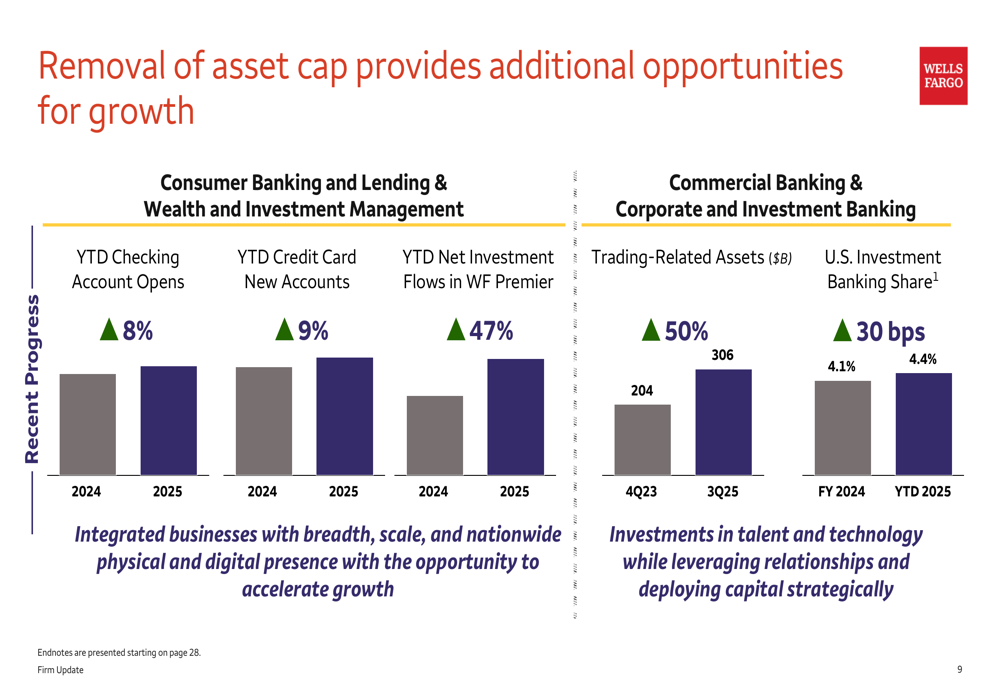

The bank’s progress and future opportunities are summarized in the following slide:

Looking ahead, Wells Fargo expects 2025 net interest income to be roughly in line with 2024’s $47.7 billion. The bank forecasts 2025 noninterest expense to be approximately $54.6 billion, up from prior guidance of $54.2 billion, primarily due to higher severance expenses of about $200 million and revenue-related compensation expenses of approximately $200 million, predominantly in Wealth and Investment Management.

The removal of the asset cap represents a significant growth opportunity for Wells Fargo. The bank has already seen positive momentum in this direction, with year-to-date checking account opens up 8%, credit card new accounts up 9%, and net investment flows in Wells Fargo Premier up 47%.

Wells Fargo’s capital position remains strong, with a Common Equity Tier 1 (CET1) ratio of 11.0% as of September 30, 2025. The bank completed $6.1 billion in gross common stock repurchases in Q3 2025, buying back 74.6 million shares, demonstrating its commitment to returning capital to shareholders.

Despite the positive outlook, Wells Fargo acknowledges that regulatory and compliance challenges continue to pose risks to its operations, along with economic uncertainties and potential interest rate fluctuations that could impact financial performance. The bank’s ability to achieve its targeted expense reductions and efficiency improvements remains crucial for reaching its medium-term ROTCE target.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.