Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

Xometry Inc (NASDAQ:XMTR) released its Q1 2025 earnings presentation on May 6, 2025, revealing accelerated growth and a significant profitability milestone. The digital manufacturing marketplace reported positive Adjusted EBITDA for the first time while posting strong revenue growth. Xometry’s stock, which closed at $27.50 on May 5, saw a 4.76% increase in premarket trading following the results, reaching $28.81.

The company’s performance demonstrates continued momentum following its strong Q4 2024 results, with marketplace revenue growth accelerating from Q4 levels. This growth comes amid Xometry’s expanding global footprint and increasing enterprise customer penetration.

Quarterly Performance Highlights

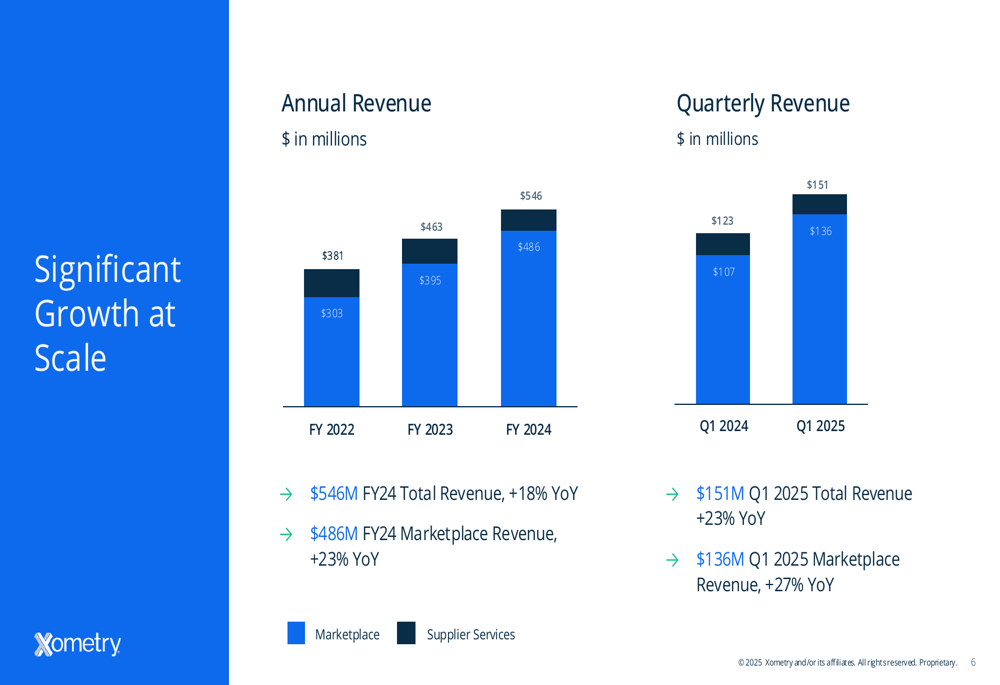

Xometry reported total revenue of $151 million for Q1 2025, representing a 23% year-over-year increase. Notably, marketplace revenue growth accelerated to 27% year-over-year, up from the previous quarter’s pace. The company achieved a positive Adjusted EBITDA of $0.1 million, marking a substantial $7.5 million improvement from the same period last year.

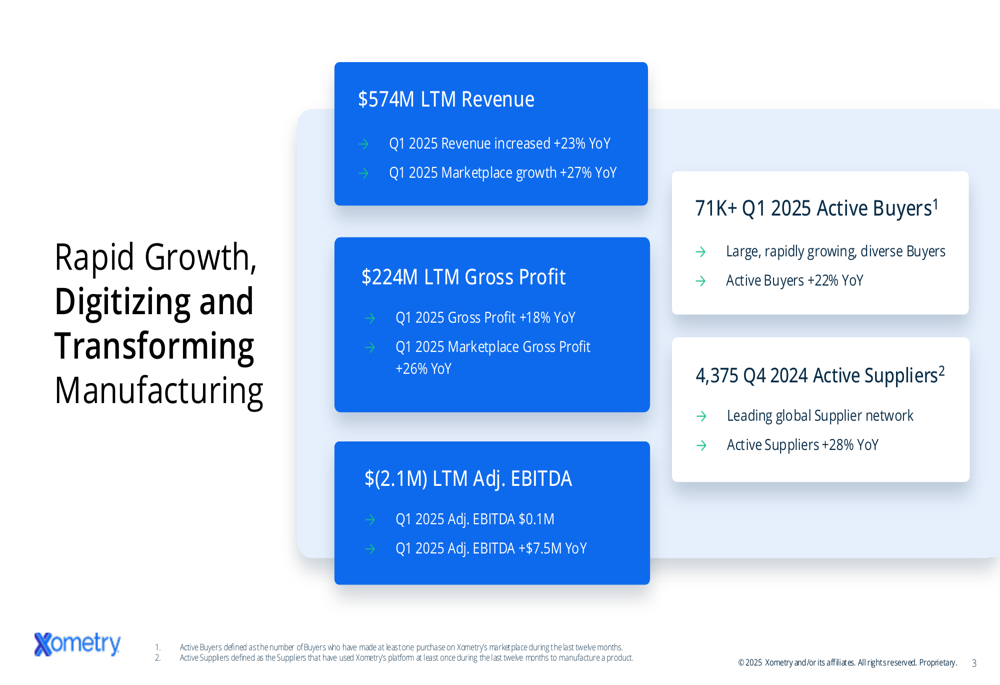

As shown in the following key metrics chart, Xometry continues to expand its network of buyers and suppliers:

Active buyers reached 71,454 in Q1 2025, increasing 22% year-over-year, while active suppliers grew to 4,375 by Q4 2024, up 28% year-over-year. The company’s last twelve months (LTM) revenue reached $574 million, with gross profit of $224 million over the same period.

The company’s revenue growth trajectory is clearly illustrated in this quarterly comparison:

Detailed Financial Analysis

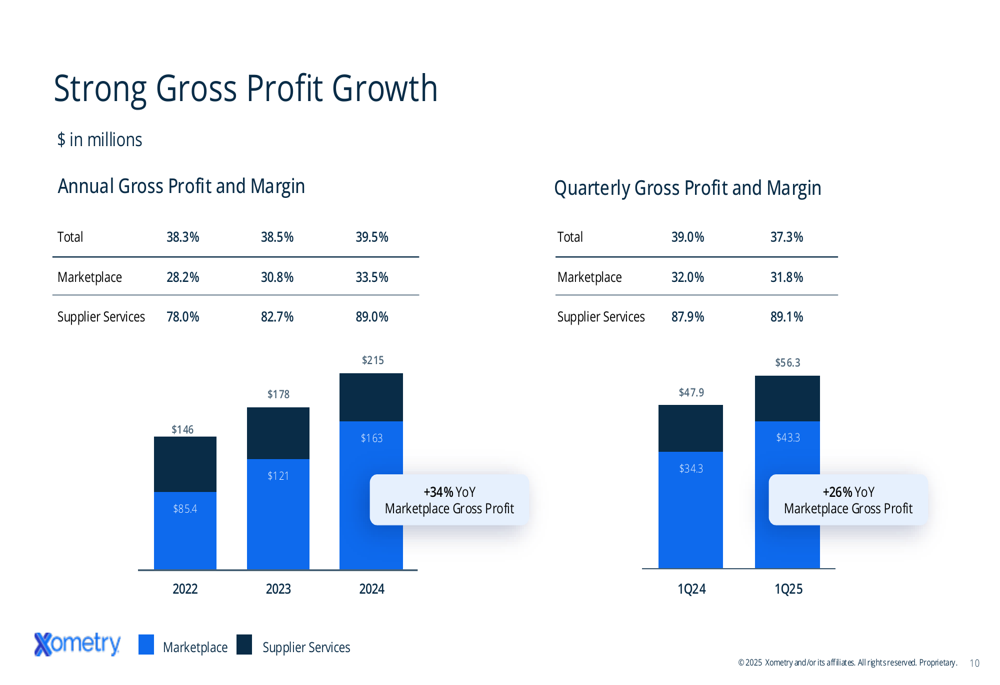

Xometry’s gross profit for Q1 2025 reached $56.3 million, an 18% increase year-over-year, driven by 26% marketplace gross profit growth. Marketplace gross margin was 31.8%, down slightly by 20 basis points year-over-year, which the company attributed to investments in its global sourcing strategy. Management expects significant margin improvement in Q2 2025.

The supplier services segment, which includes the Thomas advertising platform, maintained a strong gross margin of 89.1%. This segment continues to provide high-margin revenue, though the company expects supplier services revenue to decline approximately 5% year-over-year in FY 2025.

The following chart illustrates Xometry’s gross profit growth and margin trends:

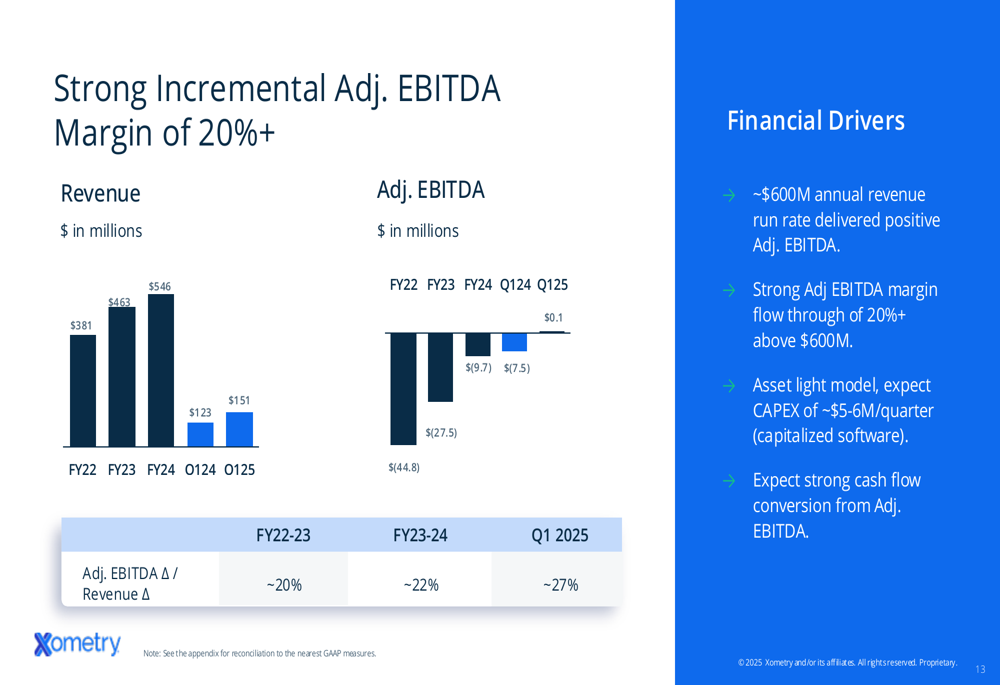

Operational efficiency improved significantly, with advertising spend as a percentage of marketplace revenue decreasing by 280 basis points year-over-year to 4.5%. Total (EPA:TTEF) non-GAAP operating expenses as a percentage of revenue declined to 37.3% in Q1 2025 from 41.5% in Q1 2024, demonstrating the company’s progress toward its long-term profitability goals.

The achievement of positive Adjusted EBITDA represents a key milestone in Xometry’s financial journey, as shown in this chart:

Strategic Initiatives

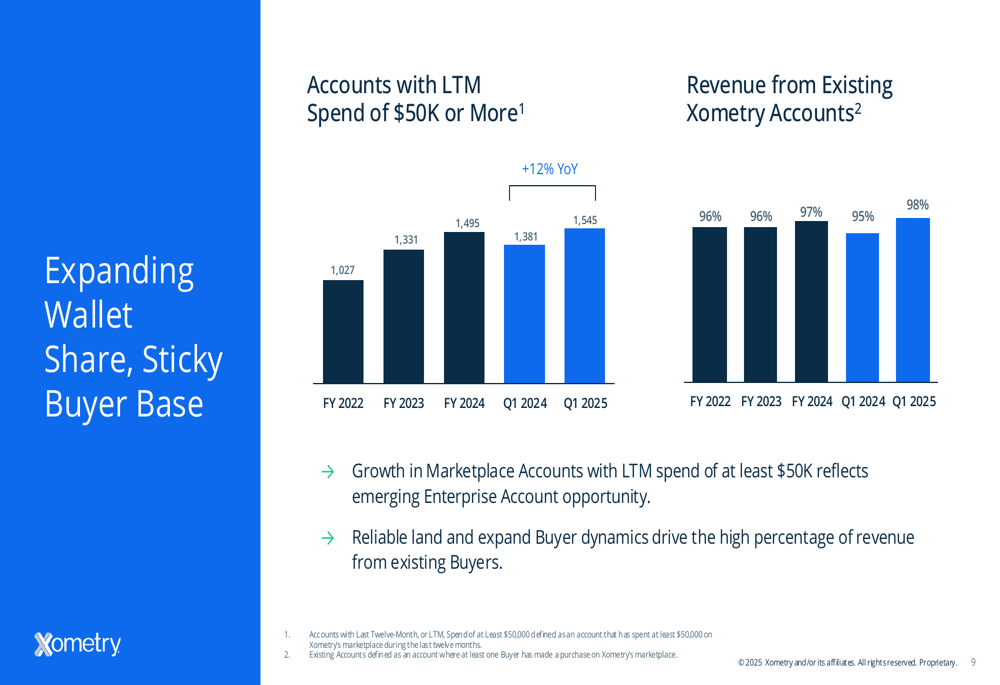

Xometry continues to focus on expanding its enterprise customer base. Accounts with last twelve months (LTM) spend exceeding $50,000 grew to 1,545 in Q1 2025, a 12% increase year-over-year. More impressively, accounts with LTM spend over $500,000 exceeded 100 in FY 2024 and grew revenue by more than 40% year-over-year.

The following chart demonstrates the company’s success in expanding wallet share among existing customers:

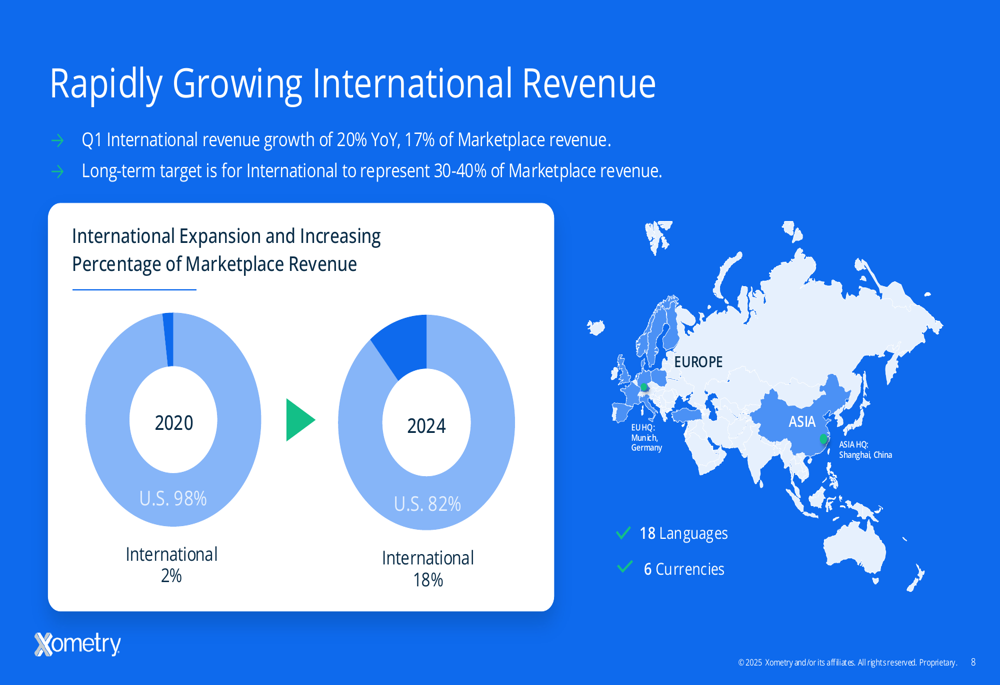

International expansion remains a key growth driver, with international revenue increasing 20% year-over-year in Q1 2025, representing 17% of marketplace revenue. Xometry aims for international markets to represent 30-40% of marketplace revenue in the long term. The company currently operates in 18 languages and 6 currencies, with headquarters in Munich, Germany for Europe and Shanghai, China for Asia.

As shown in this visualization of Xometry’s international growth:

The company is also leveraging its AI-driven platform to navigate tariff challenges. Xometry’s technology dynamically optimizes sourcing strategies, increases exposure for domestic suppliers, and mitigates cost increases by identifying competitive pricing across its global supplier network. The company’s pricing algorithms account for tariff changes with weekly updates to reflect changing costs.

Forward-Looking Statements

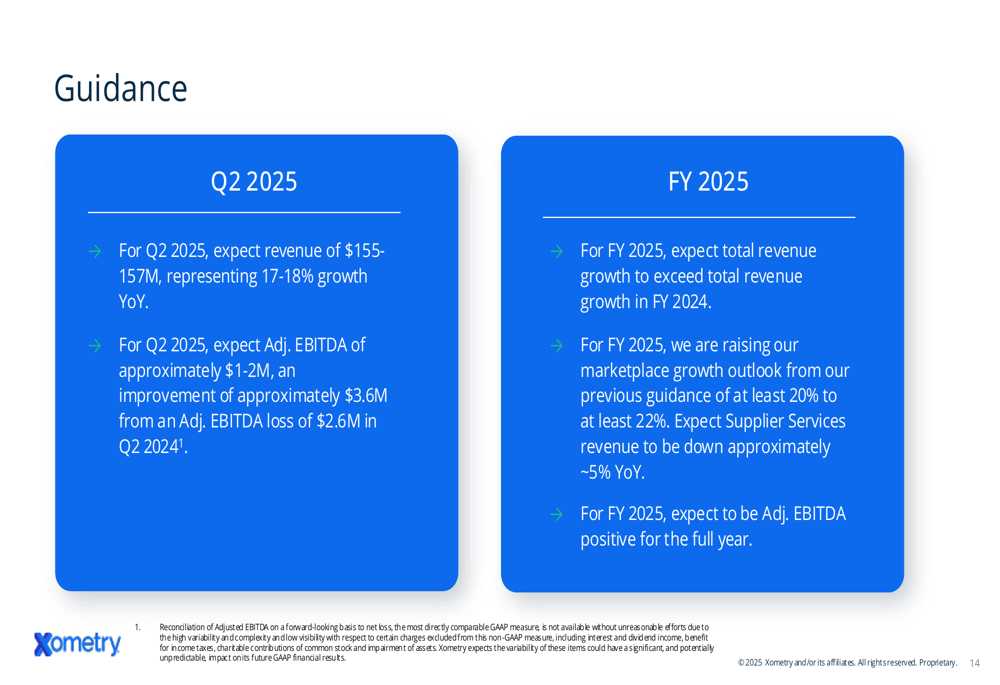

For Q2 2025, Xometry expects revenue of $155-157 million, representing 17-18% year-over-year growth. The company anticipates Adjusted EBITDA of approximately $1-2 million for Q2, an improvement of approximately $3.6 million from the $2.6 million loss in Q2 2024.

For the full year 2025, Xometry has raised its marketplace growth outlook from at least 20% to at least 22%. The company expects to be Adjusted EBITDA positive for the full year, a significant improvement from the $27.5 million Adjusted EBITDA loss in FY 2024.

The guidance reflects management’s confidence in Xometry’s growth strategy and path to profitability:

Xometry’s long-term strategy focuses on expanding buyer and supplier networks, driving deeper enterprise engagement, further expanding its marketplace platform, and growing internationally. The company targets long-term gross margins of 40-45%, operating expenses of 15-20% of revenue, and Adjusted EBITDA margins of 20-30%.

As illustrated in this strategic roadmap:

With less than 1% penetration of its addressable market and a strong competitive moat built on its AI-enabled technology platform, Xometry appears well-positioned for continued growth. The company’s asset-light business model, with minimal capital expenditure requirements, should support improved cash flow conversion as it scales toward its target of $1 billion in revenue.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.