TSX lower as gold rally takes a breather

Introduction & Market Context

YETI Holdings Inc (NYSE:YETI) reported a 4% decline in second-quarter sales but raised its full-year guidance, suggesting confidence in a stronger second half of 2025. The premium cooler and drinkware maker’s stock jumped 4.31% in premarket trading to $38 following the presentation, reflecting investor optimism about the improved outlook despite near-term challenges.

The company’s Q2 results come amid ongoing efforts to diversify its supply chain and expand internationally, with management previously describing 2025 as a "transition year." YETI continues to navigate tariff headwinds while pursuing its strategic shift toward direct-to-consumer channels and global expansion.

Quarterly Performance Highlights

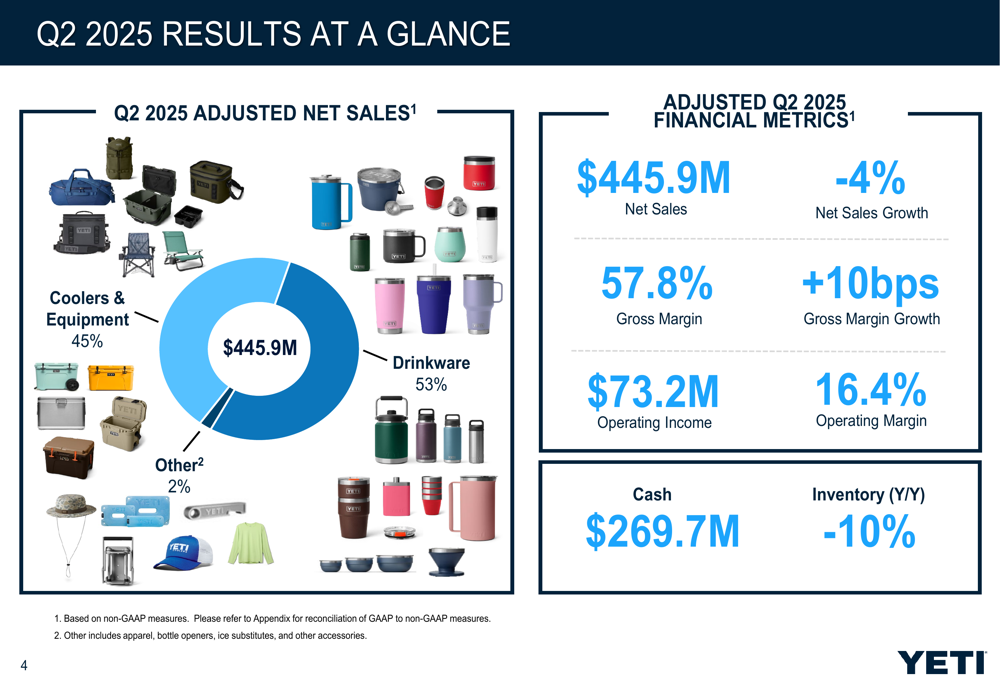

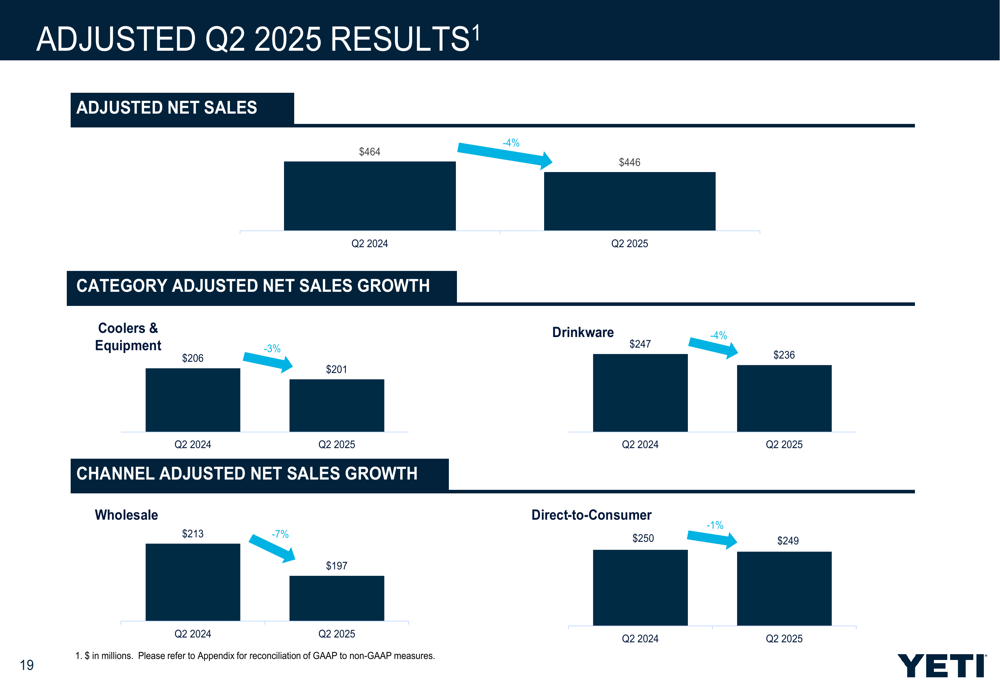

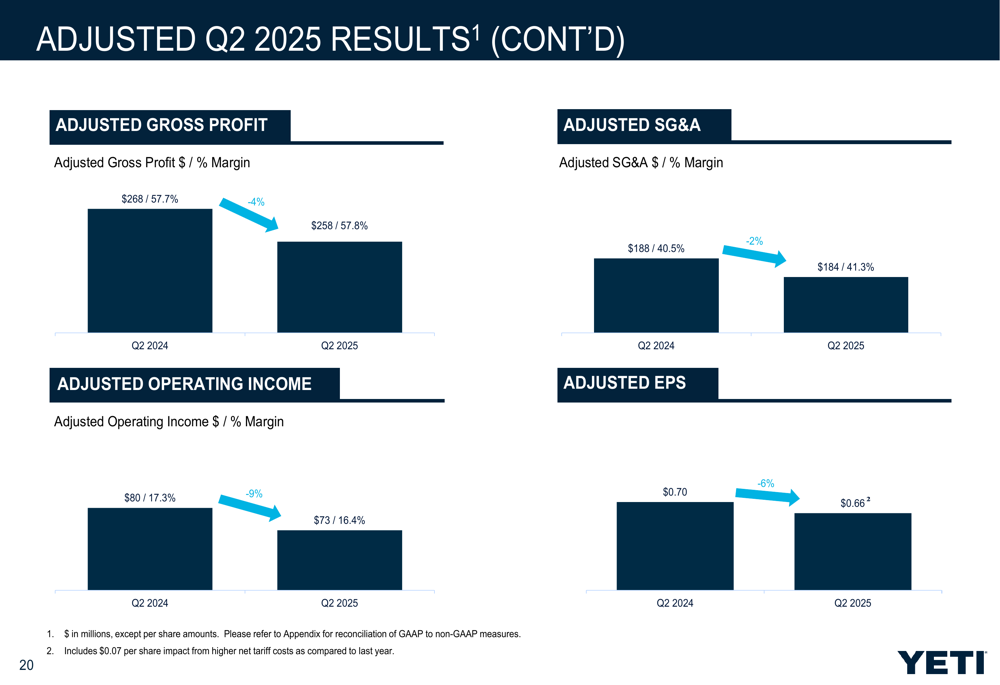

YETI reported adjusted net sales of $445.9 million for Q2 2025, down 4% from $464 million in the same period last year. Despite the revenue decline, the company maintained its gross margin at 57.8%, a slight improvement of 10 basis points year-over-year.

As shown in the following chart of YETI’s Q2 financial performance:

By product category, Coolers & Equipment sales declined 3% to $201 million, while Drinkware sales fell 4% to $236 million. The company’s channel performance showed a more pronounced decline in wholesale (down 7% to $197 million) compared to direct-to-consumer (down 1% to $249 million).

The detailed breakdown of Q2 sales performance by category and channel is illustrated here:

Profitability metrics showed some pressure, with adjusted operating income decreasing 9% to $73.2 million and operating margin contracting to 16.4% from 17.3% in the prior year. Adjusted earnings per share fell 6% to $0.66, including a $0.07 per share impact from higher net tariff costs.

Strategic Initiatives

YETI continues to execute on its long-term strategic priorities, with particular emphasis on expanding its customer base, introducing new products, accelerating direct-to-consumer sales, and growing internationally.

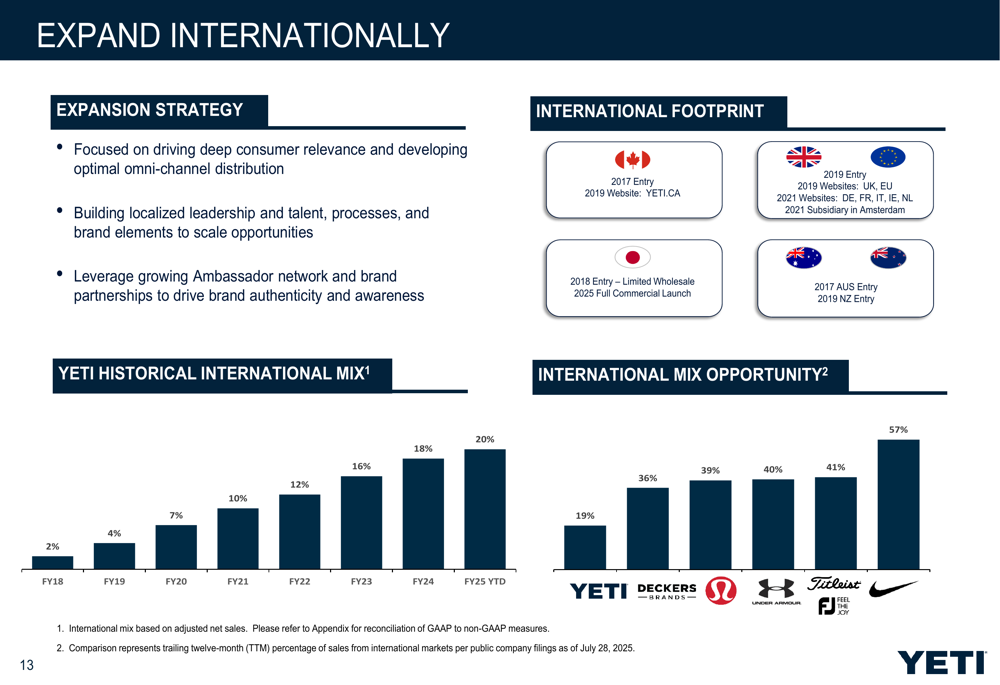

The company’s international expansion remains a key growth driver, with international sales now representing approximately 20% of total revenue in fiscal year 2025 to date. YETI is focusing on building consumer relevance and developing optimal omni-channel distribution across key markets including the UK, Europe, Canada, Australia, and Japan.

The following map illustrates YETI’s expanding global footprint:

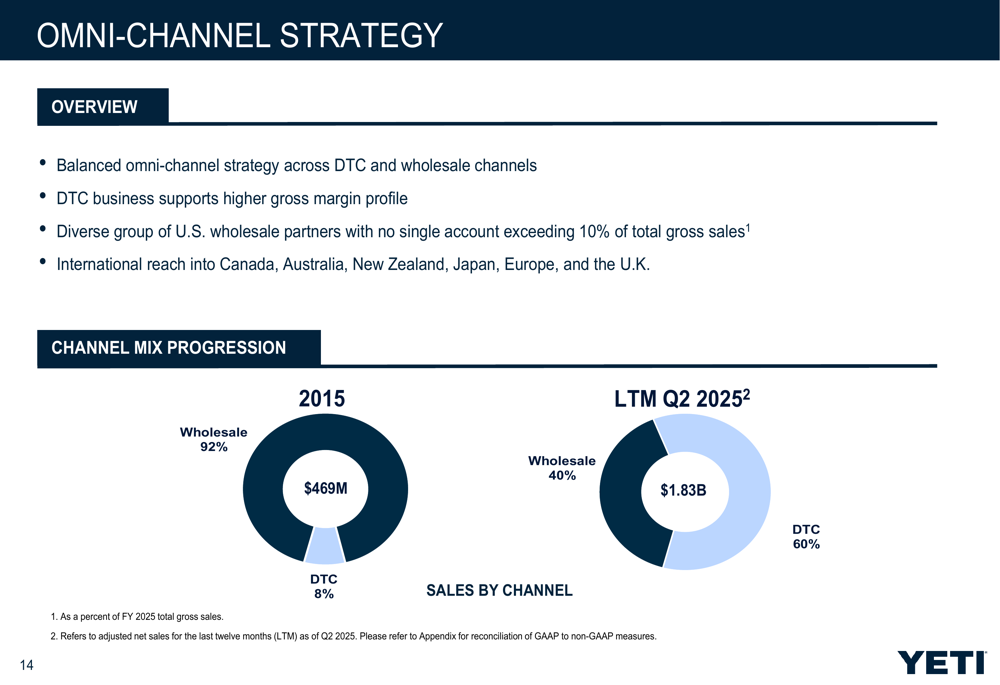

A cornerstone of YETI’s strategy has been its dramatic shift from a wholesale-dominated business to a more balanced omni-channel approach. As shown in the chart below, direct-to-consumer channels now account for 60% of sales (for the last twelve months ending Q2 2025), compared to just 8% in 2015. This transformation has supported higher gross margins while providing greater control over the customer experience.

Product innovation remains central to YETI’s growth strategy. Recent launches include the Cayo backpack, expanded "Outdoor Kitchen" product assortment with insulated food jars, and the Hondo beach chair. The company has also expanded its community reach beyond its traditional hunting and fishing base to include 15 distinct communities ranging from culinary and beverage to wellness and sports, supported by 213 brand ambassadors.

Forward-Looking Statements

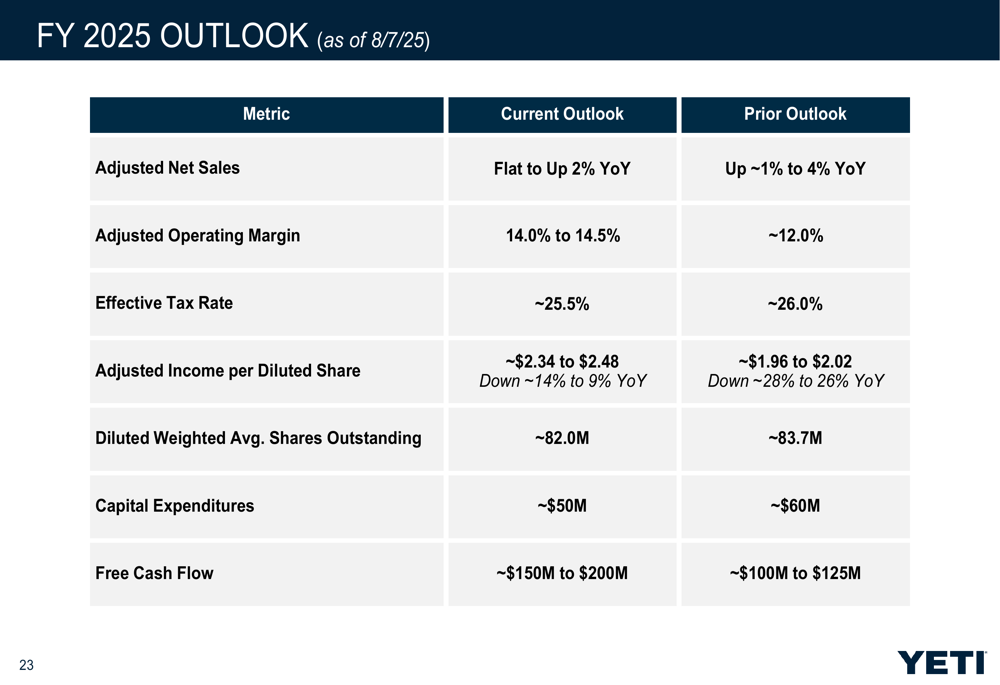

In a significant vote of confidence for the second half of 2025, YETI raised its full-year guidance across multiple metrics. The company now expects:

- Adjusted net sales to be flat to up 2% year-over-year (previously forecast at up 1-4%)

- Adjusted operating margin of 14.0% to 14.5% (improved from previous guidance of ~12.0%)

- Adjusted earnings per diluted share of $2.34 to $2.48 (substantially higher than prior outlook of $1.96 to $2.02)

- Free cash flow of $150-200 million (up from previous guidance of $100-125 million)

The following slide details the current outlook compared to previous guidance:

This improved outlook comes despite the company slightly lowering its sales growth expectations, suggesting significant operational efficiency improvements and cost control measures are taking effect. The substantial increase in EPS guidance (from a maximum of $2.02 to a new range topping out at $2.48) represents a nearly 23% improvement at the high end.

Detailed Financial Analysis

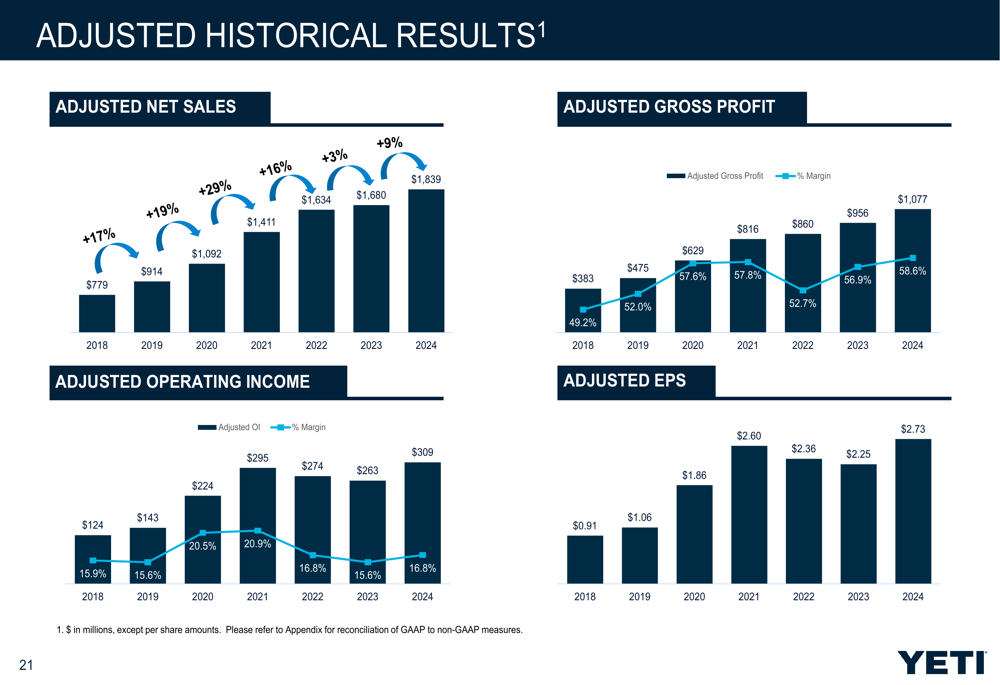

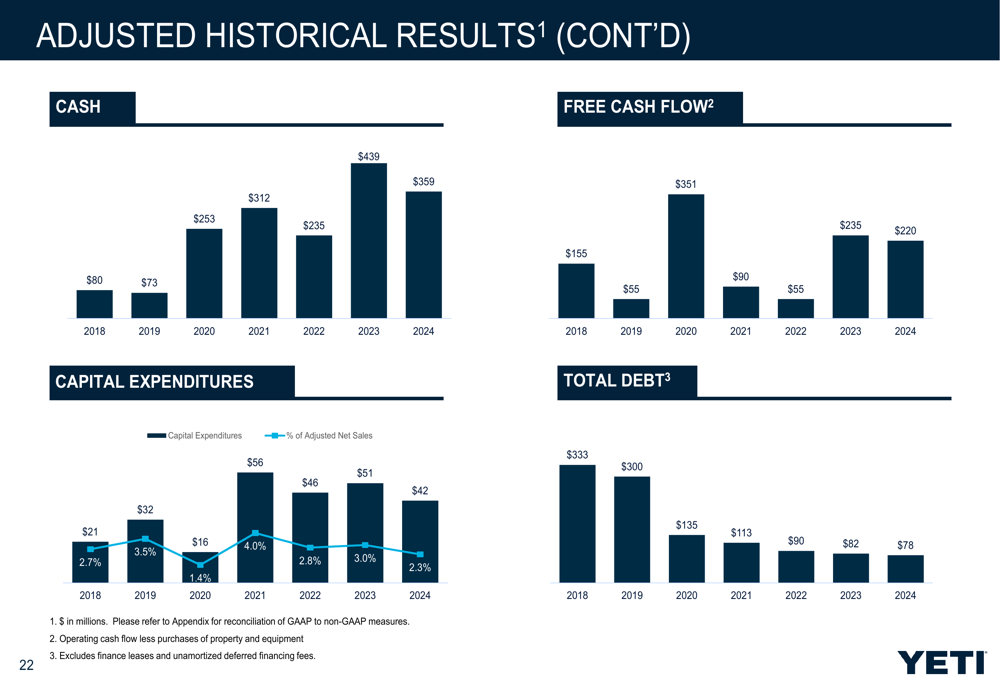

Looking at YETI’s historical performance, the company has maintained a strong growth trajectory over the past several years, though recent quarters have shown some moderation. The charts below illustrate YETI’s financial evolution from 2018 through 2024:

The company’s balance sheet and cash flow metrics remain healthy, with $269.7 million in cash as of Q2 2025 and inventory levels down 10% year-over-year, indicating improved operational efficiency and working capital management.

Conclusion

YETI’s Q2 2025 results present a mixed picture: near-term sales pressure offset by margin resilience and a significantly improved outlook for the full year. The company appears to be successfully navigating the challenges of its supply chain transformation and tariff headwinds while continuing to execute on its strategic priorities.

The raised guidance suggests management sees the current sales weakness as temporary rather than structural, with expectations for improved performance in the second half of the year. Investors appear to share this optimism, as evidenced by the stock’s premarket gains.

For YETI, 2025 continues to be a year of strategic transformation, balancing short-term challenges with long-term growth opportunities in international markets, direct-to-consumer channels, and product innovation. The company’s ability to maintain healthy margins and raise its earnings outlook despite sales pressure demonstrates operational resilience during this transition period.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.