HSBC downgrades Bloom Energy after significant rally

Introduction & Market Context

Admicom Oyj (HEL:ADMCM) presented its Q1-Q3 2023 results on October 5, showcasing the company's performance amid challenging conditions in the construction sector. The Finnish software provider is navigating a difficult market environment characterized by increasing insolvencies and halted construction projects, while simultaneously executing a strategic shift from a multi-sector ERP provider to a specialized construction technology (ConTech) company with European ambitions.

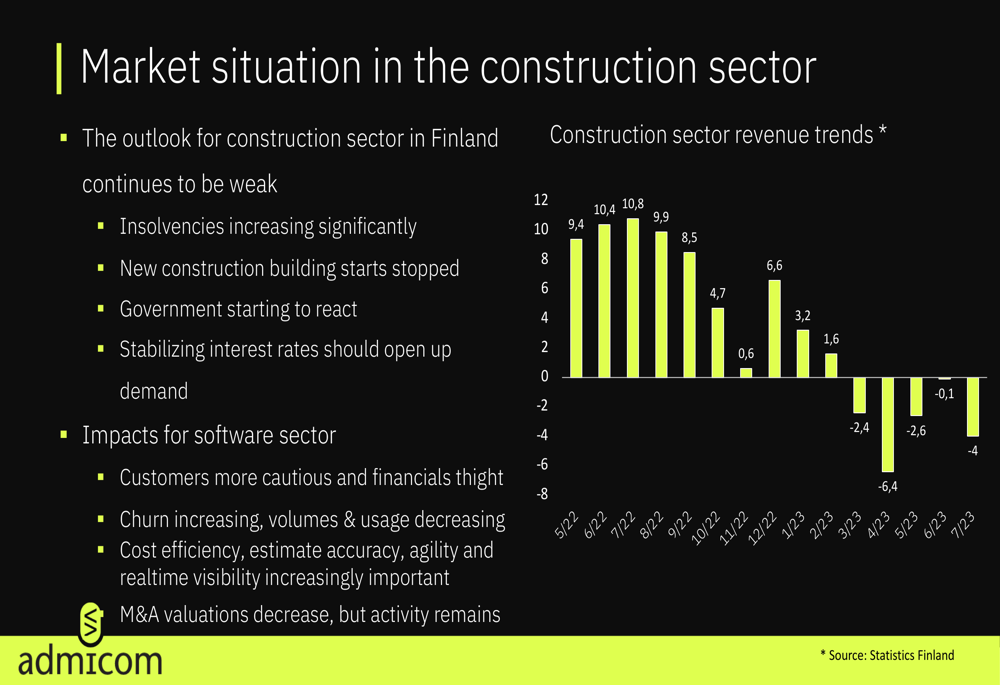

The construction market outlook remains weak, with government intervention beginning to emerge and the potential for stabilizing interest rates to eventually stimulate demand. These market conditions have created a cautious customer base for Admicom, leading to increased churn and heightened focus on cost efficiency.

As shown in the following chart of construction sector revenue trends, the industry has experienced significant volatility, declining from 9.4 in May 2022 to just 0.1 in July 2023, with a negative peak of -6.4 in April 2023:

Quarterly Performance Highlights

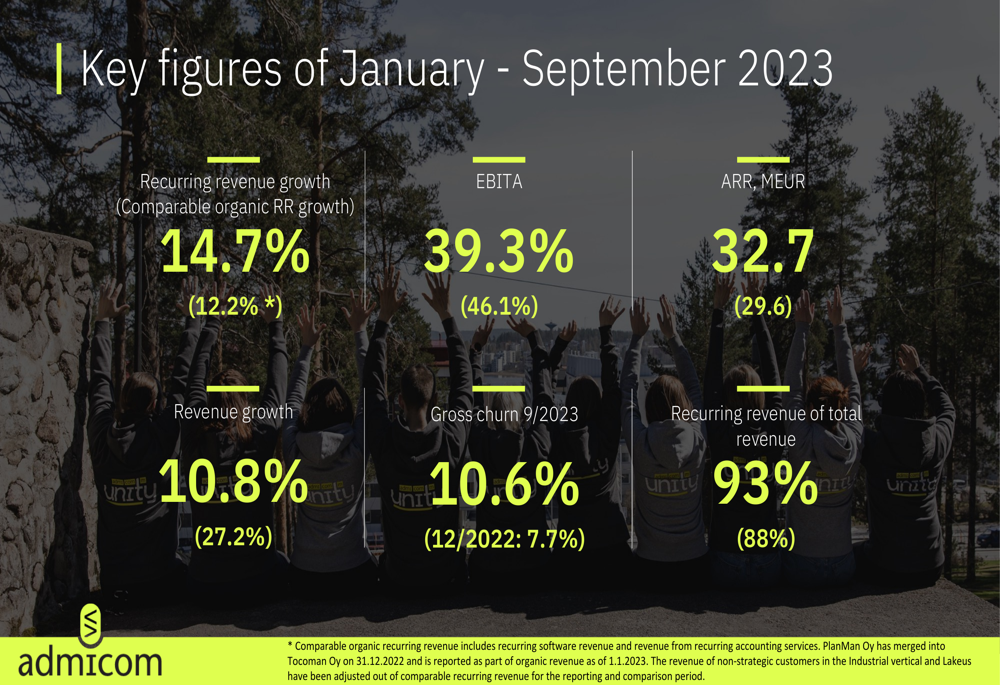

Despite market headwinds, Admicom reported solid recurring revenue growth of 14.7% for the January-September 2023 period, with comparable organic recurring revenue growth at 12.2%. The company's Annual Recurring Revenue (ARR) reached €32.7 million, up from €29.6 million in the previous period. Notably, recurring revenue now comprises 93% of total revenue, an increase from 88% previously.

The comprehensive financial overview for the first nine months of 2023 is illustrated in this key metrics summary:

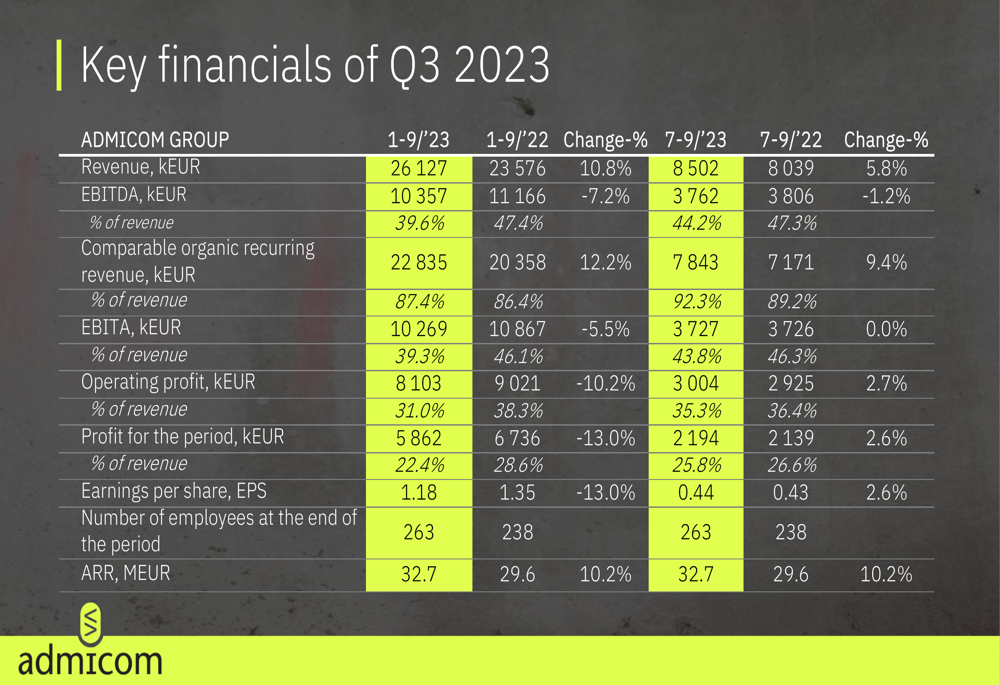

However, profitability metrics show signs of pressure, with EBITA margin declining to 39.3% from 46.1% in the comparison period. The company's Q3 2023 revenue growth was 6%, with organic new sales contributing 5% and annual fee adjustments adding 1%. The EBITDA margin for Q3 stood at 44%, representing a 3 percentage point decrease from the comparison period.

The detailed quarterly financial data reveals the specific performance metrics across key indicators:

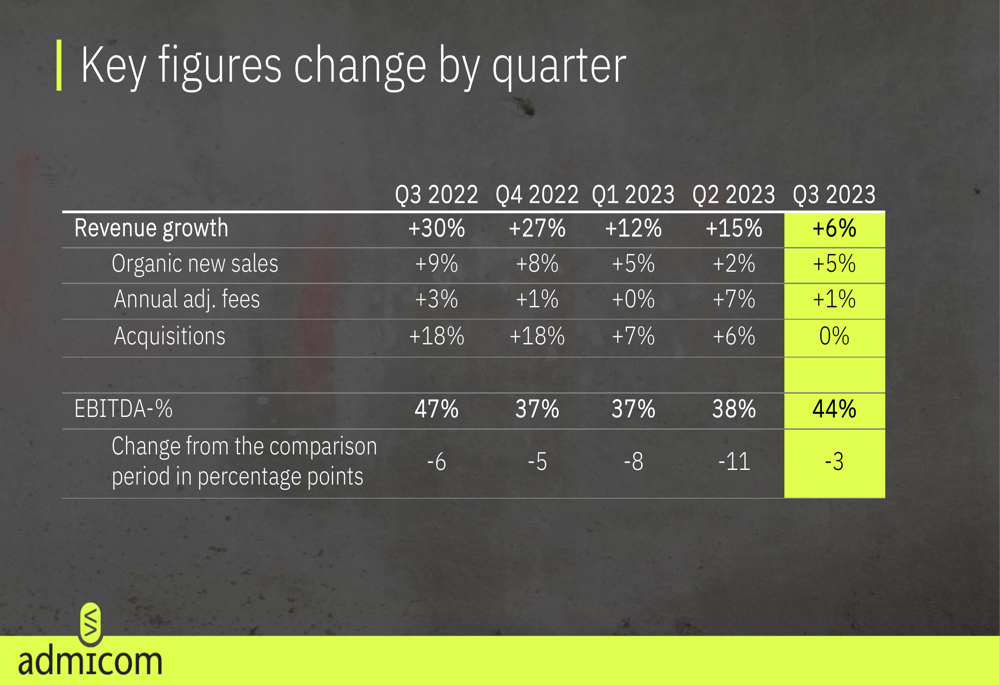

The quarter-by-quarter progression shows how Admicom's growth and profitability metrics have evolved throughout 2022 and 2023:

A concerning trend is the increase in gross churn, which rose to 10.6% as of September 2023, up from 7.7% in December 2022. This reflects the challenging market conditions in the construction sector, with Admicom noting that insolvencies have contributed to customer losses.

Strategic Initiatives

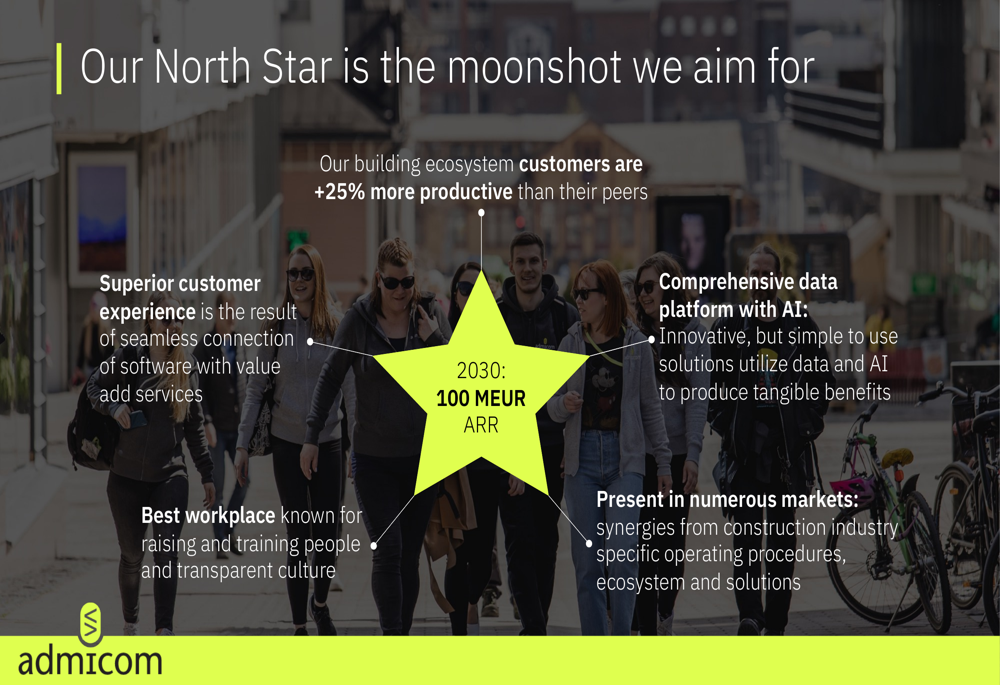

Admicom is executing a strategic transformation from a multi-sector ERP software provider to a specialized construction technology company. The company has articulated a clear vision to become the "First choice of partner in the European construction software ecosystem," with a long-term ambition to reach €100 million in ARR by 2030.

The company's strategic roadmap is guided by three principles: "Winning customer experience," "Simple innovations," and "Transparently agile." Concrete steps already taken include clarifying the operating model and governance, making growth investments into joint operating practices, deinvesting non-standard Lakeus accounting clients, and investing approximately €1 million in R&D for 2023.

The company's ambitious long-term vision is captured in its "North Star" strategy:

On the operational front, Admicom has merged the sales organizations of Tocoman and Kotopro, launched a new cost estimation software for SMEs, and appointed Satu Helamo as the new CFO effective October 9, 2023. The company has also moved its R&D to a fully agile methodology and initiated its first international pilot.

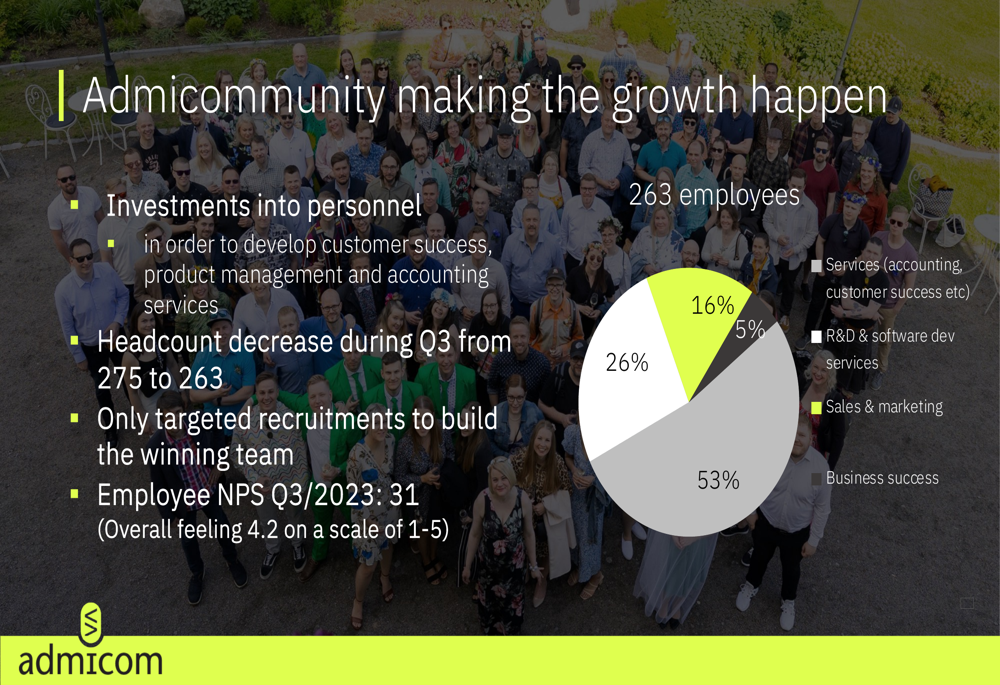

The company's workforce composition reflects its business priorities, with 53% of employees focused on business success and 26% on sales and marketing:

Forward-Looking Statements

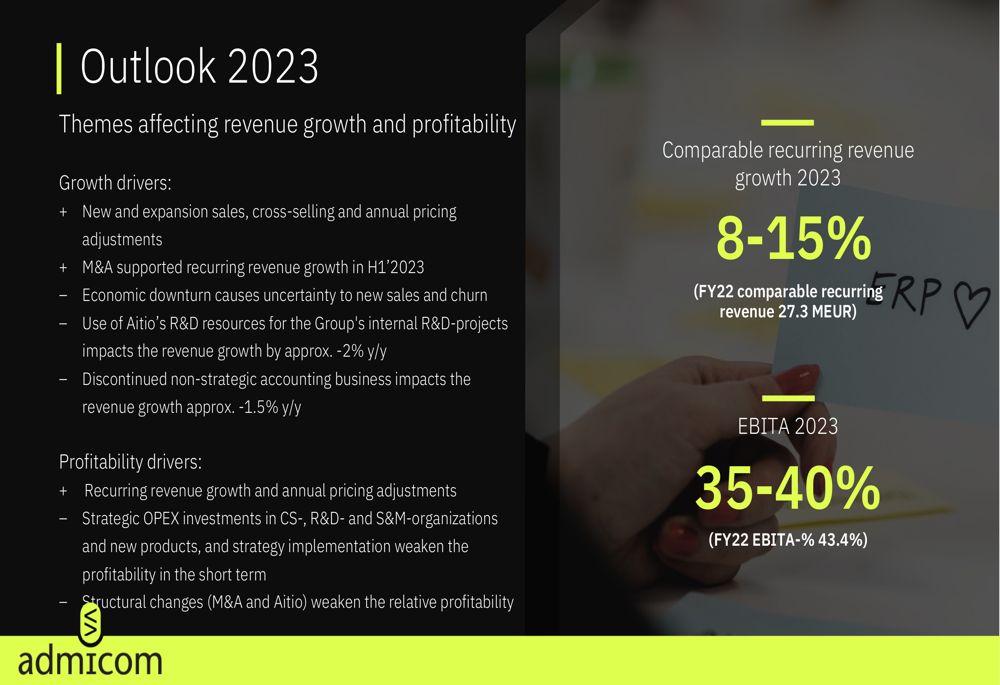

For the full year 2023, Admicom has provided guidance for comparable recurring revenue growth of 8-15% (based on FY22 comparable recurring revenue of €27.3 million) and an EBITA margin of 35-40% (compared to 43.4% in FY22). This outlook reflects both growth opportunities and margin pressures in the current market environment.

The company's near-term priorities focus on efficient sales, churn prevention, and cost control, while medium-term initiatives include finalizing a joint brand and culture, implementing the product suite vision, planning international go-to-market strategies, developing an AI strategy with initial implementations, and exploring further M&A opportunities.

Admicom's investment case centers on its foundation in the construction software space, the significant long-term potential in ConTech, its comprehensive cloud SaaS suite, and solid financials and governance. While current market conditions present challenges, the company's strategic pivot positions it to potentially capitalize on the digitalization of the construction industry across Europe, with a clear ambition to grow its ARR to €100 million by 2030.

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.