Sign up to create alerts for Instruments,

Economic Events and content by followed authors

Free Sign Up Already have an account? Sign In

Please try another search

Economic headlines were filled with talk of another "bottom" for the US dollar, reinforcing the bearish sentiment that took hold earlier in the year. The stock market's performance was mixed. After a sharp dip on "Liberation day," indices managed to trim their losses and inch closer to all-time highs.

In contrast, Germany's DAX hit a new record before pulling back, while both the Nasdaq and S&P 500 also neared their previous peaks.

On the inflation front, the US saw stability, and the labor market remained resilient. This led to a shift in market expectations around rate cuts. What was once seen as a likely rate cut in June now looks set for September, with two cuts expected by the end of 2025.

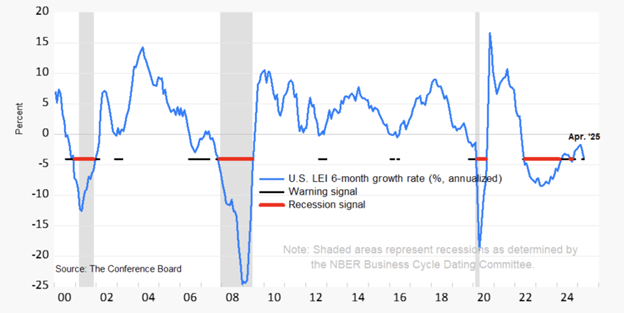

Meanwhile, the US economy showed signs of slowing in April, with the leading economic index (LEI) dropping to levels typically associated with recessions. While it's not a full recession yet, the drop signals growing uncertainty, particularly around tariffs and their potential impact on global growth.

Havens

The most notable recent development in currency markets was migration of capital to havens despite low yields. For example, the yen held relatively well, as did the franc. The latter did not react after the SNB’s rate declined to zero and below. Positions of speculators visible on COT reports have reached long-term highs for both yen and franc futures.

That, in a normal situation, might serve as a sign of overheated conditions, but in our particular case, this condition seems stable in the intermediate to long term. Global demand for havens is high.

Geopolitical situation

The geopolitical landscape acted as a trigger for immediate volatility, but rarely caused massive liquidations or sustainable rallies. The main event in focus was the escalation between Israel and Iran, and oil prices spiked above $70 (with a peak in early June of $75). However, the reaction was softer than many participants had anticipated: After the initial gap, prices started to consolidate rather than to develop a clear ongoing uptrend, but this situation is still developing at the time of writing.

Negotiations between Russia and Ukraine haven’t made substantial progress. A cementing situation there is probably more likely than escalation with additional conflict in the Middle East contributing to global uncertainty.

Potential narratives for Q3 2025

Havens might be on thin ice, so potential declines for the yen and franc are on the radar of traders: any weaker economic data published by the related countries might lead to pressure for these havens.

Tariffs are in focus: before the situation with tariffs clarifies (to the extent that analysts can build forecasts), carry trade operations probably won’t extend. If the carry trade returns to clear focus, CHF and JPY might decline.

Bitcoin shows decent resilience, pointing to bullish conditions according to MVRV indicator, MVRV pricing bands and other similar on-chain metrics.

Gold

The second quarter of 2025 was highly active for gold with the metal completing its widest monthly range in history in April. As in the first quarter, gold was one of the most positively affected instruments from the chaotic implementation then walkback of sweeping American tariffs in April, reaching an all-time intraday high of $3,500 on 22 April.

As noted in the overview, havens have generally gained as a result of the Israeli-Iranian war as well as trade disruptions caused by the American government’s flip-flopping and confused rhetoric regarding trade policy. However, gold was certainly the biggest winner among the three traditional havens since the yen and franc were held back somewhat by loose monetary policy. The likelihood of a recession is still uncertain as discussed in the overview above, but overall the American economy definitely looks weaker.

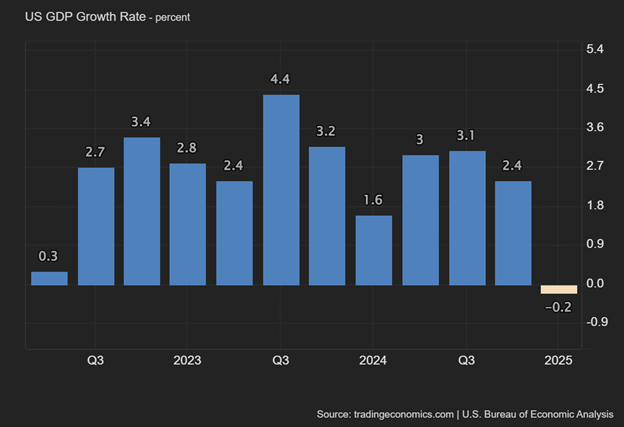

The first quarter of 2025 saw the first quarterly contraction of American GDP in three years. Meanwhile inflation remains above target although it and the labor market seem to have stabilized. Data in general suggest that the Fed’s right to be cautious: there’s no pressure to cut as soon as possible but a sustained resurgence of inflation and rates rising again this cycle seem progressively more unlikely as time goes on.

Conversely, monetary policy definitely took a backseat last quarter to tariffs and the Israeli-Iranian war. That might change in the next few months as speculation about Jerome Powell’s possible replacement increases in the runup to his second term ending in May next year.

Now that the focus has shifted onto the war in June, more big news about tariffs seems less likely immediately, but it’s very difficult to predict how the current military and diplomatic situation might resolve. Direct military intervention by the USA or possibly other countries seems to be less probable as time goes on unless Israel’s missile defenses show clear signs of buckling.

Based on May and June specifically, it’s possible that the main uptrend has paused or even finished and the current trend is sideways, but confirmation should be sought from the next attempt on $3,500, if any. Volume declined significantly in the last two months relative to the peak in the first half of April.

The 50 SMA from Bands is a very clear dynamic support with bounces having occurred from this area four times last quarter. Possible escalation of the Israeli-Iranian war and disruption in the Gulf as discussed below in the section on oil might have a strong positive effect on the price of gold.

Otherwise, the price might settle into a sideways trend: continuation of the main uptrend is also possible but seems less obvious than this time last quarter. Any continuation would probably feature lower momentum than early in the second quarter unless strong new fundamental drivers develop.

Oil

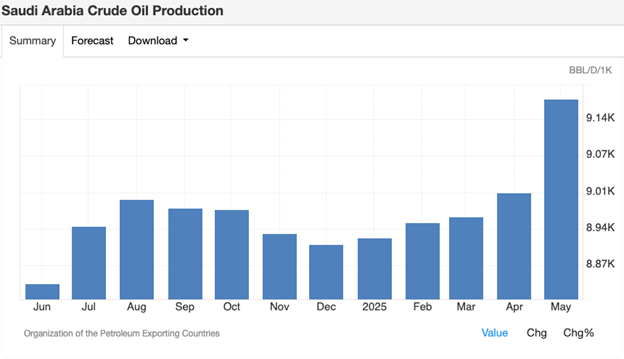

Supply from Saudi Arabia saw a steady rebound in early 2025, rising from a low of approximately 8.87mbd in December 2024 to just over 9mbd by April and surging to around 9.150mbd in May. This marks the highest monthly output in nearly a year, indicating a clear shift as Riyadh gradually unwinds voluntary cuts and responds to markets’ signals.

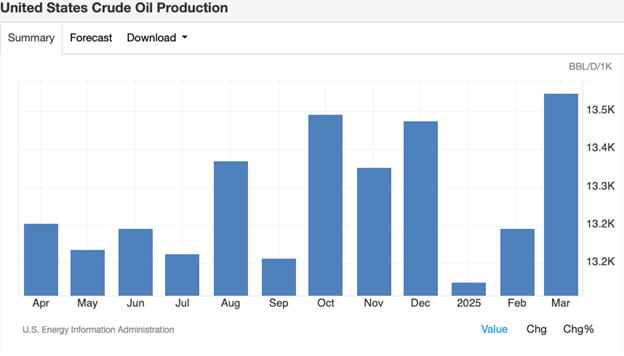

This uptick aligns with broader global trends — total supply rose by 330,000bd in May, split between OPEC+ and non-OPEC+ producers. Although OPEC+ announced a phased rollback of voluntary cuts, actual volumes might trail nominal figures, with logistical and political friction limiting real-time increases. Meanwhile, the US remains the primary engine of growth, hitting record production and expected to lead 2025’s supply expansion.

At the same time, the market remains on edge due to ongoing uncertainty around OPEC+’s coordination, wars, and macroeconomic drag from tariffs and slowing global growth.

Global demand is expected to grow by 720,000bd in 2025, slightly below projections earlier in the second quarter. Looking ahead to 2026, growth in demand might increase slightly to 740,000bd despite possible economic headwinds, the ongoing shift to clean energy and caps on consumption according to the International Energy Agency.

This growth is primarily driven by escalations in geopolitical tensions, which for the time being don’t seem to be anywhere close to ending. The Israeli-Iranian war specifically could disrupt major supply lines for around 20-30% of all production, potentially boosting the price of oil.

From the technical point of view, the price of oil had been in a sideways channel for the majority of the second quarter between $56 and $64. The recent attacks by Israel on Iran caused immense volatility with the price trading above the upper band of the Bollinger Bands and pushing the Stochastic oscillator into extreme overbought levels.

Despite the aggressive gains, the moving averages are not yet validating a complete reversal. The 50-day moving average is still below the 100. On the other hand, one might argue that the 50-day is on the move to cross above the 100 in the upcoming sessions, but this has not happened yet, and a consolidation or retracement in the short term might prevent the crossing from happening altogether.

The price is currently around $74, which is an inside resistance area of reaction in early February, whereas the medium-term high of $79 seems to be the major technical resistance for the time being. If the price moves down, the first area of possible support might be around $70, a psychological area and an area of reaction in late March.

The information on this material is provided for information purposes only and should not be construed as containing investment advice or an offer of solicitation for any transactions in financial instruments. Neither the presenter nor Exness takes into account your personal investment objectives or financial situation and assumes no liability to the accuracy, timeliness or completeness of the information provided, nor for any loss arising from any information supplied. Any opinions made throughout the presentation are strictly personal to the presenters and may not reflect the opinions of Exness. Past performance does not guarantee or predict future performance. Seek independent advice if necessary. The information on this material may only be copied with the express written permission of Exness.