TSX gains after CPI shows US inflation rose 3%

Introduction & Market Context

Allegion (NYSE:ALLE) presented its third-quarter 2025 earnings results on October 23, showcasing strong performance across its business segments. The security products manufacturer saw its stock rise 3.88% following the announcement, reflecting positive market reception to the company’s financial results and improved outlook.

The company continues to navigate a complex market environment, balancing strong non-residential demand with softer residential markets, while managing inflationary pressures and tariff impacts. Despite these challenges, Allegion has maintained its growth trajectory through strategic pricing actions, volume growth, and acquisitions.

Quarterly Performance Highlights

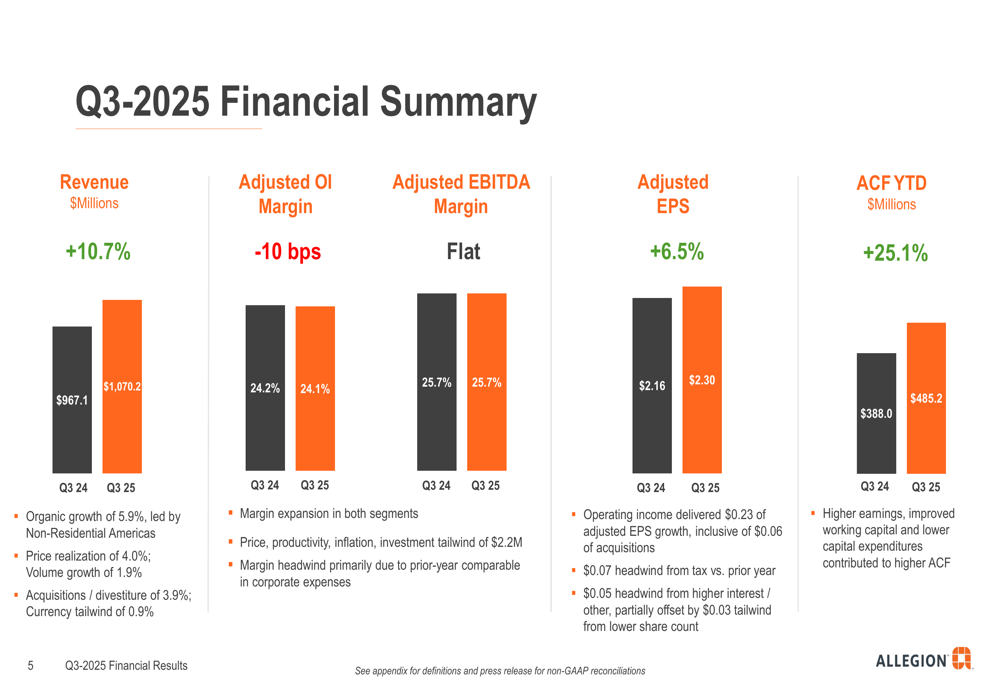

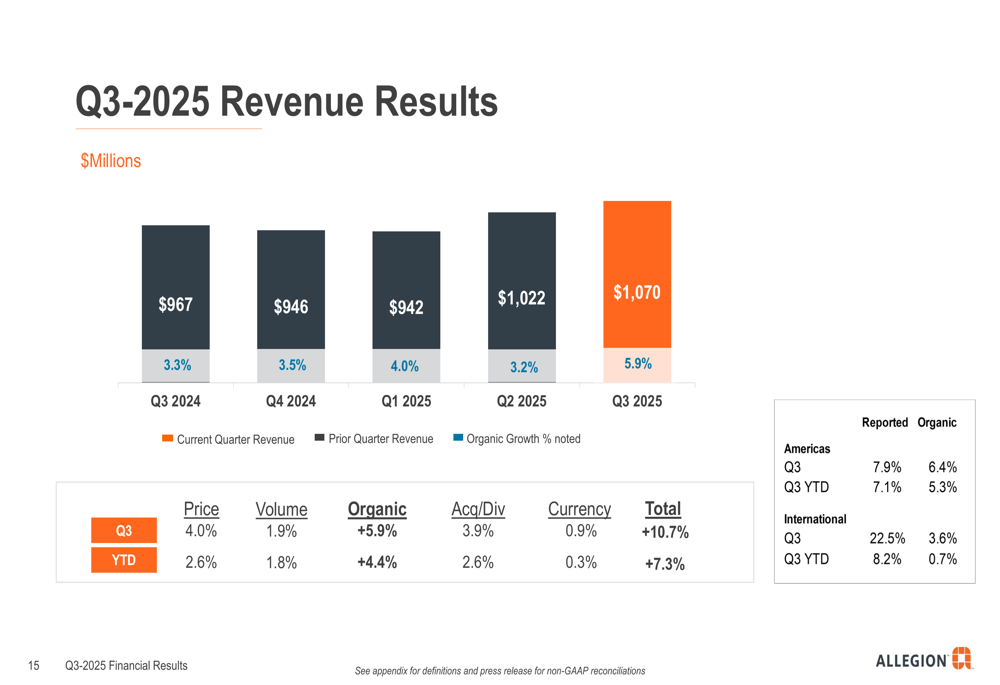

Allegion reported Q3 2025 revenue of $1,070.2 million, representing a 10.7% increase compared to the same period last year. This growth was driven by organic growth of 5.9%, acquisitions contributing 3.9%, and favorable currency impacts adding 0.9%.

As shown in the following comprehensive financial summary:

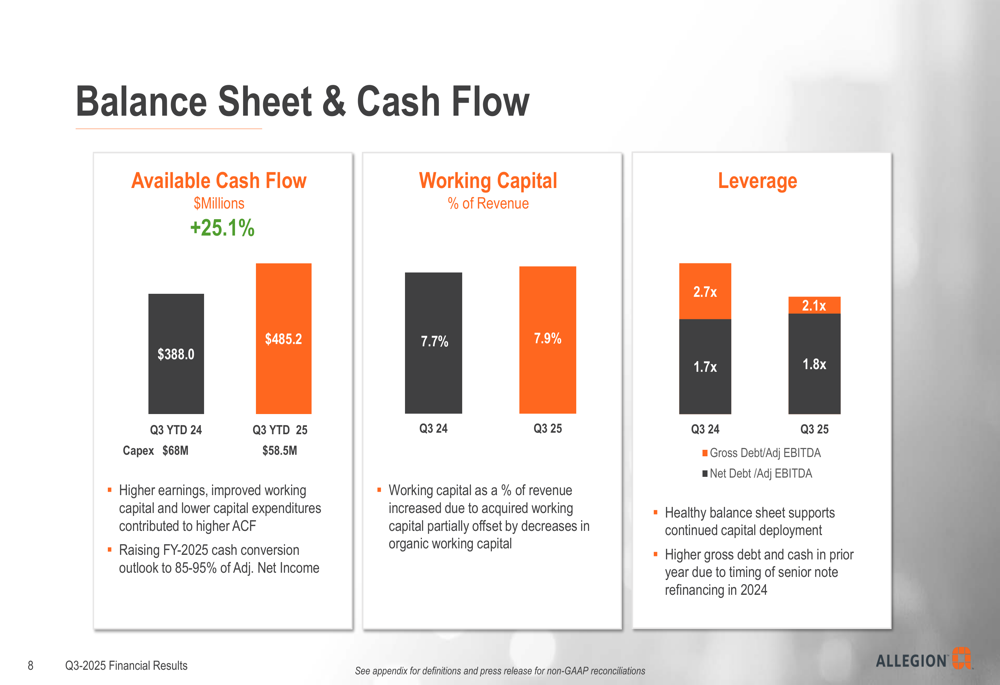

Adjusted earnings per share reached $2.30, up 6.5% year-over-year, despite headwinds from higher tax rates ($0.07) and increased interest expenses ($0.05). The company’s available cash flow for the year-to-date period reached $485.2 million, a substantial 25.1% increase from the prior year.

While adjusted operating income margin declined slightly by 10 basis points, adjusted EBITDA margin remained flat, demonstrating the company’s ability to manage costs effectively in an inflationary environment.

The detailed revenue breakdown reveals strong pricing power, with price realization of 4.0% complemented by volume growth of 1.9%:

Segment Analysis

Americas Segment

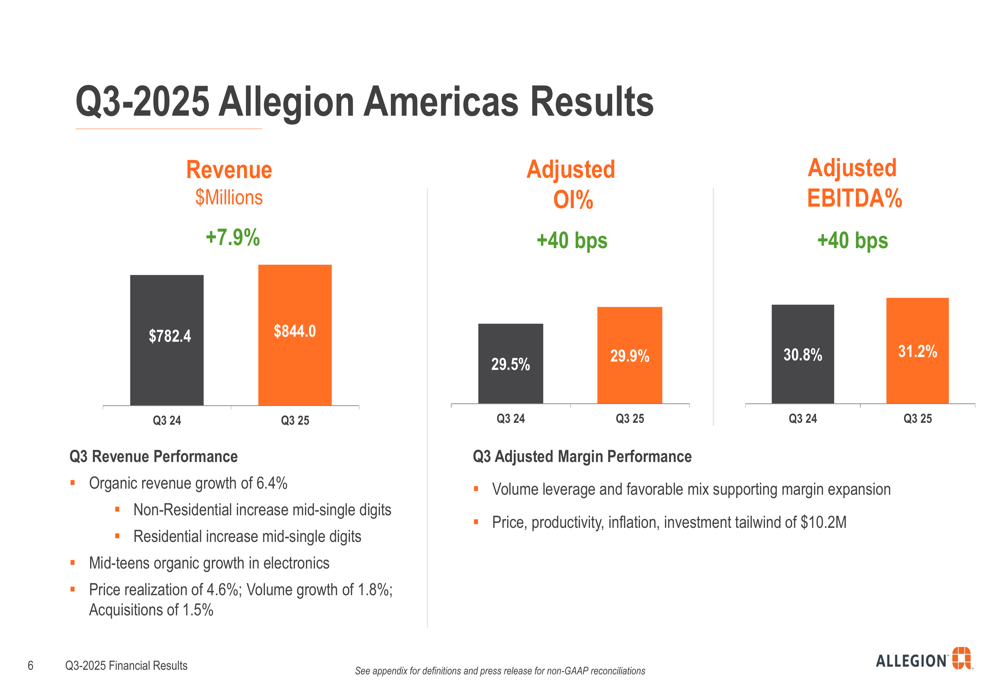

The Americas segment, Allegion’s largest business unit, delivered solid results with revenue of $844.0 million, up 7.9% year-over-year. Organic growth of 6.4% was driven by mid-single-digit growth in both non-residential and residential markets, along with impressive mid-teens growth in electronics products.

Notably, the Americas segment achieved margin expansion, with adjusted operating income margin increasing by 40 basis points to 29.9%. This improvement was attributed to volume leverage and favorable product mix, with price realization of 4.6% helping to offset inflationary pressures.

International Segment

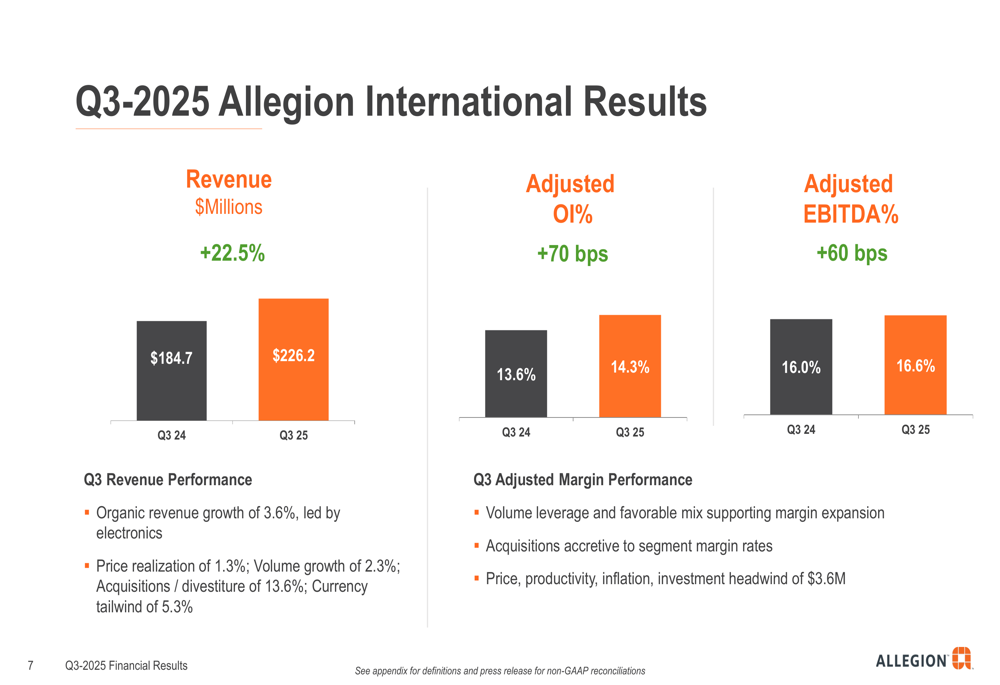

Allegion’s International segment posted exceptional growth, with revenue increasing 22.5% to $226.2 million. While organic growth was more modest at 3.6%, acquisitions and divestitures contributed 13.6% to the segment’s growth, with favorable currency impacts adding 5.3%.

The International segment also demonstrated margin improvement, with adjusted operating income margin expanding by 70 basis points to 14.3%. This expansion occurred despite a $3.6 million headwind from price, productivity, and inflation factors, highlighting the positive impact of volume leverage and favorable mix.

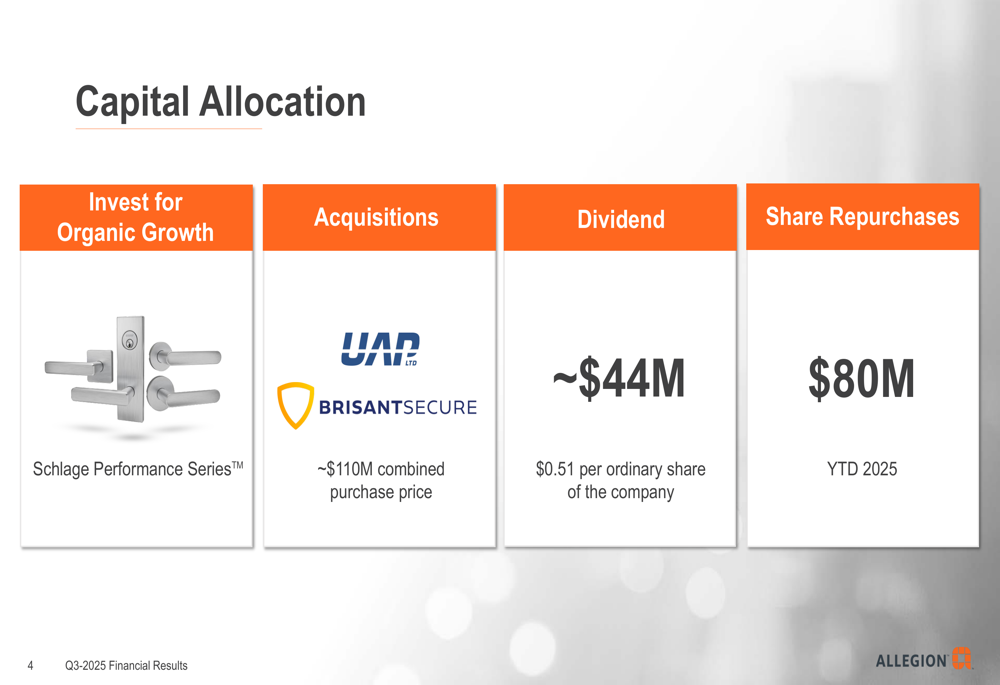

Capital Allocation Strategy

Allegion has accelerated its capital deployment strategy, focusing on four key areas: organic growth investments, acquisitions, dividends, and share repurchases.

The company allocated approximately $44 million for dividends ($0.51 per ordinary share) and $80 million for share repurchases year-to-date. Additionally, Allegion invested approximately $110 million in acquisitions, including Brisant Secure, which is expected to enhance the company’s product portfolio and market reach.

The balance sheet remains strong, with leverage at 2.1x gross debt to adjusted EBITDA and 1.8x net debt to adjusted EBITDA, providing flexibility for continued capital deployment.

Forward-Looking Statements

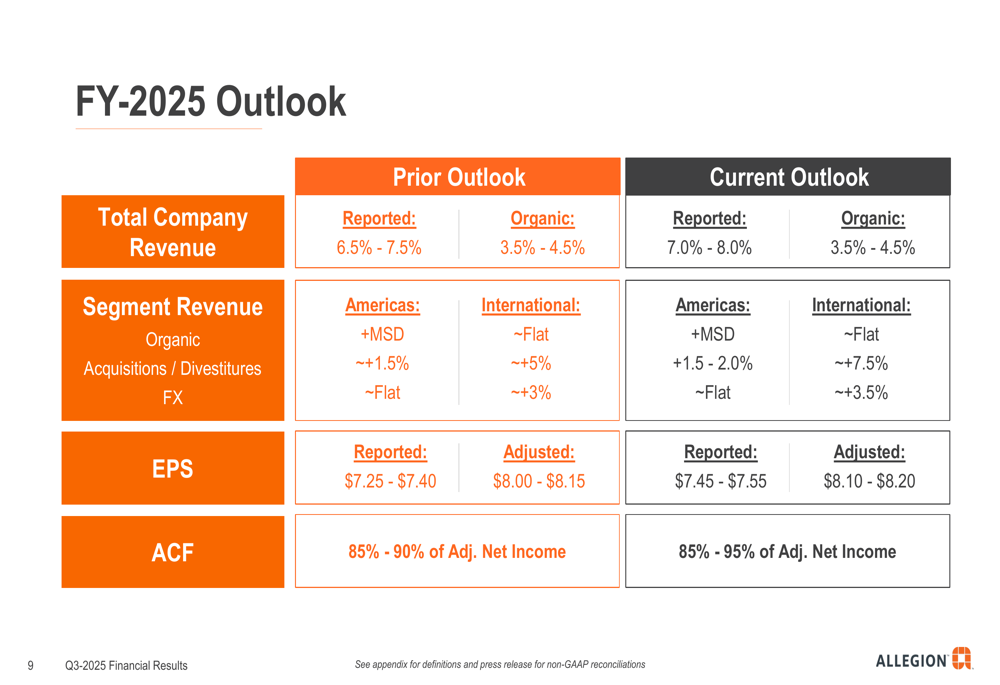

Based on its strong performance, Allegion has raised its full-year 2025 outlook. The company now expects total revenue growth of 7.0% to 8.0%, up from the previous guidance of 6.5% to 7.5%, while maintaining its organic growth forecast of 3.5% to 4.5%.

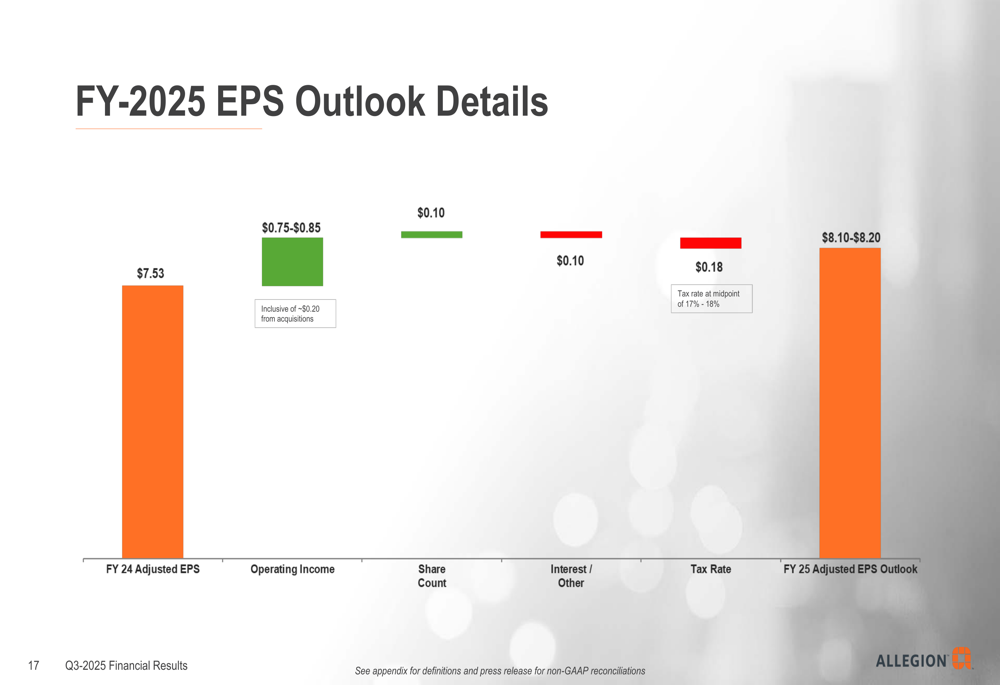

Adjusted EPS guidance has been increased to a range of $8.10 to $8.20, up from the previous outlook of $8.00 to $8.15. This improvement is driven by stronger operating income, including approximately $0.20 contribution from acquisitions, partially offset by higher interest expenses.

Looking ahead to 2026, Allegion expects to benefit from approximately 2 percentage points of revenue carryover from completed acquisitions. The company anticipates continued growth in non-residential markets, while residential markets are expected to remain soft. Management also highlighted the dynamic tariff environment, noting plans for pricing actions to cover inflation.

Conclusion

Allegion’s Q3 2025 results demonstrate the company’s ability to execute effectively in a challenging market environment. With double-digit revenue growth, strategic acquisitions, and an improved outlook, Allegion appears well-positioned to maintain its growth trajectory. The company’s focus on electronics products and international expansion, combined with disciplined capital allocation, provides multiple avenues for continued growth despite potential headwinds from inflation, tariffs, and soft residential markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.