Paul Tudor Jones sees potential market rally after late October

Introduction & Market Context

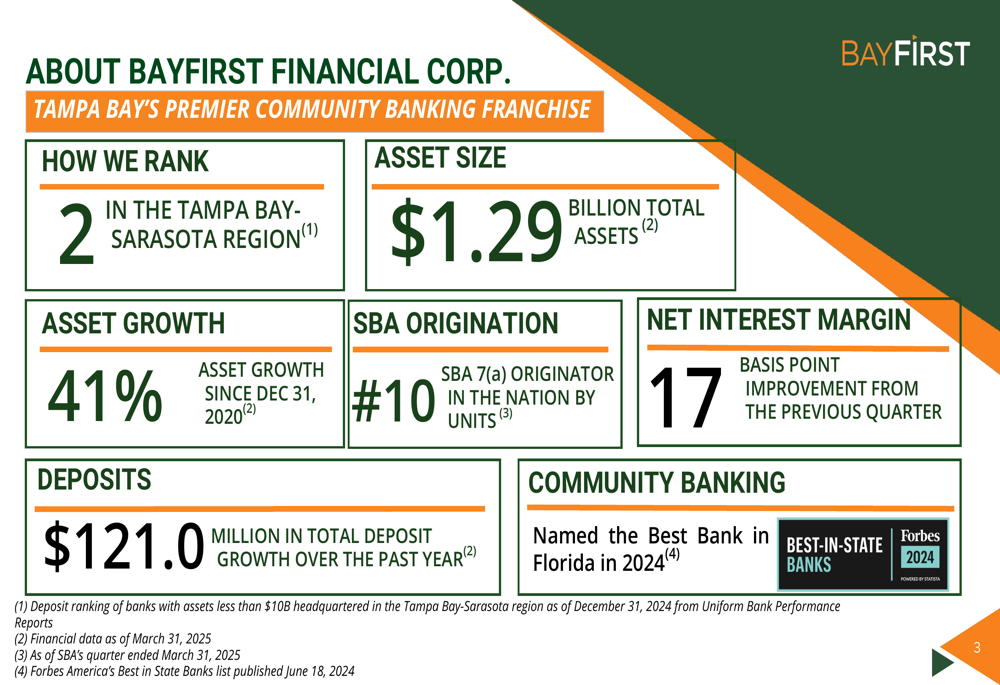

BayFirst Financial Corp. (NASDAQ:BAFN) released its first quarter 2025 results on April 25, showing mixed performance with a quarterly loss despite continued asset growth and improved net interest margin. The community bank, which ranks second in the Tampa Bay-Sarasota region, reported total assets of $1.29 billion, representing 41% growth since December 2020.

The bank’s stock closed at $16.12 in the most recent trading session, up 1.89% from its previous close of $15.90, reflecting investor confidence despite the quarterly loss.

As shown in the following overview of BayFirst’s key metrics and market position:

Quarterly Performance Highlights

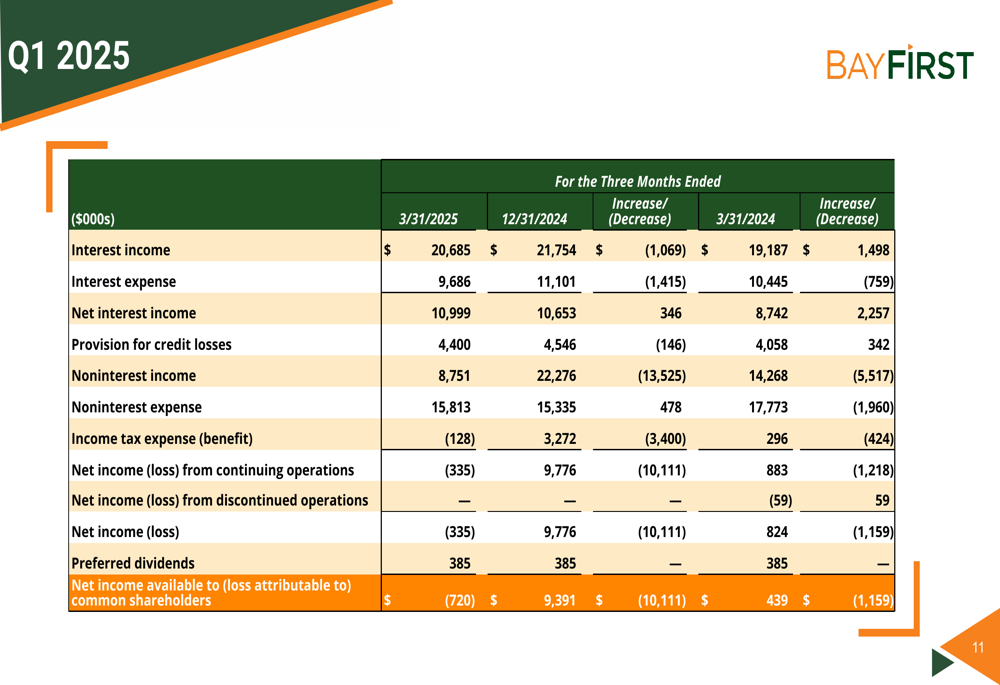

BayFirst reported a net loss attributable to common shareholders of $720,000 or -$0.17 per diluted share for Q1 2025, compared to net income of $439,000 or $0.11 per diluted share in Q1 2024. This represents a significant decline in profitability despite several positive developments in other areas.

Net interest income increased to $11.0 million in Q1 2025, up from $8.7 million in Q1 2024, reflecting a 25.8% year-over-year improvement. The bank’s net interest margin improved to 3.77% in Q1 2025, up from 3.42% in Q1 2024 and 3.60% in the previous quarter.

The detailed financial results for the quarter are presented in the following table:

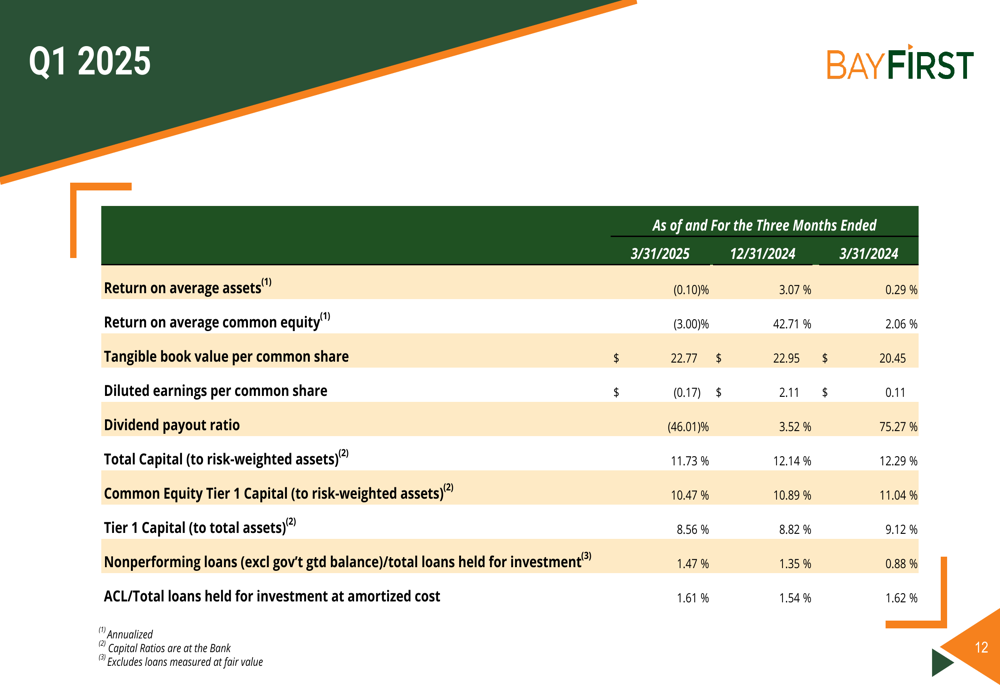

Key performance ratios show the impact of the quarterly loss on profitability metrics, with return on average assets at -0.10% and return on average common equity at -3.00% for Q1 2025, down from 0.29% and 2.06% respectively in Q1 2024. However, tangible book value per common share increased to $22.77, up from $20.45 a year earlier.

The following chart illustrates the key financial ratios:

Detailed Financial Analysis

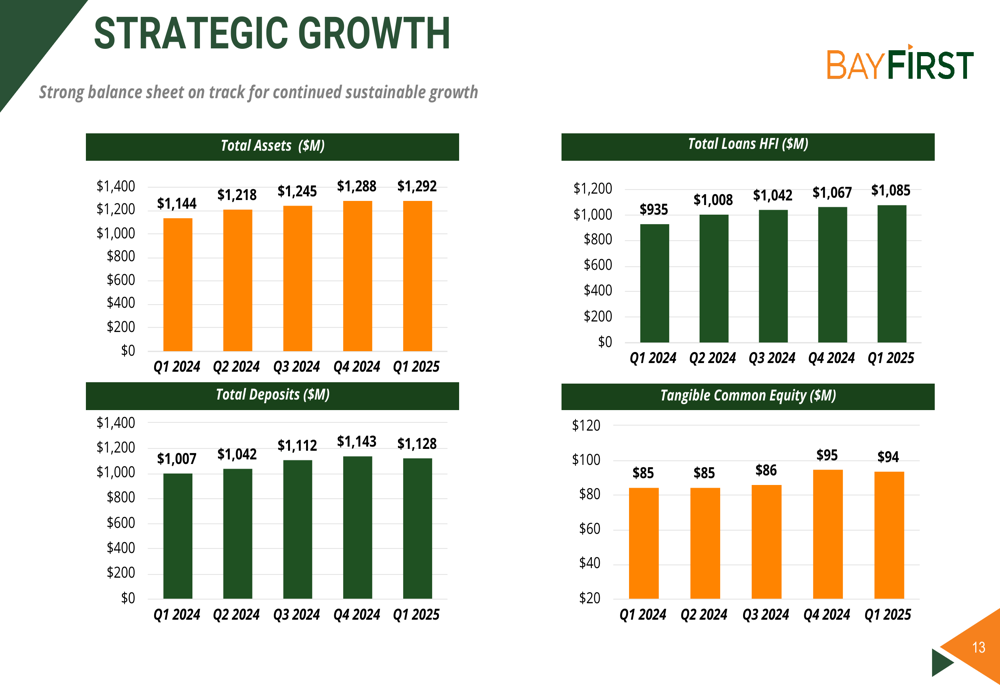

Despite the quarterly loss, BayFirst has maintained consistent growth in several key areas. Total (EPA:TTEF) assets increased to $1.29 billion in Q1 2025, up from $1.14 billion in Q1 2024. Loans held for investment grew to $1.09 billion, representing a 16% year-over-year increase from $935 million.

Total deposits reached $1.13 billion, showing strong year-over-year growth of $121 million or 12% compared to Q1 2024, though deposits decreased by $15 million during the quarter. Approximately 81% of deposits are insured as of March 31, 2025, with minimal use of short-term brokered deposits at $112 million.

The following charts illustrate the bank’s strategic growth across key metrics:

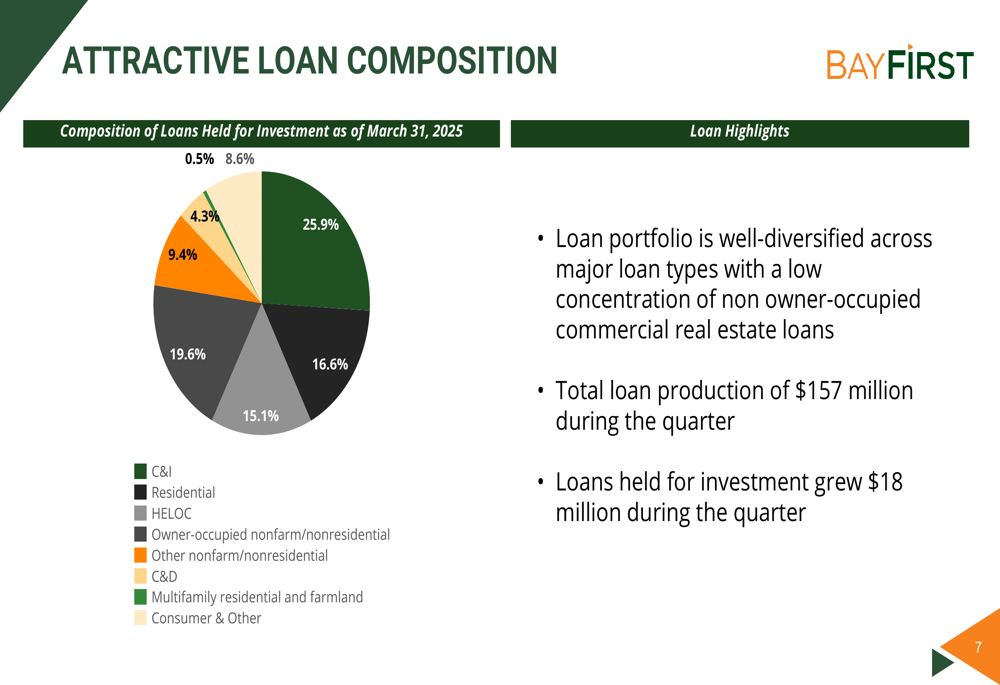

The bank’s loan portfolio remains well-diversified across major loan types, with commercial real estate (nonfarm/nonresidential) representing the largest segment at 25.9%, followed by consumer and other loans at 19.6%, and construction and development loans at 16.6%. Total loan production was $157 million during the quarter, with loans held for investment growing by $18 million.

The composition of the loan portfolio is illustrated in the following chart:

Strategic Initiatives

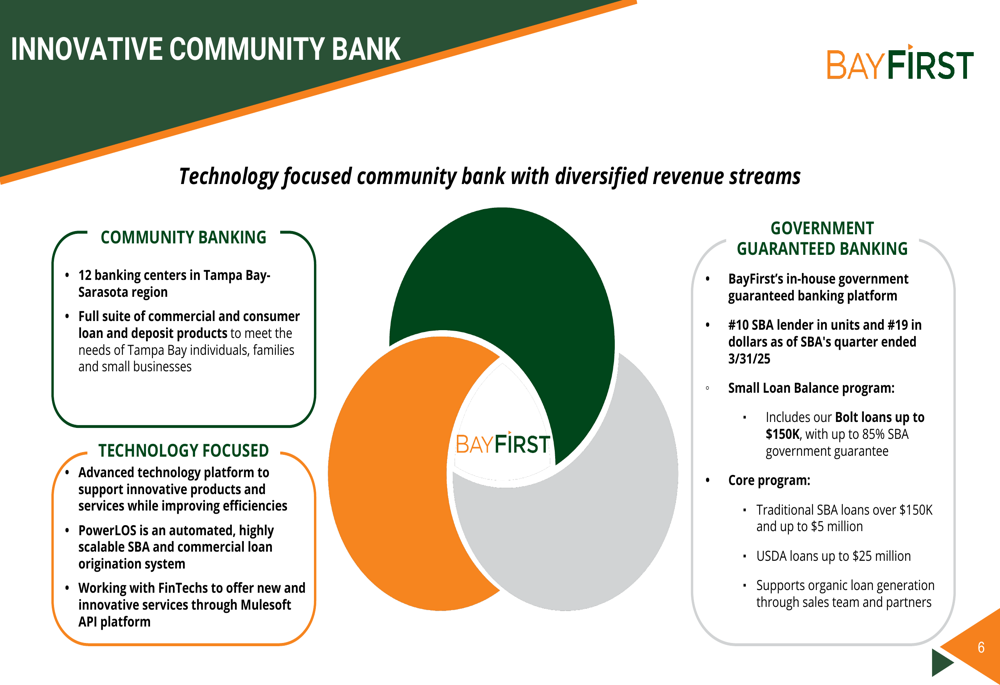

BayFirst positions itself as an innovative community bank with diversified revenue streams across three main areas: community banking, technology focus, and government guaranteed banking. The bank operates 12 banking centers in the Tampa Bay-Sarasota region and offers a full suite of commercial and consumer loan and deposit products.

The bank’s business model and focus areas are illustrated in the following diagram:

For 2025, BayFirst has introduced the "SOAR" initiative, focusing on:

- Striving for operational excellence

- Optimizing technology platform to be more data-driven

- Accelerating focus on business banking

- Realigning and diversifying revenue sources

The bank continues to be a significant player in government guaranteed lending, ranking as the #10 SBA (LON:SBA) 7(a) lender in the nation by units and #19 in dollars. However, government guaranteed loan originations have declined year-over-year, with Q1 2025 volume at $106 million (525 units) compared to $131 million (805 units) in Q1 2024.

Asset Quality and Risk Factors

A key concern in the quarterly results is the deterioration in asset quality metrics. Nonperforming loans (excluding government guaranteed balances) to total loans held for investment increased to 1.47% in Q1 2025, up from 0.88% in Q1 2024. Past due and nonaccrual loans to total loans held for investment increased to 2.38%, up from 1.76% a year earlier.

The allowance for credit losses to total loans held for investment was 1.61% as of March 31, 2025, slightly lower than 1.62% a year earlier. Net charge-offs to total average loans held for investment decreased to 1.28% from 1.71% in Q1 2024, showing some improvement in this metric.

The following charts illustrate the trends in asset quality metrics:

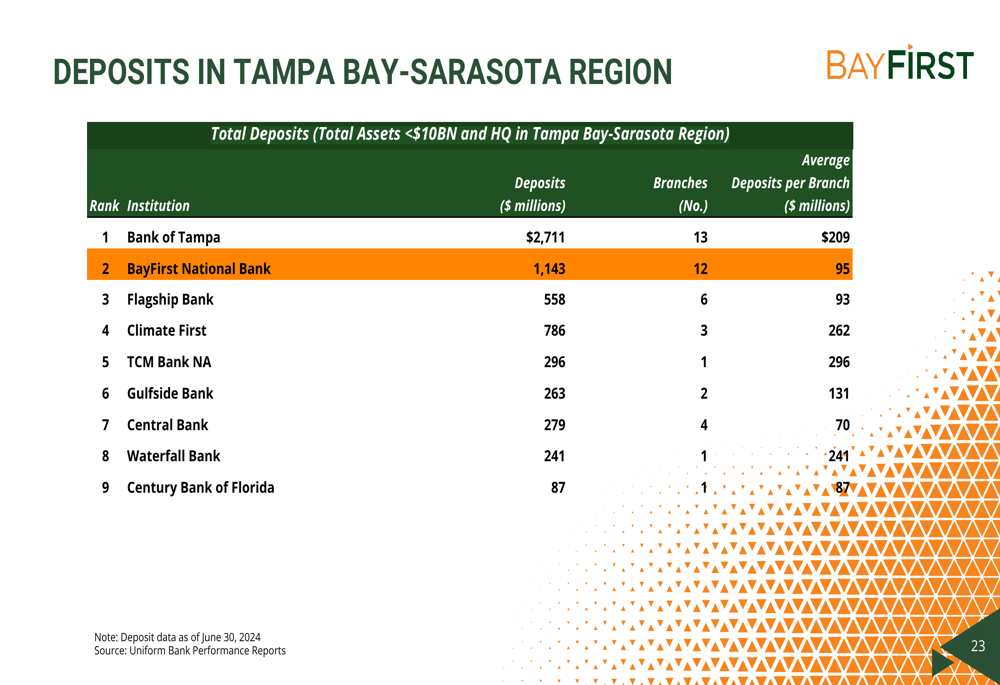

In the competitive landscape, BayFirst maintains its position as the second-largest community bank in the Tampa Bay-Sarasota region based on deposits, behind only Bank of Tampa. With $1.14 billion in deposits across 12 branches, BayFirst averages $95 million in deposits per branch.

The competitive positioning in the Tampa Bay-Sarasota region is illustrated in the following table:

Despite the quarterly loss, BayFirst continues to pay quarterly common stock cash dividends, a practice maintained since 2016. The bank’s dividend payout ratio was -46.01% for Q1 2025, reflecting the continuation of dividend payments despite the negative earnings.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.