Navitas stock soars as company advances 800V tech for NVIDIA AI platforms

Introduction & Market Context

BayFirst Financial Corp. (NASDAQ:BAFN) released its second quarter 2025 results, revealing a widening net loss despite growth in key balance sheet metrics and net interest margin. The Tampa Bay-based community bank reported a net loss of $1.24 million for Q2 2025, compared to a loss of $335,000 in the previous quarter, as credit quality concerns continued to weigh on the company’s performance.

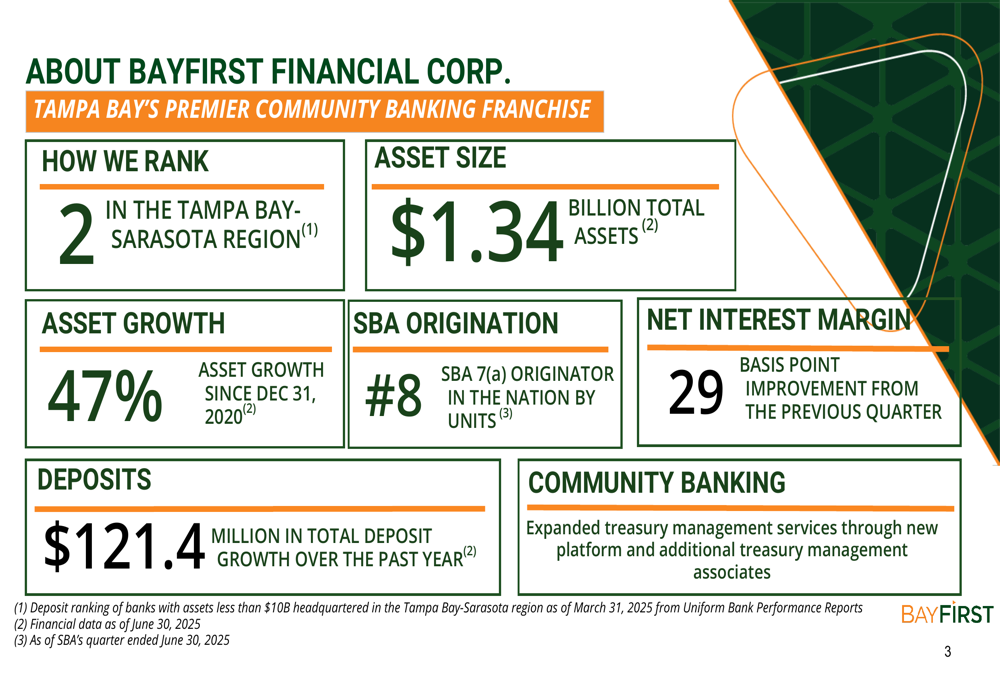

Despite profitability challenges, BayFirst maintained its position as the second-ranked bank in the Tampa Bay-Sarasota region and continued to grow its footprint with $1.34 billion in total assets, representing 47% growth since December 2020.

As shown in the following overview, the bank has achieved notable rankings and growth metrics while working to address credit quality concerns:

Quarterly Performance Highlights

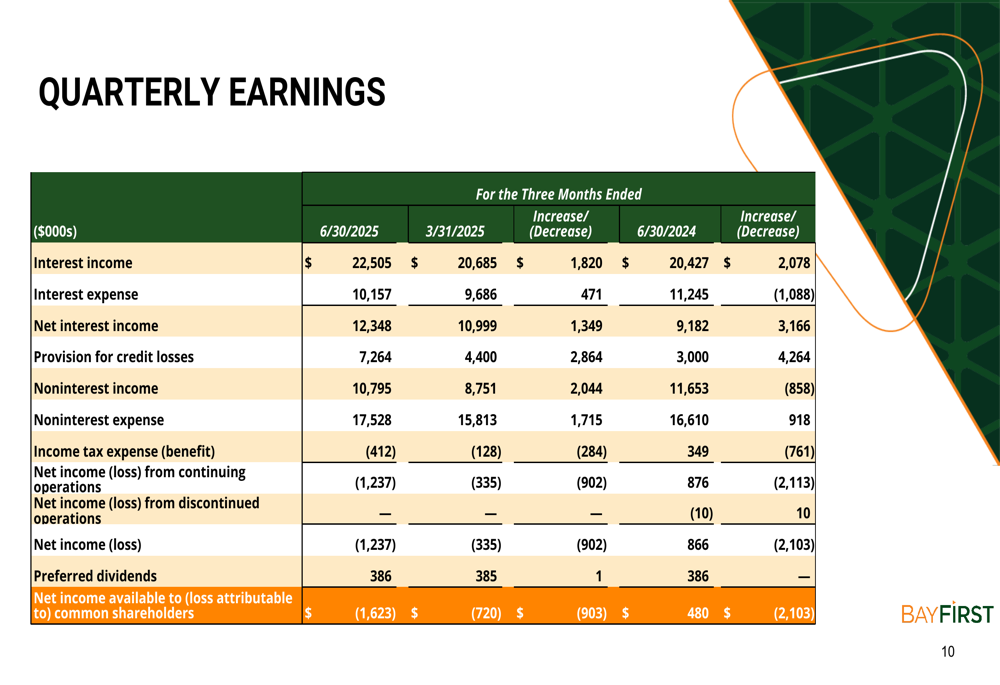

BayFirst’s Q2 2025 financial results showed mixed performance, with strong net interest margin improvement offset by significant credit loss provisions. The bank reported a net loss of $1.24 million for the quarter, compared to a net loss of $335,000 in Q1 2025 and net income of $862,000 in Q2 2024.

The following table details the quarterly earnings performance:

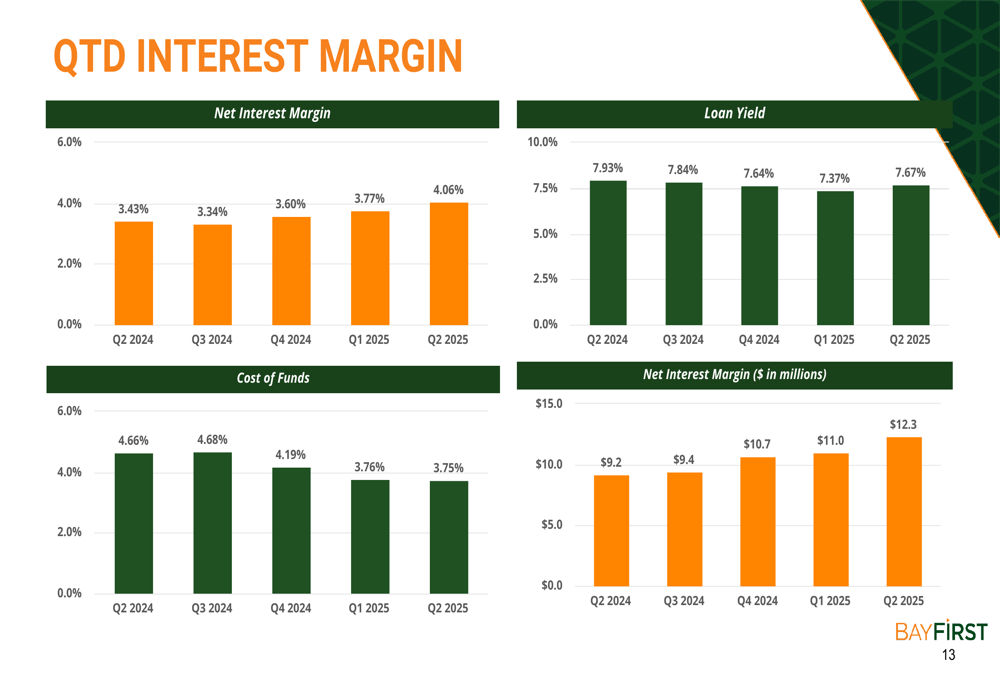

Net interest income reached $12.35 million, up from $11.0 million in the previous quarter, driven by a 29 basis point improvement in net interest margin to 4.06%. This margin expansion occurred as loan yields increased to 7.67% while the cost of funds remained stable at 3.75%.

The bank’s provision for credit losses totaled $7.26 million in Q2, significantly impacting profitability. Year-to-date provisions have reached $11.66 million, reflecting management’s focus on addressing credit quality concerns.

The following chart illustrates the positive trend in net interest margin over the past five quarters:

Balance Sheet and Deposit Growth

Despite profitability challenges, BayFirst continued to grow its balance sheet, with total assets increasing to $1.34 billion, up from $1.29 billion in Q1 2025 and $1.22 billion in Q2 2024. Loans held for investment grew by $41 million during the quarter to $1.13 billion, while deposits increased by $36 million to $1.16 billion.

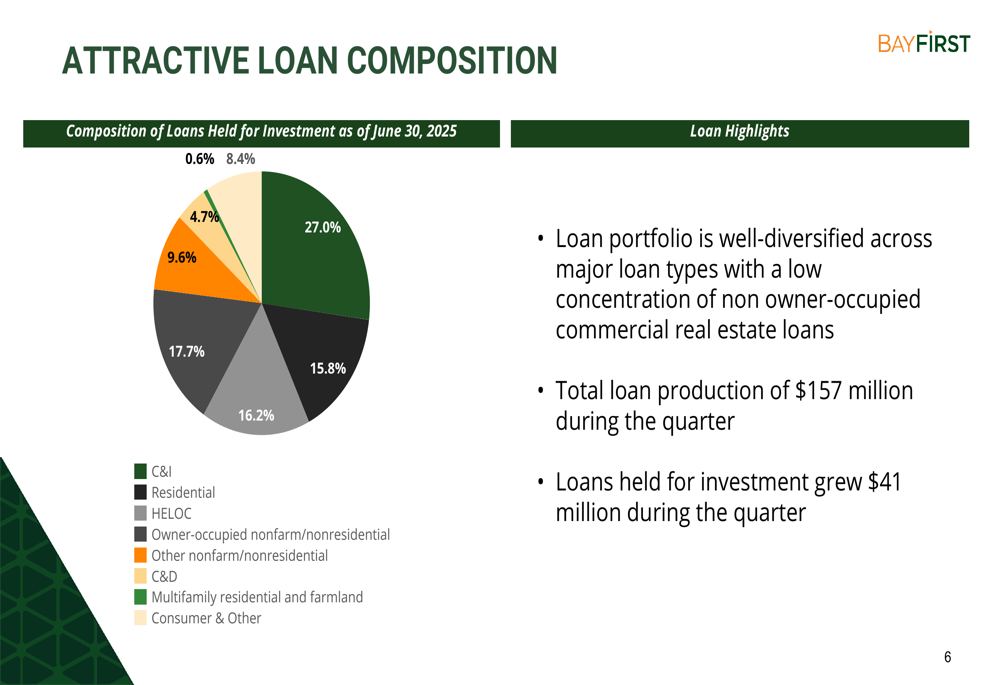

The bank’s loan portfolio remains well-diversified across major loan types, with multifamily residential and farmland representing the largest segment at 27.0%, followed by other nonfarm/nonresidential at 17.7% and construction and development at 16.2%.

The following chart illustrates the bank’s loan portfolio composition:

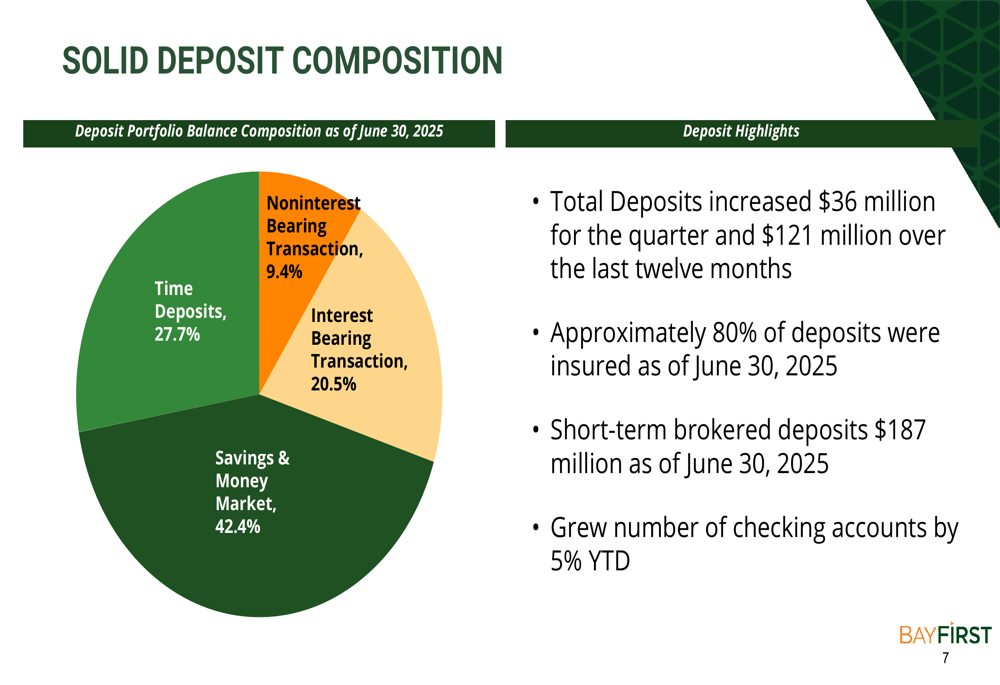

On the funding side, BayFirst reported that approximately 80% of deposits were insured as of June 30, 2025. The deposit base is primarily composed of savings and money market accounts (42.4%), time deposits (27.7%), and interest-bearing transaction accounts (20.5%).

The deposit portfolio composition is shown in the following chart:

Government Guaranteed Banking and SBA (LON:SBA) Lending

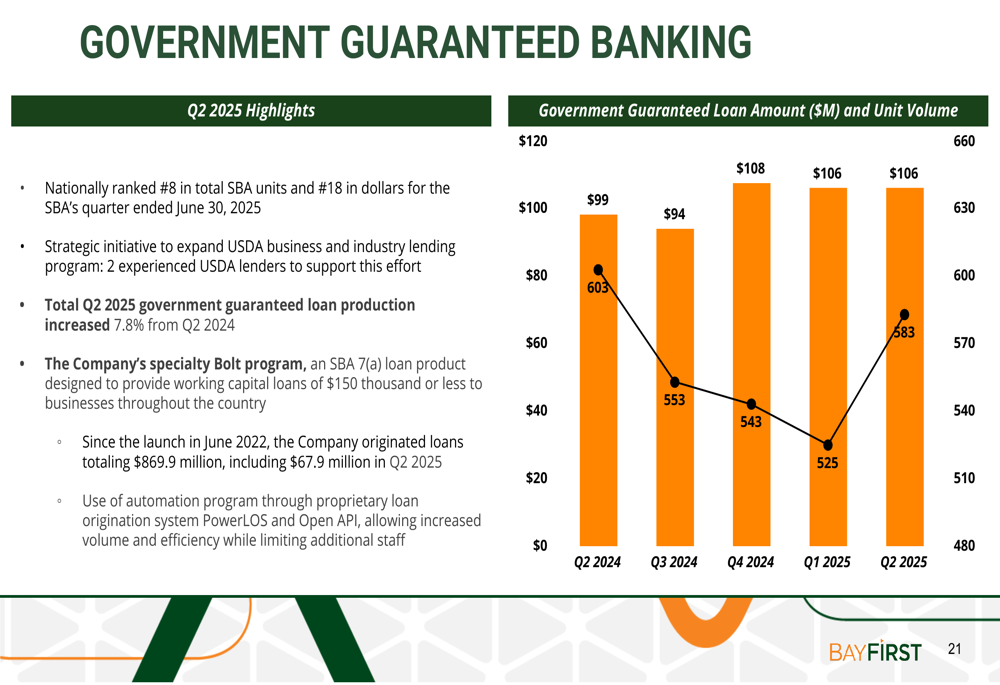

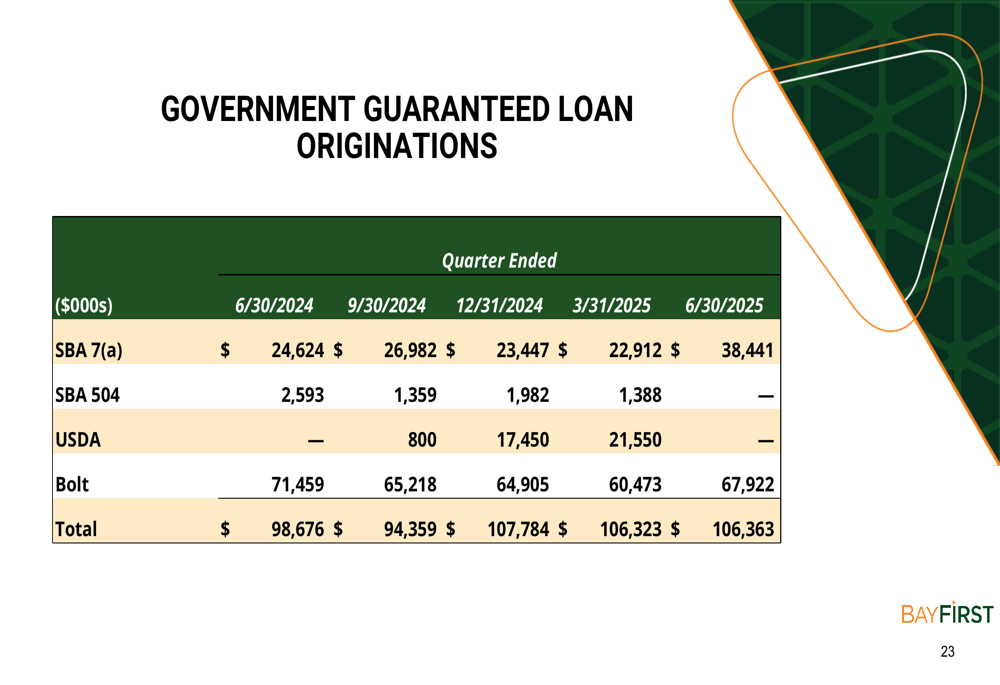

BayFirst maintained its strong position in SBA lending, ranking as the #8 SBA 7(a) originator in the nation by units and #18 by dollars for the quarter ended June 30, 2025. Government guaranteed loan originations totaled $106.4 million in Q2, with SBA 7(a) loans accounting for $38.4 million and the bank’s "Bolt" program contributing $67.9 million.

The following chart illustrates the bank’s performance in government guaranteed lending:

Government guaranteed loans held for investment increased to $440 million, up from $422 million in the previous quarter. Additionally, the bank services $1.07 billion in government guaranteed loans for others, bringing the total government guaranteed loan portfolio to $1.51 billion.

The breakdown of government guaranteed loan originations by program is shown below:

Community Banking Performance

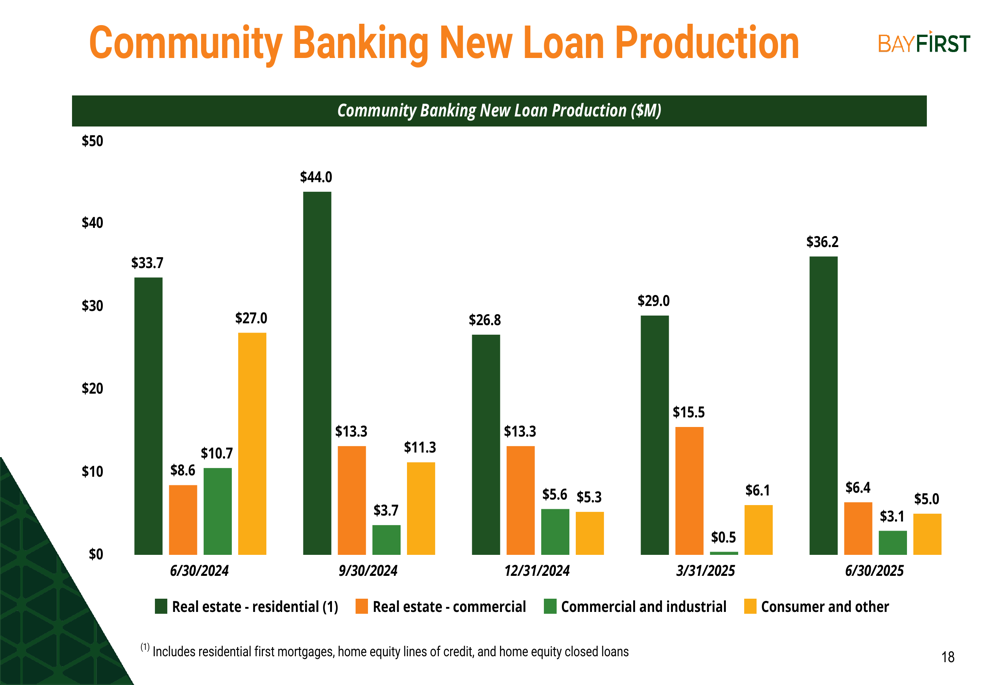

BayFirst’s community banking segment showed continued growth, with new loan production totaling $50.7 million in Q2 2025. Residential real estate loans led production at $36.2 million, followed by commercial and industrial loans at $6.4 million.

The following chart details community banking new loan production by category:

Total (EPA:TTEF) community banking loan balances reached $698.1 million as of June 30, 2025, with residential real estate loans comprising the largest portion at $378.2 million. The bank’s 12 banking centers in the Tampa Bay-Sarasota region continue to drive deposit growth, with total deposits increasing by $121.4 million over the past year.

The bank has also expanded its treasury management services through a new platform and additional treasury management associates, with treasury management fee income growing from $20,000 in 2022 to $43,000 year-to-date in 2025.

Strategic Initiatives and Outlook

BayFirst outlined its 2025 strategic initiatives under the acronym "SOAR":

- Strive for operational excellence

- Optimize technology platform to be more data-driven

- Accelerate focus on business banking

- Realign and diversify sources of revenue

These initiatives align with the bank’s efforts to address credit quality concerns while continuing to grow its franchise. The focus on operational excellence and optimizing technology appears particularly relevant given the credit challenges facing the institution.

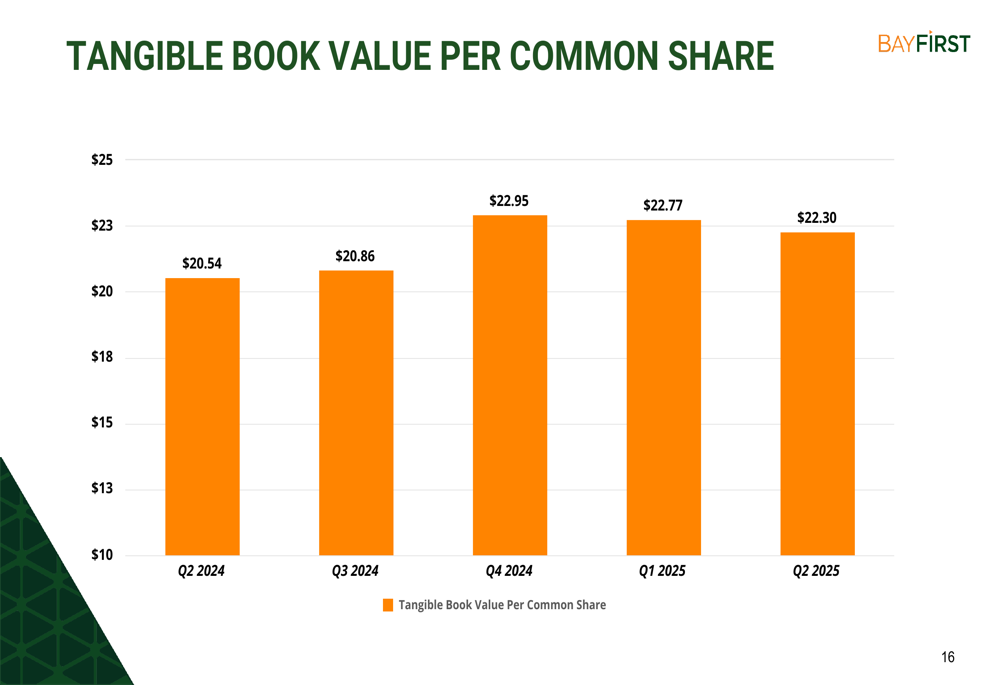

The bank’s tangible book value per common share decreased slightly to $22.30 in Q2 2025 from $22.77 in Q1 2025, as shown in the following chart:

Credit Quality and Capital Position

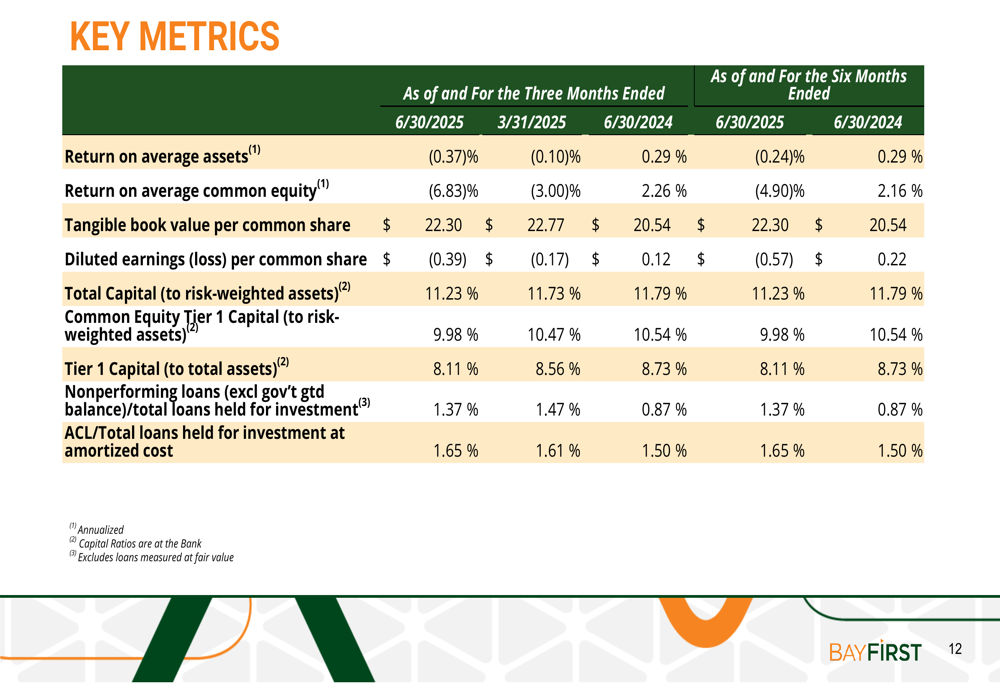

BayFirst’s credit metrics show increasing stress, with the allowance for credit losses to total loans held for investment ratio rising to 2.06% in Q2 2025 from 1.50% in Q1 2025. This increase reflects management’s proactive approach to addressing potential credit issues through significant provisions.

The bank maintains strong capital ratios, with total capital to risk-weighted assets at 13.59% and Common Equity Tier 1 capital to risk-weighted assets at 11.00% as of June 30, 2025. These ratios remain well above regulatory requirements, providing a buffer as the bank works through credit quality challenges.

The following table summarizes key performance metrics, including capital ratios and credit quality indicators:

BayFirst Financial’s Q2 2025 results reflect a bank navigating credit quality challenges while continuing to grow its franchise. The significant improvement in net interest margin provides a positive signal for future earnings potential, but the substantial provision for credit losses indicates ongoing concerns about loan portfolio quality. Investors will likely focus on whether the bank can maintain its growth trajectory while successfully addressing credit issues in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.