Gold rally may be losing steam but no major correction seen: DB

Introduction & Market Context

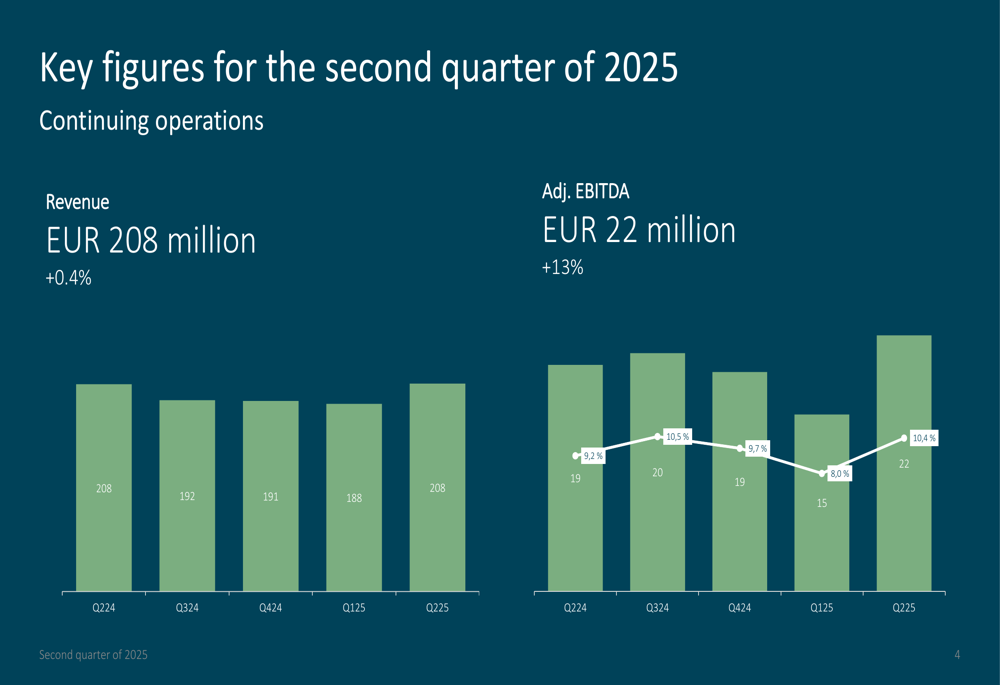

BEWI ASA (OSE:BEWI) presented its second quarter 2025 results on August 20, showing mixed performance across its business segments as the company continues its strategic repositioning efforts. The company reported modest revenue growth of 0.4% year-over-year to EUR 208 million, while adjusted EBITDA increased by 13% to EUR 22 million.

The results reflect a divergence in market conditions, with packaging segments showing robust growth while the building and construction industry’s recovery progressed slower than anticipated. BEWI’s stock closed at NOK 22.50 on August 19, down 4.26% ahead of the results presentation, and has experienced a 52-week range of NOK 19.40 to NOK 30.00.

Quarterly Performance Highlights

BEWI’s second quarter showed modest top-line growth but a significant improvement in adjusted EBITDA, demonstrating the company’s focus on operational efficiency and higher-margin business segments.

As shown in the following chart of quarterly revenue and adjusted EBITDA:

The company’s revenue remained relatively stable at EUR 208 million compared to EUR 206 million in Q2 2024, while adjusted EBITDA increased to EUR 22 million from EUR 19 million in the same period last year. This represents a 13% improvement in profitability despite flat revenue growth.

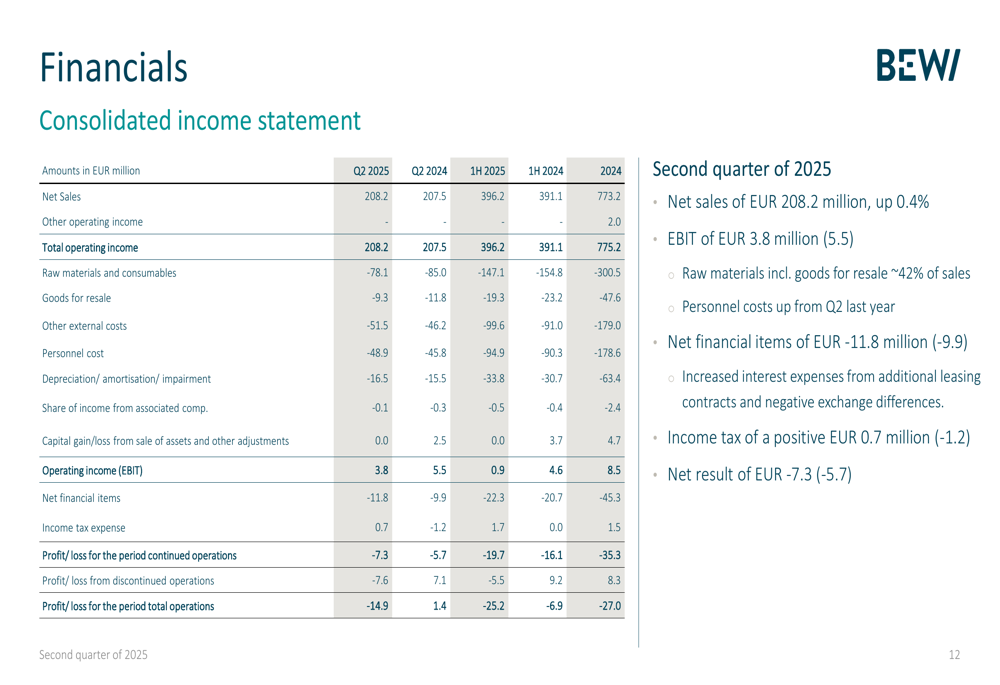

However, the consolidated income statement reveals that despite the improved adjusted EBITDA, BEWI reported a net loss of EUR 14.9 million for Q2 2025, compared to a profit of EUR 1.4 million in Q2 2024. This decline was primarily due to challenges in the RAW segment, which is now reported as discontinued operations.

Segment Performance Analysis

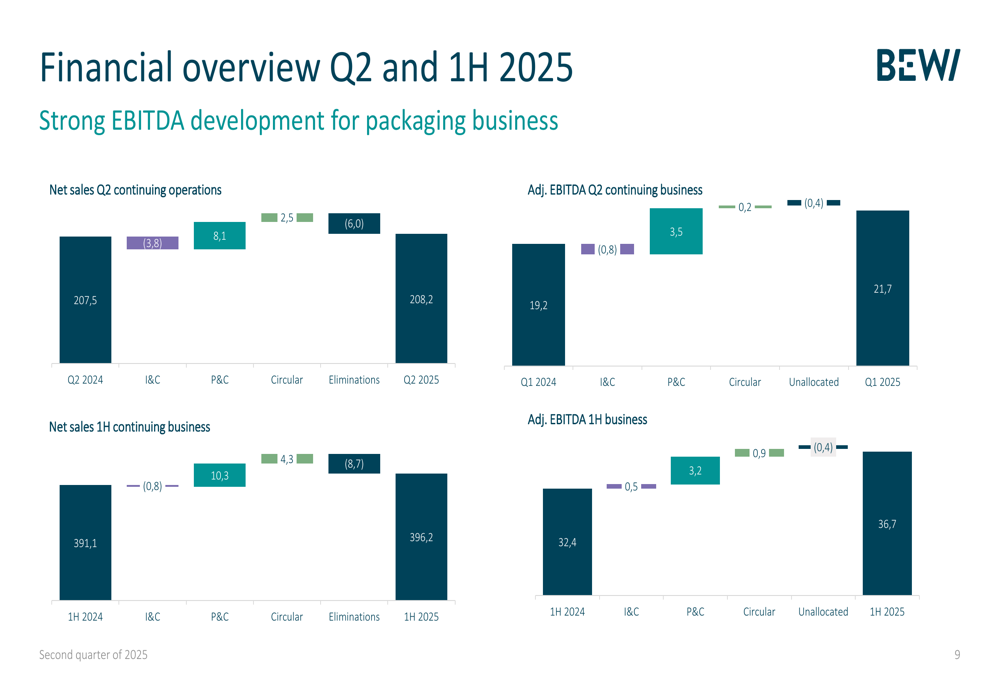

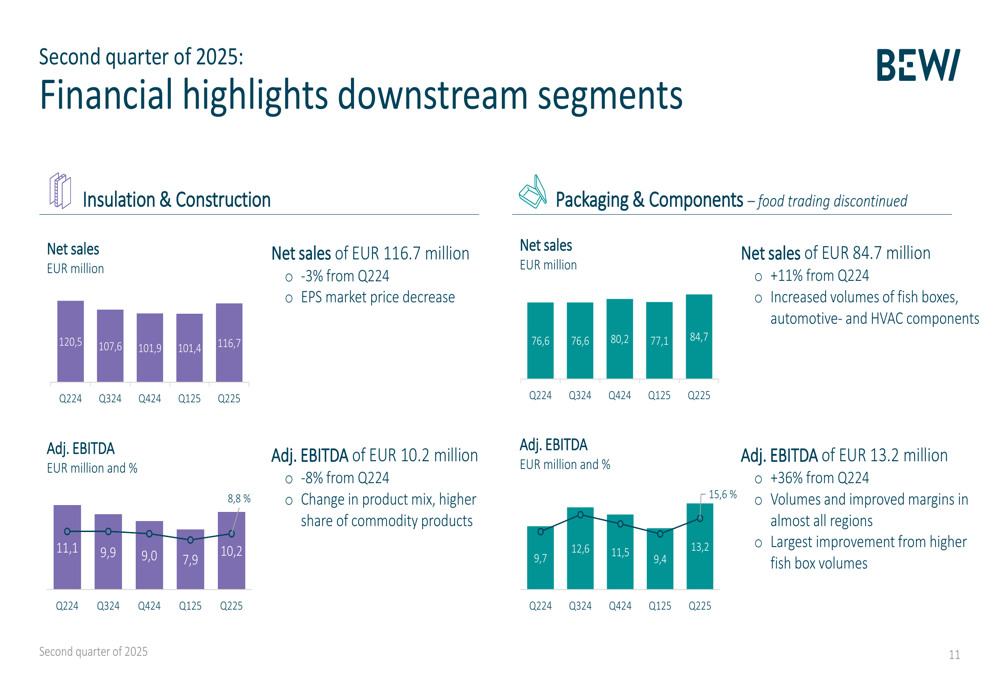

BEWI’s performance varied significantly across its business segments, with Packaging (NYSE:PKG) & Components delivering strong results while Insulation & Construction faced continued challenges.

The company provided a detailed breakdown of performance by segment, highlighting the divergent trends:

The downstream segments showed contrasting performance, with Packaging & Components delivering exceptional results while Insulation & Construction continued to face market headwinds:

The Packaging & Components segment was the standout performer, with net sales increasing by 11% to EUR 84.7 million and adjusted EBITDA surging by 36% to EUR 13.2 million. This growth was driven by increased volumes in fish boxes and automotive and HVAC components, along with improved margins across most regions.

In contrast, the Insulation & Construction segment saw a 3% decline in net sales to EUR 116.7 million and an 8% decrease in adjusted EBITDA to EUR 10.2 million. This performance reflects the slower-than-anticipated recovery in the building and construction industry and a shift in product mix toward lower-margin commodity products.

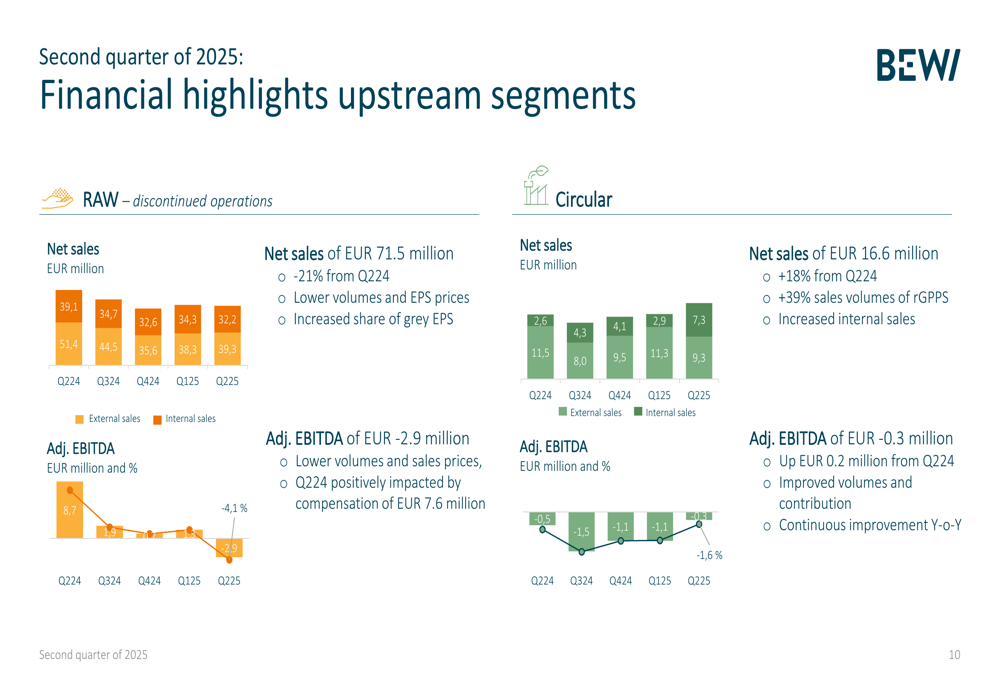

The upstream segments also showed mixed results:

The Circular segment showed promising progress with a 44% increase in collection volumes and improving production and sales volumes. While still operating at a small loss (EUR -0.3 million adjusted EBITDA), this represents an improvement from the EUR -1.1 million reported in Q2 2024.

The RAW segment, now reported as discontinued operations following the Unipol (BIT:UNPI) merger, faced challenging market conditions with volatile raw material prices, resulting in an adjusted EBITDA of EUR -2.9 million compared to EUR 8.7 million in Q2 2024, which had been positively impacted by compensation of EUR 7.6 million.

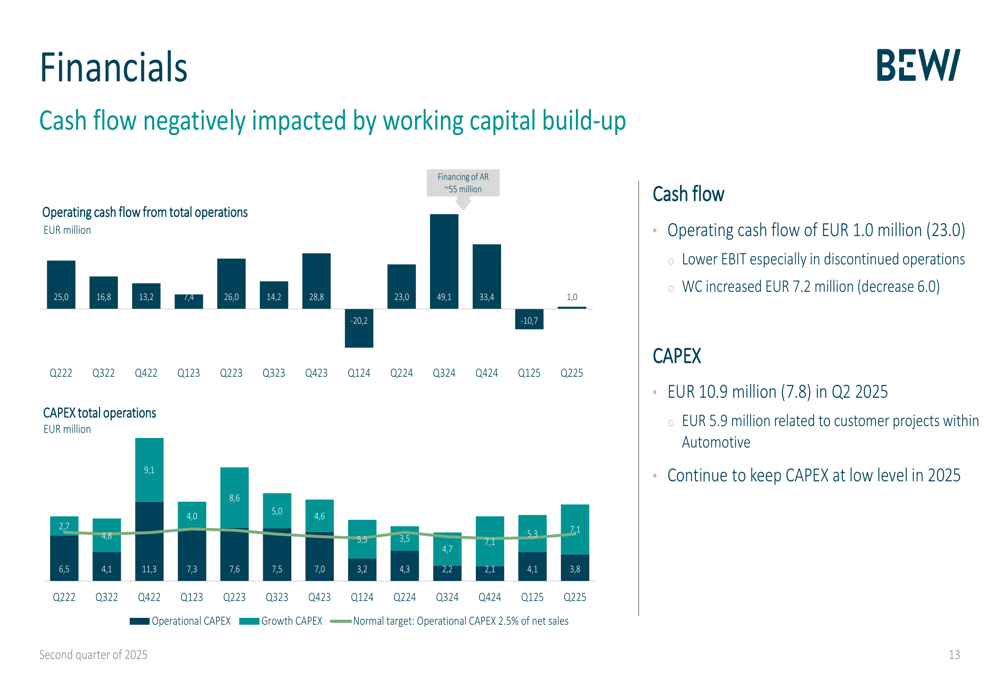

Financial Position and Cash Flow

BEWI’s cash flow performance deteriorated in Q2 2025, with operating cash flow turning negative at EUR -10.7 million compared to a strong positive flow of EUR 49.1 million in Q2 2024. This decline was attributed to lower EBIT, particularly in discontinued operations, and an increase in working capital.

The following chart illustrates the operating cash flow and CAPEX trends:

Capital expenditure increased to EUR 7.3 million in Q2 2025 from EUR 6.5 million in Q2 2024, with EUR 5.9 million related to customer projects within the Automotive segment. The company indicated it would continue to keep CAPEX at a low level throughout 2025.

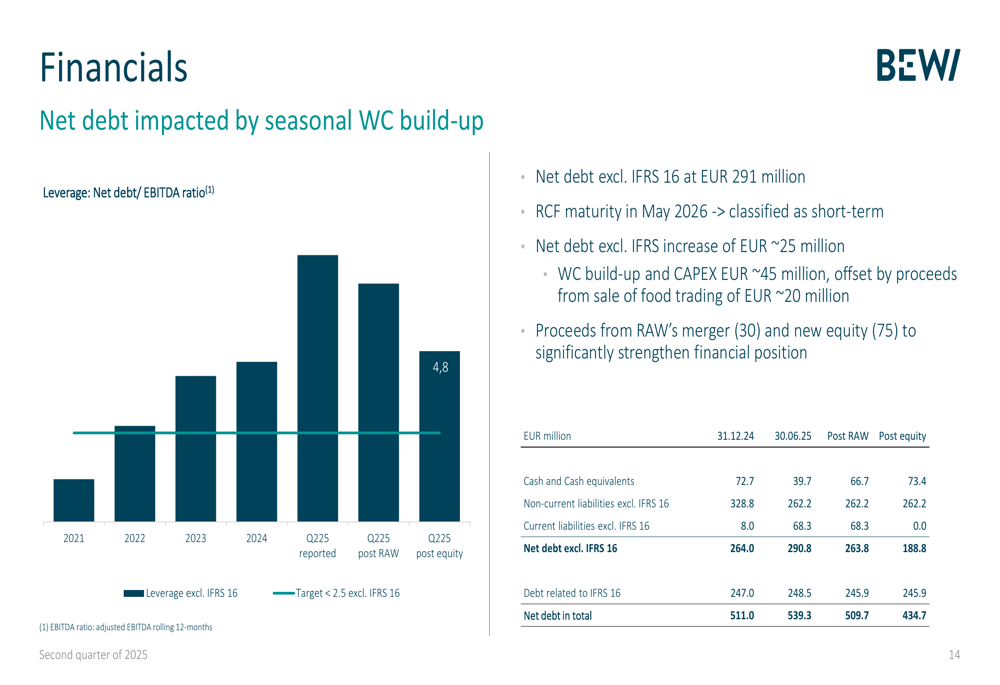

BEWI’s net debt position (excluding IFRS 16) increased to EUR 291 million as of June 30, 2025, up from EUR 264 million at the end of 2024. However, the company expects to significantly strengthen its financial position through proceeds from the RAW segment merger (EUR 30 million) and a new equity issue (EUR 75 million).

The company noted that its revolving credit facility matures in May 2026 and has been classified as short-term debt, which explains the shift from non-current to current liabilities. Post-transactions, BEWI projects its net debt excluding IFRS 16 to decrease to EUR 188.8 million, substantially improving its leverage ratio.

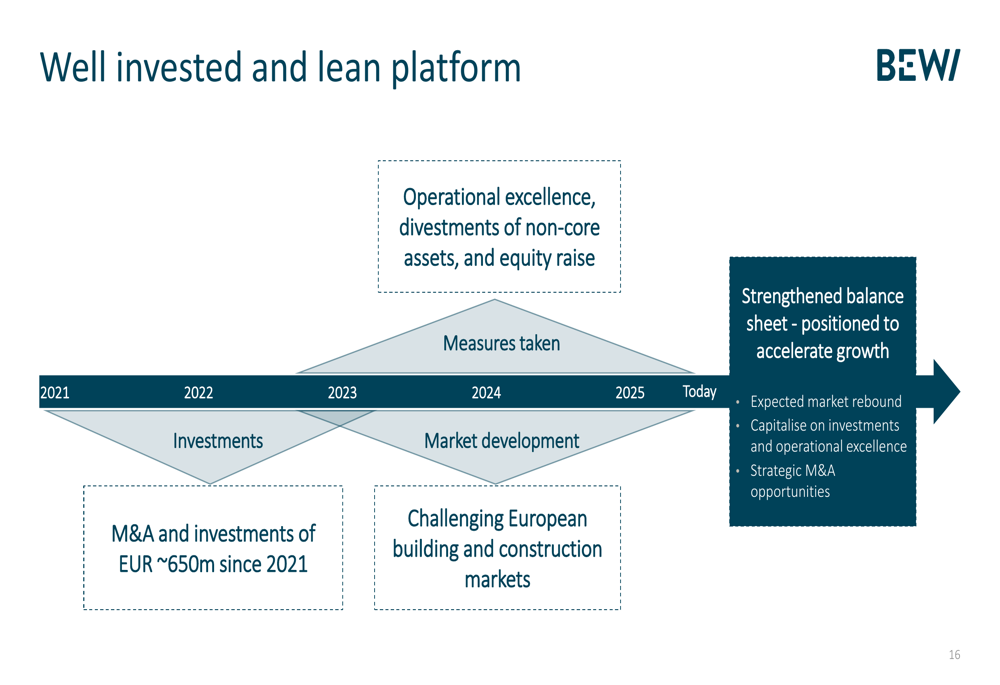

Strategic Initiatives

BEWI outlined its strategic focus on higher-margin businesses with significant growth opportunities, emphasizing energy-efficient buildings and circular packaging while reducing financial exposure to raw materials.

The company highlighted its strategic journey and positioning for future growth:

BEWI has completed two strategic transactions: the merger of its traded food packaging business with STOK and the Unipol merger for its RAW segment. These moves align with the company’s strategy to simplify its structure and focus on higher-margin businesses.

The company is sharpening its focus on growth opportunities in specific areas:

Looking ahead, BEWI is positioning itself to capitalize on market recovery, with a strengthened financial position and streamlined operations:

Outlook

BEWI provided a cautiously optimistic outlook, noting that while the recovery in building and construction markets is progressing slower than anticipated, the company is well-positioned for long-term growth with its strengthened financial position and operational improvements.

The company expects continued strong performance in food packaging and a steady improvement in the circular segment. The strategic transactions completed and the equity issue are expected to strengthen BEWI’s financial position, preparing the company for both organic growth and potential acquisitions.

This outlook aligns with the company’s Q1 2025 commentary, which highlighted investments in the automotive sector and operational efficiencies. The focus on cost management continues, with BEWI operating at 60-70% factory capacity and implementing cost-cutting initiatives.

BEWI’s strategic positioning in sustainability and circular economy initiatives remains a key focus, as the company aims to increase collection and use of recycled materials while optimizing capacity and costs to capitalize on market recovery opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.