TSX gains after CPI shows US inflation rose 3%

Introduction & Market Context

Boliden AB (STO:BOL) reported strong operational results for the third quarter of 2025, highlighted by substantial free cash flow generation and record production at key mining operations. The Swedish mining and smelting company saw its stock rise 2.34% following the earnings release, closing at SEK 409.40 on October 22, 2025.

The quarter was characterized by favorable metal prices, particularly for precious metals, which helped offset the impact of a weaker U.S. dollar. Gold prices surged 40% year-over-year, while silver prices increased by 34% during the same period, contributing positively to the company’s financial performance.

Quarterly Performance Highlights

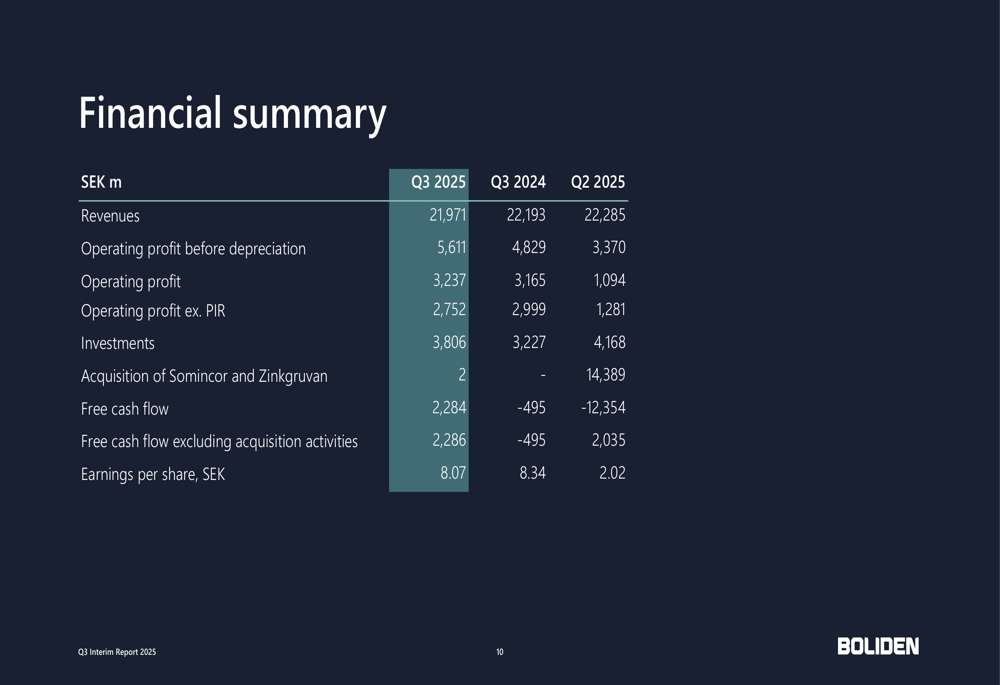

Boliden reported operating profit excluding process inventory revaluation (PIR) of SEK 2,752 million for Q3 2025, down from SEK 2,999 million in the same period last year. Despite this slight decline, free cash flow improved dramatically to SEK 2,284 million, compared to negative SEK 495 million in Q3 2024.

The company’s financial summary reveals solid performance across key metrics, though with some mixed results compared to the previous year:

The mines segment was a particular bright spot, with operating profit excluding PIR increasing to SEK 2,429 million from SEK 2,022 million in Q3 2024. However, the smelters segment experienced a decline, with operating profit falling to SEK 689 million from SEK 1,131 million year-over-year.

As illustrated in the following chart showing operating profit by business area, the mines segment has maintained a strong upward trajectory while smelters have faced more challenges:

Operational Performance

Boliden achieved record mine production at Aitik and record milled volume at Garpenberg during the quarter. Aitik’s milled volume was 9.8 million tonnes, slightly lower than the 10.3 million tonnes in Q3 2024, but with record mine production. Garpenberg’s milled volume reached 956 kilotonnes, up from 937 kilotonnes in the same period last year.

The quarter also marked the first full period with Somincor operations included in Boliden’s results following its acquisition. Meanwhile, Tara’s ramp-up has been slower than expected, presenting some operational challenges.

In the smelters segment, Rönnskär experienced planned maintenance and an unfavorable feed mix, while Harjavalta and Kokkola maintained stable production. Odda reported lower zinc production compared to the previous quarter.

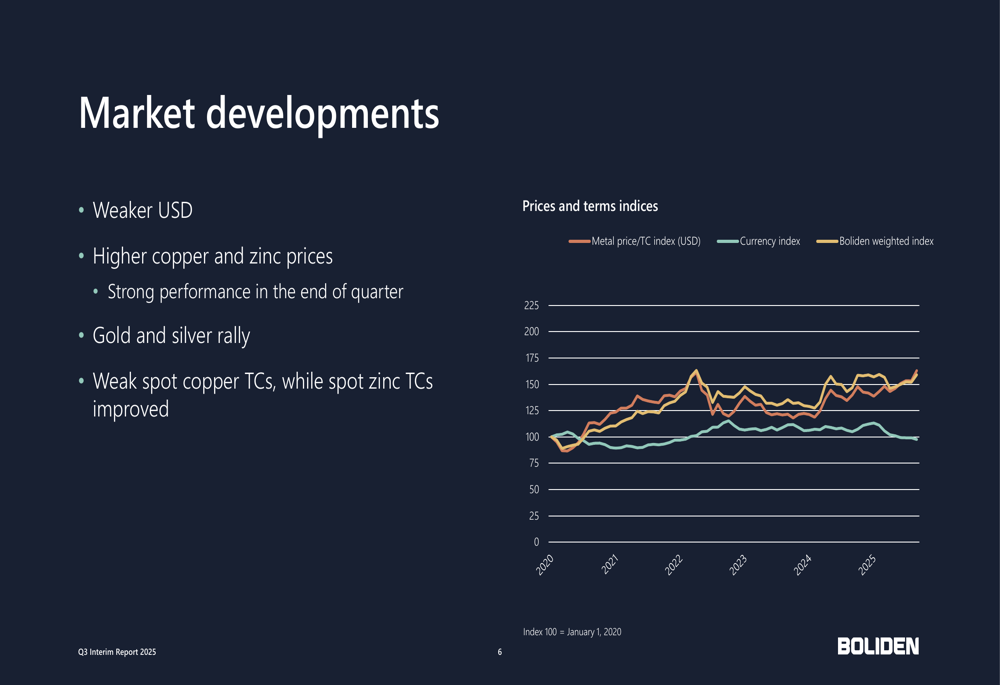

Market Developments and Price Impact

The company benefited from strong metal prices during the quarter, particularly for gold and silver, which saw significant year-over-year increases. However, these positive effects were partially offset by a weaker U.S. dollar.

As shown in the following chart of market developments, metal prices have generally trended upward despite currency headwinds:

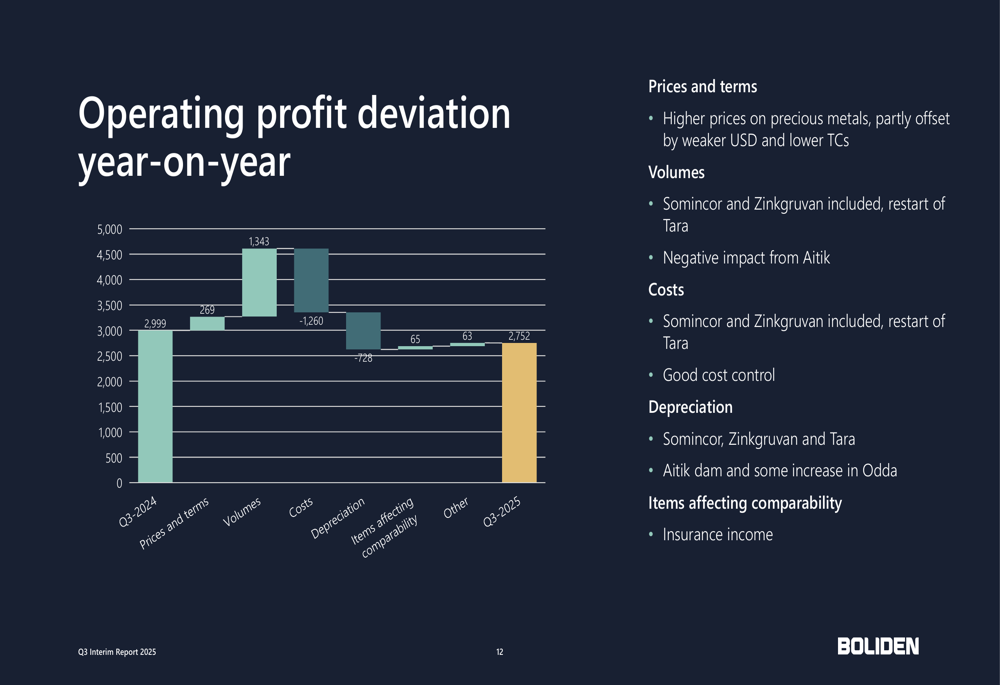

The year-over-year operating profit deviation analysis reveals that positive price effects contributed SEK 270 million to the results, but were offset by higher costs (SEK -396 million) and other factors:

Strategic Initiatives and Projects

Boliden continues to make progress on several key strategic projects. The Odda expansion is in the hot commissioning phase, with the first delivery of Odda Leach Product made in early Q4. The Rönnskär tankhouse project is on track, with ramp-up expected during the second half of 2026.

The following image shows the current status of the Odda expansion project and other key initiatives:

In a significant development for future growth, Boliden received a mining concession for the Laver deposit, although this has been appealed. The company is also advancing the Garpenberg 4.5 million tonnes expansion, with the paste project proceeding according to plan while awaiting permit approval.

Challenges and Outlook

Despite the overall positive results, Boliden faces several challenges. Proposed tax changes in Finland could increase annual costs for the Kevitsa mine by EUR 20-30 million, potentially affecting future investment decisions in the country. The Finnish parliament is expected to make a decision by the end of 2025.

On the environmental front, greenhouse gas emissions increased to 234 kilotonnes from 212 kilotonnes in the comparable period, though safety metrics improved with Lost Time Injury Frequency decreasing to 3.5 from 5.8.

For the remainder of 2025, Boliden maintains its capital expenditure guidance of SEK 15.5 billion and expects insurance cash flow of approximately SEK 2 billion. The company anticipates planned maintenance in smelters to have a negative impact of SEK 500 million and projects milled volume in Aitik to be close to 40 million tonnes for the full year.

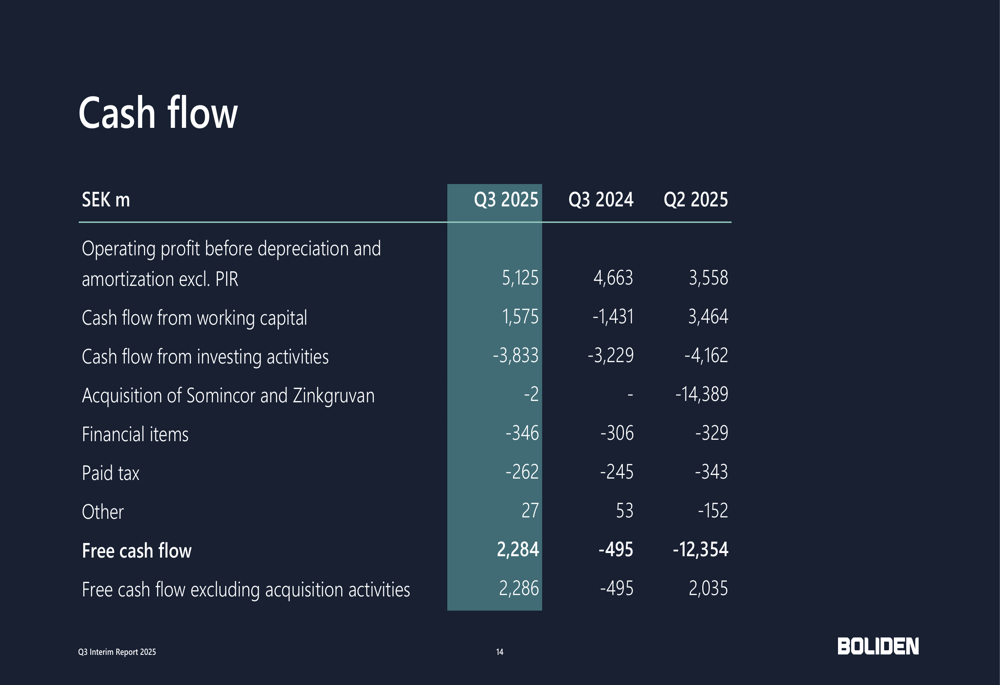

Cash Flow and Capital Structure

One of the quarter’s most significant achievements was the strong free cash flow generation of SEK 2,284 million, a substantial improvement from negative SEK 495 million in Q3 2024. This improvement was driven by better operating performance and a positive contribution from working capital.

The detailed cash flow statement below shows the key components contributing to this improvement:

Boliden maintained a solid capital structure with a net debt/equity ratio of 25%, slightly higher than the 24% reported a year earlier but improved from 29% in the previous quarter. This reflects the company’s continued focus on financial discipline despite ongoing investments in growth projects.

The company’s balance sheet remains robust with total assets of SEK 136.9 billion and equity of SEK 72.8 billion as of September 30, 2025. The average interest rate on debt decreased to 3.8% from 4.8% a year earlier, providing some relief on financing costs.

As Boliden continues to execute its strategic initiatives while navigating market volatility and regulatory challenges, investors will be closely watching the progress of key expansion projects and the company’s ability to maintain strong cash flow generation in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.