Park Ha Biological Technology stock rises on upcoming ticker symbol change

Colabor Group Inc. (TSX:GCL) released its third-quarter 2025 earnings presentation on October 17, revealing a complex financial picture marked by strong revenue growth but significant profitability challenges. The company’s stock plummeted nearly 58% following the announcement as investors reacted to a substantial net loss and increasing debt levels.

Executive Summary

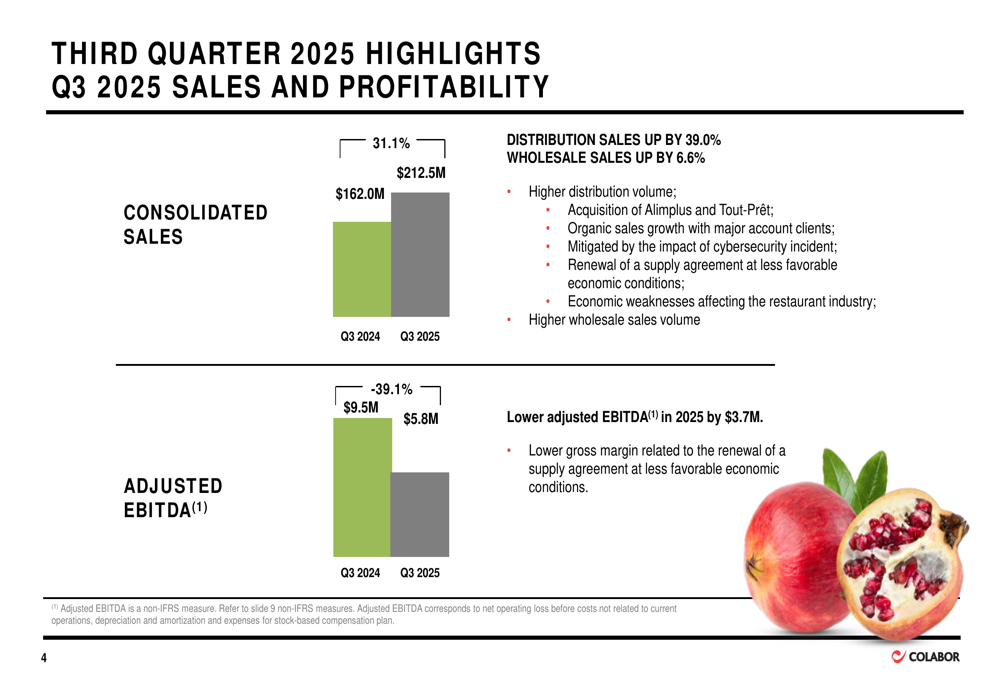

Colabor, Quebec’s largest food service operator, reported a 31.1% increase in consolidated sales to $212.5 million for Q3 2025, compared to $162.0 million in the same period last year. However, this growth was overshadowed by a net loss of $74.4 million or $0.73 per share, a dramatic reversal from the $1.1 million profit reported in Q3 2024.

The company’s presentation highlighted "Growth and Resiliency" despite facing several challenges, including a cybersecurity incident that caused an $8 million revenue loss and the need for forbearance agreements with lenders extending until January 30, 2026. Additionally, the company announced the nomination of Kelly Shipway as CEO on October 16, 2025.

As shown in the following chart detailing the company’s sales and profitability metrics:

Quarterly Performance Highlights

Distribution sales saw a significant 39.0% increase, while wholesale sales grew by 6.6%. The company attributed the distribution growth to higher volume, the acquisitions of Alimplus and Tout-Prêt, and organic sales growth. These positive factors were partially offset by a supply agreement renewal at less favorable conditions and economic weaknesses in the restaurant industry.

Despite the revenue growth, adjusted EBITDA decreased by 39.1%, falling from $9.5 million in Q3 2024 to $5.8 million in Q3 2025. The adjusted EBITDA margin contracted significantly to 2.7%, down from 5.9% in the prior year.

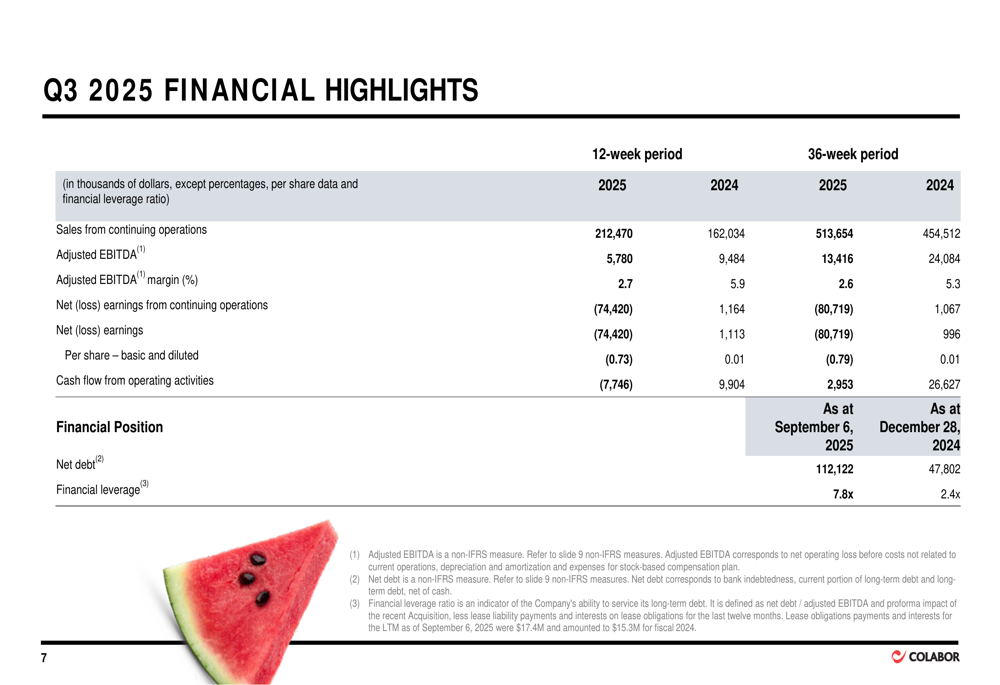

The company’s financial highlights table provides a comprehensive overview of these metrics:

Detailed Financial Analysis

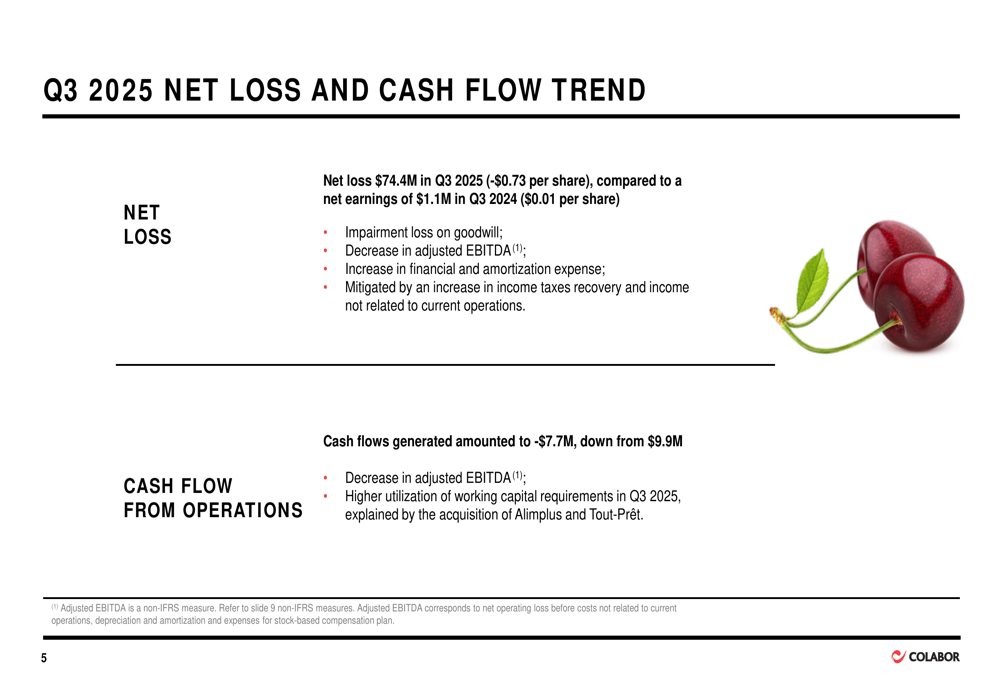

The substantial net loss of $74.4 million was primarily driven by an impairment loss on goodwill, decreased adjusted EBITDA, and increased financial and amortization expenses. Cash flow from operations turned negative at -$7.7 million, compared to a positive $9.9 million in Q3 2024, reflecting both the lower profitability and higher working capital utilization following recent acquisitions.

The following chart illustrates the company’s net loss and cash flow trends:

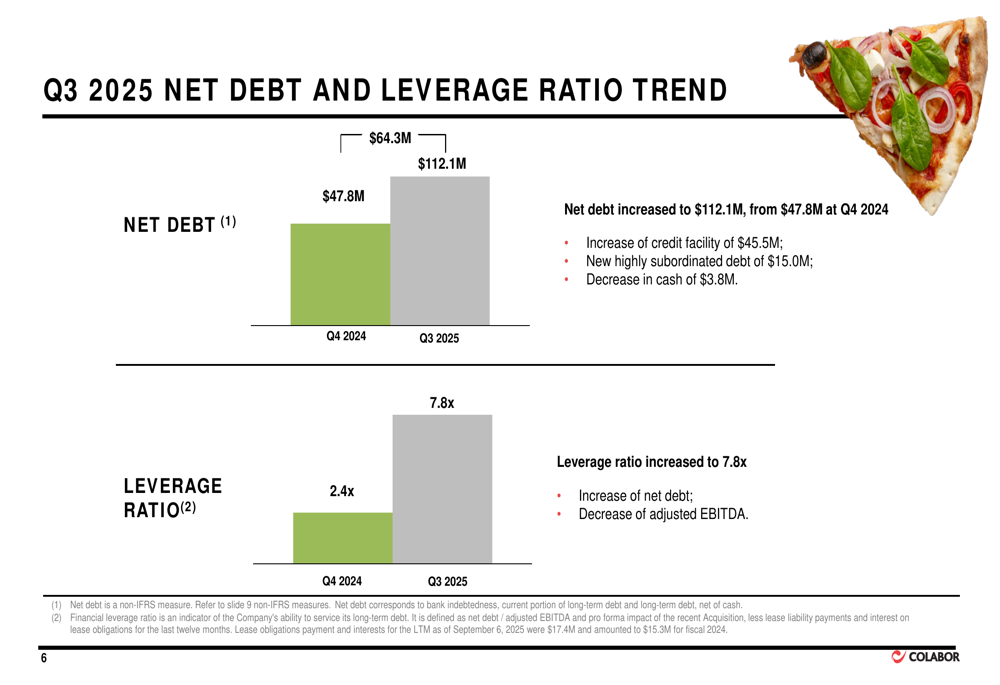

Colabor’s debt position deteriorated significantly during the quarter. Net debt increased to $112.1 million from $47.8 million at the end of Q4 2024, representing an increase of more than 134%. This was driven by a $45.5 million increase in the credit facility and $15.0 million in new highly subordinated debt. Consequently, the leverage ratio jumped to 7.8x from 2.4x previously.

The company’s debt and leverage position is illustrated in this chart:

Strategic Initiatives

Colabor is undertaking several strategic initiatives to address its financial challenges. The company plans to gradually close Alimplus facilities in Drummondville and Anjou by the end of November 2025 and January 2026, respectively, as part of its integration efforts following recent acquisitions.

The appointment of Kelly Shipway as CEO on October 16, 2025, represents a leadership change that comes at a critical juncture for the company. According to the earnings article, management views fiscal 2025 as a "transition year," with expectations for stronger profitability in 2026.

The company aims to achieve $12 million in cost synergies through the integration of recent acquisitions and plans to raise $15 million in equity. Additionally, Colabor intends to convert its cash flow loan to an asset-backed loan, indicating a strategic shift in financial management.

Forward-Looking Statements

Despite the current challenges, Colabor’s presentation attempts to position the company for future recovery. However, investors appear skeptical, as evidenced by the sharp stock price decline following the earnings release. According to real-time data, Colabor’s stock fell by 57.94% to trade near its 52-week low of $0.13, far from its high of $1.25.

The company faces several ongoing risks, including cybersecurity threats, market pressures in the foodservice sector, high financial leverage, integration challenges with recent acquisitions, and persistent margin pressures. The forbearance agreements with lenders until January 2026 provide some breathing room, but underscore the severity of the company’s financial situation.

As Colabor works to stabilize its operations and financial health, investors will be closely watching whether the company can successfully integrate its acquisitions, realize the promised synergies, and reverse the negative trends in profitability and cash flow that dominated this quarter’s results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.