Street Calls of the Week

Introduction & Market Context

Danish logistics giant DSV A/S presented its third-quarter 2025 results on October 23, highlighting the successful integration of Schenker and strong cash flow generation despite challenging market conditions. The company’s stock responded positively, rising 5.49% following the presentation, as investors welcomed progress on synergy realization and debt reduction efforts.

DSV’s performance comes amid a complex global logistics landscape characterized by trade tariffs, macroeconomic uncertainty, and geopolitical tensions affecting freight volumes, particularly in sea freight and European road transport.

Schenker Integration Progress

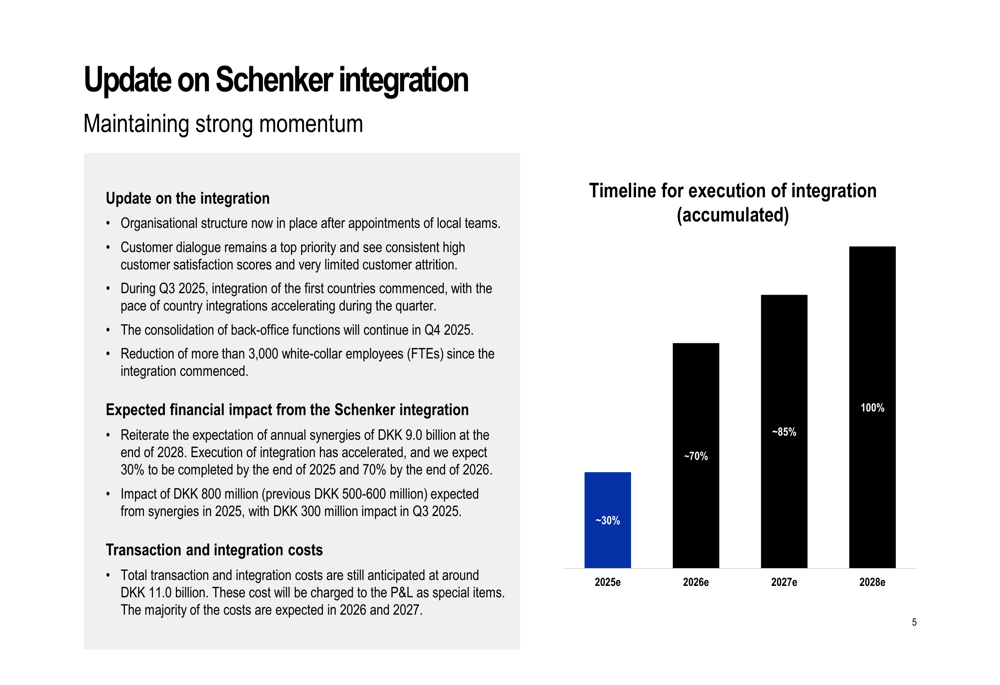

A central theme of DSV’s presentation was the accelerating integration of Schenker, with management emphasizing strong momentum and positive customer feedback. The company has already reduced white-collar staff by over 3,000 employees since the integration began, while maintaining high customer satisfaction scores and experiencing minimal customer attrition.

As shown in the following integration timeline chart, DSV expects to realize approximately 30% of planned synergies by the end of 2025, accelerating to 70% by the end of 2026:

The company has increased its expected synergies for 2025 to DKK 800 million (up from DKK 500-600 million previously), with DKK 300 million already realized in Q3. DSV continues to target total annual synergies of DKK 9 billion by the end of 2028, while estimating total transaction and integration costs at around DKK 11 billion.

Quarterly Performance Highlights

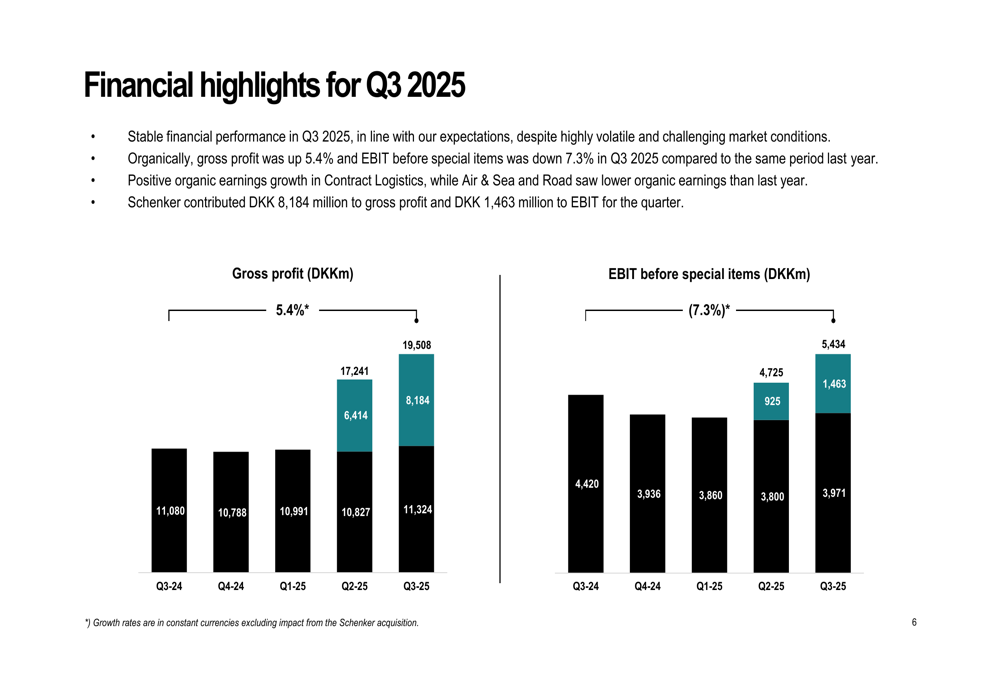

DSV reported solid financial results for Q3 2025, with Schenker contributing significantly to the top and bottom lines. The following chart illustrates the company’s gross profit and EBIT performance over recent quarters:

Gross profit reached DKK 19,508 million in Q3 2025, compared to DKK 11,080 million in the same period last year. EBIT before special items totaled DKK 5,434 million, up from DKK 4,420 million in Q3 2024. Organically (excluding Schenker’s contribution), gross profit increased by 5.4% while EBIT before special items declined by 7.3% in constant currencies.

The Q3 highlights slide summarizes key achievements across financial performance and integration progress:

Detailed Financial Analysis

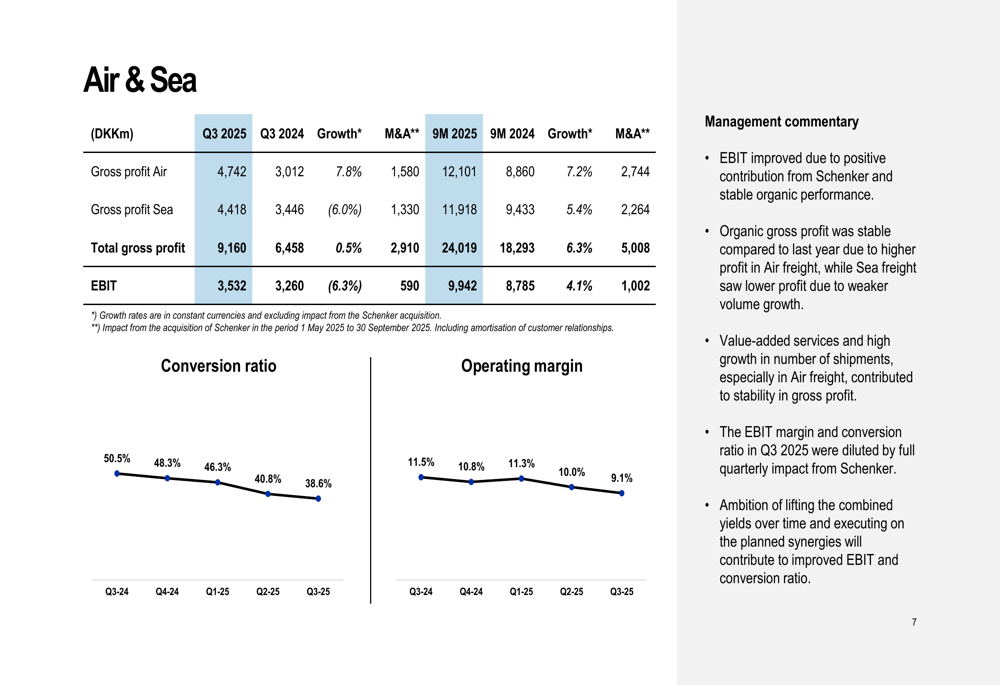

Performance varied across DSV’s business segments, reflecting different market dynamics and integration impacts:

Air & Sea

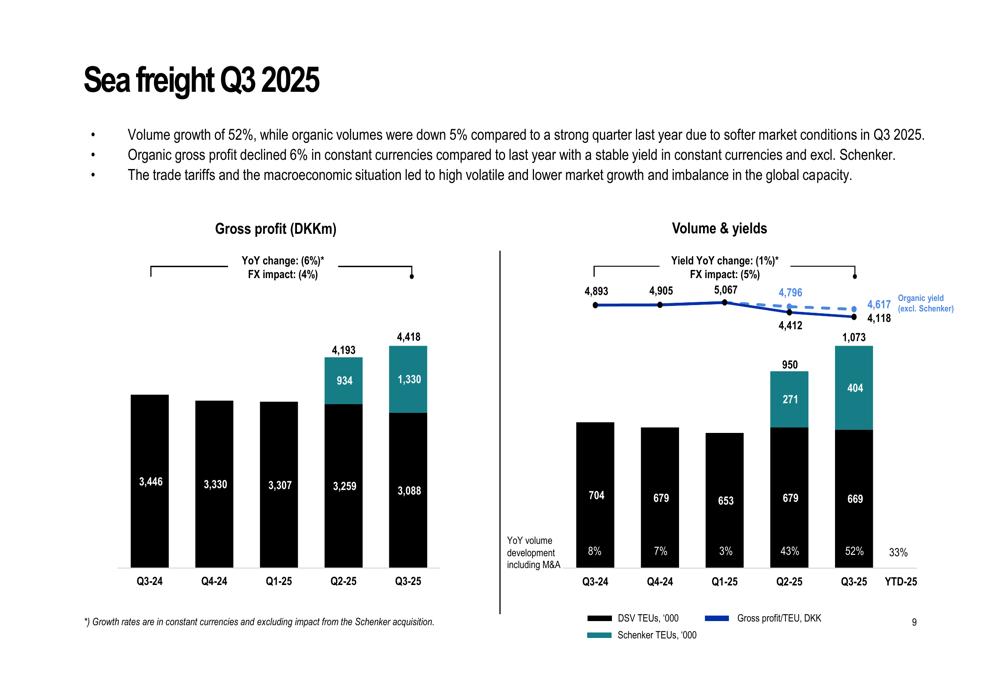

The Air & Sea division saw stable organic gross profit (+0.5%) but experienced a 6.3% decline in organic EBIT. Air freight volumes grew 64% including Schenker’s contribution, with organic gross profit up 8%, while sea freight volumes increased 52% but faced challenges with organic volumes down 5% compared to a strong Q3 2024.

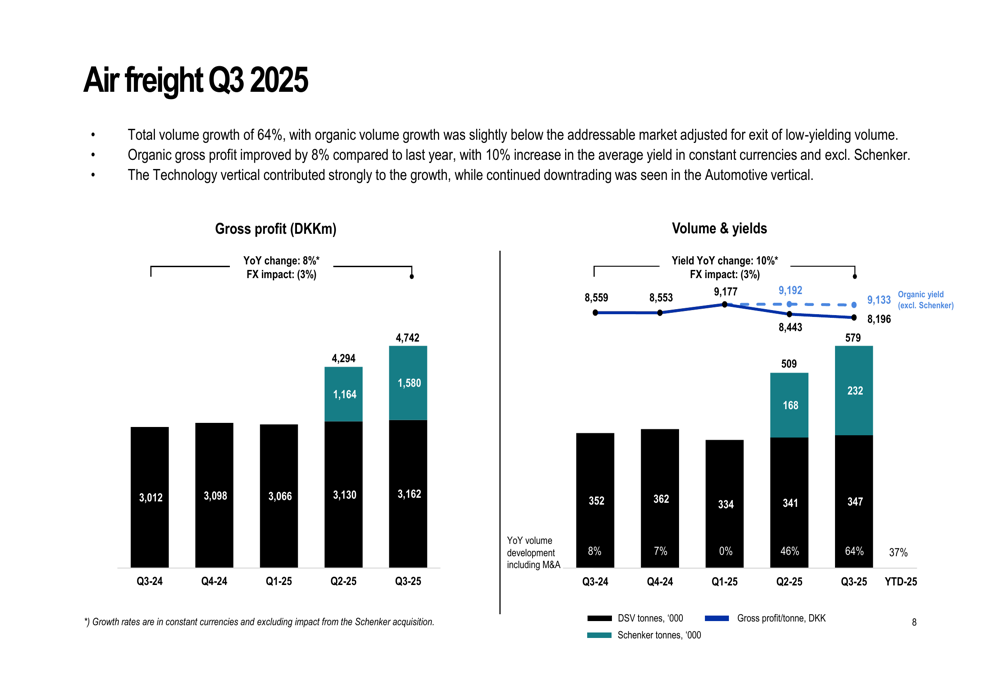

In air freight, the technology vertical contributed strongly to growth, with average yields increasing 10% in constant currencies (excluding Schenker):

Sea freight faced more challenging conditions due to trade tariffs and macroeconomic headwinds creating volatility and capacity imbalances:

Road

The Road segment benefited from Schenker’s contribution but saw organic declines in both gross profit (-3.6%) and EBIT (-15.6%). Management noted signs of market stabilization but highlighted continued softness in European markets, especially in domestic groupage and the automotive sector.

Contract Logistics

Contract Logistics emerged as the strongest performer, with organic EBIT growth of 10.4% alongside Schenker’s contribution. Revenue growth was driven by the technology vertical and increased business from major customers, while improved utilization rates supported gross profit margins.

Cash Flow and Debt Reduction

DSV demonstrated strong financial discipline with impressive cash flow generation and progress on deleveraging. The company reported adjusted free cash flow of DKK 4,276 million in Q3 2025, achieving a cash conversion rate of 96%.

Working capital management improved significantly, with net working capital reduced to DKK 5,018 million, representing just 1.7% of revenue including Schenker. Most notably, DSV reduced its net interest-bearing debt by more than DKK 4 billion during the quarter to DKK 89.0 billion, advancing its deleveraging plan following the Schenker acquisition.

Forward-Looking Statements

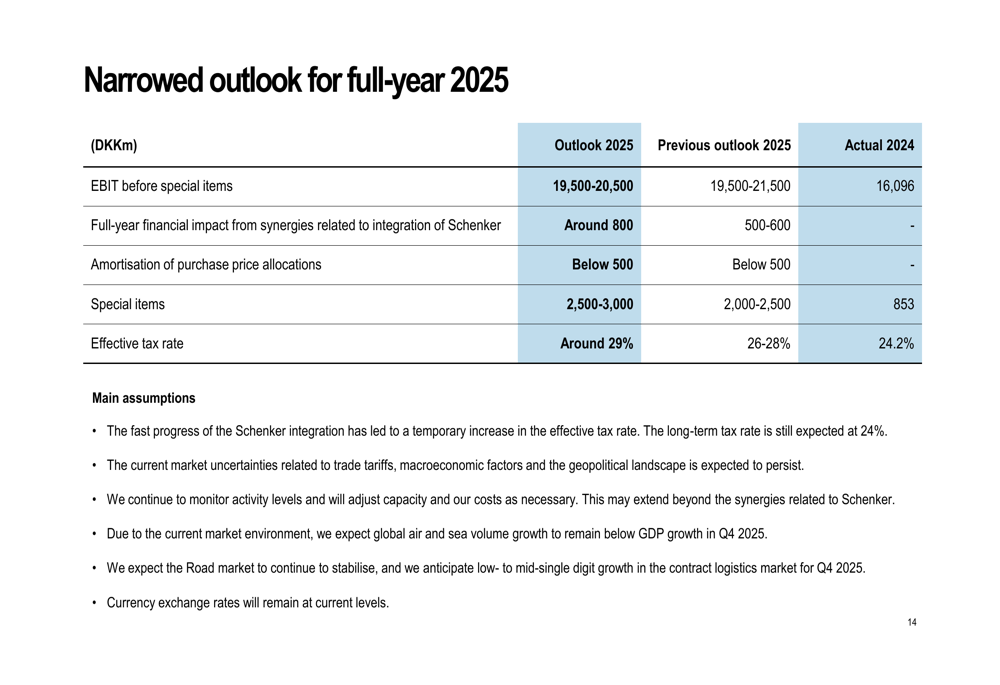

DSV narrowed its full-year 2025 guidance, providing the following updated outlook compared to previous estimates:

The company now expects EBIT before special items to range between DKK 19,500-20,500 million, compared to the previous range of DKK 19,500-21,500 million. Special items are projected at DKK 2,500-3,000 million, reflecting higher integration costs as the process accelerates.

Management highlighted three key assumptions underlying this outlook:

1. A temporary increase in the effective tax rate due to accelerated Schenker integration

2. Persistent market uncertainties related to trade tariffs, macroeconomic factors, and geopolitical tensions

3. Continued monitoring of activity levels with potential cost adjustments beyond Schenker synergies

Executive Summary

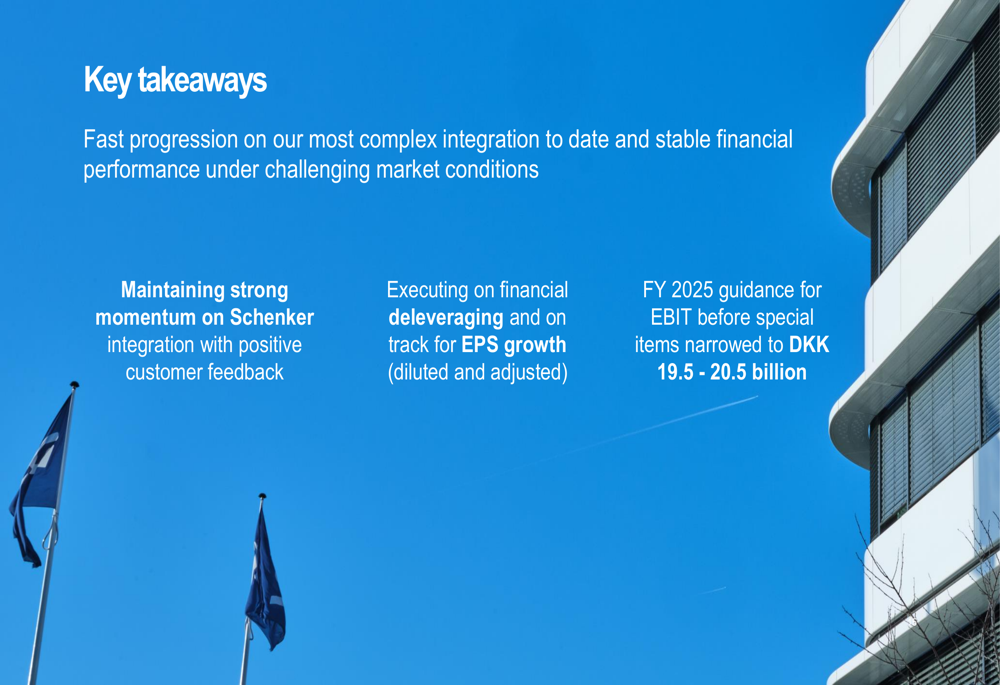

DSV’s Q3 2025 presentation concluded with these key takeaways, emphasizing the balance between integration execution and financial performance:

CEO Jens Lund’s comment from the earnings call reinforces this message: "We are off to a good start when it comes to the combination of the company and the financial performance." The CFO added confidence regarding synergy targets, stating: "We can promise you that we will deliver at least the $4 billion, and we will work whatever we can to make that faster and higher."

As DSV continues to integrate Schenker while navigating challenging market conditions, investors appear encouraged by the company’s execution capabilities and financial discipline, reflected in the positive stock price movement following the results presentation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.