Street Calls of the Week

Introduction & Market Context

EchoStar Corporation (NASDAQ:SATS) released its Q2 2025 earnings presentation on August 1, 2025, revealing a company navigating significant challenges across most business segments while finding growth in its wireless operations. The company’s stock reacted with a modest decline of 1.18% in aftermarket trading, falling to $73.97, as investors digested mixed results that showed revenue pressure but some encouraging operational metrics.

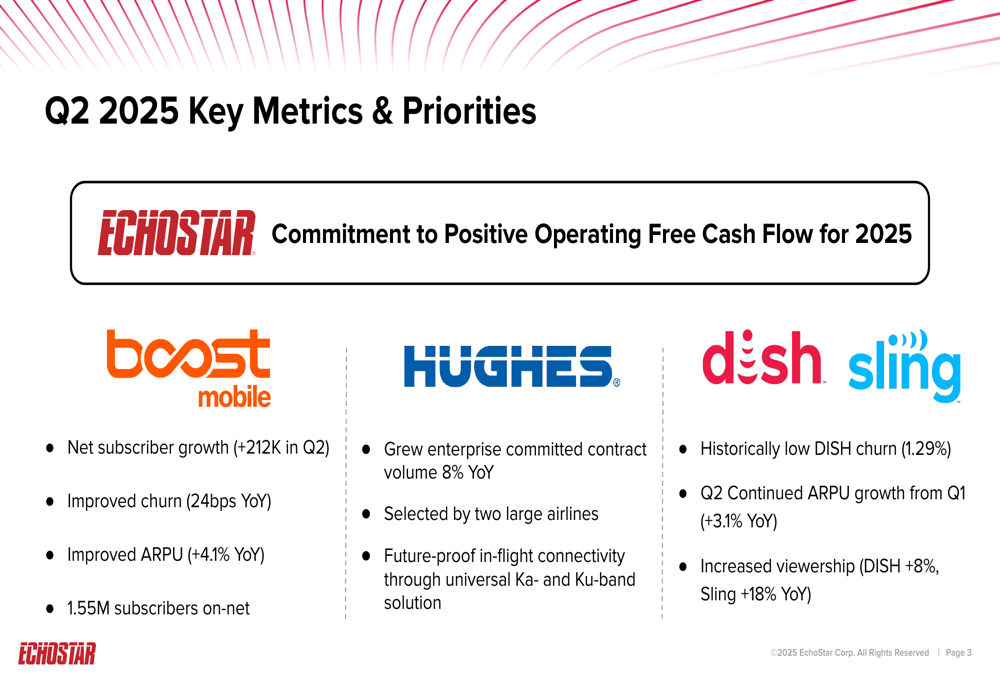

The presentation highlighted EchoStar’s commitment to achieving positive operating free cash flow for 2025, despite reporting negative free cash flow for the quarter. With a market capitalization of approximately $21.6 billion and facing intense competition across its business segments, EchoStar continues to balance its legacy Pay-TV operations with growth initiatives in wireless and satellite services.

Quarterly Performance Highlights

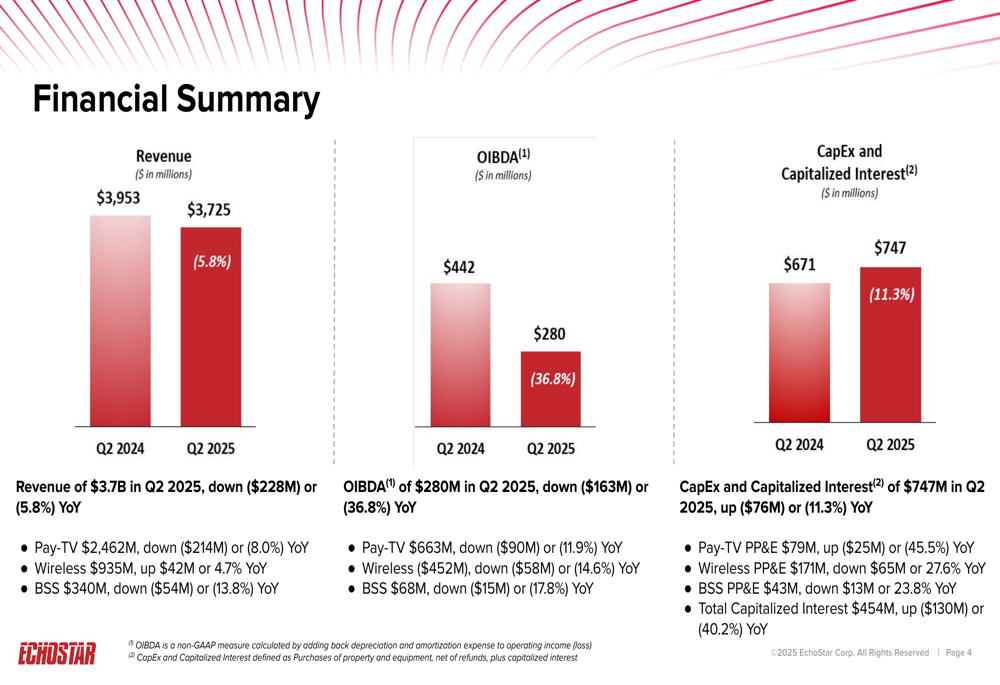

EchoStar’s Q2 2025 financial results showed broad revenue declines offset partially by growth in the wireless segment. The company reported total revenue of $3.7 billion, representing a year-over-year decrease of 5.8%. Operating Income Before Depreciation and Amortization (OIBDA) fell to $280 million, down 36.8% compared to the same period last year.

As shown in the following key metrics summary:

The company highlighted several positive developments across its business units. Boost Mobile achieved net subscriber growth of 212,000 in Q2, improved churn by 24 basis points year-over-year, and increased Average Revenue Per User (ARPU) by 4.1%. The Hughes enterprise segment grew its committed contract volume by 8% year-over-year, while DISH TV reported historically low churn of 1.29% and ARPU growth of 3.1%.

Detailed Financial Analysis

The financial summary reveals significant challenges across EchoStar’s business segments, with revenue and OIBDA declining in most areas:

Revenue declined across two of three major segments, with Pay-TV revenue falling 8.0% to $2.46 billion and Broadband & Satellite Services (BSS) revenue dropping 13.8% to $340 million. The wireless segment was the sole bright spot, with revenue increasing 4.7% to $935 million.

OIBDA declined across all segments, with total OIBDA falling 36.8% to $280 million. The company also reported increased capital expenditures and capitalized interest of $747 million, up 11.3% year-over-year, primarily due to a 40.2% increase in capitalized interest to $454 million.

Segment Performance Analysis

Wireless Segment

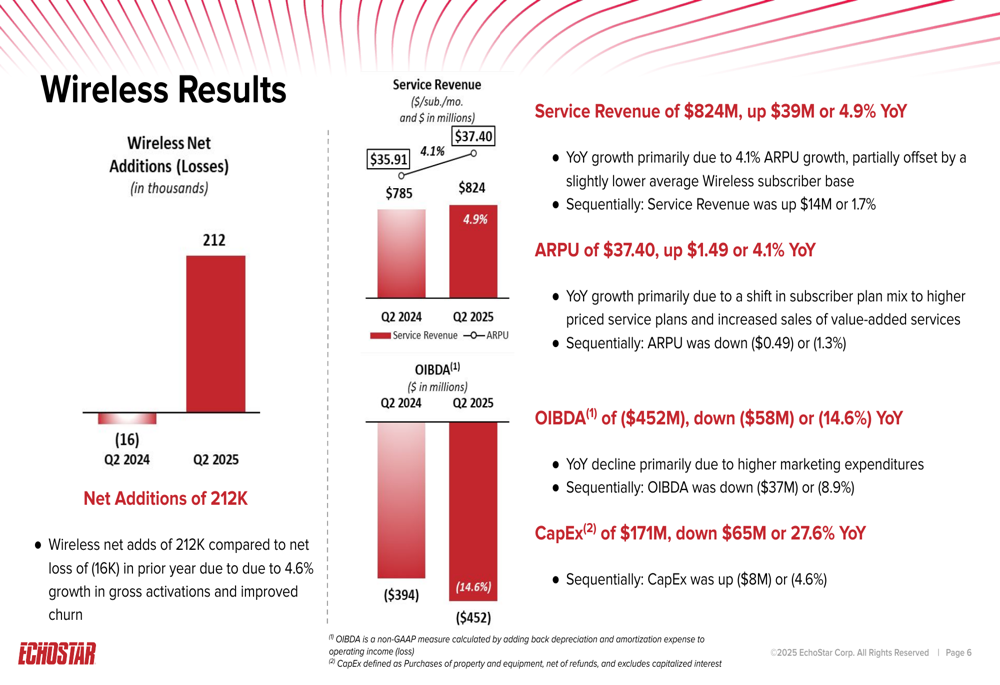

The wireless segment demonstrated the strongest performance among EchoStar’s business units:

Wireless net additions reached 212,000 in Q2 2025, a significant improvement from the net loss of 16,000 subscribers in the prior year. This growth was attributed to a 4.6% increase in gross activations and improved customer retention. Service revenue grew 4.9% year-over-year to $824 million, driven primarily by ARPU growth of 4.1% to $37.40, as customers shifted to higher-priced service plans.

However, wireless OIBDA declined 14.6% to $452 million due to higher marketing expenditures. Capital expenditures in the wireless segment decreased 27.6% year-over-year to $171 million.

Pay-TV Segment

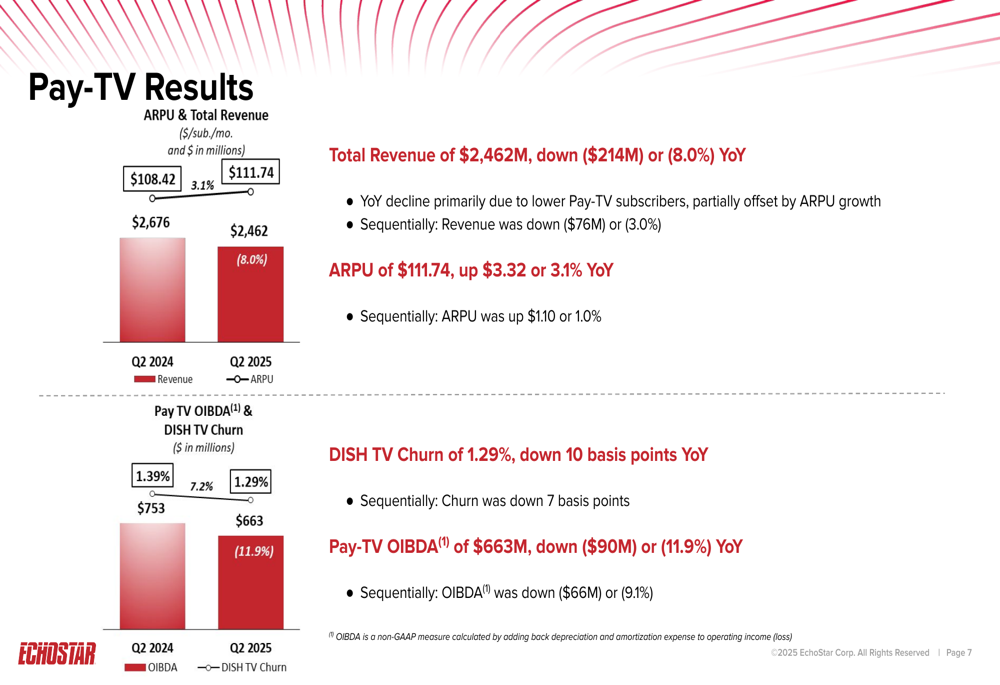

The Pay-TV segment continued to face challenges from cord-cutting and increased competition:

Total Pay-TV revenue fell 8.0% year-over-year to $2.46 billion, primarily due to lower subscriber counts, though partially offset by ARPU growth of 3.1% to $111.74. DISH TV churn improved to 1.29%, down 10 basis points year-over-year, representing a historically low level. Despite this operational improvement, Pay-TV OIBDA declined 11.9% to $663 million.

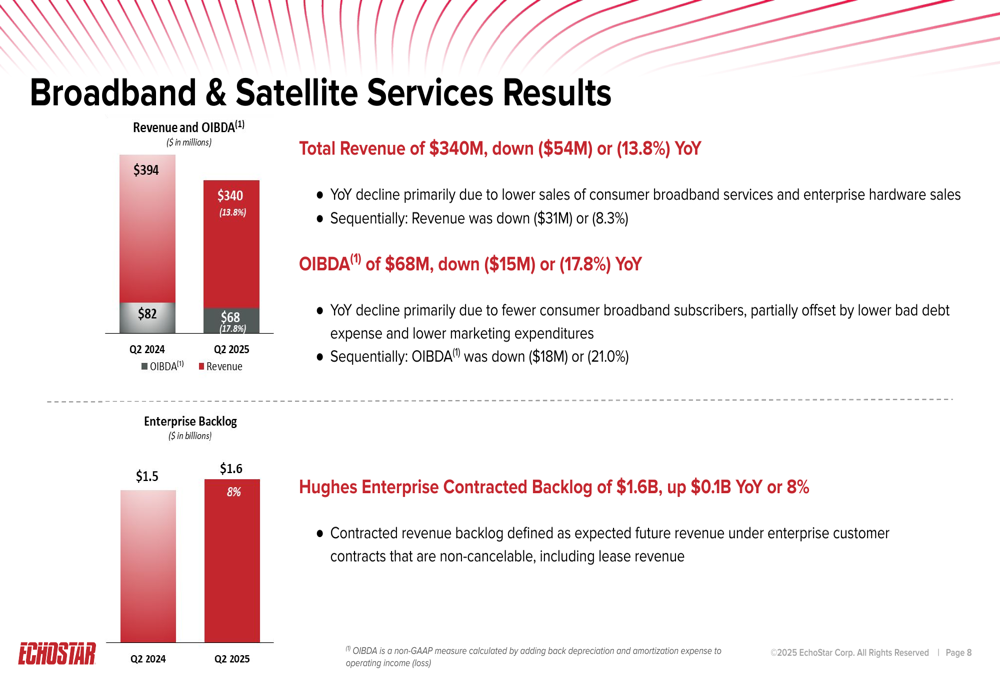

Broadband & Satellite Services

The BSS segment showed mixed results with declining consumer services but growing enterprise backlog:

BSS revenue decreased 13.8% year-over-year to $340 million, primarily due to lower sales of consumer broadband services. OIBDA fell 17.8% to $68 million. However, the Hughes Enterprise Contracted Backlog grew 8% year-over-year to $1.6 billion, suggesting potential future revenue stability from enterprise customers.

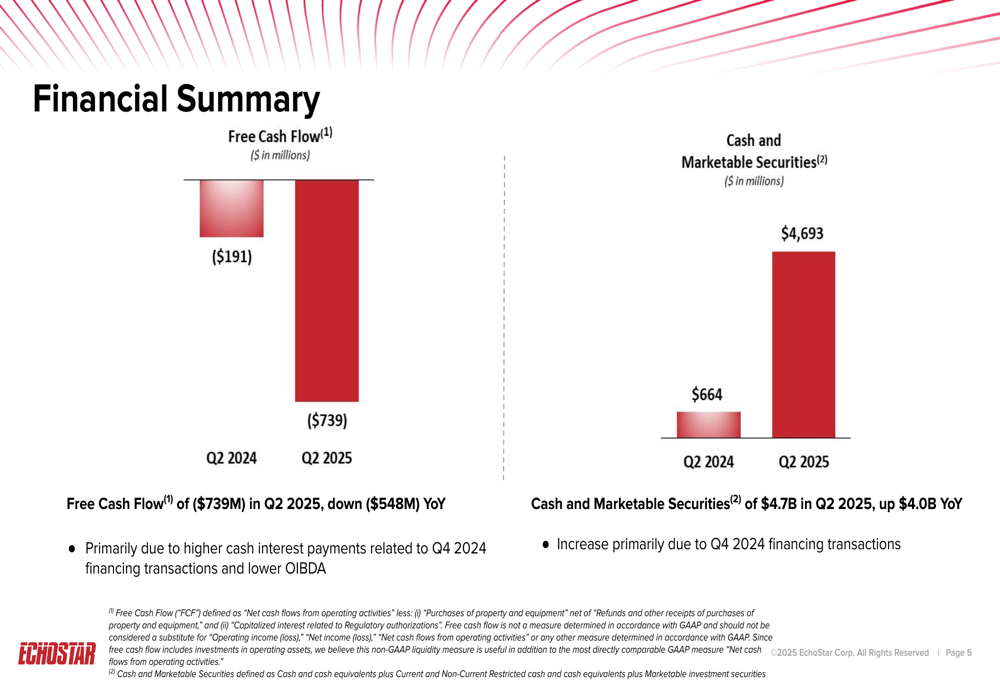

Cash Flow and Debt Position

EchoStar’s cash flow and liquidity position showed significant pressures in Q2 2025:

Free cash flow was negative $739 million in Q2 2025, deteriorating by $548 million compared to the same period last year. This decline was primarily attributed to higher cash interest payments related to financing transactions completed in Q4 2024, as well as lower OIBDA.

The company’s cash and marketable securities position stood at $4.7 billion, a substantial increase of $4.0 billion year-over-year, primarily resulting from the Q4 2024 financing transactions. However, this increased cash position comes with higher debt service costs that are pressuring free cash flow.

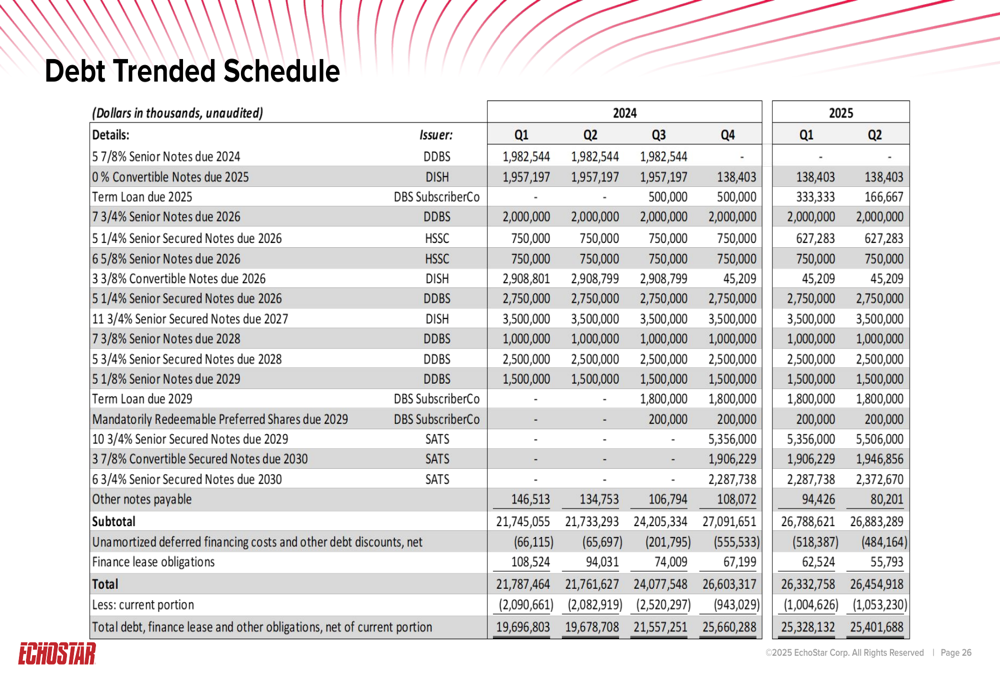

The company’s debt structure shows significant obligations coming due in the near term:

Forward-Looking Statements

Despite the challenging quarter, EchoStar maintained its commitment to achieving positive operating free cash flow for the full year 2025. The company’s presentation emphasized operational improvements in wireless subscriber metrics and enterprise backlog growth as foundations for future performance.

According to the earnings call, EchoStar is also developing a new LEO satellite constellation for direct-to-device services, with launch planned for 2028 and commercial services expected by 2029. This project, requiring approximately $5 billion in peak funding, represents a significant strategic initiative for the company’s long-term growth.

President and CEO Hamid Akhavan emphasized the company’s unique position in the satellite connectivity market during the earnings call, stating, "We are the unique one everybody that today." He also highlighted EchoStar’s collaborative approach with carriers, leveraging their customer relationships for market expansion.

While EchoStar faces significant challenges in its traditional business segments, the company’s wireless subscriber growth and enterprise backlog expansion provide some optimism amid broader revenue and profitability pressures. The market’s relatively muted reaction to the earnings suggests investors are taking a wait-and-see approach to EchoStar’s efforts to balance near-term cash flow commitments with longer-term strategic investments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.