5 big analyst AI moves: Apple lifted to Buy, AI chip bets reassessed

Introduction & Market Context

Fortis Inc. (NYSE:FTS) presented its second quarter 2025 earnings results on August 1, 2025, reporting solid financial performance with earnings per share (EPS) of $0.76, up 13.4% from $0.67 in the same period last year. The North American utility company continues to execute on its long-term growth strategy while advancing clean energy initiatives and expanding its customer base.

The company’s shares closed at $48.97 on July 31, 2025, near its 52-week high of $50.06, reflecting investor confidence in Fortis’s regulated business model and consistent dividend growth track record.

Quarterly Performance Highlights

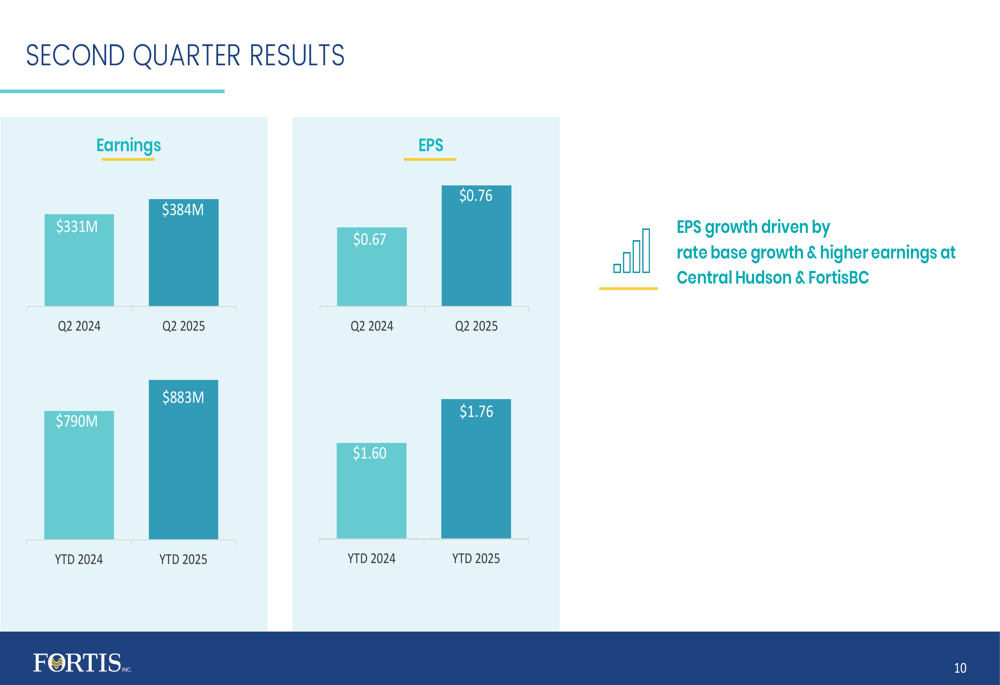

Fortis reported Q2 2025 earnings of $384 million, up from $331 million in Q2 2024, while year-to-date earnings reached $883 million compared to $790 million in the prior year period. The company’s EPS for the first half of 2025 increased to $1.76, a 10% improvement from $1.60 in the same period of 2024.

As shown in the following chart of quarterly earnings and EPS results:

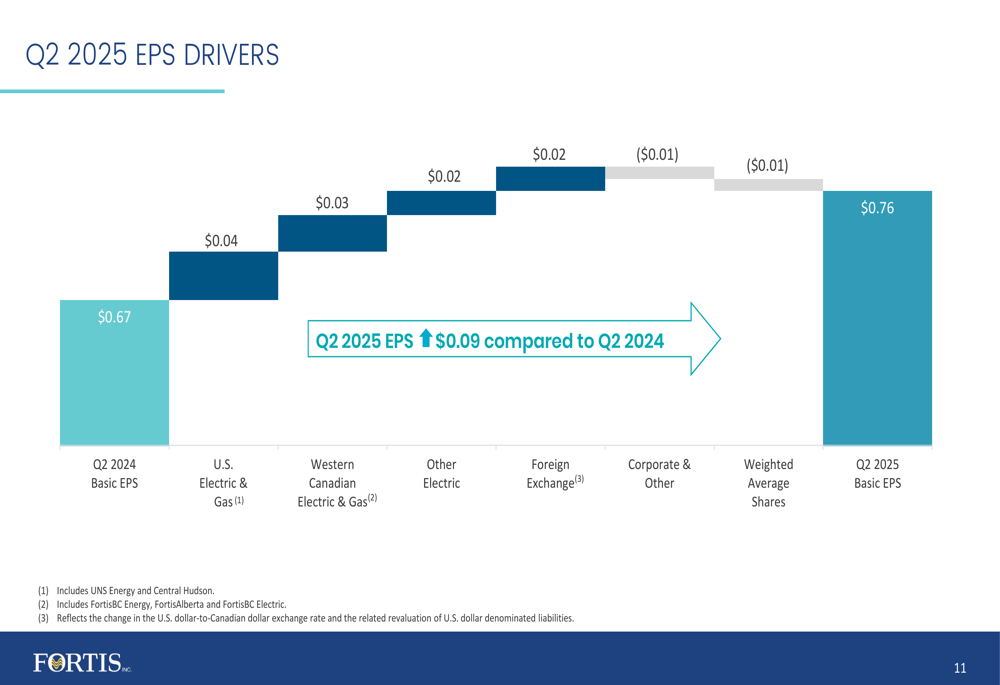

The EPS growth was primarily driven by rate base growth and higher earnings at Central Hudson (NYSE:HUD) and FortisBC. A detailed breakdown of the Q2 2025 EPS drivers shows contributions from U.S. Electric & Gas ($0.04), Western Canadian Electric & Gas ($0.03), Other Electric ($0.02), and Foreign Exchange ($0.02), partially offset by Corporate & Other (-$0.01) and Weighted Average Shares (-$0.01).

The following waterfall chart illustrates these EPS drivers:

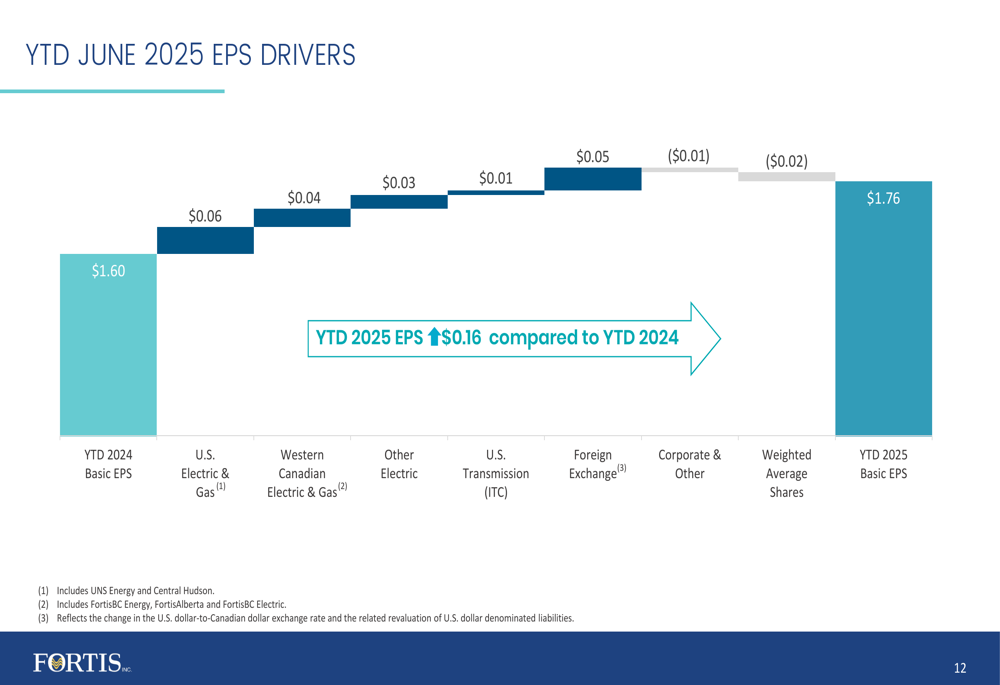

Year-to-date EPS drivers show a similar pattern with additional positive contributions from U.S. Transmission ITC (NSE:ITC):

Capital Investment and Growth Strategy

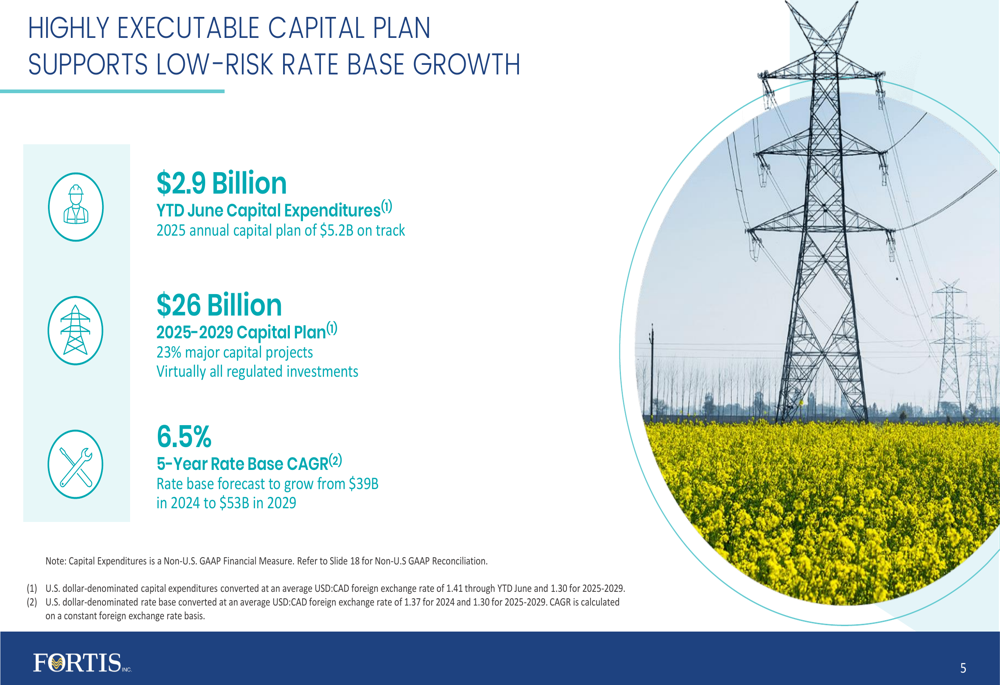

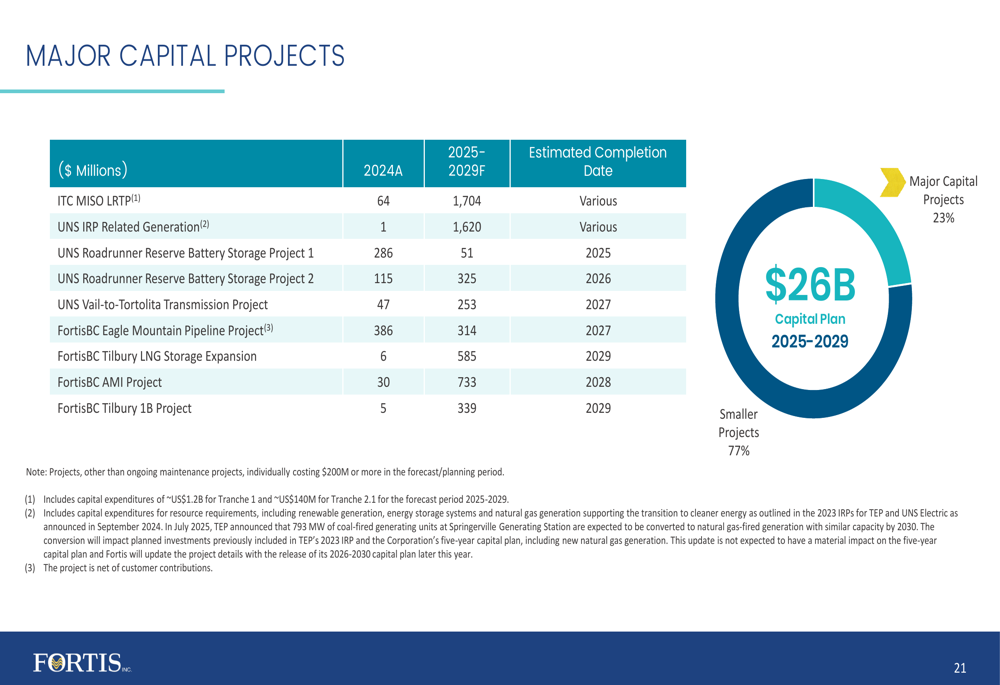

Fortis has invested $2.9 billion in capital expenditures year-to-date through June 2025, keeping pace with its $5.2 billion annual capital plan. The company’s five-year capital plan (2025-2029) totals $26 billion, with virtually all investments in regulated assets. This is expected to drive a 6.5% compound annual growth rate (CAGR) in rate base from $39 billion in 2024 to $53 billion by 2029.

The company’s capital investment strategy is illustrated in this slide:

Major capital projects represent 23% of the total five-year capital plan, with significant investments in ITC MISO LRTP ($1,704 million), UNS IRP-related generation ($1,620 million), and various other transmission and LNG projects. The remaining 77% consists of smaller, recurring capital investments across Fortis’s service territories.

As shown in the following breakdown of major capital projects:

Strategic Initiatives

Fortis is advancing several strategic initiatives to drive growth beyond its base capital plan. A key opportunity highlighted in the presentation is a data center agreement for approximately 300 MW of power demand with a customer in Arizona, ramping up in 2027. This agreement has potential to expand to 600 MW at the initial site and an additional 500-700 MW at a subsequent location.

The company is also progressing on its clean energy transition, with plans to convert 793 MW of coal-fired generation at the Springerville Generating Station to natural gas by 2030. This supports Fortis’s commitment to achieve a coal-free generation mix by 2032 and reach net-zero direct emissions by 2050.

The sustainability leadership slide highlights the company’s progress:

Regulatory Developments

Fortis’s subsidiary Tucson Electric Power (TEP) filed a General Rate Application during the quarter, which will be an important regulatory proceeding to watch. Central Hudson also has an ongoing rate application in New York. These regulatory outcomes will impact the company’s ability to earn its allowed returns and recover costs associated with its capital investments.

Dividend Growth and Shareholder Returns

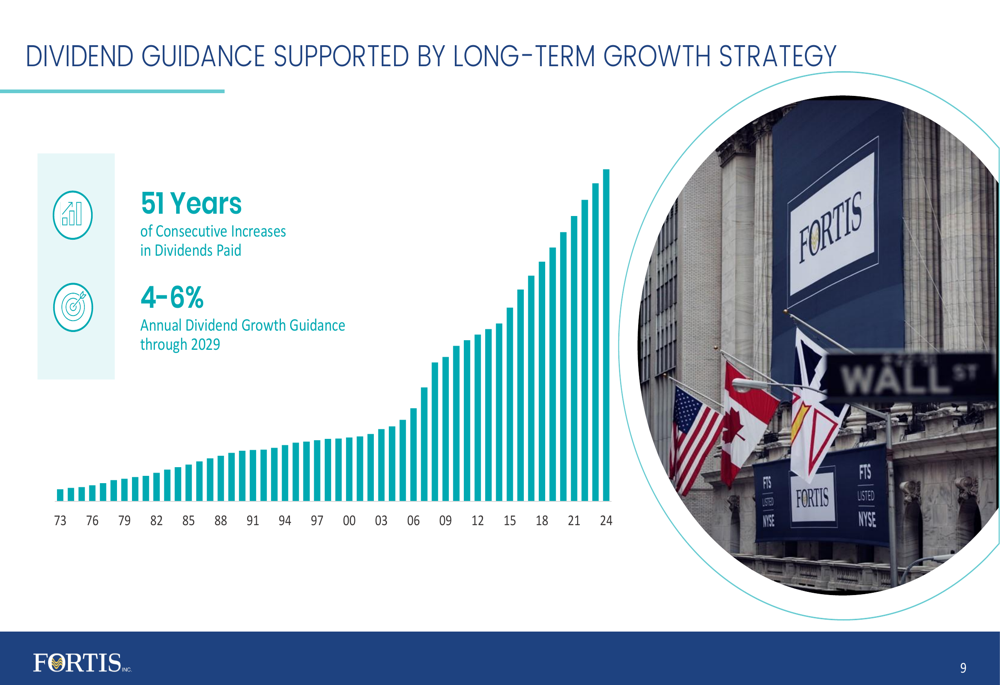

One of Fortis’s most compelling investment attributes is its 51-year track record of consecutive dividend increases. The company has provided guidance for continued annual dividend growth of 4-6% through 2029, supported by its regulated business model and predictable cash flows.

The following chart illustrates Fortis’s dividend growth history:

Financial Position

Fortis maintains strong investment-grade credit ratings from major rating agencies, including S&P Global (A-), Morningstar DBRS (A low), Fitch Ratings (BBB+), and Moody’s (Baa3). The company has managed its liquidity position with new long-term debt issuances for Central Hudson and Maritime Electric during the quarter.

Investment Thesis

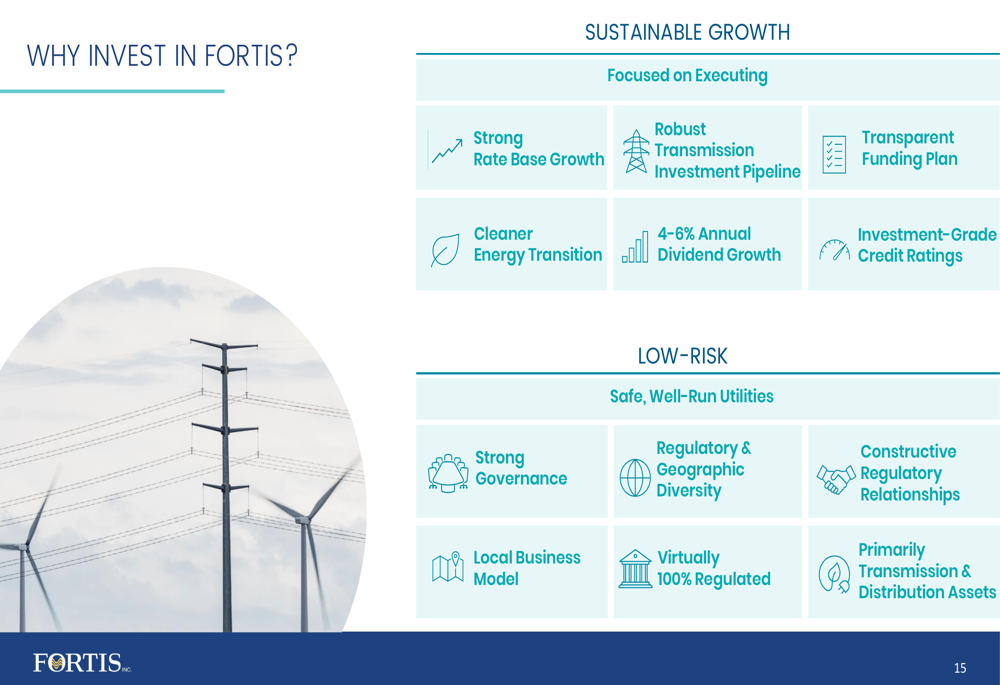

The presentation concluded with Fortis’s investment thesis, highlighting its combination of sustainable growth and low-risk profile. Key attributes include strong rate base growth, robust transmission investment pipeline, transparent funding plan, cleaner energy transition, and consistent dividend growth, all supported by investment-grade credit ratings and geographic diversity.

The investment case is summarized in this slide:

Outlook

Looking ahead, Fortis remains focused on executing its $26 billion capital plan while pursuing additional growth opportunities, particularly in transmission infrastructure and supporting data center expansion. The company’s regulated business model, geographic diversification, and focus on transmission and distribution assets position it well to navigate the evolving energy landscape while delivering consistent returns to shareholders.

With its strong Q2 2025 performance and clear long-term growth strategy, Fortis continues to offer investors a combination of current income through dividends and capital appreciation through rate base growth. The company’s next earnings release is scheduled for November 4, 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.