5 big analyst AI moves: Apple lifted to Buy, AI chip bets reassessed

Introduction & Market Context

Genuine Parts Company (NYSE:GPC), a global distributor of automotive and industrial parts, presented its third quarter 2025 earnings on October 21, showcasing resilient performance despite challenging market conditions. The company reported revenue of $6.3 billion, exceeding analyst expectations of $6.12 billion, while adjusted earnings per share of $1.98 fell slightly short of the anticipated $2.01.

The stock responded positively to the results, rising 2.2% to close at $134.72, as investors focused on the company’s revenue beat and improved full-year guidance. GPC continues to navigate a complex operating environment characterized by inflationary pressures and mixed demand signals across its global markets.

Quarterly Performance Highlights

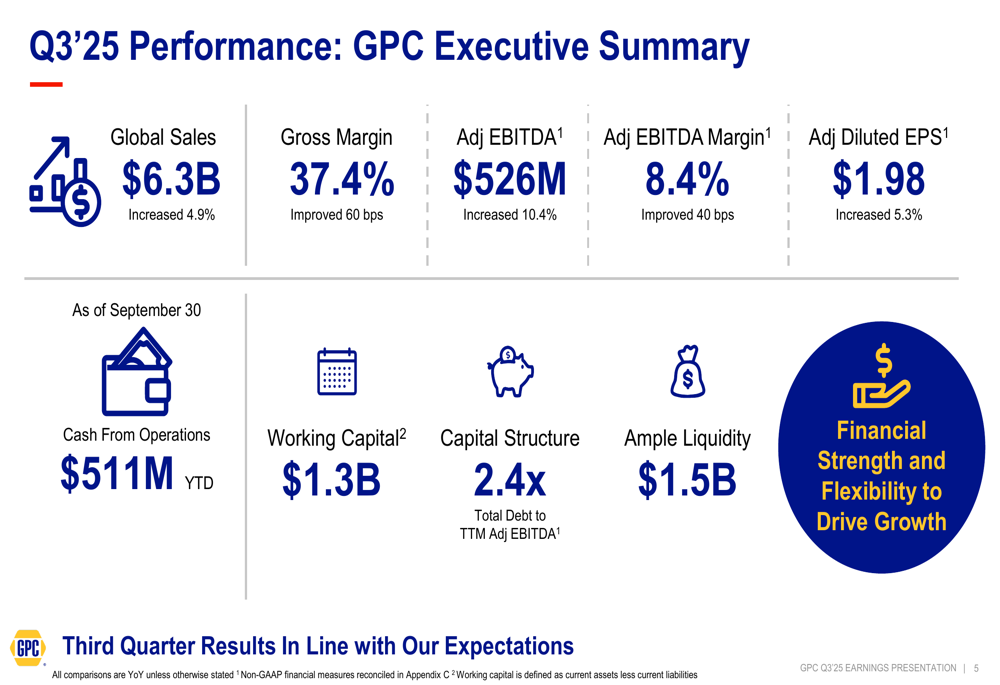

GPC delivered solid financial results for the third quarter, with global sales increasing 4.9% year-over-year to $6.3 billion. The company improved its gross margin by 60 basis points to 37.4% while adjusted EBITDA grew 10.4% to $526 million, representing an 8.4% margin improvement of 40 basis points compared to the prior year.

As shown in the following executive summary of GPC’s third quarter performance:

The company maintained a strong balance sheet with $1.5 billion in available liquidity and a healthy leverage ratio of 2.4x total debt to trailing twelve-month adjusted EBITDA. Year-to-date cash from operations reached $511 million, providing financial flexibility to support growth initiatives.

Segment Performance Analysis

GPC’s business is divided into two primary segments: Automotive, representing 63% of total revenue, and Industrial, accounting for the remaining 37%. Both segments demonstrated growth during the quarter despite varying market conditions.

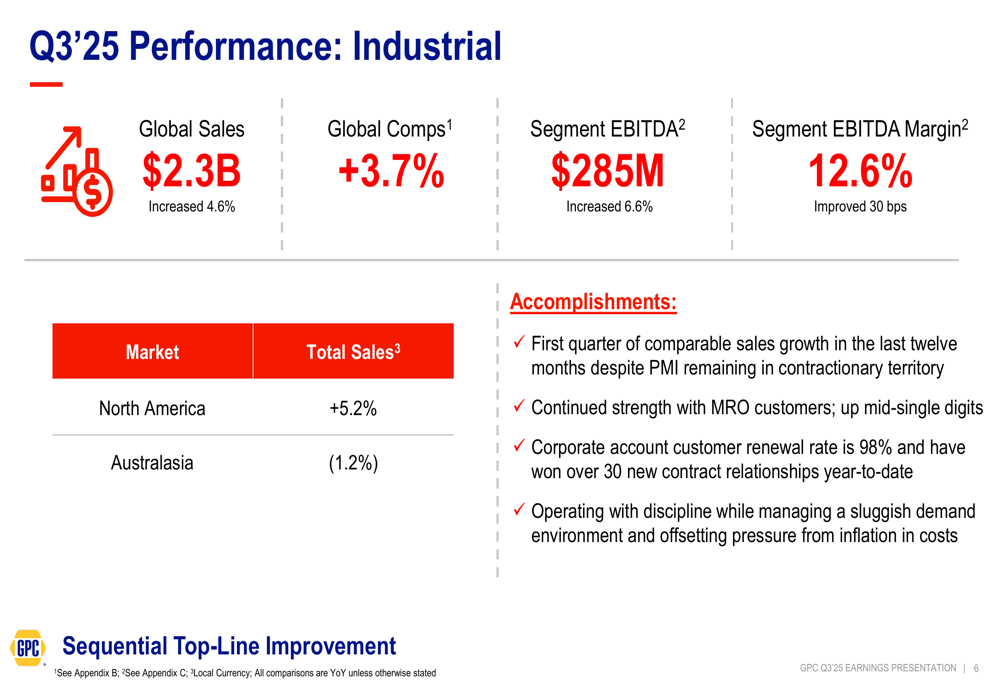

The Industrial segment showed encouraging signs of recovery with sales increasing 4.6% to $2.3 billion and comparable sales growth of 3.7%. This performance is particularly noteworthy given that the Purchasing Managers’ Index (PMI) remained in contractionary territory. Segment EBITDA increased 6.6% to $285 million, with margins improving 30 basis points to 12.6%.

The Industrial segment’s performance is detailed in the following slide:

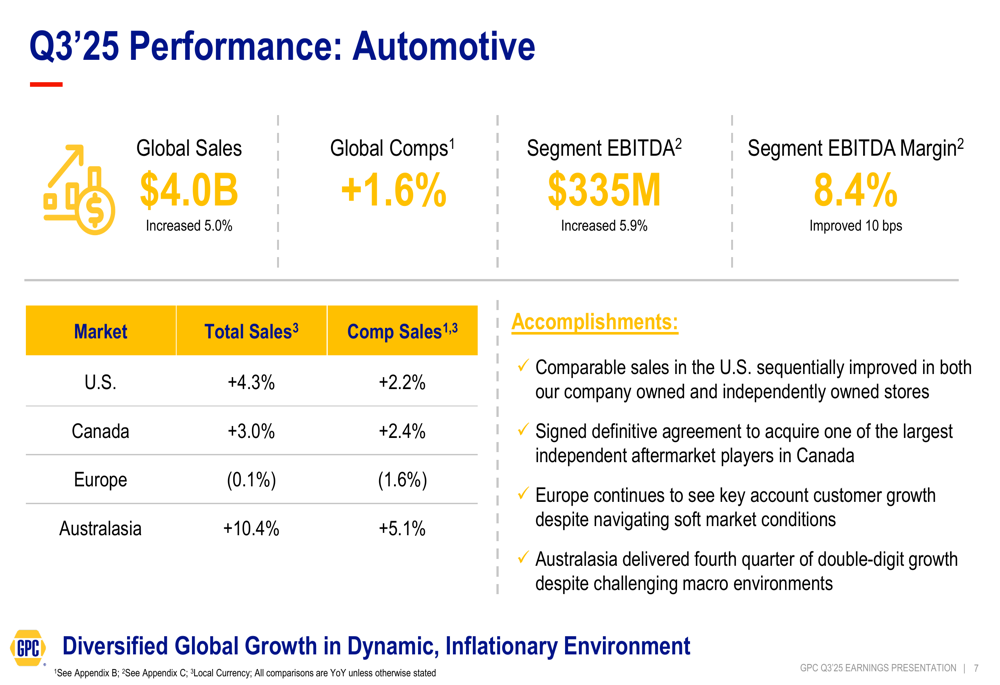

The Automotive segment delivered 5.0% sales growth, reaching $4.0 billion with comparable sales increasing 1.6%. Performance varied by region, with Australasia leading the way with 10.4% total sales growth and 5.1% comparable sales growth. The U.S. market showed sequential improvement with 4.3% total sales growth and 2.2% comparable sales growth. European operations faced more challenging conditions, with total sales declining slightly by 0.1% and comparable sales down 1.6%.

The following slide breaks down the Automotive segment’s performance by region:

Updated Guidance and Outlook

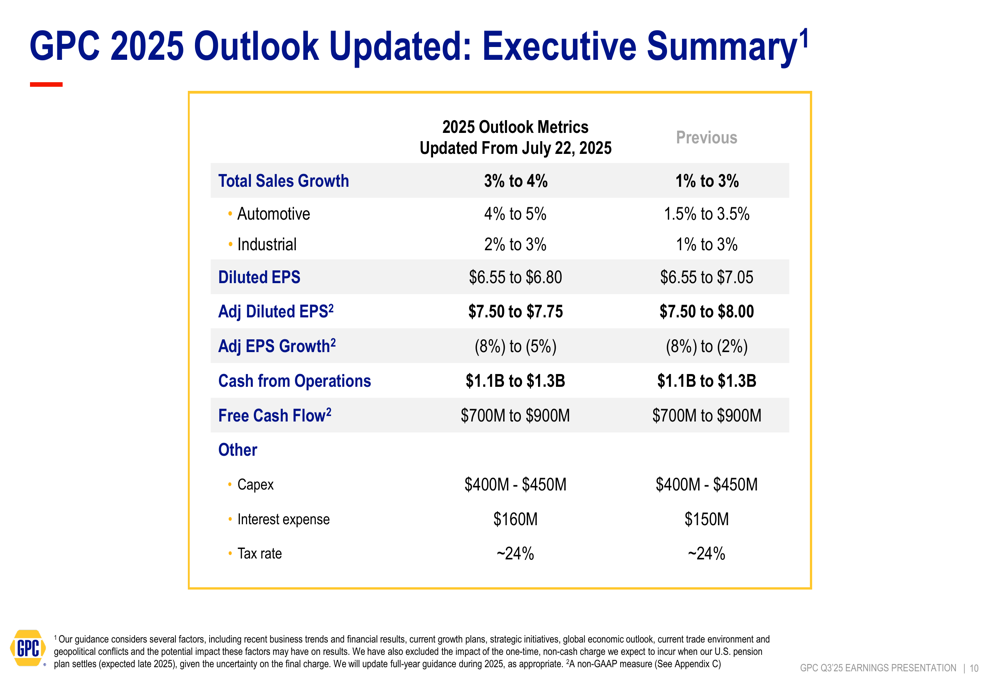

Based on its year-to-date performance, GPC raised its full-year 2025 sales growth guidance from 1-3% to 3-4%. The company now expects Automotive segment sales to grow 4-5% (up from previous guidance of 1.5-3.5%) and Industrial segment sales to increase 2-3% (compared to prior guidance of 1-3%).

GPC narrowed its adjusted diluted EPS guidance to $7.50-$7.75 from the previous range of $7.50-$8.00, representing a year-over-year decline of 5-8%. The company maintains its free cash flow projection of $700 million to $900 million for the full year.

The updated outlook is presented in detail in the following slide:

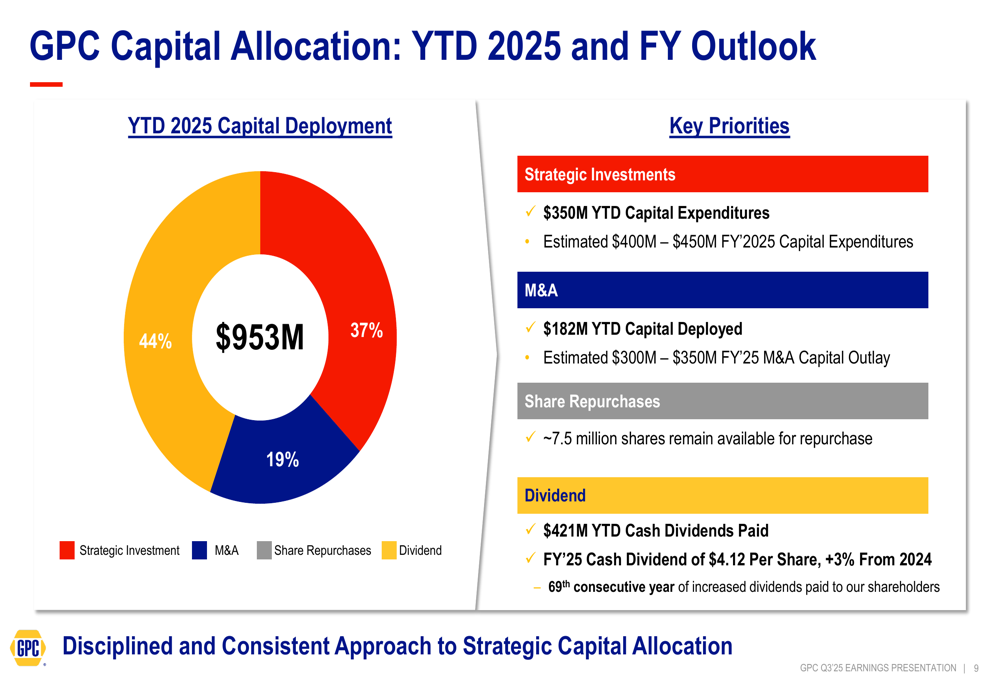

Strategic Initiatives and Capital Allocation

GPC continues to focus on four strategic investment priorities: Talent & Culture, Sales Effectiveness, Supply Chain, and Emerging Technology. These initiatives aim to enhance data and digital capabilities to deliver improved customer experiences, drive profitable growth, and increase operational productivity.

The company’s year-to-date capital allocation reflects these priorities, with 44% directed toward strategic investments, 37% to share repurchases, and 19% to mergers and acquisitions. GPC has deployed $350 million in capital expenditures year-to-date and expects to invest $400-$450 million for the full year 2025.

The following slide illustrates GPC’s capital allocation strategy:

Notably, GPC has maintained its 69-year streak of consecutive dividend increases, with a full-year 2025 cash dividend of $4.12 per share, representing a 3% increase from 2024. The company’s current dividend yield stands at 3.0%.

Forward-Looking Statements

Looking ahead, GPC remains focused on executing its growth initiatives while managing through inflationary pressures. The company highlighted several positive developments, including the signing of a definitive agreement to acquire one of Canada’s largest independent aftermarket players and continued strength with MRO (maintenance, repair, and operations) customers in the Industrial segment.

During the earnings call, CEO Will Stengel emphasized the company’s focus on controllable factors and finishing 2025 strong, while CFO Bert Nappier acknowledged challenges such as tariff impacts and cost inflation but expressed confidence in the company’s momentum.

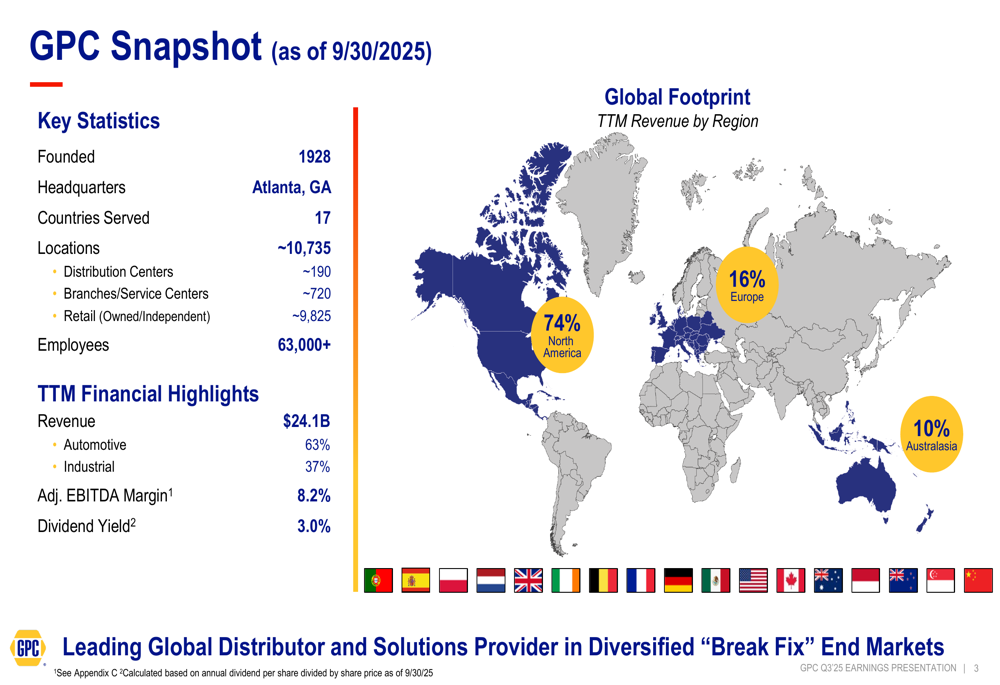

GPC’s global footprint continues to be a strategic advantage, with operations spanning 17 countries through approximately 10,735 locations and over 63,000 employees. The company’s snapshot provides a comprehensive overview of its global presence:

Despite ongoing macroeconomic uncertainties, including soft industrial markets, European challenges, and inflationary pressures in wages and rent, GPC’s diversified business model and strong market position continue to provide resilience. The company’s ability to raise sales guidance while maintaining solid margins demonstrates its operational effectiveness in navigating a complex global business environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.