Gold has topped $4,200. Here’s why Yardeni thinks the rally could go even higher.

Introduction & Market Context

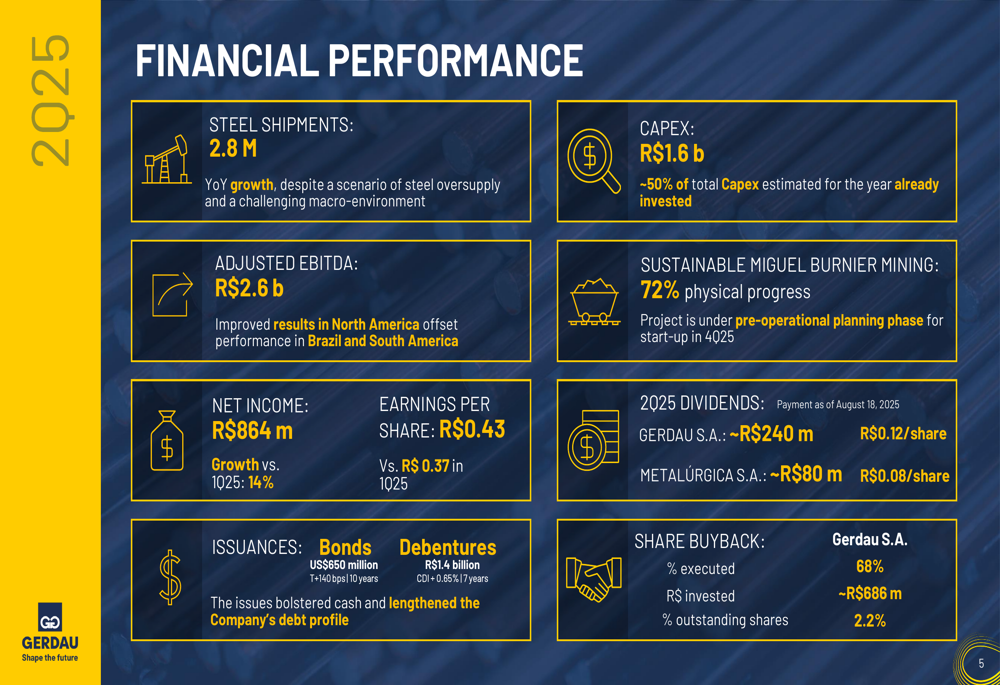

Gerdau SA (BOVESPA:GGBR4) released its second quarter 2025 earnings presentation on August 1, highlighting improved financial performance despite significant challenges from record steel imports. The Brazilian steelmaker reported a 14% quarter-over-quarter increase in net income to R$864 million, with earnings per share rising to R$0.43 from R$0.37 in the previous quarter.

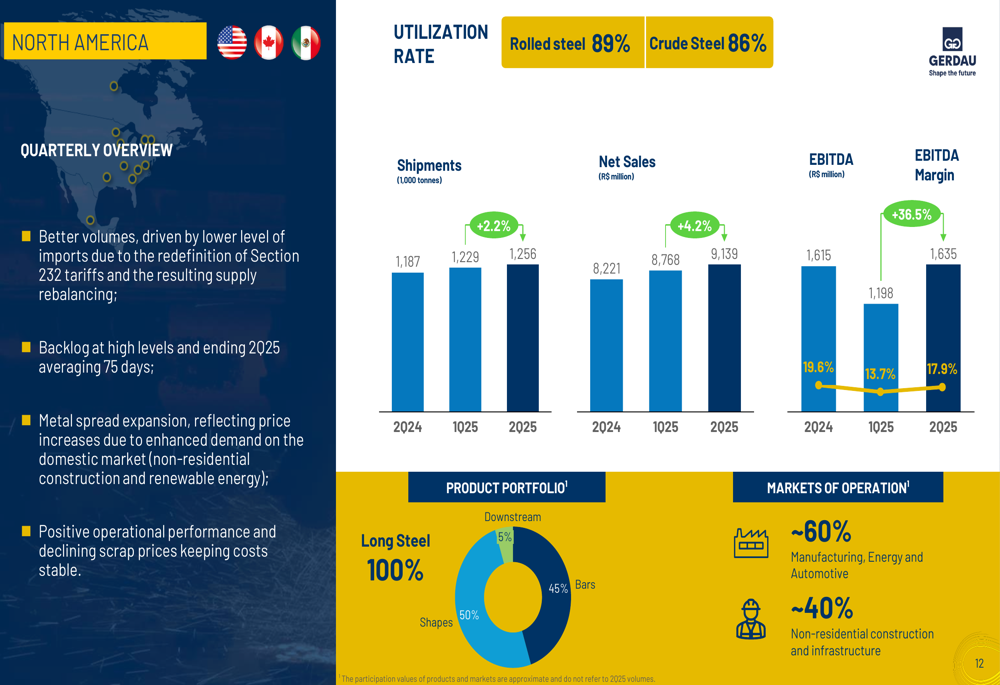

The company’s geographic diversification strategy proved effective during the quarter, with North American operations reaching an all-time high contribution to consolidated EBITDA at 61%, compared to 48% in the first quarter. This strength helped offset ongoing challenges in the Brazilian market, where steel import penetration reached a record 26%, up 3.9 percentage points from 2024.

Quarterly Performance Highlights

Gerdau delivered an adjusted EBITDA of R$2.6 billion in Q2 2025, representing a 6.6% increase from the previous quarter. The company reported steel shipments growth of 2.8 million tonnes year-over-year, while maintaining its focus on operational efficiency and sustainability initiatives.

As shown in the following financial performance overview:

The company continued its capital return program, declaring dividends of approximately R$240 million (R$0.12 per share) for Gerdau S.A., with payment scheduled for August 18, 2025. Additionally, the ongoing share buyback program has reached 68% completion, with approximately R$686 million invested to repurchase 2.2% of outstanding shares.

Gerdau also strengthened its financial position during the quarter by issuing US$650 million in 10-year bonds (T+140 bps) and R$1.4 billion in 17-year debentures (CDI+0.65%), which extended the company’s debt profile while bolstering cash reserves.

Regional Performance Analysis

North America emerged as the standout performer for Gerdau in Q2 2025, with significant margin expansion driving results. The segment benefited from robust volumes, metal spread expansion, and decreased imports following the redefinition of Section 232 tariffs, which helped rebalance supply in the region.

The North American operations demonstrated impressive metrics as illustrated in this overview:

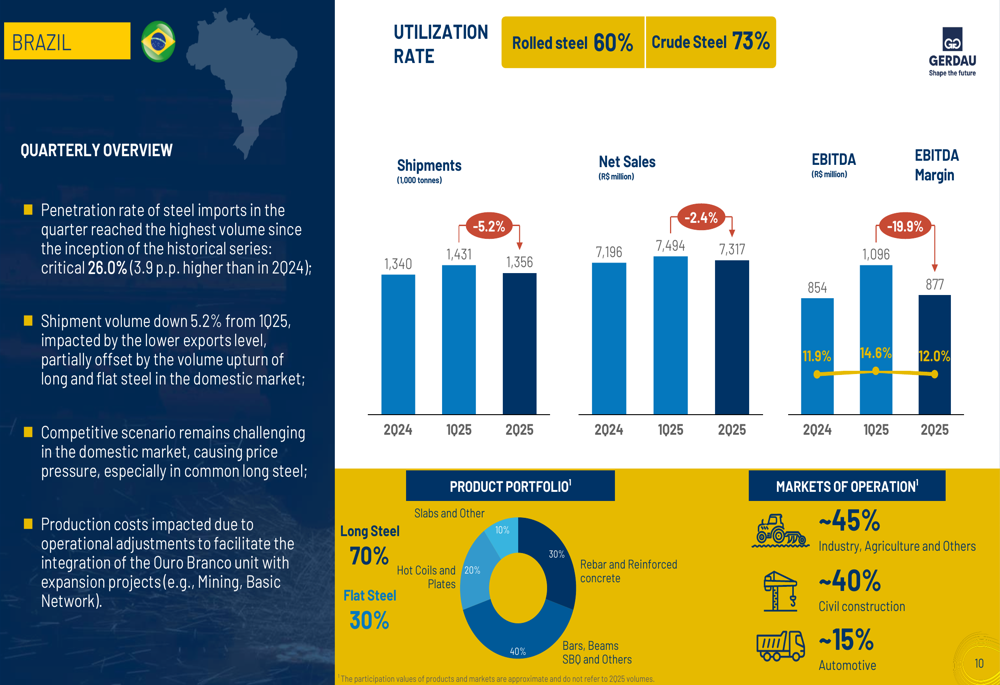

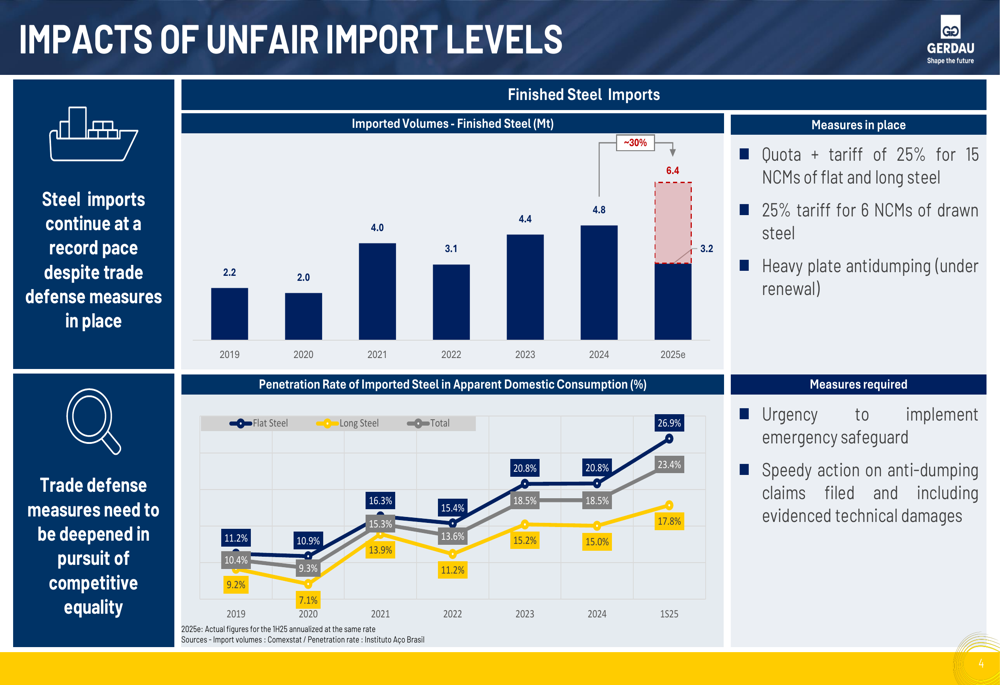

In contrast, Gerdau’s Brazilian operations continued to face significant challenges from steel imports, which reached their highest levels since the inception of historical tracking. The import penetration rate in Brazil hit a critical 26.0%, 3.9 percentage points higher than in 2024, putting pressure on domestic pricing and margins.

The Brazilian segment performance shows the impact of these challenges:

The company highlighted the urgent need for enhanced trade defense measures, including emergency safeguards and expedited action on anti-dumping claims. The presentation emphasized that despite existing measures (quota + 25% tariff for certain steel products), imports continue at a record pace.

As demonstrated in this detailed analysis of import impacts:

South American operations also faced headwinds, with EBITDA margin declining to 11.2% in Q2 2025 from 13.8% in Q1 2025 and 16.2% in Q2 2024. While volumes showed a slight upturn, demand remains weak in the main sectors served by this segment.

Strategic Initiatives & CAPEX Projects

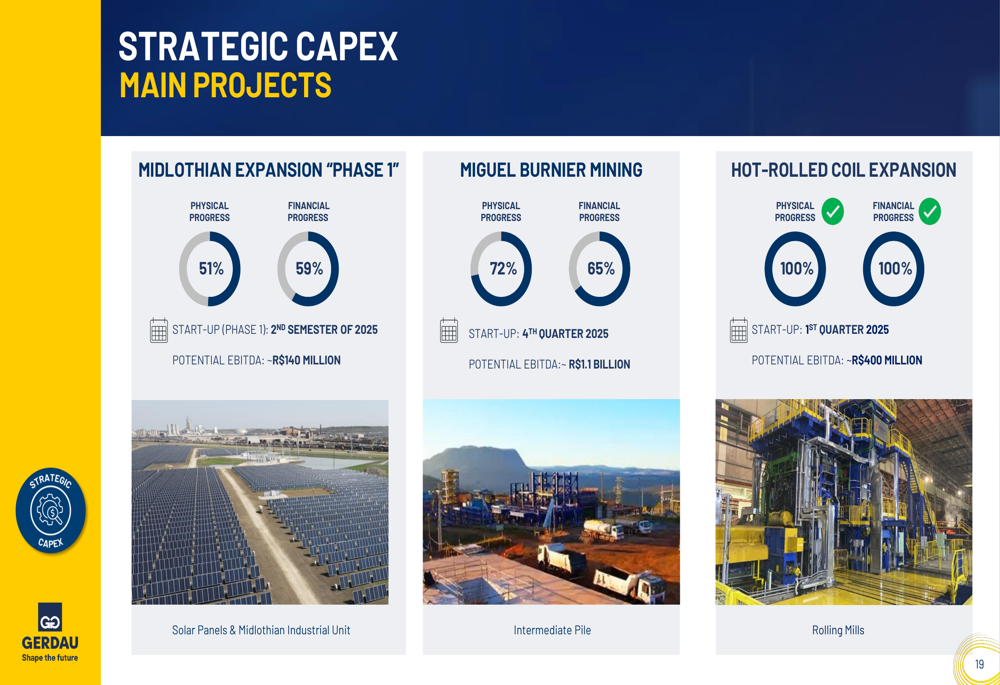

Gerdau continues to advance its key strategic projects, with significant progress reported across its major initiatives. The Miguel Burnier Mining project has reached 72% physical completion and is on track for start-up in the fourth quarter of 2025. This sustainable mining operation is currently in the pre-operational planning phase.

The company’s Midlothian expansion in North America has achieved 51% physical progress and 59% financial progress, with Phase 1 scheduled to start operations in the second half of 2025. Meanwhile, the Hot-Rolled Coil Expansion project has been completed and began operations in the first quarter of 2025.

These strategic investments are visualized in the following progress report:

Gerdau also highlighted its continued commitment to sustainability, reporting carbon emissions of 0.85 tCO2e per tonne of steel, the lowest level in the company’s historical series. Additionally, workplace safety remains a priority, with the accident frequency rate at 0.71 in Q2 2025, continuing the company’s long-term improvement trend in this area.

Financial Position & Shareholder Returns

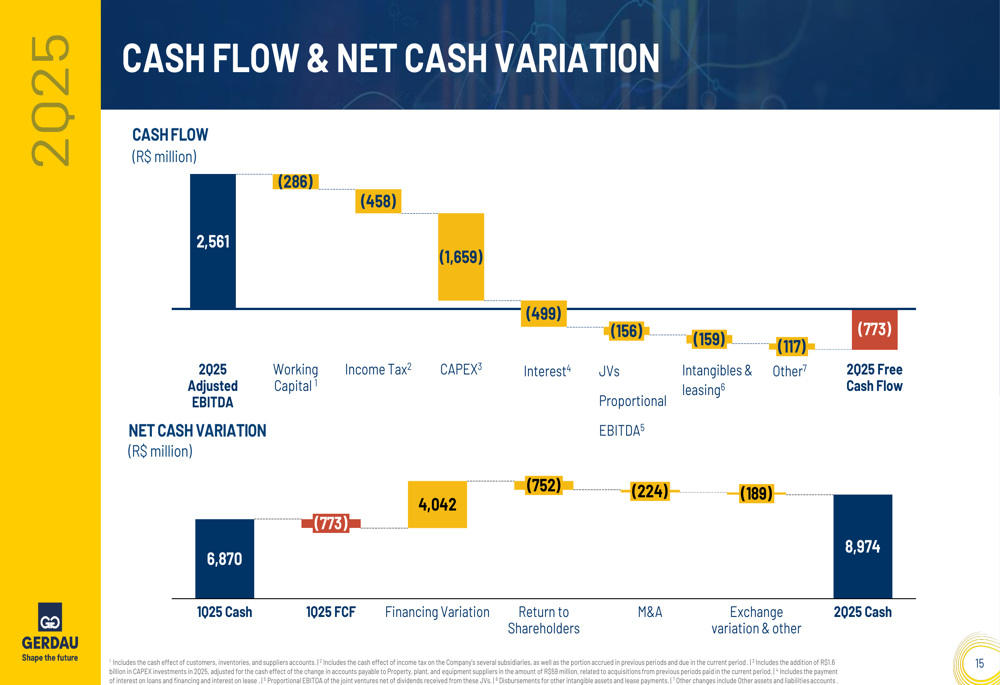

The company maintained a strong financial position with a disciplined approach to capital allocation. Gerdau’s cash flow and debt management strategy is reflected in its liquidity position, with an average debt term of 7.2 years and competitive financing costs (average cost in BRL:CDI + 0.49% Y/Y and USD: 5.6% Y/Y).

The company’s financial policy targets include maintaining gross debt below R$12 billion, keeping the Net Debt/EBITDA ratio at or below 1.5x, and maintaining an average debt term greater than 6 years. Gerdau’s credit ratings remain stable, with investment-grade ratings from all major agencies (Fitch:BBB stable, S&P: BBB stable, Moody’s: Baa2 stable).

The cash flow for Q2 2025 shows the company’s financial movements:

Outlook & Forward-Looking Statements

Looking ahead to the second half of 2025, Gerdau provided a differentiated outlook for its key markets. In North America, the company expects continued margin expansion driven by robust volumes, metal spread expansion, and decreased imports, though it noted the need to monitor customer uncertainty.

For Brazil, Gerdau anticipates a margins upturn despite the risk of new record import levels. The company cited resilient demand from civil construction and opportunities to recover margins through operating cost reductions. Management is also monitoring potential effects that U.S. tariffs on Brazil could have on the domestic market.

As outlined in the regional outlook:

The company announced it will host an Investor Day on October 1, 2025, in São Paulo, where it is expected to provide more details on its long-term strategy and capital allocation plans.

According to the earnings call transcript, Gerdau plans to reduce global CapEx starting in 2026, with a focus on North American investments. The company expects EBITDA growth from mining and HRC projects in 2026-2027 and is considering share buybacks as a primary capital allocation strategy going forward.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.