TSX gains after CPI shows US inflation rose 3%

Introduction & Market Context

Cyfrowy Polsat SA (WSE:CPS), operating as Grupa Polsat Plus, presented its Q1 2025 financial results on May 22, 2025, showcasing continued revenue and EBITDA growth despite a significant decline in net profit. The company maintained its strategic focus on three key business pillars: telecommunications, media, and green energy, with particularly strong performance in its renewable energy segment.

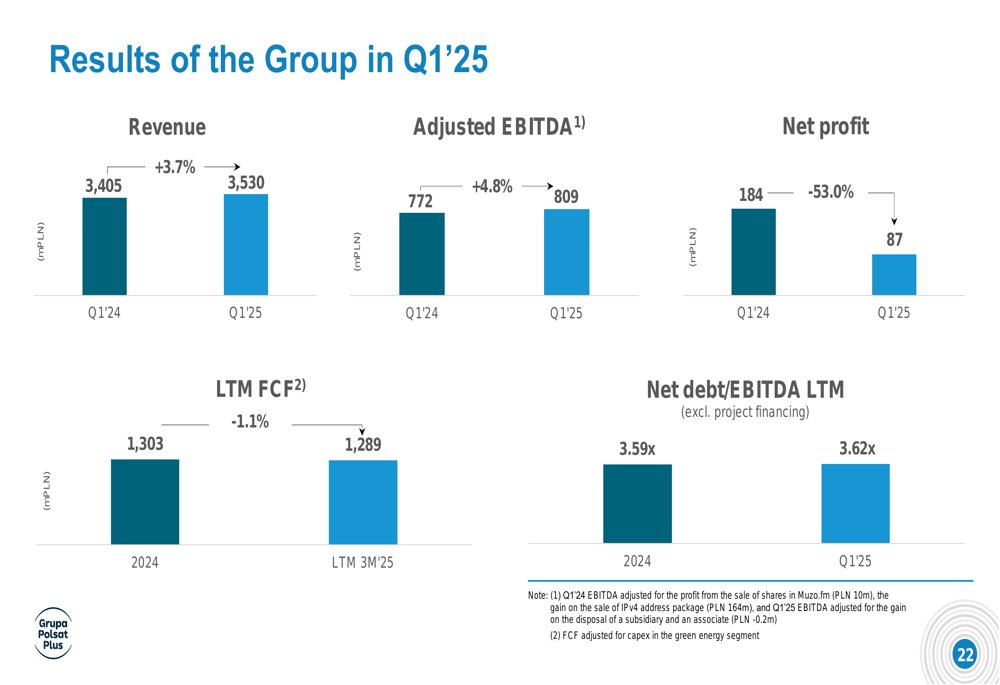

The Polish telecommunications and media conglomerate reported a 3.7% year-over-year increase in revenue to PLN 3,530 million and a 4.8% growth in adjusted EBITDA to PLN 809 million. These results continue the positive trend seen in the company’s 2024 performance, when it achieved a 4.7% revenue increase for the full year.

Quarterly Performance Highlights

Grupa Polsat Plus achieved several notable milestones across its business segments in Q1 2025. The company’s multiplay strategy continued to yield positive results, with over 2.5 million customers now using bundled services, representing 44% of the total customer base. This strategy has contributed to a low churn rate of 6.8% and increasing average revenue per user (ARPU).

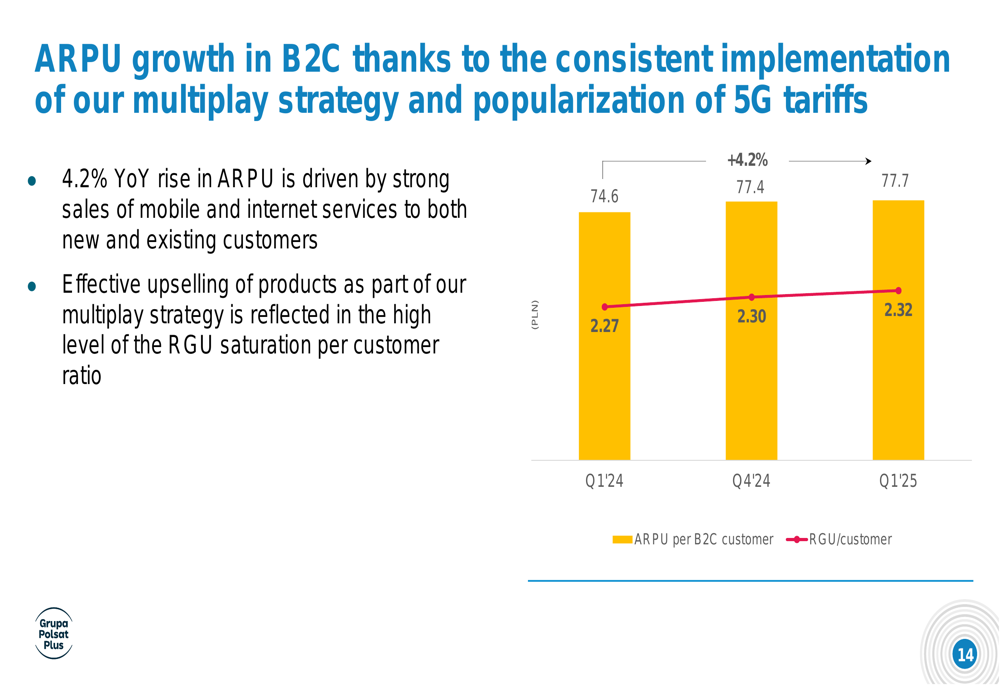

As shown in the following chart, ARPU in the B2C segment increased by 4.2% year-over-year to PLN 77.7, while the number of services per customer (RGU/customer) rose to 2.32:

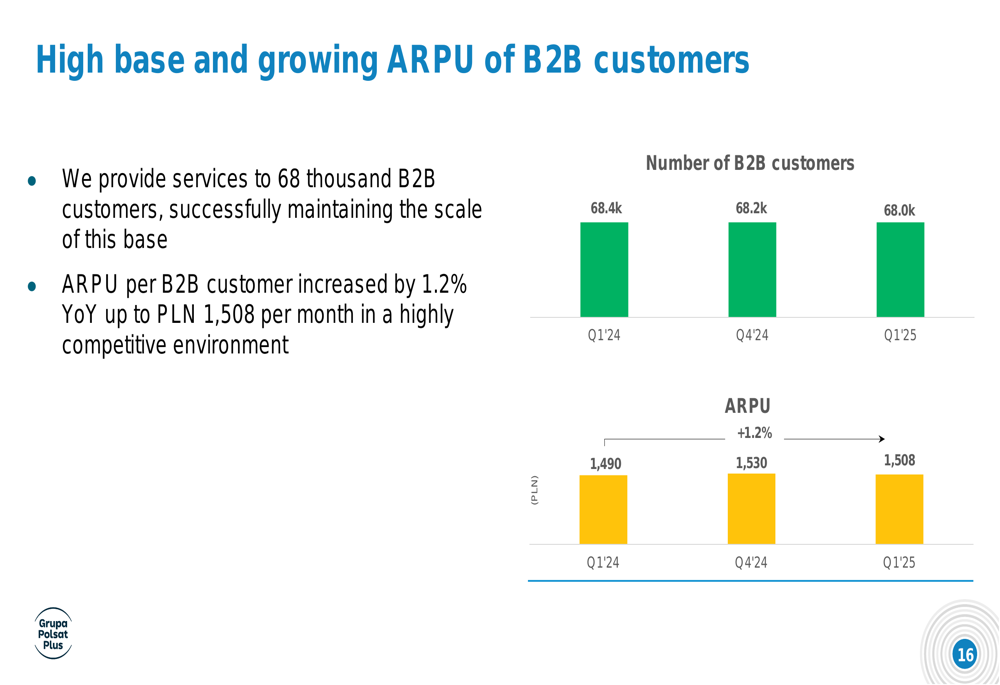

In the B2B segment, the company maintained a stable customer base of 68,000 clients while increasing ARPU by 1.2% year-over-year to PLN 1,508 per month:

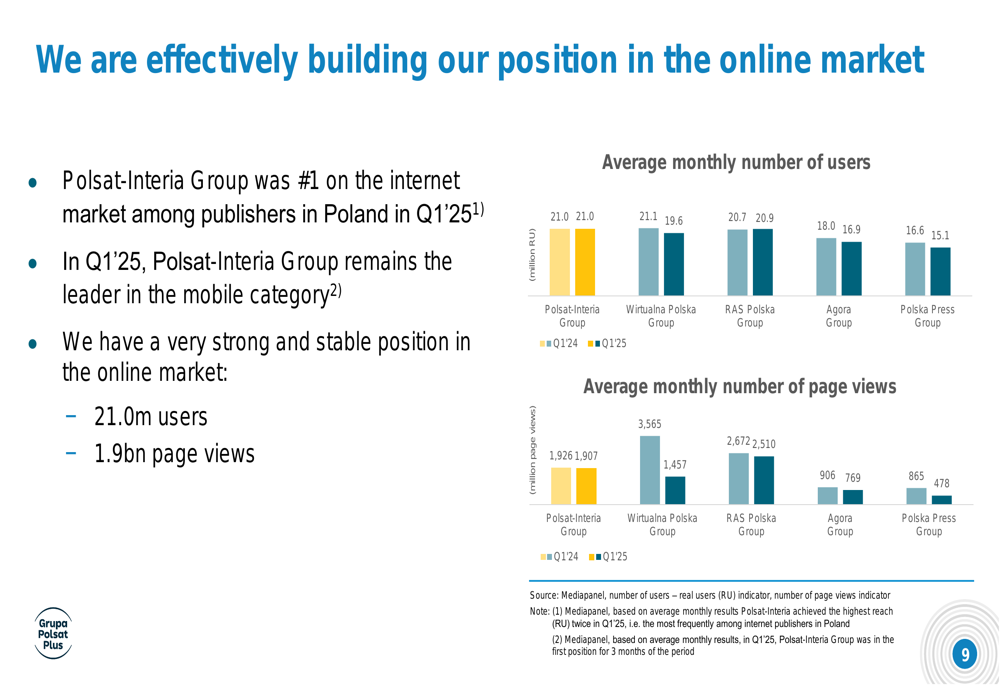

The media segment maintained its strong market position with TV channels achieving a 22.1% audience share. Additionally, the Polsat-Interia Group remained the leader among internet publishers in Poland with 21.0 million users and 1.9 billion page views in Q1 2025:

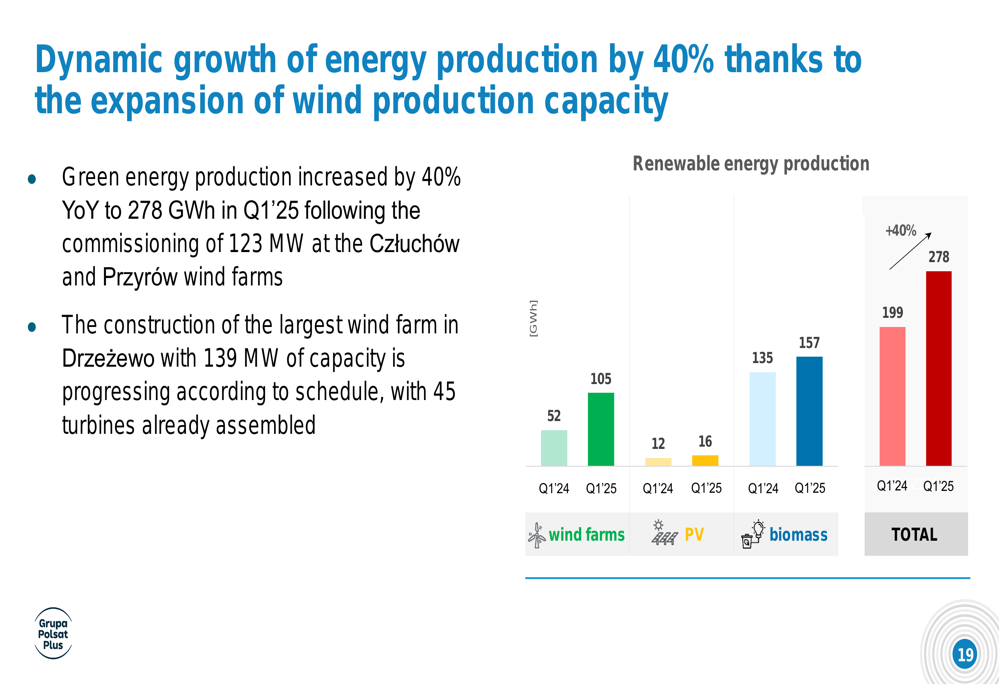

One of the most impressive areas of growth was in the green energy segment, where production increased by 40% year-over-year to 278 GWh, driven by the expansion of wind production capacity:

Detailed Financial Analysis

The company’s financial results for Q1 2025 showed mixed performance across key metrics. While revenue and adjusted EBITDA demonstrated healthy growth, net profit declined significantly by 53.0% to PLN 87 million compared to the same period last year.

The following chart illustrates the Group’s key financial results:

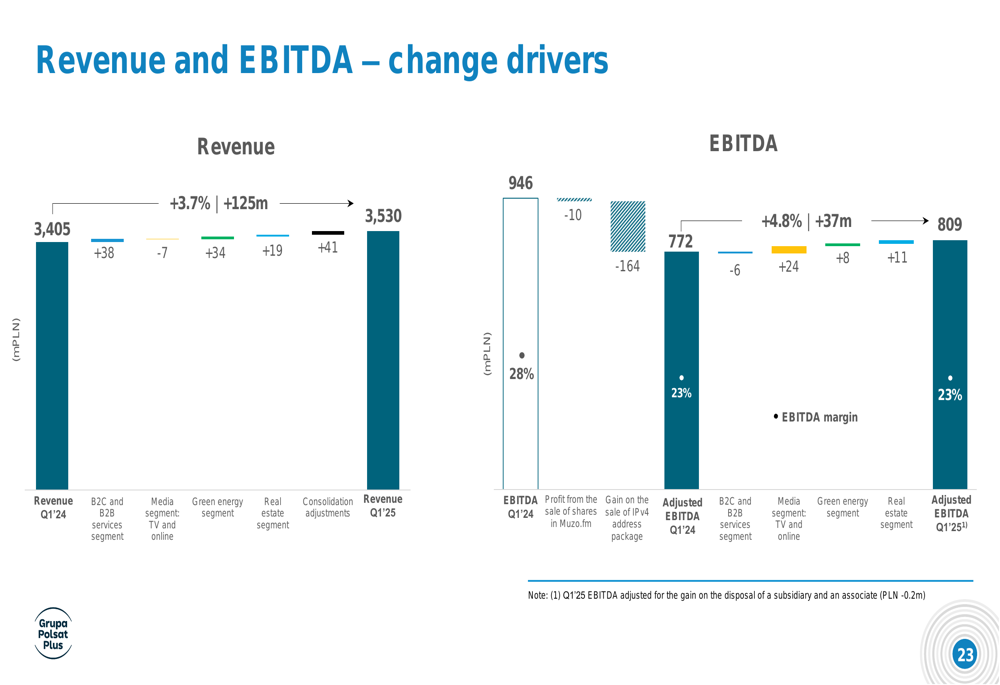

The growth in revenue and EBITDA was primarily driven by the B2C segment and green energy expansion, as shown in this breakdown of contributing factors:

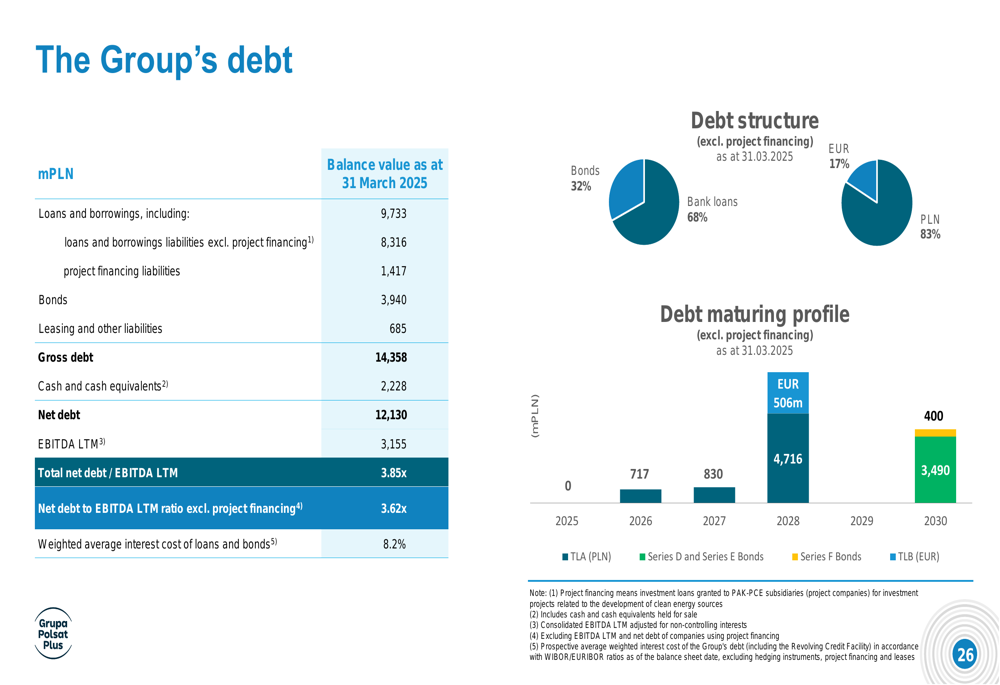

Despite solid operational performance, the company’s debt levels remain relatively high, with the net debt to EBITDA ratio at 3.62x (excluding project financing). This represents a slight increase from the 3.59x reported at the end of 2024. The debt structure and maturity profile are illustrated below:

The company’s capital expenditure remained under control in the telecommunications, media, and technology (TMT) segment at 10% of revenue, while development capex in the green energy segment reached PLN 157 million in Q1 2025, reflecting continued investment in renewable energy projects.

Strategic Initiatives

Grupa Polsat Plus continued to implement its Strategy 2023+ during the quarter, focusing on three main business areas. In telecommunications, the company acquired a block in the 700 MHz band for PLN 363 million, strengthening its network capabilities. The company’s 5G network coverage, which reached 70% of Poland’s population by the end of 2024, continues to expand.

In the media segment, the company maintained its leading position in both traditional TV and online platforms. The successful programming schedule and broadcasting of attractive sports events contributed to the increase in audience share to 22.1%.

The green energy segment saw significant progress, with the company reporting that it has achieved its strategic goals of becoming a leading producer of clean energy and building a complete green hydrogen value chain. The construction of the Drzeżewo wind farm, which will be the company’s largest with 139 MW capacity, is progressing according to schedule with 45 turbines already assembled.

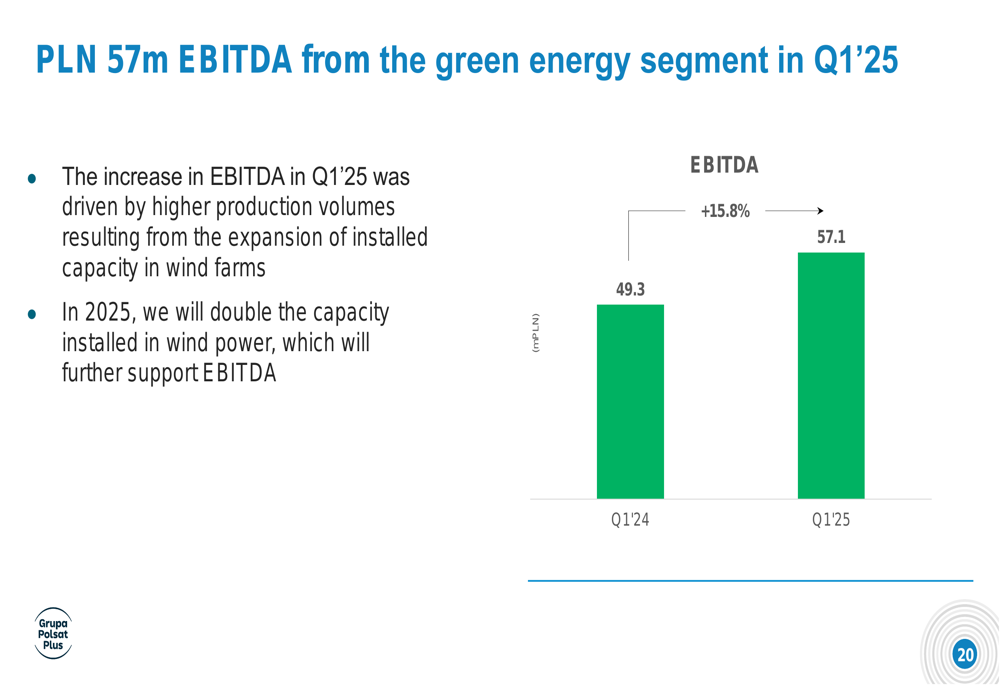

The green energy segment’s EBITDA increased by 15.8% year-over-year to PLN 57.1 million, as shown in the following chart:

The company also made progress in its green hydrogen initiatives, winning tenders for the delivery of 41 Nesobuses (hydrogen-powered buses) to Kraków, Rybnik, and Rzeszów.

Forward-Looking Statements

Looking ahead, Grupa Polsat Plus remains committed to its multiplay strategy in the telecommunications segment, focusing on increasing ARPU and maintaining low churn rates. The company expects to double its installed capacity in wind power in 2025, which should further support EBITDA growth in the green energy segment.

The company is targeting approximately PLN 500 million in EBITDA from the green energy segment by 2026, as it transitions from the investment phase to the monetization phase. This aligns with CFO Katarzyna Ostap-Tomann’s statement from the previous quarter that the company is "approaching the end of investments in the development of the energy segment and moving to the monetization phase."

While the company faces challenges such as a high debt level and significant interest costs, its diversified business model and strategic investments in growth areas position it to continue delivering solid operational results. The consistent implementation of its multiplay strategy and the monetization of investments in green energy remain key priorities for sustainable long-term growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.