Gold has topped $4,200. Here’s why Yardeni thinks the rally could go even higher.

Introduction & Market Context

Keyera Corp . (TSX:KEY) presented its August 2025 investor presentation on August 7, highlighting strategic growth initiatives centered around its Plains acquisition and projected financial performance. The stock closed at $43.55, up 1.66% from the previous day, as investors digested the company’s expansion plans and recent earnings beat.

The midstream energy infrastructure company, which recently reported Q1 2025 earnings that exceeded analyst expectations with EPS of $0.57 versus a forecast of $0.5398, emphasized its position to capitalize on growth in the Western Canadian Sedimentary Basin and expanded market access through strategic acquisitions.

Strategic Expansion through Plains Acquisition

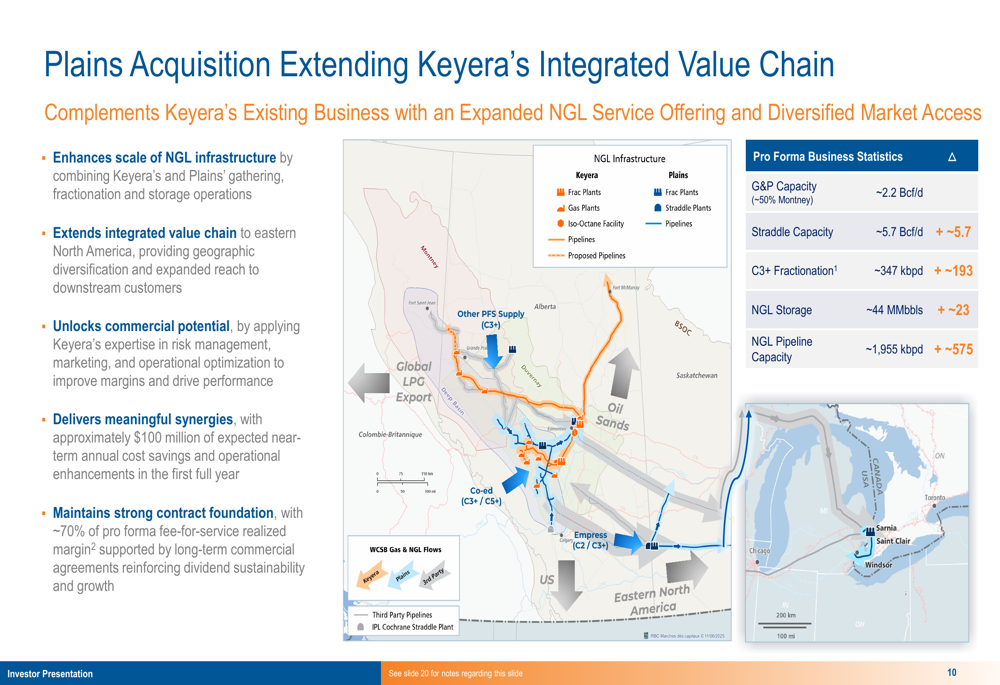

A central focus of Keyera’s presentation is how the Plains acquisition extends its integrated value chain and creates a cross-Canada NGL corridor. The transaction significantly enhances Keyera’s scale in NGL infrastructure while extending its reach to eastern North America.

As shown in the following infrastructure map:

The acquisition complements Keyera’s existing business with expanded NGL service offerings and diversified market access. Pro forma business statistics reveal impressive scale: 2.2 Bcf/d G&P capacity, 5.7 Bcf/d straddle capacity, 347 kbpd C3+ fractionation, 44 MMbbls NGL storage, and 1,955 kbpd NGL pipeline capacity.

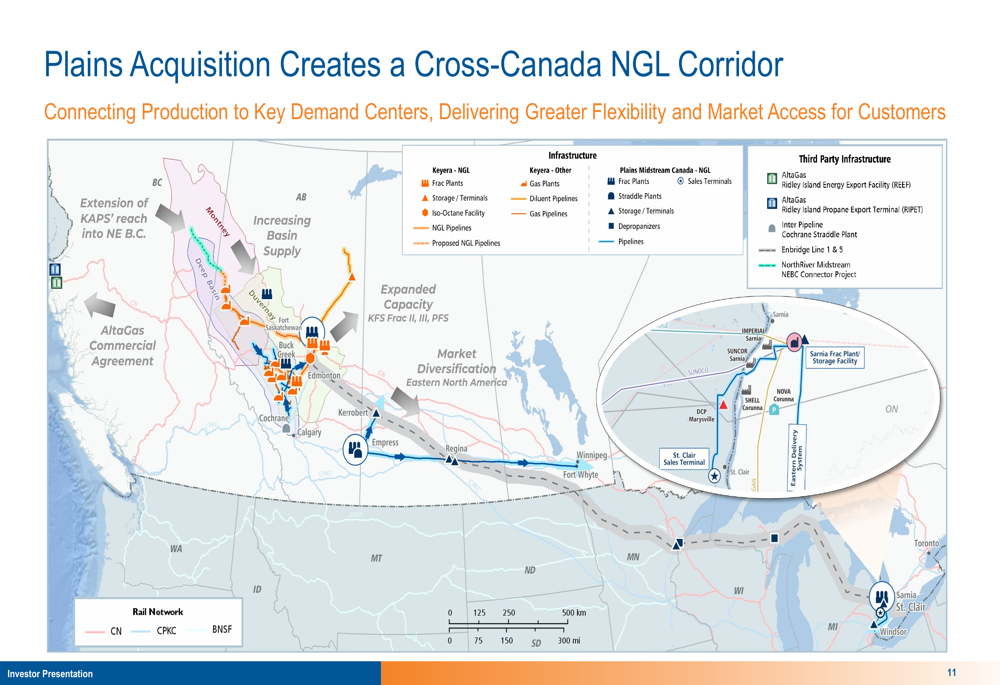

The transaction creates a comprehensive cross-Canada NGL corridor that connects production to key demand centers:

This expanded network is expected to deliver greater flexibility and market access for customers, strengthening Keyera’s competitive position in the North American midstream space.

Financial Performance and Growth Projections

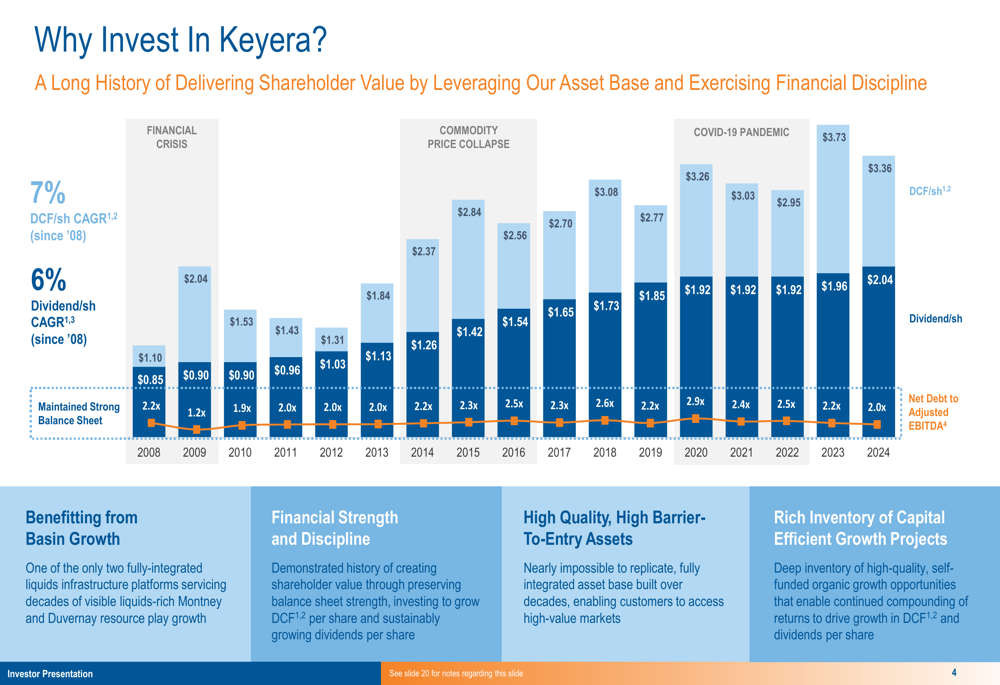

Keyera has demonstrated consistent financial performance, with a 7% DCF/share CAGR and 6% dividend/share CAGR since 2008, while maintaining a disciplined approach to leverage.

The company’s historical performance is illustrated in this chart:

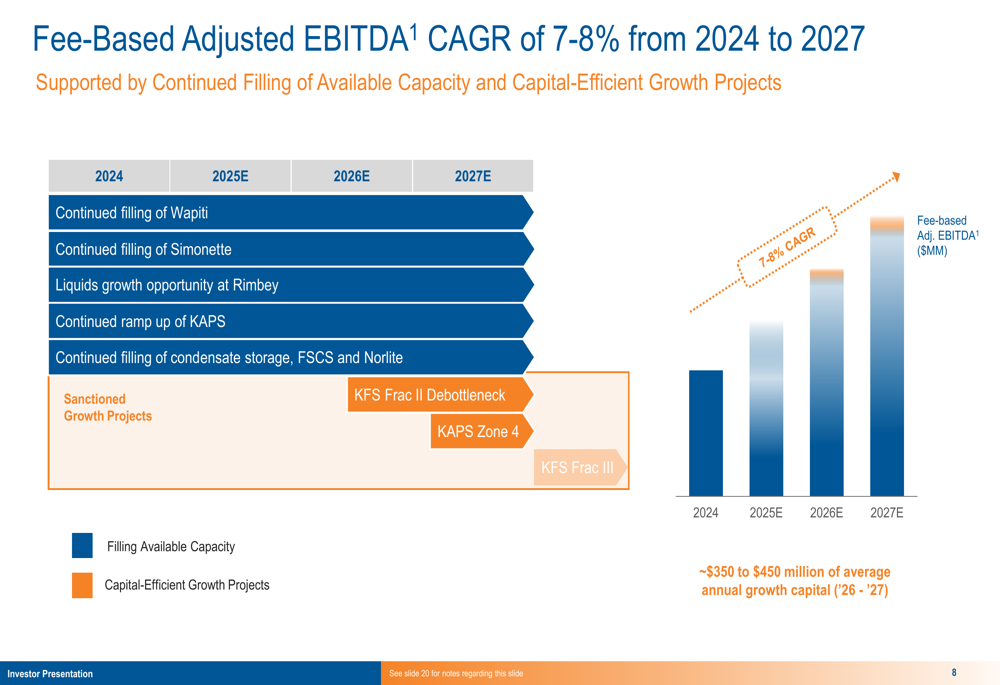

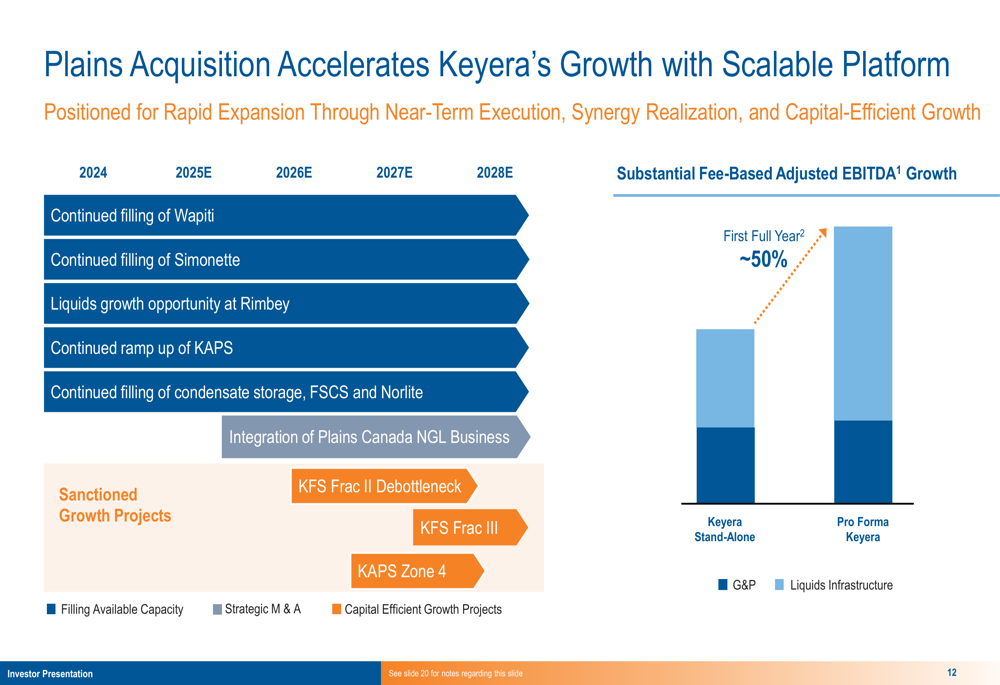

Looking ahead, Keyera projects a fee-based adjusted EBITDA CAGR of 7-8% from 2024 to 2027, supported by continued filling of available capacity and capital-efficient growth projects:

The Plains acquisition is expected to accelerate this growth trajectory, with 50% of the first full year’s fee-based adjusted EBITDA coming from the merger:

These projections align with the company’s recent financial performance. In Q1 2025, Keyera reported revenue of $1.73 billion, exceeding the expected $1.58 billion, and net earnings increased to $130 million from $71 million in the same quarter last year.

Capital Allocation and Financial Discipline

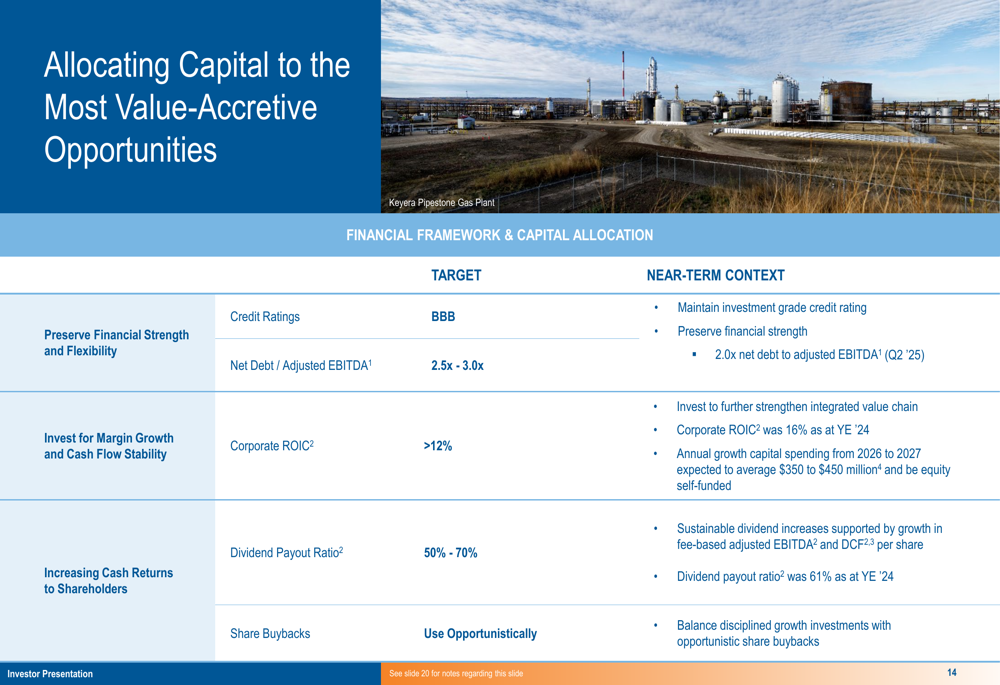

Keyera emphasized its disciplined approach to capital allocation, targeting the most value-accretive opportunities while maintaining financial strength:

The company maintains a solid financial position with a 2.0x net debt to adjusted EBITDA ratio as of Q2 2025, investment grade credit ratings, and total liquidity of $1.5 billion. This strong balance sheet enables Keyera to pursue and equity self-fund growth opportunities.

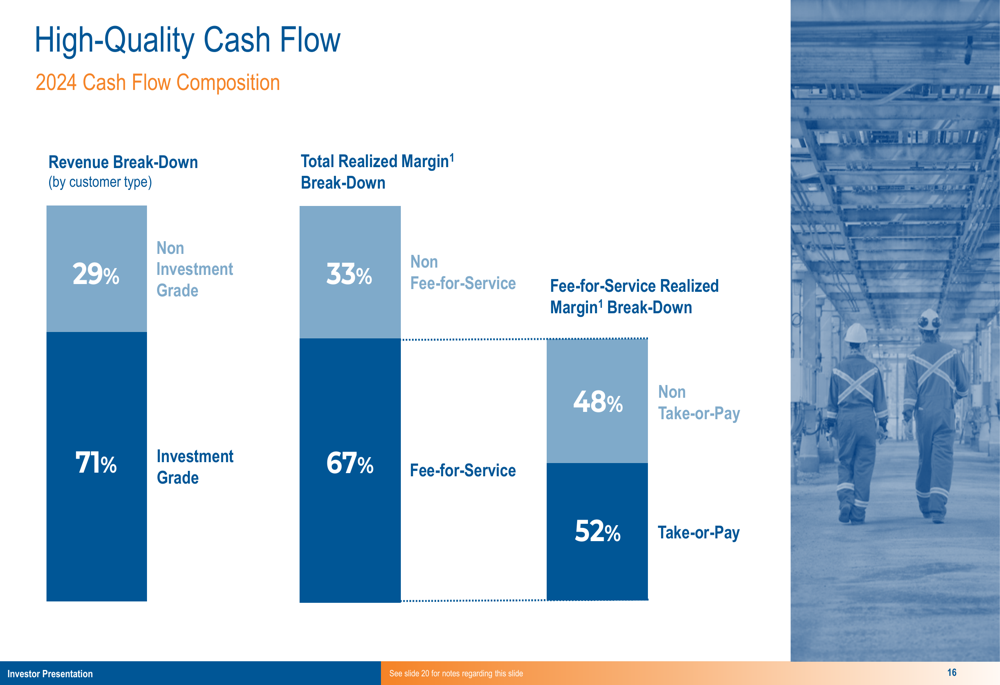

Keyera’s high-quality cash flow composition provides further stability:

With 67% of total realized margin coming from fee-for-service activities and 71% of revenue derived from investment-grade customers, Keyera maintains a stable foundation for its growth initiatives.

2025 Guidance and Future Outlook

For 2025, Keyera provided the following financial guidance:

These projections align with the guidance reaffirmed in the company’s recent Q1 2025 earnings report, which projected marketing segment realized margins between $310 million and $350 million, growth capital expenditures of $300 million to $330 million, and maintenance capital expenditures of $70 million to $90 million.

Beyond 2027, Keyera identified several growth opportunities, including liquids extraction, AEF debottlenecking, expanding gathering and processing capacity in the North Region, enhancing rail and logistics capabilities, and developing a conventional energy and low-carbon hub at Josephburg.

Sustainability Initiatives

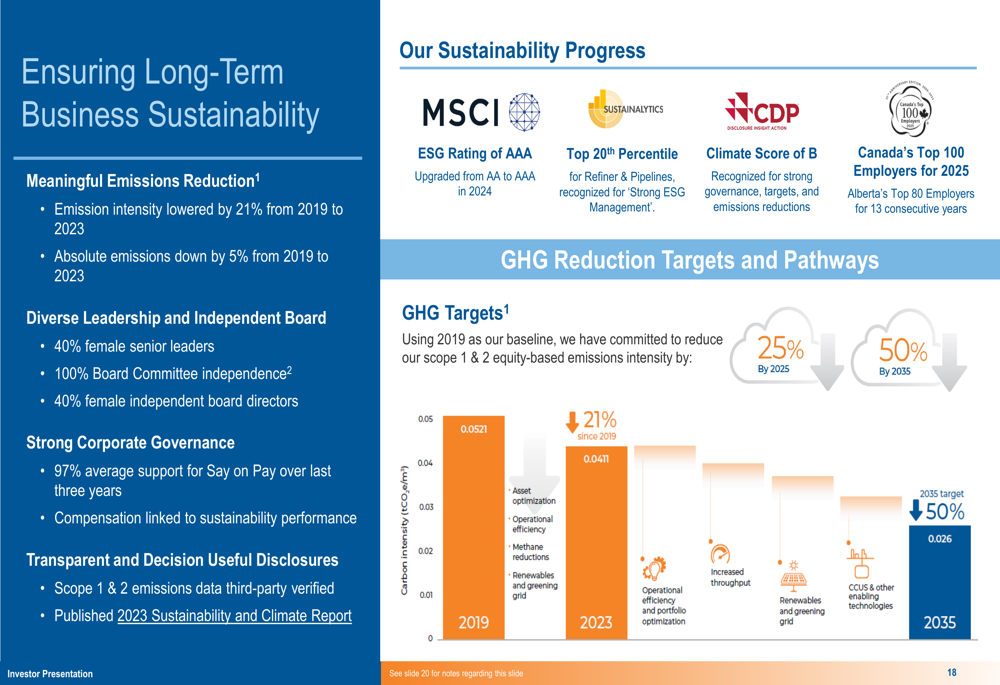

Keyera highlighted its commitment to long-term business sustainability through environmental and social initiatives:

The company has reduced emission intensity by 21% from 2019 to 2023, with absolute emissions decreasing by 5%. Keyera has set ambitious GHG targets to decrease emissions by 25% by 2025 and 50% by 2035, demonstrating its commitment to responsible operations.

Forward-Looking Statements

While Keyera’s presentation paints an optimistic picture of growth and expansion, investors should note some challenges mentioned in the recent earnings call, including extended maintenance outages at facilities like AEF, commodity price volatility, and potential regulatory changes regarding emissions policies.

Despite beating earnings expectations in Q1 2025, Keyera’s stock experienced a 1.04% decline in pre-market trading following the earnings release, suggesting some investor concerns about operational challenges that weren’t prominently addressed in the August presentation.

Nevertheless, with its strategic Plains acquisition creating a cross-Canada NGL corridor, projected 7-8% fee-based adjusted EBITDA growth through 2027, and strong financial discipline, Keyera appears well-positioned to execute its growth strategy while maintaining its 23-year track record of dividend payments, currently offering a 4.94% yield.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.