Trump administration authorizes CIA for covert action in Venezuela - Bloomberg

Introduction & Market Context

LuxExperience B.V. (NYSE:LUXE), formerly known as MYT Netherlands Parent (NYSE:MYTE) B.V., presented its Q3 FY25 results on May 14, 2025, highlighting the company’s recent acquisition of YOOX NET-A-PORTER and subsequent rebranding. The presentation revealed a company navigating challenging luxury market conditions while maintaining growth and profitability across key metrics.

The newly formed LuxExperience now positions itself as "the leading global multi-brand digital luxury group" with combined revenue of approximately €3 billion following the YOOX NET-A-PORTER acquisition. The company continues to trade on the New York Stock Exchange but now under the new ticker symbol "LUXE."

Quarterly Performance Highlights

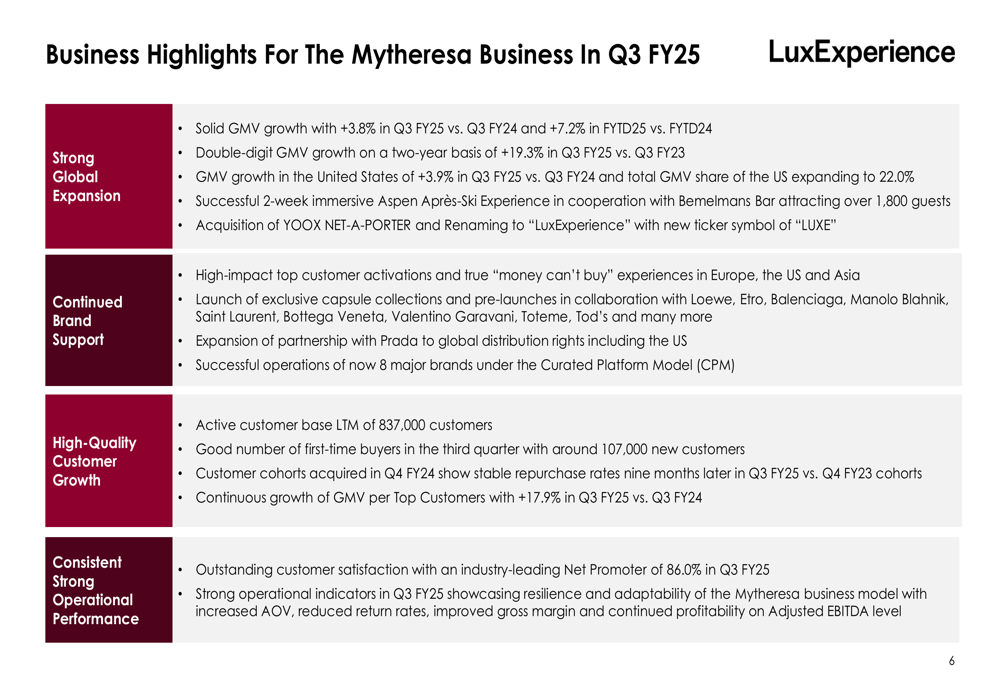

LuxExperience reported solid Gross Merchandise Value (GMV) growth of 3.8% year-over-year for Q3 FY25, with fiscal year-to-date growth of 7.2%. More notably, the company achieved double-digit GMV growth of 19.3% on a two-year basis compared to Q3 FY23, demonstrating longer-term momentum despite recent market headwinds.

The United States continues to be a growth driver, with US GMV increasing by 3.9% in Q3 FY25 compared to the same period last year. The US market now represents 22.0% of the company’s total GMV, up from previous quarters.

As shown in the following business highlights chart:

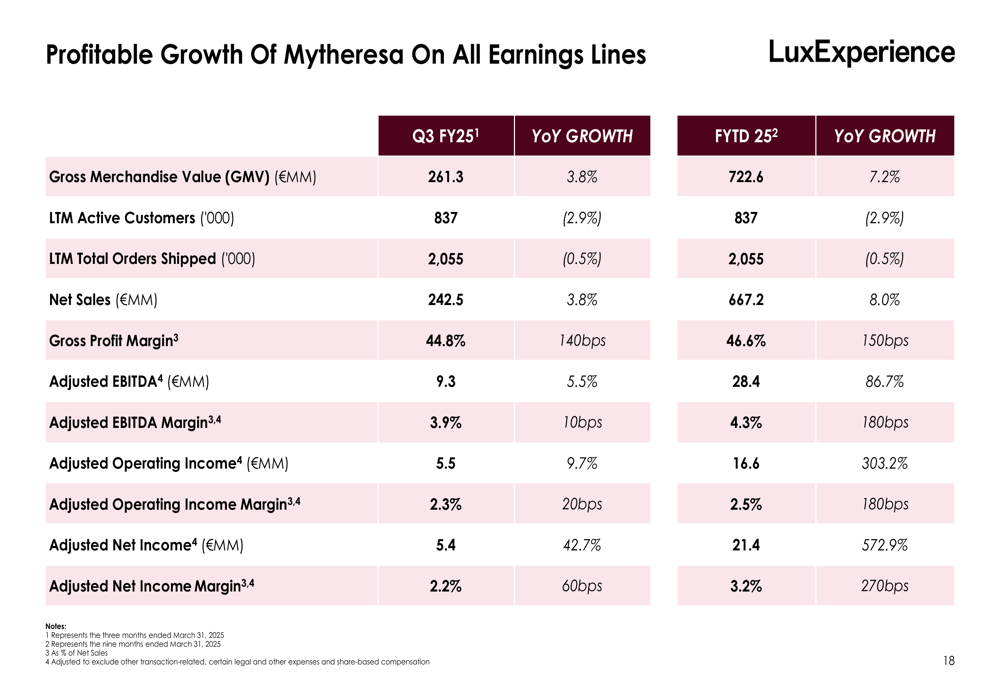

Financial performance remained strong with net sales of €242.5 million in Q3 FY25, representing 3.8% year-over-year growth. The company maintained profitability with an Adjusted EBITDA of €9.3 million, up 5.5% from Q3 FY24, and Adjusted Net Income of €5.4 million, showing impressive growth of 42.7% year-over-year.

The company’s active customer base stood at 837,000 for the last twelve months, representing a slight decrease of 2.9% compared to the previous year. However, customer satisfaction remains exceptionally high with an industry-leading Net Promoter Score of 86.0% in Q3 FY25, an improvement of 5.4 percentage points year-over-year.

Strategic Initiatives

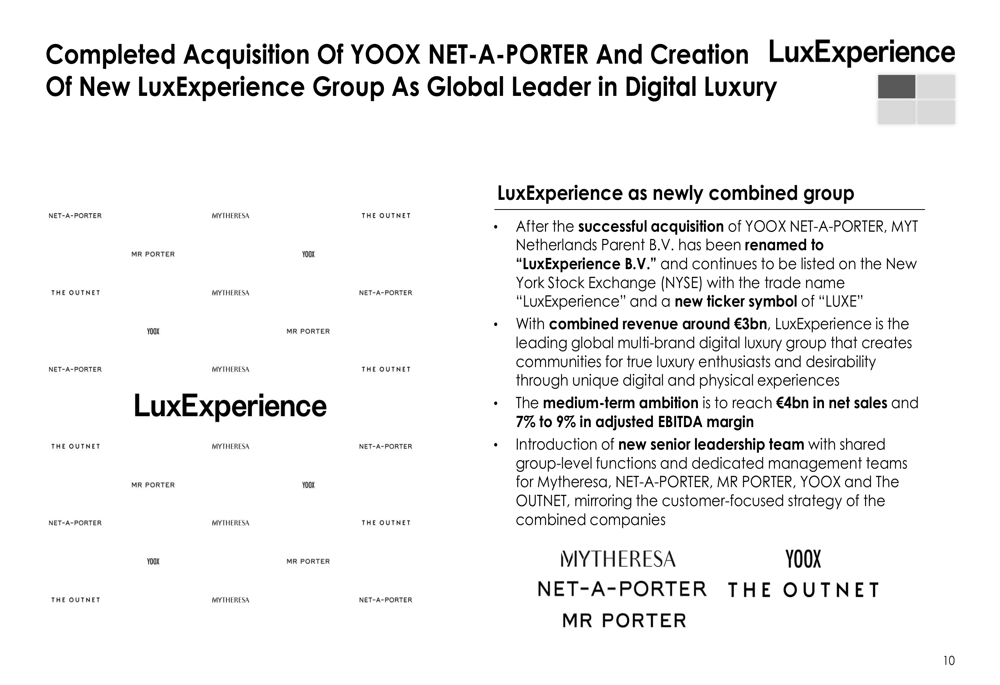

The most significant strategic development was the completed acquisition of YOOX NET-A-PORTER, creating the new LuxExperience Group. This acquisition brings together multiple luxury e-commerce platforms including Mytheresa, NET-A-PORTER, MR PORTER, YOOX, and THE OUTNET.

The company has introduced a new senior leadership team with shared group-level functions while maintaining dedicated management teams for each platform, reflecting the customer-focused strategy of the combined companies.

As illustrated in the acquisition announcement:

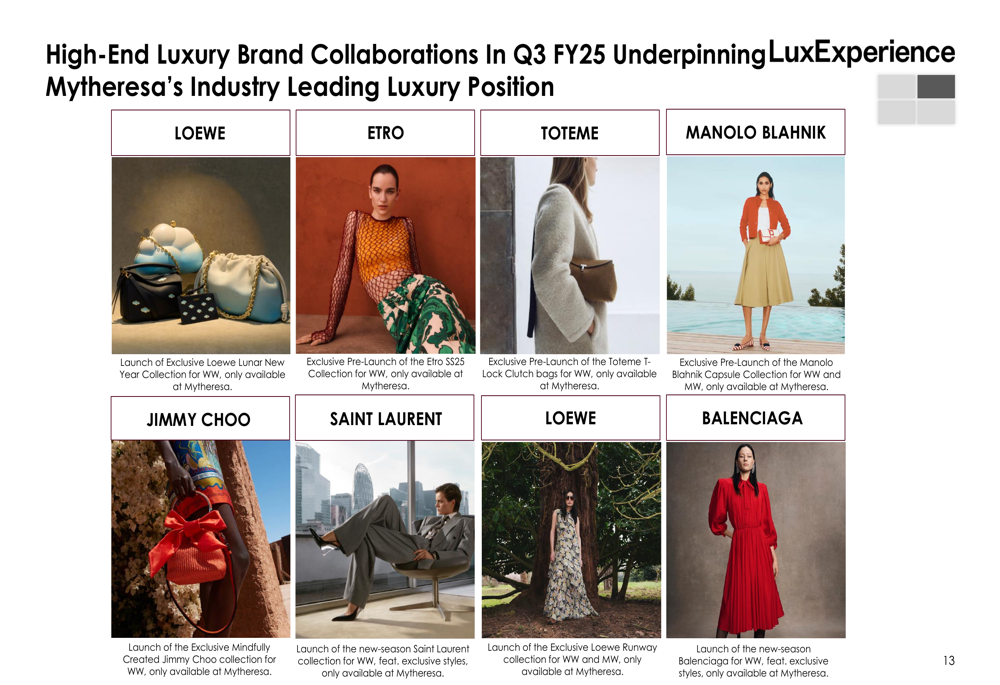

LuxExperience continues to strengthen its brand partnerships, announcing the expansion of its relationship with Prada (OTC:PRDSY) to include global distribution rights, including the US market. Previously, Prada products were only available to European customers through the platform.

The company also highlighted its ongoing collaborations with other luxury brands including LOEWE, ETRO, TOTEME, MANOLO BLAHNIK, JIMMY CHOO, SAINT LAURENT, and BALENCIAGA, reinforcing its position in the high-end luxury segment.

These brand partnerships are showcased in the following image:

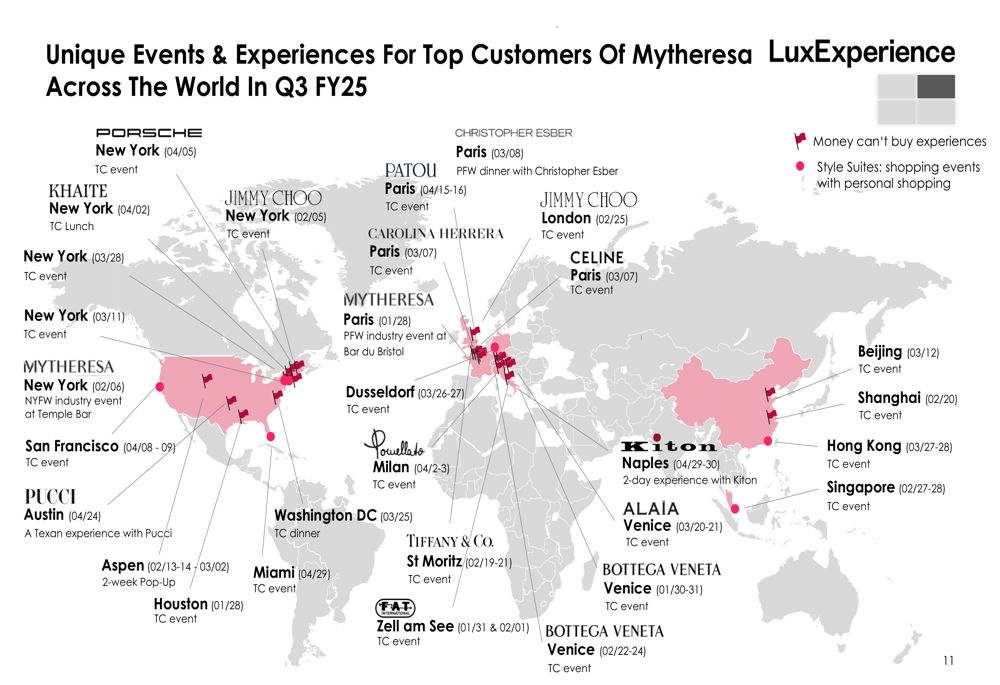

A key element of LuxExperience’s strategy is creating exclusive experiences for high-value customers. The company highlighted its two-week immersive Après-Ski Experience in Aspen, which successfully attracted new high-net-worth customers. The event generated 827,000 EUR in revenue and captured 2,368 contact details, with 56% being new contacts and achieving a 48% repurchase rate.

The Aspen experience exemplifies the company’s approach to customer acquisition and retention:

This focus on exclusive experiences extends globally, with LuxExperience hosting VIP customer events across multiple continents during Q3 FY25:

Detailed Financial Analysis

LuxExperience’s financial performance shows resilience in a challenging macro environment, with improvements across several key metrics. Gross profit margin increased by 140 basis points year-over-year to 44.8% in Q3 FY25, while the company also improved its shipping and payment cost margin by 130 basis points.

The company’s profitability metrics show consistent improvement across all earnings lines:

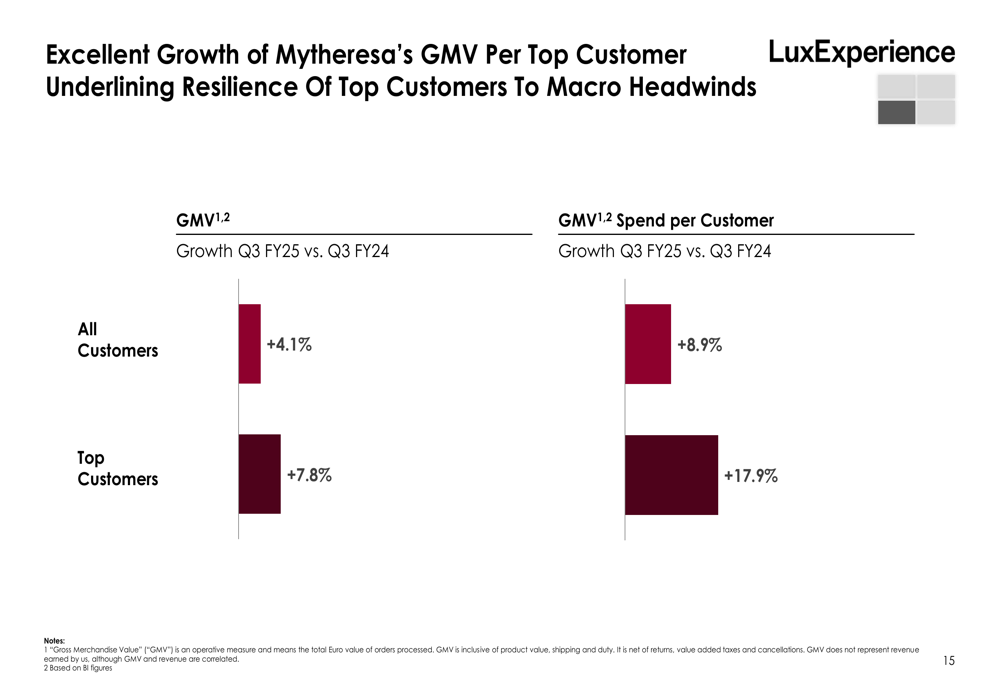

Particularly noteworthy is the strong performance among top customers, who demonstrated greater resilience to macroeconomic headwinds. GMV growth for top customers reached 7.8% in Q3 FY25 compared to 4.1% for all customers. Even more impressive, spend per customer increased by 17.9% for top customers versus 8.9% for all customers.

This trend is illustrated in the following chart:

Operational indicators also showed improvement, with Average Order Value (AOV) for womenswear increasing by 7.0% and return rates decreasing by 2.9 percentage points. These improvements helped offset a 20.2% increase in Customer Acquisition Cost (CAC), reflecting the more challenging customer acquisition environment.

Forward-Looking Statements

For the full fiscal year 2025, LuxExperience provided guidance for its legacy Mytheresa standalone business, projecting GMV and Net Sales growth at the lower end of its previously stated 7% to 13% range. The company expects an Adjusted EBITDA margin between 3% and 5%.

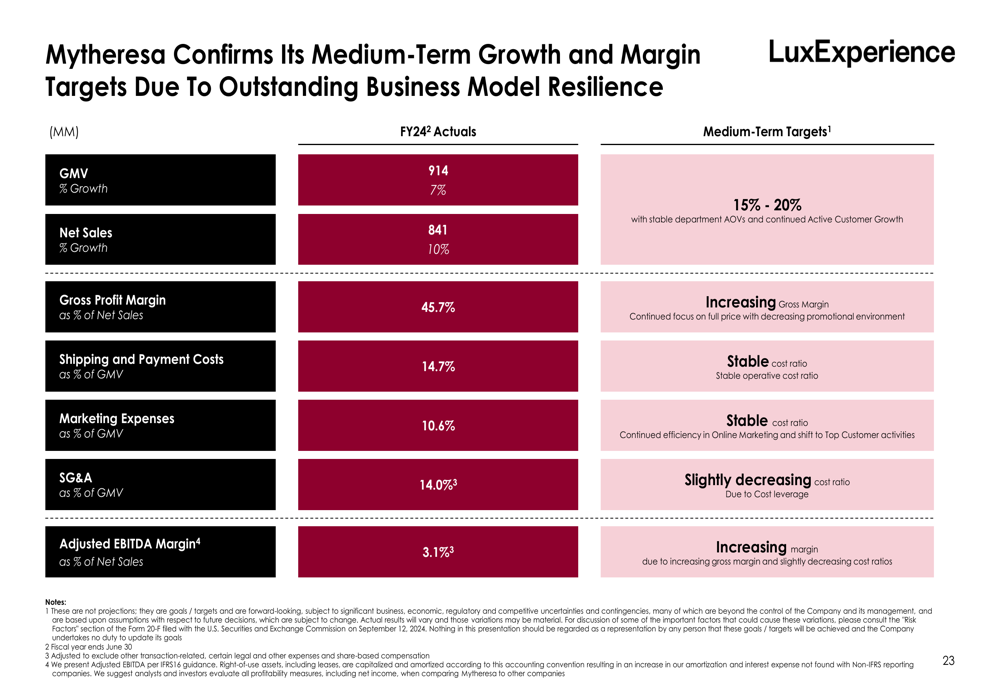

Looking further ahead, LuxExperience confirmed its medium-term ambitions following the YOOX NET-A-PORTER acquisition, targeting €4 billion in net sales and an adjusted EBITDA margin of 7% to 9%.

The company’s medium-term growth strategy and targets are outlined in the following chart:

Management noted that while the new tariff situation and its potential impact remain unclear, they expect to continue capturing market share with above-market growth in GMV and Net Sales. The company’s focus on high-value customers and exclusive experiences appears to be a cornerstone of this strategy, as these segments have demonstrated greater resilience to macroeconomic challenges.

Overall, LuxExperience’s Q3 FY25 presentation portrays a company successfully navigating a challenging luxury market environment while executing a significant acquisition and maintaining profitability across all earnings lines. The focus on high-value customers and exclusive experiences appears to be yielding results, particularly in terms of increased spending per customer and improved operational metrics.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.