5 big analyst AI moves: Apple lifted to Buy, AI chip bets reassessed

Introduction & Market Context

Matson , Inc. (NYSE:MATX) presented its second quarter 2025 earnings results on July 31, 2025, reporting performance that exceeded expectations despite ongoing market uncertainties. The shipping and logistics company navigated challenges in its China service while showing strength in domestic tradelanes, particularly Hawaii and Alaska.

The company’s stock closed at $106.50 on July 31, up 0.26% from the previous day’s close, reflecting cautious optimism about Matson’s ability to manage through global trade disruptions. This follows a significant drop after Q1 earnings when the stock fell 6.88% despite beating estimates, indicating persistent investor concerns about future performance.

Quarterly Performance Highlights

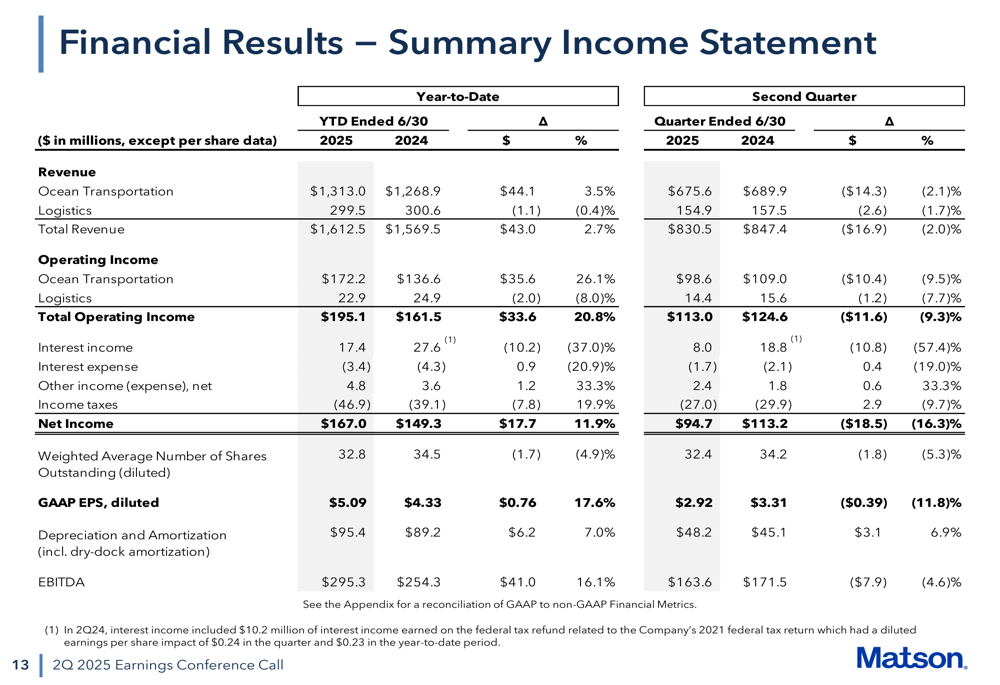

Matson reported total revenue of $830.5 million for Q2 2025, with consolidated operating income of $113.0 million and net income of $94.7 million. Diluted earnings per share reached $2.92, with EBITDA of $163.6 million.

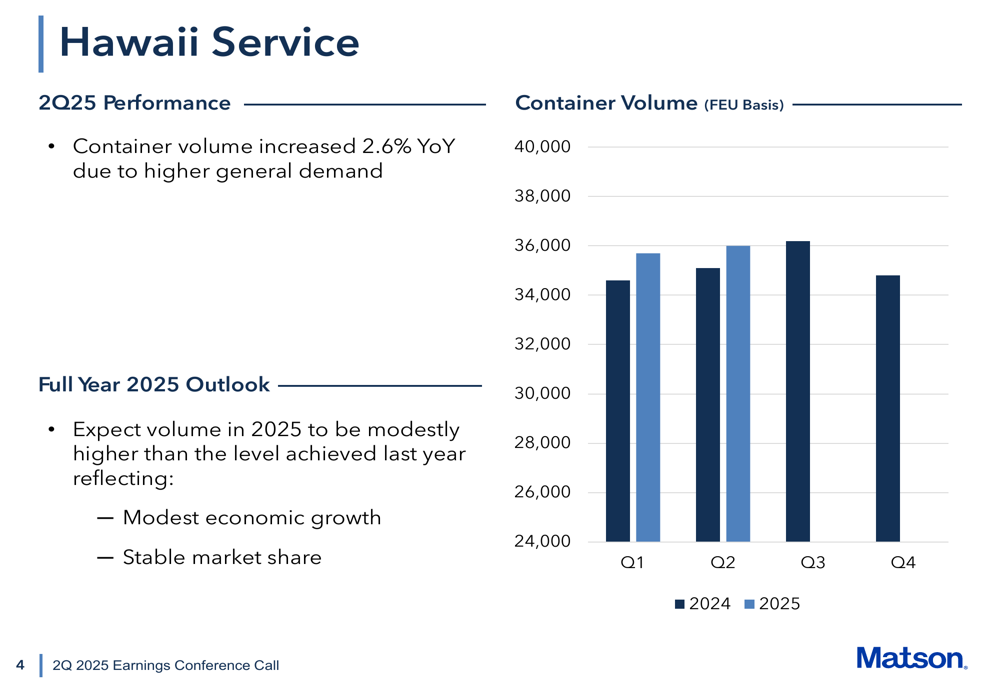

The company’s Hawaii service showed solid growth with container volume increasing 2.6% year-over-year due to higher general demand. The company expects this positive trend to continue through 2025.

As shown in the following chart of Hawaii container volumes:

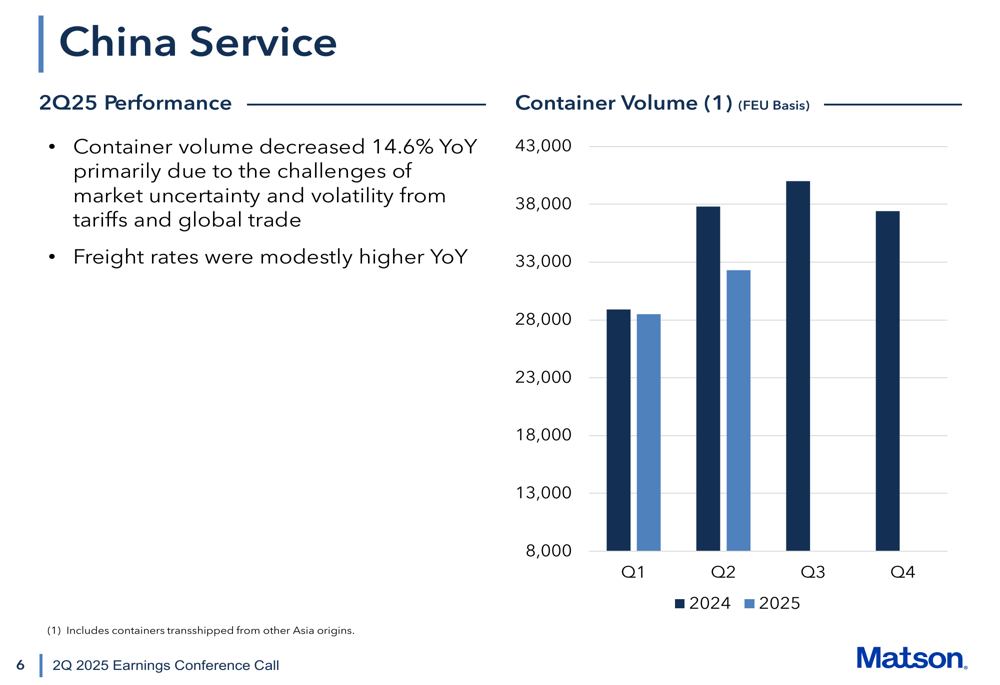

In contrast, China service experienced significant challenges with container volume decreasing 14.6% year-over-year, primarily due to market uncertainty from tariffs and global trade tensions. Despite these headwinds, freight rates were modestly higher compared to the same period last year.

The following chart illustrates the decline in China service container volume:

Matson’s management explained that at the onset of tariffs in April, freight demand decreased as customers held back shipments. A rebound occurred in mid-May after the U.S. and China agreed to temporary tariff reductions, and following the London meeting in June, volume stabilized modestly below prior year levels.

Alaska service showed resilience with container volume increasing 0.9% year-over-year, while Guam service experienced a slight decline of 2.2%.

Detailed Financial Analysis

The company’s summary income statement reveals the financial impact across its business segments:

Ocean Transportation, Matson’s largest segment, generated $675.6 million in revenue for Q2 2025 with operating income of $98.6 million. While still profitable, this represents a decrease from the previous year due to lower China service volume.

Logistics segment contributed $154.9 million in revenue with operating income of $14.4 million, a year-over-year decrease of approximately $1.2 million due to lower contribution from transportation brokerage.

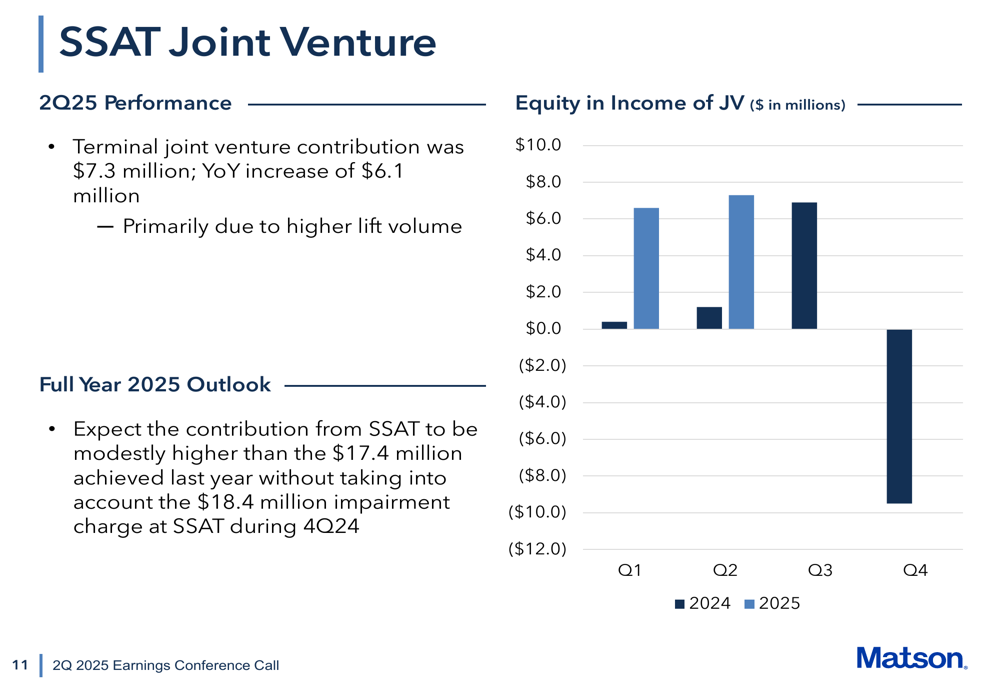

The SSAT terminal joint venture was a bright spot, with a contribution of $7.3 million, representing a year-over-year increase of $6.1 million primarily due to higher lift volume.

Matson maintained a strong balance sheet with total assets of $4,482.1 million as of June 30, 2025. The company continued its shareholder return program, repurchasing approximately 0.9 million shares for a total cost of $93.7 million in Q2 2025. Total (EPA:TTEF) debt decreased by $9.8 million from Q1 2025 to $381.0 million, and the company secured a new 5-year $550 million revolving credit facility on July 23, 2025.

Strategic Initiatives

Matson has been actively adapting to shifting trade patterns throughout Asia. The company highlighted its focus on supporting customers diversifying their manufacturing base beyond China. A notable development is the new expedited Ho Chi Minh service, which contributed to sequential quarterly volume increases.

Management emphasized Matson’s commitment to maintaining the fastest and most reliable Transpacific services, positioning the company to outperform the broader market despite challenging conditions. This service differentiation has allowed Matson to maintain relatively stable freight rates and volumes compared to competitors.

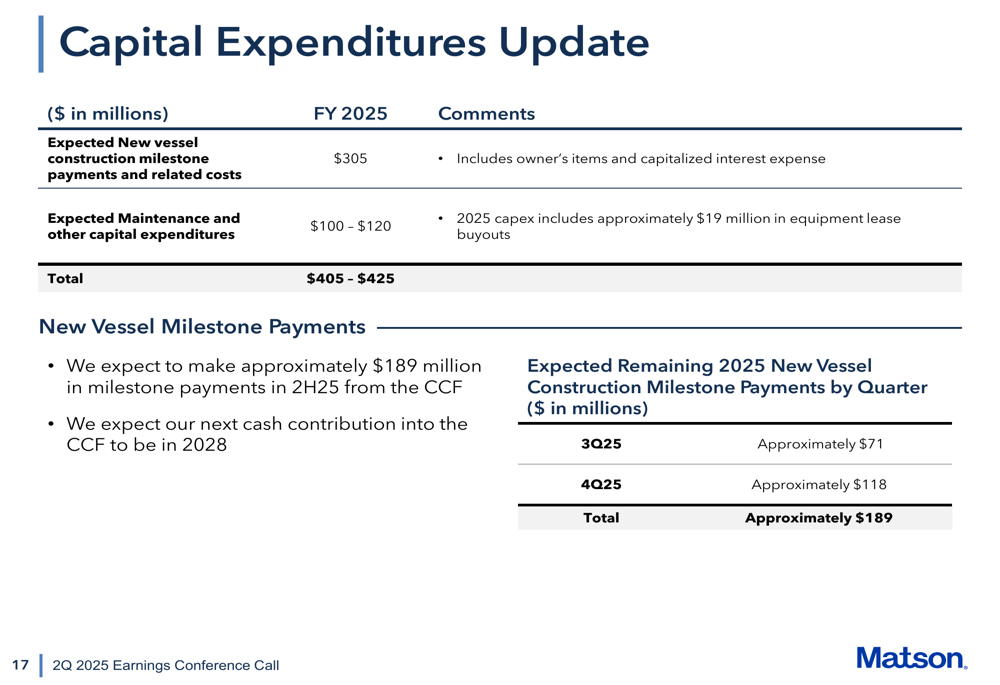

The company’s capital expenditure plans remain on track, with expected new vessel construction milestone payments of $305 million for FY 2025, plus maintenance and other capital expenditures of $100-120 million.

Forward-Looking Statements

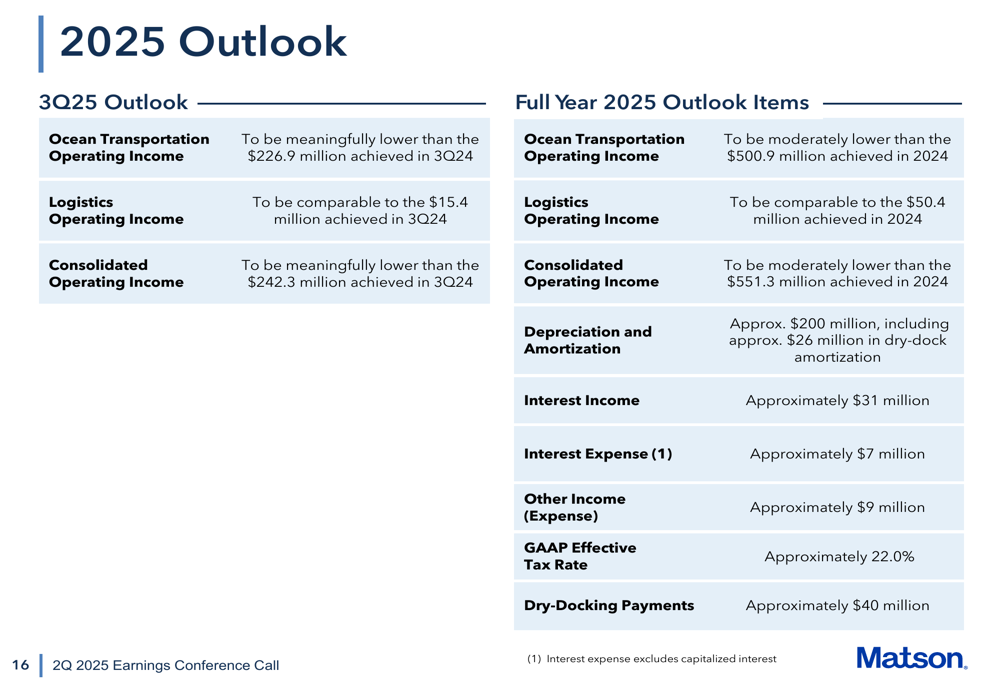

Matson provided a detailed outlook for the remainder of 2025, raising its full-year guidance based on Q2 performance while acknowledging continued uncertainties:

For Q3 2025, Matson expects Ocean Transportation operating income to be meaningfully lower than the $226.9 million achieved in Q3 2024. Logistics operating income is anticipated to be comparable to the $15.4 million achieved in the same period last year.

For the full year 2025, the company projects Ocean Transportation operating income to be moderately lower than the $500.9 million achieved in 2024, while Logistics operating income is expected to be comparable to the $50.4 million achieved last year.

The company maintains a cautious outlook regarding China service, expecting lower year-over-year freight rates and volume compared to 2024. However, management noted that volume and rates have stabilized in July, with Matson outperforming the broader market due to its service differentiation.

In domestic markets, Matson expects modest growth in Hawaii and Alaska volumes for the full year, supported by stable economic conditions in these regions. The Guam economy is expected to remain stable with a slow recovery in tourism, though volume is projected to be modestly lower than last year.

Despite the challenges, Matson appears well-positioned to navigate the uncertain trade environment while maintaining its financial strength and commitment to shareholder returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.