Moody’s downgrades Senegal to Caa1 amid rising debt concerns

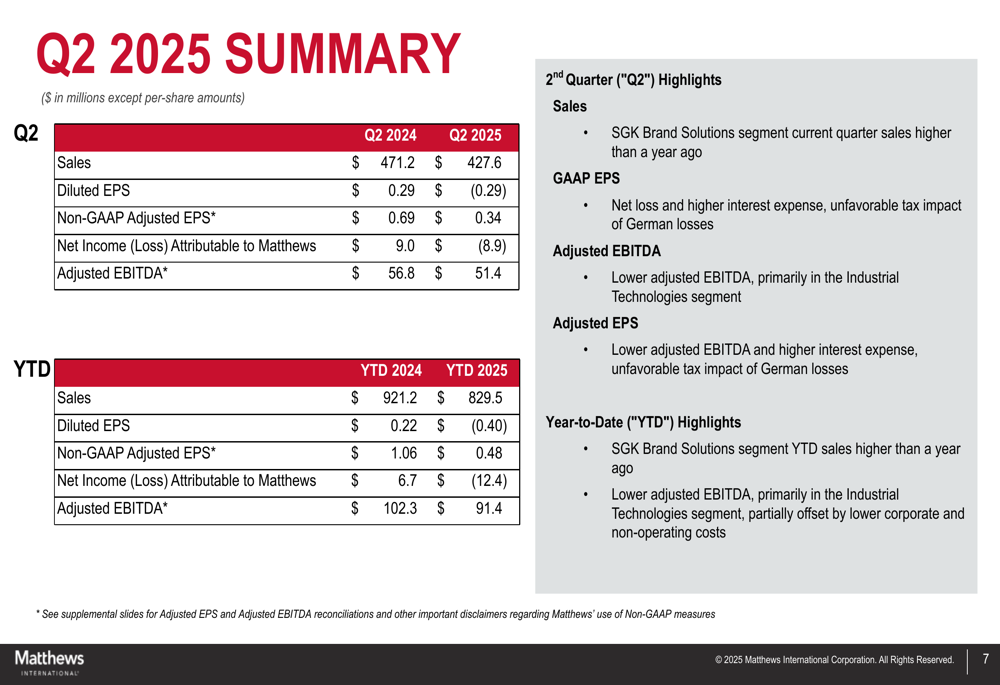

Matthews International Corporation (NASDAQ:MATW) reported a net loss of $8.9 million for its second quarter of fiscal 2025, a significant decline from the $9.0 million net income recorded in the same period last year. The company released its quarterly presentation on May 1, 2025, revealing mixed performance across business segments and highlighting upcoming strategic developments.

Executive Summary

Matthews International reported Q2 2025 sales of $427.6 million, down 9.3% from $471.2 million in Q2 2024. The company posted a GAAP loss per share of $0.29, compared to earnings per share of $0.29 in the prior-year quarter. Adjusted EBITDA decreased to $51.4 million from $56.8 million, primarily due to challenges in the Industrial Technologies segment.

The company’s stock has been under pressure, with shares closing at $21.48 on April 30, 2025, down 4.8% for the day. In after-hours trading, the stock fell an additional 1.3% to $20.18.

As shown in the following comprehensive financial summary:

Quarterly Performance Highlights

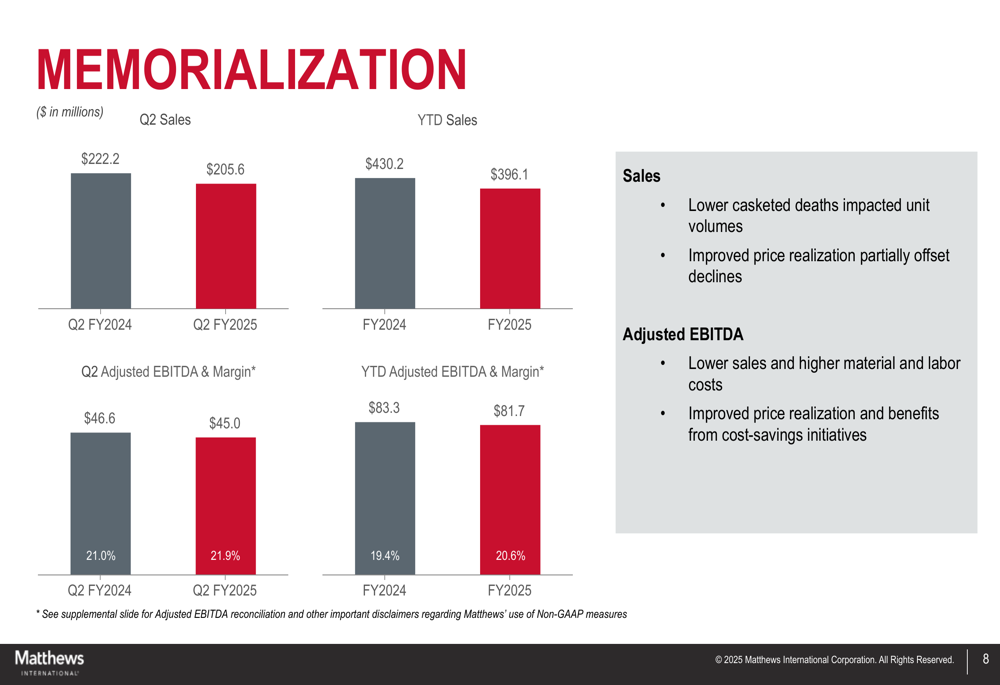

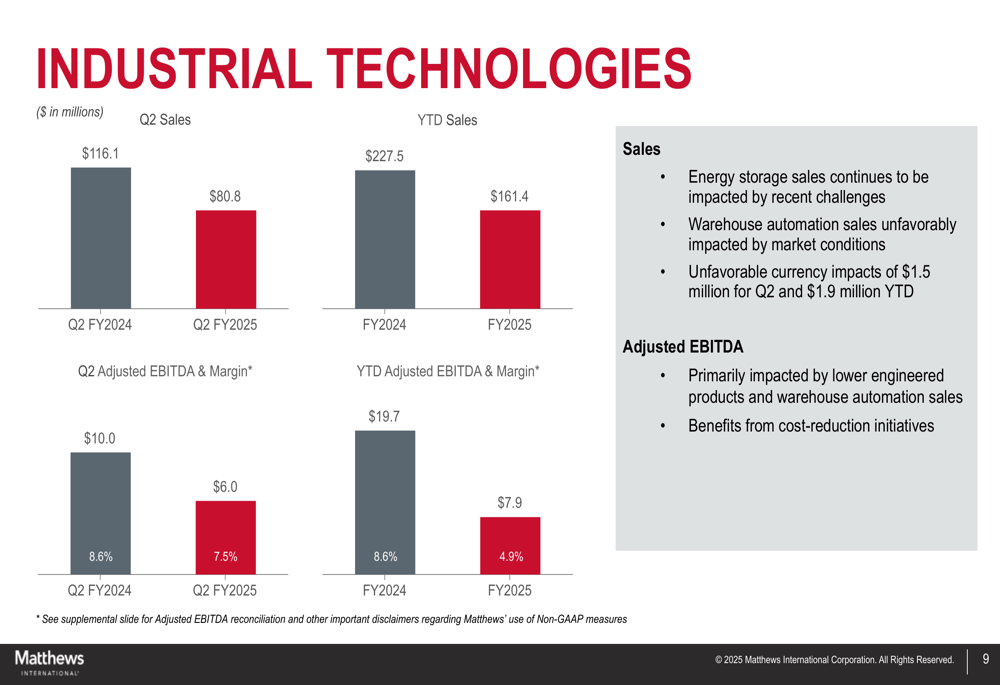

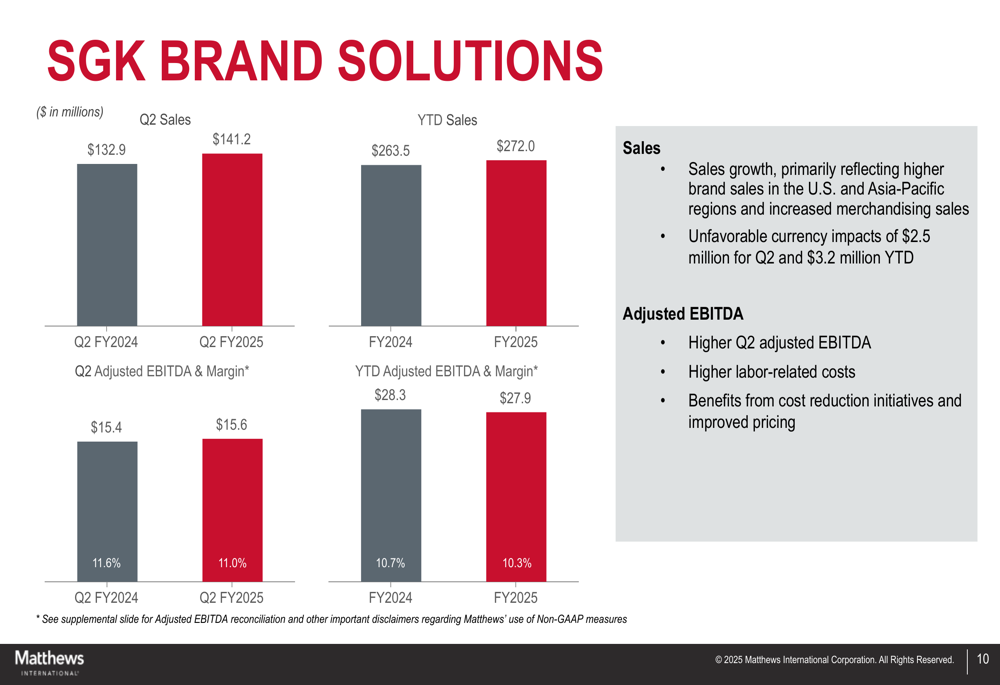

Matthews International’s performance varied significantly across its three business segments. The Memorialization segment, while experiencing lower sales, managed to improve its profit margins. The Industrial Technologies segment continued to face significant challenges, while SGK Brand Solutions showed modest growth.

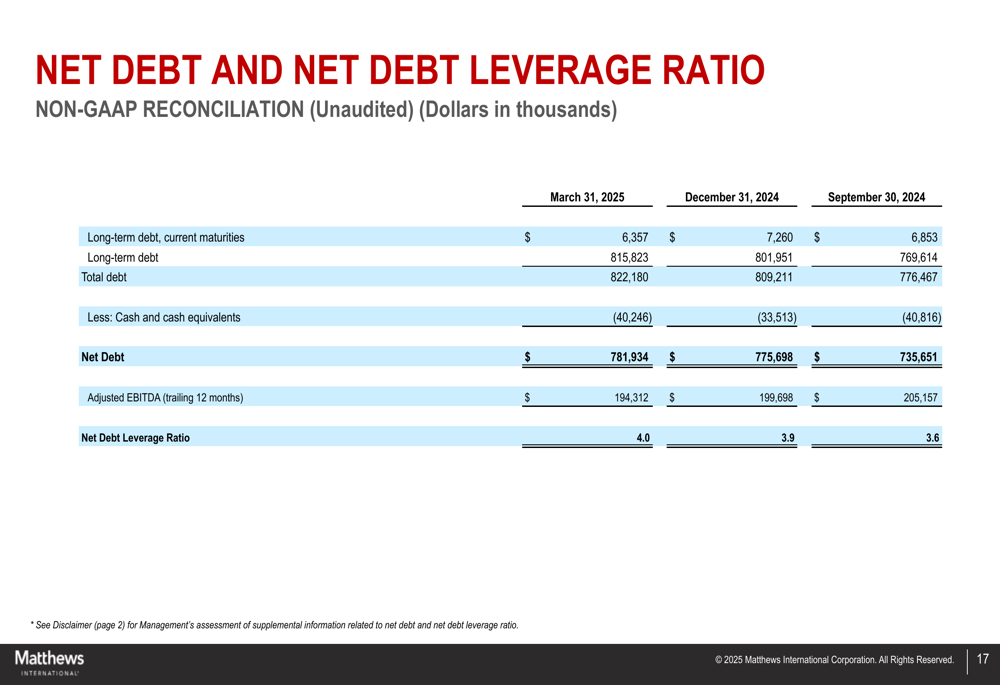

The company’s net debt increased to $781.9 million as of March 31, 2025, up from $735.7 million on September 30, 2024. This pushed the net debt leverage ratio to 4.0, compared to 3.6 six months earlier. Operating cash flow for the first half of fiscal 2025 was negative at $(18.7) million, a substantial decline from the positive $29.8 million reported in the same period last year.

Joseph C. Bartolacci, President and CEO, emphasized that Q2 cash flows reflected costs related to the SGK transaction, contested proxy, and restructuring actions. Despite these challenges, the company maintained its quarterly dividend of $0.25 per share, payable on May 26, 2025.

Segment Analysis

The Memorialization segment, which includes caskets, memorials, and cremation equipment, reported Q2 sales of $205.6 million, down from $222.2 million in Q2 2024. Despite the sales decline, adjusted EBITDA margin improved to 21.9% from 21.0% a year ago, reflecting successful cost reduction initiatives and improved price realization.

As shown in the following segment performance breakdown:

The Industrial Technologies segment faced the most significant challenges, with Q2 sales falling to $80.8 million from $116.1 million in Q2 2024. Adjusted EBITDA margin declined to 7.5% from 8.6%. The company cited ongoing impacts from the Tesla (NASDAQ:TSLA) litigation and challenging market conditions in warehouse automation as key factors affecting performance.

The detailed performance of the Industrial Technologies segment is illustrated below:

In contrast, the SGK Brand Solutions segment showed improvement with Q2 sales increasing to $141.2 million from $132.9 million in Q2 2024. While adjusted EBITDA margin decreased slightly to 11.0% from 11.6%, absolute adjusted EBITDA increased to $15.6 million from $15.4 million, reflecting higher brand sales in the U.S. and Asia-Pacific regions and increased merchandising sales.

The following chart details the SGK Brand Solutions segment performance:

Financial Position and Debt

Matthews International’s financial position showed some deterioration during the quarter. Total (EPA:TTEF) debt increased to $822.2 million as of March 31, 2025, from $776.5 million on September 30, 2024. Cash and cash equivalents remained relatively stable at $40.2 million.

The company’s net debt leverage ratio increased to 4.0, raising potential concerns about financial flexibility. This represents a significant change from the previous earnings call, where the company had reported debt reduction of over $50 million.

The following chart illustrates the company’s debt position and leverage ratio:

Operating cash flow for the first half of fiscal 2025 was negative at $(18.7) million, compared to positive $29.8 million in the same period last year. The company attributed this decline to costs related to the SGK transaction, contested proxy, and restructuring actions.

Forward-Looking Statements

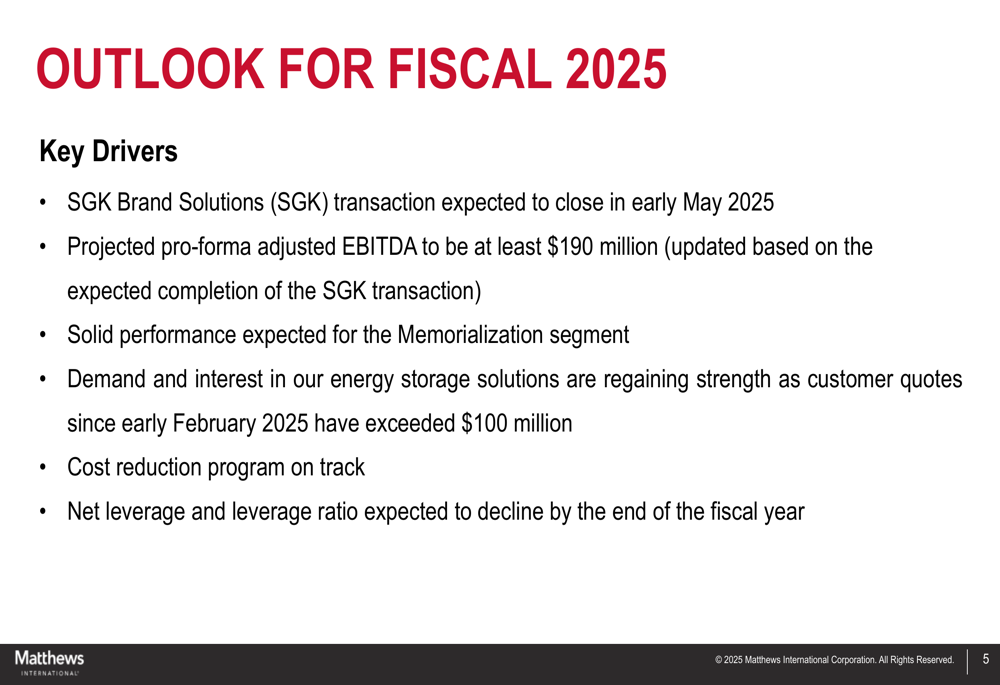

Despite current challenges, Matthews International maintained an optimistic outlook for the remainder of fiscal 2025. The company expects the SGK Brand Solutions transaction to close in early May 2025 and has updated its projected pro-forma adjusted EBITDA to be at least $190 million for fiscal 2025.

This represents a downward revision from the previous guidance of $205-$215 million mentioned in the fiscal 2024 earnings call, likely reflecting the ongoing challenges in the Industrial Technologies segment.

The company highlighted encouraging signs in its energy storage solutions business, noting that customer quotes since early February 2025 have exceeded $100 million. Management expressed confidence that demand and interest in energy storage solutions are regaining strength.

As shown in the following outlook summary:

Matthews International also emphasized that its cost reduction program remains on track, and it expects net leverage and leverage ratio to decline by the end of the fiscal year, which would represent a reversal of the current trend.

The Memorialization segment is expected to continue its solid performance, benefiting from ongoing productivity and cost reduction initiatives. The company also anticipates improved market conditions for the SGK Brand Solutions segment, particularly in merchandising sales.

While challenges persist, particularly in the Industrial Technologies segment and with ongoing litigation, Matthews International’s management remains focused on strategic initiatives to improve performance and reduce leverage as it moves through the remainder of fiscal 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.